| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 21.17 Billion |

| Market Size (2030) | USD 81.35 Billion |

| CAGR (2025 - 2030) | 30.90 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

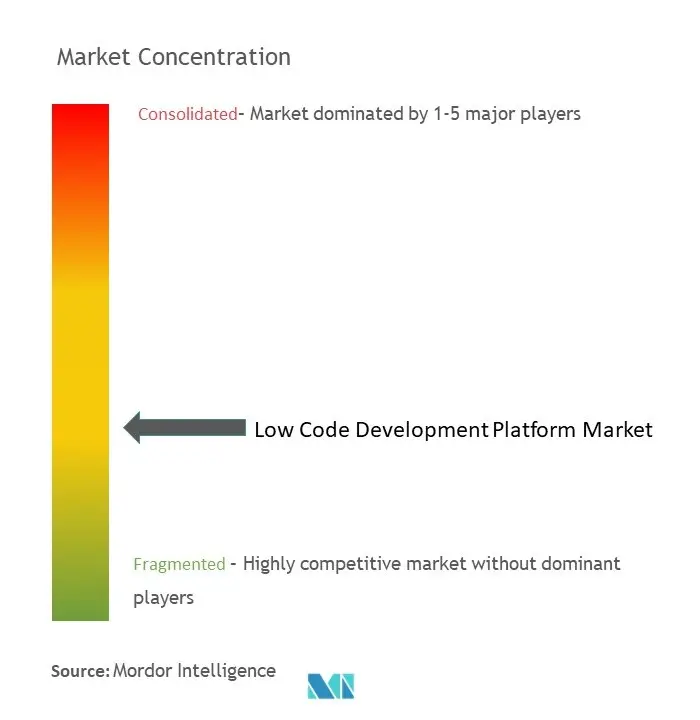

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Low-code Development Platform Market Analysis

The Low-code Development Platform Market size is estimated at USD 21.17 billion in 2025, and is expected to reach USD 81.35 billion by 2030, at a CAGR of 30.9% during the forecast period (2025-2030).

The low-code development platform market is experiencing transformative growth driven by the accelerating pace of digital modernization across industries. According to Microsoft, over 500 million new applications will need to be built over the next few years, which is more than all the apps developed in the last 40 years combined. Organizations are increasingly adopting visual development environments that enable rapid application creation through drag-and-drop interfaces and pre-built templates, significantly reducing the traditional coding burden. The shift towards these platforms represents a fundamental change in how enterprises approach software development, moving away from conventional programming paradigms to more agile and accessible development methodologies.

The democratization of application development has emerged as a defining characteristic of the low-code development platform landscape, with platforms becoming increasingly sophisticated in their capabilities while maintaining user-friendly interfaces. A notable indicator of this trend is that 70% of low-code development platform users with no prior experience were able to learn the platform within one month or less, according to Mendix statistics. This accessibility has led to the rise of citizen developers within organizations, enabling business users to create custom applications while maintaining IT governance and security protocols. The platforms now incorporate advanced features such as artificial intelligence, machine learning, and robotic process automation, allowing for the creation of more complex and intelligent applications.

Enterprise integration capabilities have become a crucial differentiator in the low-code development platform market, with vendors focusing on providing robust connectivity options across diverse business systems. Modern low-code development platforms are evolving to offer pre-built connectors, API management capabilities, and integration with popular enterprise applications, enabling seamless data flow across organizational systems. The market has witnessed significant advancement in cross-platform deployment capabilities, with solutions supporting a hybrid mix of cloud and on-premise deployments across Windows, IBM i platforms, and Linux environments with minimal code modification.

The industry is experiencing a shift towards more specialized and industry-specific low-code development platform solutions, with vendors developing targeted offerings for different sectors. According to recent industry surveys, 73% of organizations have invested in IT and collaboration tools to support their distributed workforce, indicating a strong focus on digital workplace solutions. This specialization is evident in the emergence of vertical-specific templates, components, and workflows that address unique industry requirements. Vendors are increasingly partnering with industry experts to develop pre-built solutions that accelerate time-to-market for sector-specific applications while ensuring compliance with industry regulations and standards.

