| Study Period | 2017 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 197.1 Billion |

| Market Size (2030) | USD 304.7 Billion |

| CAGR (2025 - 2030) | 9.10 % |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

LEO Satellite Market Analysis

The LEO Satellite Market size is estimated at 197.1 billion USD in 2025, and is expected to reach 304.7 billion USD by 2030, growing at a CAGR of 9.10% during the forecast period (2025-2030).

The LEO satellite industry is experiencing unprecedented transformation driven by technological advancements and increasing commercial space activities. The sector has witnessed remarkable growth in satellite deployments, with over 4,100 satellites launched during 2017-2022, demonstrating the industry's rapid expansion. Private LEO companies are leading innovation in satellite technology, with developments in miniaturization, cost-effective manufacturing techniques, and improved launch capabilities making space more accessible than ever. The emergence of reusable launch vehicles and advanced manufacturing processes has significantly reduced launch costs, enabling more organizations to participate in space activities.

The telecommunications sector continues to drive significant developments in the LEO satellite market, particularly in global internet connectivity initiatives. SpaceX's Starlink program exemplifies this trend, with over 250,000 user terminals currently in operation, highlighting the growing consumer adoption of satellite-based internet services. In December 2022, SpaceX received FCC approval to launch 7,500 satellites as part of its Gen2 Starlink constellation, demonstrating the ongoing expansion of satellite internet infrastructure. These developments are reshaping global connectivity patterns and creating new opportunities for remote and underserved regions.

Propulsion technology innovations are revolutionizing satellite capabilities and operational efficiency. In April 2023, Dawn Aerospace secured a contract with the German Aerospace Center to enhance the performance of nitrous-oxide-based green propellant for satellites, representing a significant shift toward environmentally sustainable space operations. Electric propulsion systems, including ion and Hall-effect thrusters, are gaining prominence due to their superior fuel efficiency and extended mission capabilities, particularly in large-scale constellation deployments.

International collaboration and competition are intensifying in the LEO satellite sector, with multiple nations advancing their space capabilities. China's announcement in March 2023 to launch a mega constellation of 13,000 satellites weighing 190 kg each demonstrates the scale of national space ambitions. The European Space Agency is developing new navigation satellites with enhanced positioning capabilities, while private companies continue to forge partnerships for technological advancement. These developments are occurring against a backdrop of increasing global military expenditure, which reached $2,240 billion in 2022, influencing satellite technology development and deployment strategies.

Global LEO Satellite Market Trends

The trend for better fuel and operational efficiency is expected to positively impact the market

- The success of a satellite mission is highly dependent on the accuracy of measuring its mass properties before the flight and the proper ballasting of the satellite to bring the mass properties within tight limits. Failure to properly control mass properties can result in the satellite tumbling end over end after launch or quickly using up its thruster capacity in an attempt to point in the correct direction. Solar panels must continue to point toward the sun as the satellite orbits the Earth.

- Low earth orbit satellites orbit from 160 to 2000 km above the Earth, take approximately 1.5 hours for a full orbit, and only cover a portion of the Earth’s surface. The mass of a satellite has a significant impact on the launch of the satellite. This is because the heavier the satellite, the more fuel and energy are required to launch it into space. Launching a satellite involves accelerating it to a very high speed, typically around 28,000 km per hour, to place it in orbit around the Earth. The amount of energy required to achieve this speed is proportional to the mass of the satellite.

- As a result, a heavier satellite requires a larger rocket and more fuel to launch it into space. This, in turn, increases the cost of the launch and can also limit the types of launch vehicles that can be used. The major classification types according to mass are large satellites that are more than 1,000 kg. During 2017-2022, 65+ large satellites were launched in the LEO orbit. A medium-sized satellite has a mass of 500 and 1000 kg, and 250+ medium-sized satellites were launched. Satellites with a launch mass of less than 500 kg are small satellites. There are 4000+ small satellites in the LEO orbit.

-by-region,-Number-of-Satellites-Launched,-Global,-2017---2022.svg)

Understand The Key Trends Shaping This Market

Download PDF

Growing demand for earth observation, imaging, and connectivity services is expected to surge the research and development expenditure in LEO satellites category

- Low Earth orbit (LEO) is an orbit relatively closer to the surface of the Earth. LEO is usually below 1000 km altitude but can be as high as 160 km above Earth. LEO satellites are widely used for communications, military reconnaissance, and other imaging applications. Communications satellites have the advantage of short signal runtimes to LEO. This reduction in propagation delay results in lower latency. Most satellites sent into space are in the LEO constellation. One of the major LEO satellite constellations is owned by satellite communications provider Iridium. The competitive rivalry in the LEO orbit globally is high as companies such as Amazon-owned Kuiper Systems want to compete with companies like OneWeb's Starlink to provide broadband connectivity from space. After Federal Communications Commission approval, the company plans to launch its first satellite to be launched in 2023.

- Considering the increase in space-related activities in the Asia-Pacific region, satellite manufacturers are enhancing their satellite production capabilities. The prominent Asia-Pacific countries with robust space infrastructure are China, India, Japan, and South Korea. China National Space Administration announced space exploration priorities for 2021–2025, including enhancing national civil space infrastructure facilities. As a part of this plan, the Chinese government established China Satellite Network Group Co. Ltd to develop a 13,000-satellite constellation for satellite internet. Overall, the trend in R&D expenditure on LEO satellites is an increase, driven by the need for innovation and government funding. This investment is expected to lead to the development of new technologies that will improve the performance and capabilities of LEO satellites.

Segment Analysis: Application

Communication Segment in LEO Satellite Market

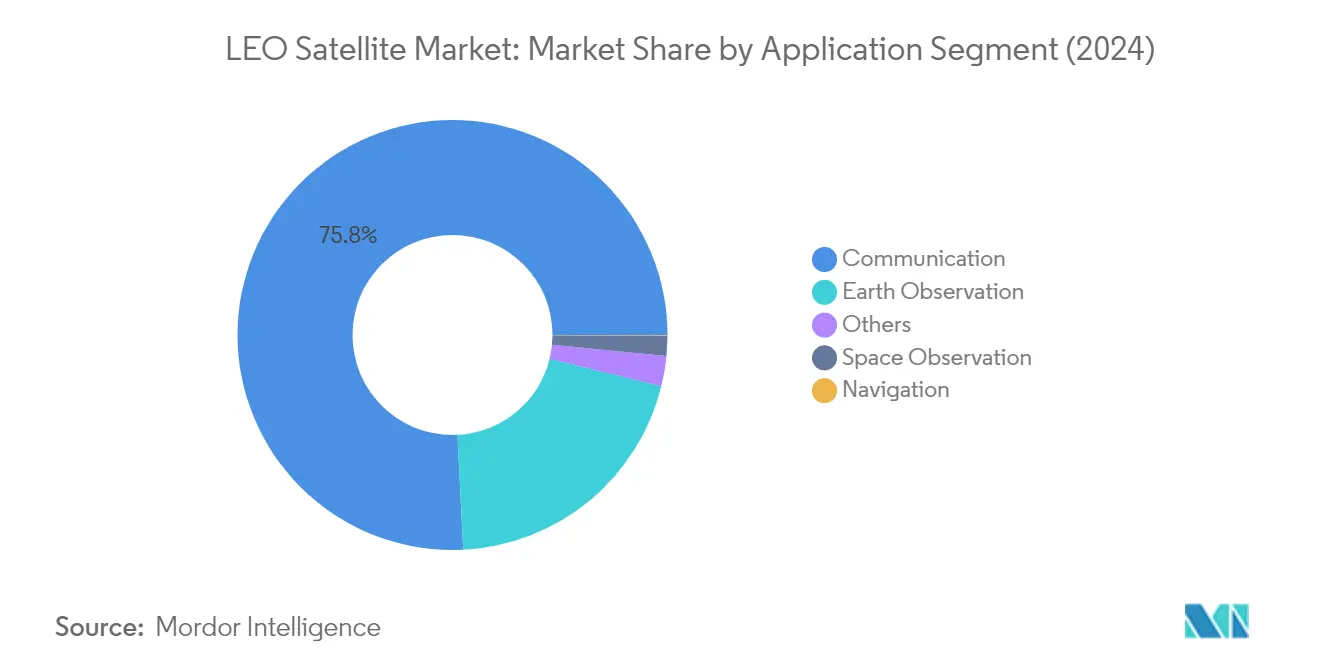

The communication segment dominates the global LEO satellite market, accounting for approximately 76% of the total market share in 2024. This significant market position is primarily driven by the increasing global demand for high-speed internet connectivity and advanced communication services. Major players like SpaceX's Starlink and OneWeb are actively deploying large constellations of communication satellites to create comprehensive global broadband networks. The segment's growth is further supported by the rising need for reliable connectivity in remote and underserved regions, maritime communications, and emergency response systems. The deployment of next-generation satellite constellations is enabling improved data transmission speeds, lower latency, and enhanced coverage capabilities, making low Earth orbit satellites increasingly attractive for telecommunications applications.