Low-code Development Platform Market Trends

Increasing Need for Rapid Customization and Scalability

The creation of applications from scratch is becoming increasingly resource-intensive and expensive, particularly for startups and small businesses looking to verify ideas and enter the market faster than competitors. Low-code development platforms provide development environments that enable businesses to develop software quickly with minimal coding, reducing the need for extensive coding experience. These platforms provide base-level code, scripts, and integrations so companies can prototype, build, or scale applications without developing complex infrastructures, allowing both developers and non-developers to practice rapid application development with customized workflows and functionality.

Recent research indicates that 61% of low-code development platform users successfully deliver custom apps on time, on scope, and within budget, demonstrating the platform's effectiveness in meeting customization needs. The platforms offer various specialized solutions, including business process management platforms for internal operations, process creation and management tools for digital transformation, and platforms for user-facing applications and websites. For instance, in November 2023, OutSystems Japan launched their low-code solution, OutSystems Developer Cloud, specifically designed for cloud-native application development, enabling secure utilization in large-scale applications and allowing full-stack development from front-end to back-end.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Enterprise Mobility

Enterprise mobility has become a crucial factor driving the adoption of low-code development platforms, as organizations seek to provide their mobile workforce with efficient access to business-critical applications and information. Enterprise vendors are increasingly providing solutions that can address the needs of the proliferating mobile workforce, leveraging information such as worker locations and products through low-code functionalities in mobile devices. This trend has led to the emergence of a new generation of mobile-first solutions that prioritize mobile users, particularly crucial for applications with mobility functionalities such as logistics applications managing vehicle fleets and field service applications.

The integration of low-code platforms with enterprise mobility is evidenced by various technological advancements and initiatives. For instance, in July 2022, Kissflow released its unified low-code/no-code work platform, accelerating business digital transformation by combining the complete range of task management for enterprise-wide users, including end users, teams, team managers, process specialists, citizen developer platforms, and IT developers. These developments enable employees to access information unavailable to customers and offer prompt and informative experiences, thereby enhancing overall customer experience while maintaining operational efficiency.

Elimination of Gaps in the Required IT Skills

The growing adoption of emerging technologies has created a significant demand for skilled IT professionals, leading organizations to turn to low-code platforms as a solution to bridge the skills gap. According to recent industry data, 63% of low-code platform users possess the skills and resources necessary to fulfill the demand for custom apps, while 58% can effectively keep up with the demand for custom app requests across their business operations. This demonstrates how low-code platforms are successfully addressing the IT skills shortage by enabling existing staff and non-developers to contribute to application development.

The elimination of IT skills gaps is further supported by the integration of advanced technologies within low-code platforms. For example, Huawei's General Digital Engine (GDE) platform, with its "1+4+N" architecture, enables data sharing, intelligent production flow, capability sharing, and integrated low-code self-development, making it accessible to users with varying levels of technical expertise. Additionally, companies like Retool are expanding their presence in emerging markets like India with exclusive offerings, specifically targeting IT service providers and startups to help bridge the technical skills gap through simplified development processes and intuitive interfaces. These efforts align with the broader adoption of business process automation platforms and digital transformation platforms to streamline operations and enhance productivity.