Navigation Segment in LEO Satellite Market

The navigation segment is emerging as the fastest-growing segment in the LEO satellite market, with a projected growth rate of approximately 28% during 2024-2029. This remarkable growth is driven by increasing applications in autonomous vehicles, precision agriculture, and advanced positioning services. The segment is witnessing substantial investments from both commercial entities and government organizations to develop more accurate and reliable navigation systems. The integration of LEO satellites in navigation applications is revolutionizing traditional GPS services by providing enhanced accuracy, reduced signal latency, and improved coverage in urban and remote areas. The development of multi-layer satellite navigation systems and the incorporation of advanced technologies are further accelerating the segment's growth trajectory.

Remaining Segments in Application

The remaining segments in the LEO satellite market include Earth observation, space observation, and other specialized applications. Earth observation satellites play a crucial role in environmental monitoring, disaster management, and urban planning, offering high-resolution imagery and real-time data collection capabilities. The space observation segment focuses on astronomical research, space weather monitoring, and debris tracking, contributing to scientific advancement and space safety. Other applications encompass technology demonstration missions, scientific research, and specialized commercial services, each serving unique market needs and contributing to the overall ecosystem of LEO satellite applications.

Segment Analysis: Satellite Mass

100-500kg Segment in LEO Satellite Market

The 100-500kg satellite segment dominates the global LEO satellite market, commanding approximately 76% of the total market share in 2024. This significant market position is primarily driven by the segment's versatility in supporting various applications, including Earth observation, remote sensing, climate monitoring, maritime surveillance, and communication services. The segment's dominance is further reinforced by major satellite constellation deployments from leading companies, particularly in the communications sector. These minisatellites offer an optimal balance between payload capacity and cost-effectiveness, making them particularly attractive for commercial applications. The China Academy of Space Technology (CAST) has announced plans to launch a mega constellation of satellites weighing 190 kg each for broadband applications, demonstrating the continued preference for this weight class in large-scale deployments.

Below 10kg Segment in LEO Satellite Market

The Below 10kg satellite segment is emerging as the fastest-growing segment in the LEO satellite market, with a projected growth rate of approximately 19% from 2024 to 2029. This remarkable growth is driven by increasing adoption of nanosatellites and CubeSats for various commercial and research applications. The segment's rapid expansion is fueled by technological advancements in miniaturization, reduced launch costs, and growing demand for small satellite constellations. These lightweight satellites are particularly attractive to academic institutions, startups, and research organizations due to their cost-effectiveness and shorter development cycles. The segment is witnessing increased investment in Earth observation applications, with companies like Planet Labs manufacturing and launching multiple small satellites to provide high-resolution imagery and data collection capabilities.

Remaining Segments in Satellite Mass

The remaining segments in the LEO satellite market include the 10-100kg, 500-1000kg, and above 1000kg categories, each serving distinct market needs. The 10-100kg segment caters to microsatellite applications, offering a balance between capability and cost. The 500-1000kg segment typically serves medium-sized satellites designed for more complex missions requiring higher power and larger payloads. The above 1000kg segment focuses on heavy-class satellites that support advanced communication systems, high-resolution imaging, and sophisticated scientific research missions. These segments complement each other in the market, providing options for various mission requirements and operational needs across different industries and applications.