Segment Analysis: By Application Type

Desktop and Server-Based Segment in Low-Code Development Platform Market

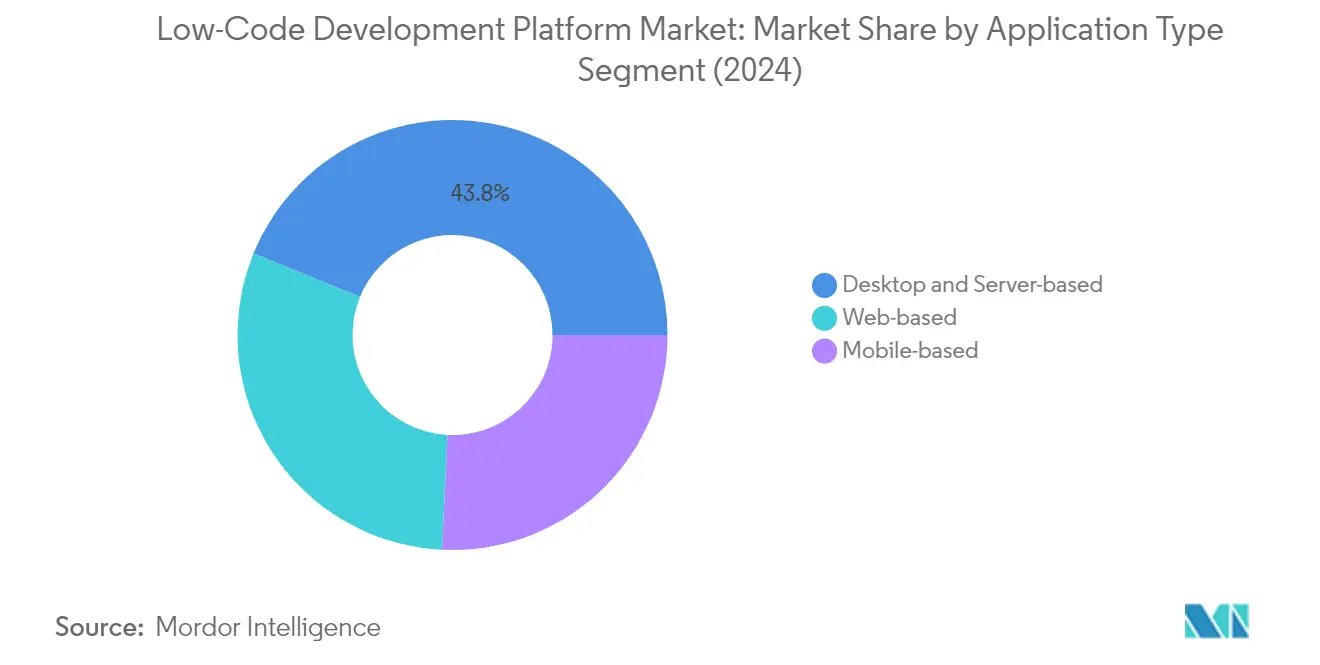

The Desktop and Server-based segment dominates the application development platform market, holding approximately 44% of the market share in 2024. This significant market position is driven by the segment's comprehensive functionality and ability to handle complex enterprise processes. Desktop and server-based platforms offer robust capabilities for building sophisticated applications, supporting both professional developers and citizen developers in creating enterprise-grade solutions. These platforms provide extensive integration capabilities with existing systems, enhanced security features, and better control over the development environment, making them particularly attractive for large enterprises and organizations with complex IT infrastructures.

Mobile-Based Segment in Low-Code Development Platform Market

The Mobile-based segment is emerging as the fastest-growing category in the enterprise application development platform market, with a projected growth rate of approximately 31% during 2024-2029. This rapid growth is primarily driven by the increasing enterprise mobility trends and the rising demand for mobile application development solutions. Organizations are increasingly focusing on mobile-first strategies, leading to greater adoption of mobile-based low-code platforms. These platforms enable rapid development of mobile applications with features like drag-and-drop interfaces, pre-built templates, and cross-platform compatibility, allowing businesses to quickly respond to changing market demands and customer needs through mobile solutions.

Remaining Segments in Application Type

The Web-based segment represents a significant portion of the low-code development platform market, offering unique advantages for organizations seeking to develop web applications and portals. Web-based low-code platforms enable businesses to create sophisticated web applications without extensive coding knowledge, providing features like responsive design capabilities, web-specific components, and seamless integration with web services. These platforms are particularly valuable for organizations focusing on customer-facing applications, internal web portals, and cloud-based solutions, contributing to the overall digital transformation initiatives across various industries.