Segment Analysis: End User

Commercial Segment in LEO Satellite Market

The commercial segment dominates the global LEO satellite market, accounting for approximately 78% of the total market value in 2024, driven by the increasing demand for satellite-based services across various industries. This segment's prominence is largely attributed to major players like SpaceX's Starlink, OneWeb, and Amazon's Project Kuiper, who are actively deploying large constellations of low Earth orbit satellites to create global broadband networks. The segment is also expected to maintain its leading position with the fastest growth rate of around 11% during 2024-2029, fueled by increasing investments in satellite manufacturing, launch capabilities, and ground infrastructure. The growth is further supported by the rising demand for high-speed internet connectivity in both urban and rural areas, with companies focusing on bridging the digital divide through reliable and affordable broadband services. Commercial applications span across multiple sectors including telecommunications, Earth observation, remote sensing, and data analytics services, making it the most diverse and economically significant segment in the market.

Remaining Segments in End User Segmentation

The military and government segment represents a significant portion of the LEO satellite market, driven by increasing defense spending and the growing importance of space-based assets for national security. This segment encompasses various applications including military reconnaissance, surveillance, communication systems, and weather monitoring capabilities essential for defense operations. The military and government sector continues to invest in advanced satellite technologies to enhance situational awareness, improve communication infrastructure, and strengthen defense capabilities. The 'Other' segment, which includes academic institutions, research organizations, and non-governmental entities, plays a crucial role in technological innovation and scientific research. These organizations contribute to the advancement of satellite technology through experimental missions, educational initiatives, and specialized research projects, though their market impact remains relatively smaller compared to commercial and military applications.

Segment Analysis: Propulsion Tech

Liquid Fuel Segment in LEO Satellite Market

The liquid fuel propulsion segment dominates the LEO satellite market, commanding approximately 73% market share in 2024. This significant market position is attributed to the segment's superior performance characteristics, including higher specific impulses compared to other propulsion technologies, resulting in greater efficiency and longer satellite lifespans. Liquid propulsion systems offer satellite operators precise thrust control and throttling capabilities, enabling optimized maneuvers and efficient fuel usage for extended mission durations and orbital adjustments. Major space agencies and commercial operators prefer liquid propulsion systems due to their reliability and proven track record in various space missions. The segment's growth is further supported by ongoing technological advancements focused on developing more efficient and environmentally friendly propellants, as well as innovations in propulsion system design that aim to reduce manufacturing costs while maintaining high performance standards.

Gas Based Segment in LEO Satellite Market

The gas-based propulsion segment is emerging as the fastest-growing segment in the LEO satellite market, with projections indicating robust growth of approximately 14% from 2024 to 2029. This remarkable growth is driven by the increasing adoption of cold gas propulsion technology, which offers significant advantages for small satellite applications. The segment's expansion is supported by ongoing innovations in gas propulsion systems, particularly in the development of more efficient cold gas thrusters and the integration of advanced control systems. Companies are increasingly investing in research and development to enhance the performance of gas-based propulsion systems, focusing on improving thrust efficiency and developing more sophisticated control mechanisms. The growth is further accelerated by the rising demand for precise attitude control in small satellites and the increasing preference for environmentally friendly propulsion solutions in the space industry.

Remaining Segments in Propulsion Tech

The electric propulsion segment represents another significant technology in the LEO satellite market, offering unique advantages for specific mission profiles. Electric propulsion systems, including ion thrusters and Hall-effect thrusters, are particularly valuable for missions requiring long-term station-keeping and precise orbital adjustments. These systems excel in providing high specific impulse and efficient propellant utilization, making them ideal for extended-duration missions. The technology continues to evolve with improvements in power efficiency and thrust capabilities, supported by ongoing research and development efforts from both established aerospace companies and innovative startups. Electric propulsion systems are increasingly being integrated into modern satellite designs, particularly in cases where precise orbital maintenance and long operational lifetimes are primary requirements.