Segment Analysis: By Deployment Type

Cloud Segment in Low-Code Development Platform Market

The cloud deployment model dominates the rapid application development platform market, commanding approximately 58% market share in 2024, driven by its inherent flexibility and scalability advantages. Organizations are increasingly adopting cloud-based low-code platforms to leverage benefits such as lower capital expenditure requirements, rapid scalability, and enhanced collaboration capabilities. The segment's growth is further accelerated by the rising emphasis of businesses towards digital transformation and the need for remote development capabilities. Cloud deployment offers significant advantages in terms of automatic updates, lower provisioning costs, elastic scaling, and built-in security features. Major cloud providers are expanding their low-code offerings, with enhanced AI-driven capabilities and improved integration features, making it easier for organizations to develop and deploy applications in the cloud environment.

On-Premise Segment in Low-Code Development Platform Market

The on-premise deployment model continues to maintain its significance in the low-code development platform market, particularly among organizations with stringent security requirements and data privacy concerns. This deployment option provides organizations with complete control over their integrations with external functionality and offers a much larger level of customization. Government agencies and highly regulated industries often prefer on-premise solutions to comply with specific data security and privacy regulations. The segment is particularly strong in sectors where network isolation is crucial, such as military environments and closed operational systems. Despite the higher costs associated with managing and maintaining on-premise environments, many organizations value the enhanced control over configuration, upgrades, and system changes that this deployment model offers.

Segment Analysis: By Organization Size

Small and Medium Enterprises Segment in Low-Code Development Platform Market

Small and Medium Enterprises (SMEs) have emerged as the dominant force in the enterprise application development platform market, commanding approximately 57% of the total market share in 2024, while also demonstrating the strongest growth trajectory with a projected growth rate of around 36% from 2024 to 2029. The segment's dominance can be attributed to SMEs' increasing focus on cost-efficient solutions and their need for rapid application development with minimal programming expertise. Low-code platforms are naturally designed for business users, allowing SMEs to empower functional teams to build applications quickly without extensive technical knowledge. These platforms enable businesses to leverage the benefits of low-code development while saving money on overhead costs and expensive development resources. The cloud-based nature of most low-code platforms particularly appeals to SMEs, as it eliminates the need for substantial upfront infrastructure investments. Furthermore, these platforms have become increasingly attractive to SMEs due to their ability to bridge the skills gap by allowing existing IT staff and non-developers to quickly and easily build mobile and web applications, thereby accelerating their digital transformation initiatives.

Large Enterprises Segment in Low-Code Development Platform Market

Large enterprises represent a significant segment in the low-code development platform market, driven by their need to automate internal operations and build custom applications for various business functions. These organizations typically have more complex internal operations and therefore require sophisticated ways to build internal apps to automate and digitize their processes. The adoption of low-code platforms by large enterprises has been particularly notable in sectors such as banking, retail, and healthcare, where the need for rapid application development and process automation is crucial. Large enterprises are leveraging these platforms to accelerate their digital transformation initiatives, reduce technical debt, and improve time-to-market for new applications. The segment's growth is further supported by the increasing integration of low-code platforms with emerging technologies such as artificial intelligence, robotic process automation, and cloud computing, enabling enterprises to create more sophisticated and scalable applications. Additionally, large enterprises are using low-code platforms to empower citizen developers within their organizations, fostering innovation while maintaining proper governance and security protocols.

Segment Analysis: By End-User Vertical

Information Technology Segment in Low-Code Development Platform Market

The Information Technology sector has emerged as the dominant segment in the low-code development platform market, commanding approximately 18% of the total market share in 2024. This leadership position is driven by IT enterprises' increasing need to develop numerous applications for both mobile and online platforms, serving both internal needs and client requirements. The segment's dominance is further strengthened by the significant payoffs it offers for developers and customers relying on their software applications, with major players incorporating cloud platforms and hybrid solutions to enhance flexibility and transparency. Recent research indicates that over 60% of Low Code platform users in the IT sector successfully deliver custom apps on time, on scope, and on budget, while maintaining the ability to keep up with the growing demand for custom application requests across various business functions.