LEO Satellite Market Geography Segment Analysis

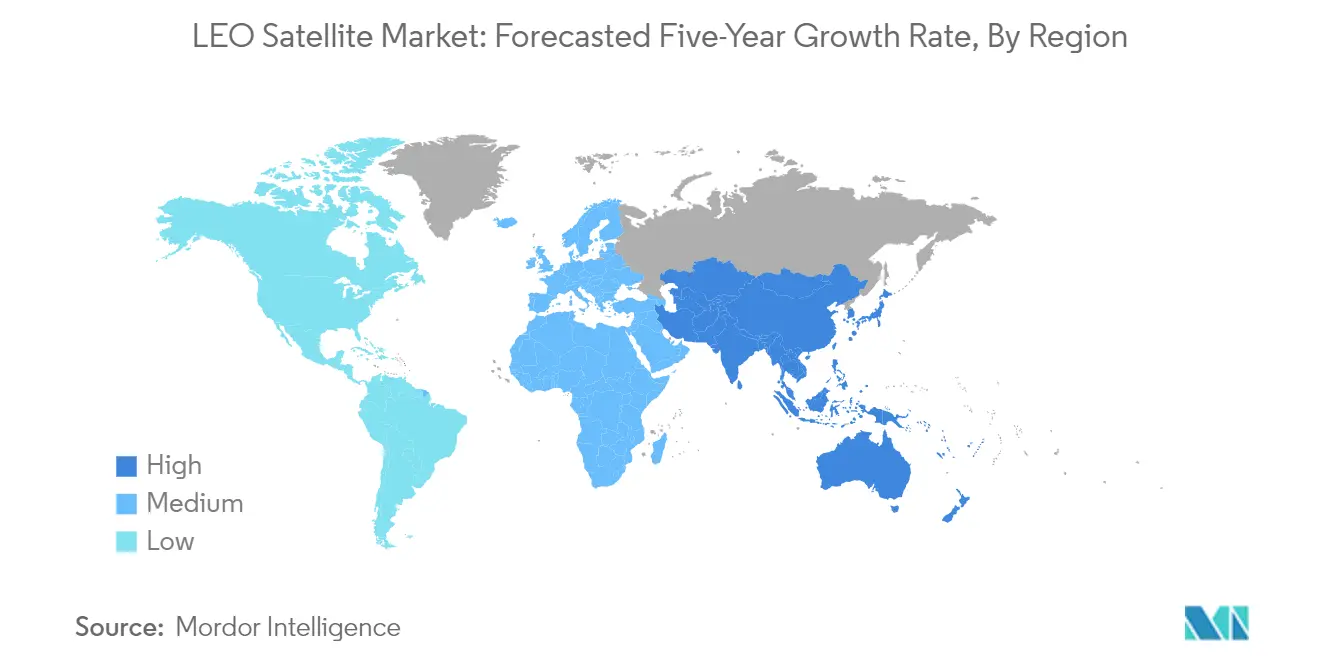

LEO Satellite Market in Asia-Pacific

The Asia-Pacific region represents approximately 4% of the global LEO satellite market in 2024, showcasing its emerging position in the space industry. The region's market is primarily driven by ambitious space programs from major economies like China, Japan, and India. These countries are actively developing and deploying satellites for various applications, including Earth observation, communication, and scientific research. The technological capabilities in the region continue to advance, with significant investments in research and development facilities. Local manufacturers are increasingly developing indigenous satellite manufacturing capabilities, reducing dependence on international suppliers. The region's universities and research institutions are also playing a crucial role in developing next-generation satellite technologies. Private sector participation has been growing, with numerous startups entering the LEO market. The market is further supported by strong government backing and favorable regulatory environments in several countries. Regional cooperation in space activities has also been strengthening, with various collaborative projects and knowledge-sharing initiatives among countries.

LEO Satellite Market in Europe

The European LEO satellite market has demonstrated remarkable growth, recording approximately 60% growth from 2019 to 2024, establishing itself as a significant player in the global space industry. The region's success is built upon its strong aerospace manufacturing base and advanced technological capabilities. The European Space Agency (ESA) continues to play a pivotal role in coordinating space activities across member states and fostering innovation in satellite technology. The region benefits from a well-established ecosystem of satellite manufacturers, launch service providers, and ground segment operators. European companies are particularly strong in Earth observation satellites and telecommunications systems. The market is characterized by strong collaboration between academic institutions, research centers, and private companies. Public-private partnerships have become increasingly common, driving innovation and commercial applications. The region's regulatory framework supports sustainable space activities while promoting commercial opportunities. European countries are actively working on reducing space debris and promoting responsible space operations.

LEO Satellite Market in North America

The North American LEO satellite market is projected to grow at approximately 9% during the period 2024-2029, maintaining its position as the largest regional market globally. The region's dominance is underpinned by its advanced technological infrastructure and strong presence of major aerospace companies. The market benefits from substantial private sector investments and innovative business models in the commercial space sector. A robust ecosystem of suppliers, manufacturers, and service providers supports the industry's growth. The region leads in developing new applications for low Earth orbit satellites, particularly in communications and Earth observation. Universities and research institutions contribute significantly to technological advancement and workforce development. The regulatory environment continues to evolve to support commercial space activities while ensuring safety and security. Strong government support through various space programs and initiatives provides stability to the market. The region's emphasis on developing reusable launch vehicles has significantly reduced launch costs.

Get Analysis on Important Geographic Markets

Download PDF

LEO Satellite Industry Overview

Top Companies in LEO Satellite Market

The LEO satellite market is characterized by intense innovation and strategic developments among key players. Companies are heavily investing in research and development to enhance satellite capabilities, particularly focusing on communication services, Earth observation, and navigation applications. Operational agility is demonstrated through rapid satellite deployment capabilities and the establishment of manufacturing facilities across strategic locations. Market leaders are pursuing vertical integration strategies, developing in-house launch capabilities while simultaneously maintaining partnerships with launch service providers. Geographic expansion remains a key focus, with LEO companies establishing ground stations and operational centers worldwide to ensure comprehensive coverage. Product portfolios are being diversified to address emerging applications in sectors such as agriculture, maritime, and urban planning, while strategic collaborations with technology providers enhance service offerings.

Consolidated Market with Strong Global Players

The LEO satellite market exhibits a highly consolidated structure dominated by established global aerospace and defense conglomerates alongside specialized LEO satellite companies. These major players leverage their extensive technological expertise, manufacturing capabilities, and established relationships with government agencies to maintain market leadership. The market demonstrates significant barriers to entry due to high capital requirements, complex regulatory frameworks, and the need for specialized technical expertise. Merger and acquisition activities are primarily focused on acquiring innovative technologies and expanding service capabilities, with larger companies actively pursuing smaller firms with unique technological solutions or market access.

The competitive dynamics are further shaped by the presence of government-backed enterprises and private commercial entities, creating a complex ecosystem of collaboration and competition. Regional players, particularly in Asia-Pacific and Europe, are gaining prominence through government support and strategic partnerships with global leaders. The market structure encourages long-term relationships between manufacturers and customers, with multi-year contracts and ongoing service agreements being common practice. Vertical integration trends are evident as companies seek to control critical components of the value chain, from manufacturing to launch services and ground operations.

Innovation and Integration Drive Future Success

Success in the LEO market increasingly depends on technological innovation, cost efficiency, and service reliability. Incumbent players must focus on developing next-generation satellite technologies while optimizing manufacturing processes to reduce costs and improve deployment speeds. Strategic partnerships with ground segment operators and data analytics providers are becoming crucial for delivering comprehensive solutions. Companies need to invest in advanced manufacturing capabilities, including automation and additive manufacturing, while maintaining strong relationships with key stakeholders in government and commercial sectors. The ability to offer integrated solutions that combine satellite hardware, communication services, and data analytics will become increasingly important for maintaining market position.

For emerging players and contenders, success lies in identifying and exploiting niche market segments while building strategic partnerships to overcome infrastructure limitations. Focus areas should include developing specialized applications for specific industries, offering innovative service models, and leveraging new technologies to reduce operational costs. Regulatory compliance and certification capabilities will become increasingly important as space traffic management concerns grow. Companies must also consider environmental sustainability in their operations, including debris mitigation strategies and end-of-life management solutions. The ability to adapt to evolving customer needs while maintaining cost competitiveness will be crucial for long-term success in this dynamic market.

LEO Satellite Market Leaders

-

Airbus SE

-

China Aerospace Science and Technology Corporation (CASC)

-

Lockheed Martin Corporation

-

ROSCOSMOS

-

Space Exploration Technologies Corp.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

LEO Satellite Market News

- February 2024: SpaceX launches 23 Leap Day Starlink satellites into orbit with the help of SpaceX Falcon 9 rocket.The company is planning to have 42,000 satellites in LEO orbit.

- February 2024: The company has launched a group of 21 Starlink satellites into orbit using Falcon 9 rocket. The launch happened at Vandenberg Space Force Base in California

- February 2024: SpaceX is planning to remove around 100 old Starlink satellites from the orbit because of a design flaw that could cause them to fail.