Healthcare Segment in Low-Code Development Platform Market

The healthcare sector is experiencing the fastest growth in the low-code development platform market, with a projected growth rate of approximately 32% during 2024-2029. This remarkable growth is primarily driven by the accelerating digital transformation in healthcare organizations and the increasing need for remote healthcare services. The sector's rapid adoption of low-code solutions is fueled by the ability to quickly adapt and develop applications without disrupting current operations, particularly crucial in healthcare settings where continuous service delivery is essential. The integration of advanced technologies such as Machine Learning, Artificial Intelligence, and compliance with healthcare standards like HIPAA and HL7 is further accelerating the adoption of low-code platforms in this sector, enabling healthcare providers to optimize patient workloads and orchestrate hospital resources more efficiently.

Remaining Segments in End-User Vertical

The low-code development platform market encompasses several other significant segments including Retail & E-commerce, which is driving digital transformation in customer experience; BFSI, which leverages low-code for financial service automation; Government & Defense, focusing on modernizing public services; Energy & Utilities, implementing smart grid solutions; and Manufacturing, utilizing low-code for process automation. Each of these segments contributes uniquely to the market's dynamics, with Retail & E-commerce focusing on omnichannel experiences, BFSI emphasizing security and compliance, Government & Defense prioritizing citizen services, Energy & Utilities focusing on operational efficiency, and Manufacturing concentrating on industrial automation and quality control. These segments collectively demonstrate the versatility and wide-ranging applications of low-code development platforms across different industries.