Free With This Report

We offer a comprehensive set of global and local metrics that illustrate the fundamentals of the satellites industry. Clients can access in-depth market analysis of various satellites and launch vehicles through granular level segmental information supported by a repository of market data, trends, and expert analysis. Data and analysis on satellite launches, satellite mass, application of satellites, spending on space programs, propulsion systems, end users, etc., are available in the form of comprehensive reports as well as excel based data worksheets.

LEO Satellite Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

- 4.1 Satellite Mass

- 4.2 Spending On Space Programs

-

4.3 Regulatory Framework

- 4.3.1 Global

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 China

- 4.3.6 France

- 4.3.7 Germany

- 4.3.8 India

- 4.3.9 Iran

- 4.3.10 Japan

- 4.3.11 New Zealand

- 4.3.12 Russia

- 4.3.13 Singapore

- 4.3.14 South Korea

- 4.3.15 United Arab Emirates

- 4.3.16 United Kingdom

- 4.3.17 United States

- 4.4 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

-

5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

-

5.2 Satellite Mass

- 5.2.1 10-100kg

- 5.2.2 100-500kg

- 5.2.3 500-1000kg

- 5.2.4 Below 10 Kg

- 5.2.5 above 1000kg

-

5.3 End User

- 5.3.1 Commercial

- 5.3.2 Military & Government

- 5.3.3 Other

-

5.4 Propulsion Tech

- 5.4.1 Electric

- 5.4.2 Gas based

- 5.4.3 Liquid Fuel

-

5.5 Region

- 5.5.1 Asia-Pacific

- 5.5.2 Europe

- 5.5.3 North America

- 5.5.4 Rest of World

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Airbus SE

- 6.4.2 Astrocast

- 6.4.3 China Aerospace Science and Technology Corporation (CASC)

- 6.4.4 German Orbital Systems

- 6.4.5 GomSpaceApS

- 6.4.6 Lockheed Martin Corporation

- 6.4.7 Nano Avionics

- 6.4.8 Planet Labs Inc.

- 6.4.9 ROSCOSMOS

- 6.4.10 Space Exploration Technologies Corp.

- 6.4.11 SpaceQuest Ltd

- 6.4.12 Surrey Satellite Technology Ltd.

7. KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- SATELLITE MASS (ABOVE 10KG) BY REGION, NUMBER OF SATELLITES LAUNCHED, GLOBAL, 2017 - 2022

- Figure 2:

- SPENDING ON SPACE PROGRAMS BY REGION, USD, GLOBAL, 2017 - 2022

- Figure 3:

- GLOBAL LEO SATELLITE MARKET, VALUE, USD, 2017 - 2029

- Figure 4:

- VALUE OF LEO SATELLITE MARKET BY APPLICATION, USD, GLOBAL, 2017 - 2029

- Figure 5:

- VALUE SHARE OF LEO SATELLITE MARKET BY APPLICATION, %, GLOBAL, 2017 VS 2023 VS 2029

- Figure 6:

- VALUE OF COMMUNICATION MARKET, USD, GLOBAL, 2017 - 2029

- Figure 7:

- VALUE OF EARTH OBSERVATION MARKET, USD, GLOBAL, 2017 - 2029

- Figure 8:

- VALUE OF NAVIGATION MARKET, USD, GLOBAL, 2017 - 2029

- Figure 9:

- VALUE OF SPACE OBSERVATION MARKET, USD, GLOBAL, 2017 - 2029

- Figure 10:

- VALUE OF OTHERS MARKET, USD, GLOBAL, 2017 - 2029

- Figure 11:

- VALUE OF LEO SATELLITE MARKET BY SATELLITE MASS, USD, GLOBAL, 2017 - 2029

- Figure 12:

- VALUE SHARE OF LEO SATELLITE MARKET BY SATELLITE MASS, %, GLOBAL, 2017 VS 2023 VS 2029

- Figure 13:

- VALUE OF 10-100KG MARKET, USD, GLOBAL, 2017 - 2029

- Figure 14:

- VALUE OF 100-500KG MARKET, USD, GLOBAL, 2017 - 2029

- Figure 15:

- VALUE OF 500-1000KG MARKET, USD, GLOBAL, 2017 - 2029

- Figure 16:

- VALUE OF BELOW 10 KG MARKET, USD, GLOBAL, 2017 - 2029

- Figure 17:

- VALUE OF ABOVE 1000KG MARKET, USD, GLOBAL, 2017 - 2029

- Figure 18:

- VALUE OF LEO SATELLITE MARKET BY END USER, USD, GLOBAL, 2017 - 2029

- Figure 19:

- VALUE SHARE OF LEO SATELLITE MARKET BY END USER, %, GLOBAL, 2017 VS 2023 VS 2029

- Figure 20:

- VALUE OF COMMERCIAL MARKET, USD, GLOBAL, 2017 - 2029

- Figure 21:

- VALUE OF MILITARY & GOVERNMENT MARKET, USD, GLOBAL, 2017 - 2029

- Figure 22:

- VALUE OF OTHER MARKET, USD, GLOBAL, 2017 - 2029

- Figure 23:

- VALUE OF LEO SATELLITE MARKET BY PROPULSION TECH, USD, GLOBAL, 2017 - 2029

- Figure 24:

- VALUE SHARE OF LEO SATELLITE MARKET BY PROPULSION TECH, %, GLOBAL, 2017 VS 2023 VS 2029

- Figure 25:

- VALUE OF ELECTRIC MARKET, USD, GLOBAL, 2017 - 2029

- Figure 26:

- VALUE OF GAS BASED MARKET, USD, GLOBAL, 2017 - 2029

- Figure 27:

- VALUE OF LIQUID FUEL MARKET, USD, GLOBAL, 2017 - 2029

- Figure 28:

- VALUE OF LEO SATELLITE MARKET BY REGION, USD, GLOBAL, 2017 - 2029

- Figure 29:

- VALUE SHARE OF LEO SATELLITE MARKET BY REGION, %, GLOBAL, 2017 VS 2023 VS 2029

- Figure 30:

- VALUE OF LEO SATELLITE MARKET, USD, ASIA-PACIFIC, 2017 - 2029

- Figure 31:

- VALUE SHARE OF LEO SATELLITE MARKET %, ASIA-PACIFIC, 2017 VS 2029

- Figure 32:

- VALUE OF LEO SATELLITE MARKET, USD, EUROPE, 2017 - 2029

- Figure 33:

- VALUE SHARE OF LEO SATELLITE MARKET %, EUROPE, 2017 VS 2029

- Figure 34:

- VALUE OF LEO SATELLITE MARKET, USD, NORTH AMERICA, 2017 - 2029

- Figure 35:

- VALUE SHARE OF LEO SATELLITE MARKET %, NORTH AMERICA, 2017 VS 2029

- Figure 36:

- VALUE OF LEO SATELLITE MARKET, USD, REST OF WORLD, 2017 - 2029

- Figure 37:

- VALUE SHARE OF LEO SATELLITE MARKET %, REST OF WORLD, 2017 VS 2029

- Figure 38:

- NUMBER OF STRATEGIC MOVES OF MOST ACTIVE COMPANIES, GLOBAL LEO SATELLITE MARKET, ALL, 2017 - 2029

- Figure 39:

- TOTAL NUMBER OF STRATEGIC MOVES OF COMPANIES, GLOBAL LEO SATELLITE MARKET, ALL, 2017 - 2029

- Figure 40:

- MARKET SHARE OF GLOBAL LEO SATELLITE MARKET, %, ALL, 2023

LEO Satellite Industry Segmentation

Communication, Earth Observation, Navigation, Space Observation, Others are covered as segments by Application. 10-100kg, 100-500kg, 500-1000kg, Below 10 Kg, above 1000kg are covered as segments by Satellite Mass. Commercial, Military & Government are covered as segments by End User. Electric, Gas based, Liquid Fuel are covered as segments by Propulsion Tech. Asia-Pacific, Europe, North America are covered as segments by Region.| Application | Communication |

| Earth Observation | |

| Navigation | |

| Space Observation | |

| Others | |

| Satellite Mass | 10-100kg |

| 100-500kg | |

| 500-1000kg | |

| Below 10 Kg | |

| above 1000kg | |

| End User | Commercial |

| Military & Government | |

| Other | |

| Propulsion Tech | Electric |

| Gas based | |

| Liquid Fuel | |

| Region | Asia-Pacific |

| Europe | |

| North America | |

| Rest of World |

Need A Different Region or Segment?

Customize Now

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.

Get More Details On Research Methodology

Download PDF