Low-code Development Platform Market Geography Segment Analysis

Low-code Development Platform Market in North America

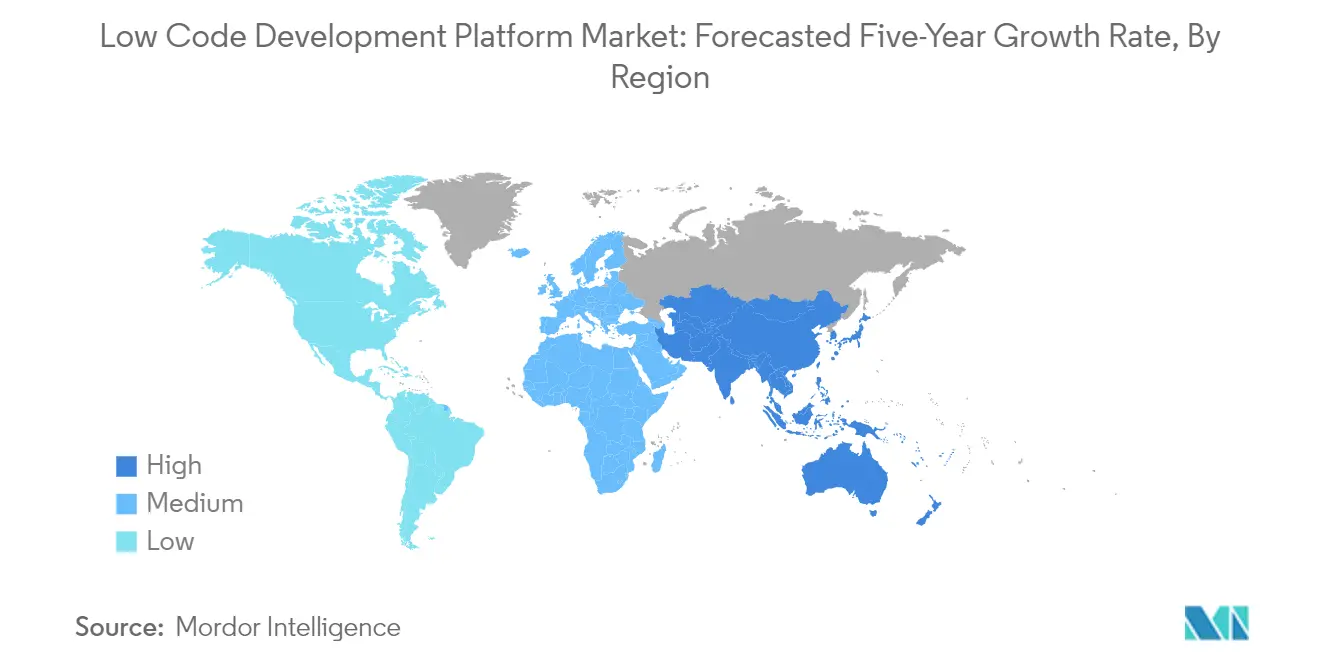

North America continues to dominate the low-code development platform market, holding approximately 34% of the global market share in 2024. The region's leadership position is driven by its high digital penetration rate and extensive investment in IT technologies. The presence of major developed economies like the United States and Canada significantly contributes to market growth. Multiple factors, including increasing competition, extensive R&D programs, and growing data proliferation, are assisting the growth of the low-code development platform market in North America. The region's enterprises are increasingly focusing on digital transformation initiatives, leading to higher adoption of low-code platforms. The market is characterized by strong demand for cloud-based solutions and increasing emphasis on enterprise mobility. Furthermore, the presence of numerous technology giants and innovative startups has created a robust ecosystem for the low-code development platforms market. The region also benefits from early technology adoption trends and a strong focus on automation and efficiency improvements across industries.

Low-code Development Platform Market in Europe

The European low-code development platform market has demonstrated remarkable growth, recording approximately 30% growth annually from 2019 to 2024. The region's market is characterized by strong adoption across various industries, particularly in digital-first economies. Organizations across Europe, regardless of their size, are increasingly relying on digital service providers to maintain a competitive advantage and ensure technology usage to transform and scale businesses. The market is particularly strong in countries like Germany, France, and the United Kingdom, where digital transformation initiatives are gaining significant momentum. European enterprises are showing particular interest in low-code solutions that can help address the growing need for rapid application development while maintaining compliance with strict regional data protection regulations. The region's focus on innovation and digital sovereignty has also contributed to the growth of local low-code platform providers. Additionally, the market is seeing increased adoption in sectors such as banking, healthcare, and manufacturing, where process automation and digital transformation are key priorities.

Low-code Development Platform Market in Asia-Pacific

The Asia-Pacific low-code development platform market is positioned for exceptional growth, with projections indicating approximately 31% annual growth from 2024 to 2029. The region's market is being primarily driven by the increasing adoption of mobile applications and digital transformation initiatives across various sectors. The presence of numerous SMEs with limited resources has created a strong demand for managed services and low-code solutions. Government initiatives promoting digital transformation and smart city development are creating favorable conditions for market growth. The region's diverse market landscape, spanning developed economies like Japan and Australia to emerging markets like India and Southeast Asian countries, presents unique opportunities for providers of low-code development platforms. The market is witnessing increasing adoption across various sectors, particularly in financial services, retail, and public sector organizations. The growing emphasis on technological innovation and digital literacy in countries like China and South Korea is further accelerating market growth.

Low-code Development Platform Market in Latin America

The Latin American low-code development platform market is experiencing significant transformation, driven by increasing digital adoption and modernization initiatives. Brazil leads the regional market, followed by Mexico, Argentina, Chile, and Colombia, with each country showing unique adoption patterns and growth trajectories. The region's market is characterized by a growing focus on cloud adoption and digital transformation across various sectors. Organizations are increasingly looking for competitive advantages and efficient cost management solutions through low-code platforms. The market is particularly active in the financial services sector, where institutions are leveraging low-code solutions to accelerate their digital transformation journey. The region's growing startup ecosystem and increasing focus on technology innovation are creating new opportunities for adoption of low-code development platforms. Additionally, the market is benefiting from increasing investments in IT infrastructure and growing awareness about the benefits of rapid application development.

Low-code Development Platform Market in Middle East & Africa

The Middle East and African low-code development platform market is emerging as a significant growth opportunity, driven by ambitious digital transformation initiatives across the region. Businesses across the Middle East are implementing comprehensive transformation roadmaps to ensure relevance in the digital world. The adoption of platform technologies, including cloud, low-code, mobility, and social platforms, is becoming mainstream throughout the region. The market is particularly active in countries like the United Arab Emirates and Saudi Arabia, where government-led digital transformation initiatives are creating substantial opportunities. The financial services sector is leading the adoption of low-code platforms, followed by government and healthcare sectors. Organizations in the region are increasingly recognizing the value of low-code platforms in accelerating their digital transformation journey while addressing the technical skills gap. The market is also benefiting from increasing investments in IT infrastructure and a growing focus on smart city initiatives.

Get Analysis on Important Geographic Markets

Download PDF

Low-code Development Platform Industry Overview

Top Companies in Low-Code Development Platform Market

The low-code development platform market features prominent players like Salesforce, Microsoft, Oracle, Appian, and OutSystems leading the innovation curve through continuous product development and strategic partnerships. These companies are focusing on enhancing their platforms with artificial intelligence capabilities, cloud integration, and advanced automation features to streamline application development processes. Market leaders are actively pursuing geographical expansion through both organic growth and strategic acquisitions, particularly in emerging markets. The competitive landscape is characterized by substantial investments in research and development, with companies introducing new features like visual development interfaces, drag-and-drop capabilities, and pre-built templates to accelerate application deployment. Additionally, vendors are strengthening their positions through strategic collaborations with system integrators and technology consulting firms, while also expanding their partner ecosystems to provide comprehensive solutions across various industry verticals.

Dynamic Market with Strong Growth Potential

The low-code development platform market exhibits a moderately consolidated structure, with global technology conglomerates competing alongside specialized platform providers. Major players like Microsoft and Oracle leverage their existing enterprise relationships and comprehensive product portfolios to maintain market dominance, while specialized providers like Appian and OutSystems differentiate themselves through focused innovation in low-code capabilities. The market has witnessed significant merger and acquisition activity, with larger technology companies acquiring smaller, innovative players to enhance their low-code offerings and expand their market presence.

The competitive dynamics are shaped by the increasing demand for rapid application development platform solutions across industries, driving both established players and new entrants to enhance their product offerings. Market participants are actively pursuing strategic partnerships with cloud service providers, system integrators, and industry-specific solution providers to strengthen their market position. The landscape is further characterized by the emergence of regional players who are gaining traction by offering localized solutions and addressing specific industry requirements, particularly in emerging markets where digital transformation initiatives are accelerating.

Innovation and Integration Drive Market Success

Success in the low-code development platform market increasingly depends on vendors' ability to provide comprehensive, integrated solutions that address the evolving needs of enterprises undergoing digital transformation. Market leaders are focusing on developing industry-specific templates and solutions, enhancing platform scalability, and ensuring seamless integration with existing enterprise systems. Companies are also investing in building robust security features, compliance capabilities, and governance frameworks to address growing concerns around data protection and regulatory requirements. The ability to provide effective training, support services, and comprehensive documentation has become crucial for platform adoption and customer retention.

For contenders looking to gain market share, differentiation through specialized features, industry focus, or technological innovation presents significant opportunities. Success factors include developing strong partner ecosystems, offering competitive pricing models, and providing superior customer support and training resources. Vendors must also address the growing demand for mobile application development capabilities, cross-platform compatibility, and integration with emerging technologies such as artificial intelligence and machine learning. The market's future will be shaped by vendors' ability to balance ease of use with powerful functionality, while maintaining robust security features and compliance with evolving regulatory requirements. The role of a digital transformation platform is becoming increasingly critical as enterprises seek to streamline their processes and enhance operational efficiency.

Low-code Development Platform Market Leaders

-

Salesforce.com Inc.

-

Microsoft Corporation

-

Appian Corporation

-

Oracle Corporation

-

Pegasystems Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Low-code Development Platform Market News

- January 2024: A collaboration between Neptune Software and KPS AG, a consulting partner specializing in customer-centric transformations, introduced advanced solutions for enterprise application development across industries. Neptune, renowned for its low-code app development platform, facilitates agile digitalization and process optimization, particularly within the SAP domain. Its platform streamlines SAP processes and allows for the swift development of bespoke applications. The alliance between KPS AG and Neptune Software is poised to expedite and cost-effectively revolutionize business processes through their innovative low-code approach.

- September 2023: Salesforce unveiled the Einstein 1 Platform, showcasing significant enhancements to its Data Cloud and Einstein AI features. Salesforce's robust metadata framework underpins these innovations. Positioned as a reliable AI hub for customer-centric firms, the Einstein 1 Platform empowers companies to seamlessly integrate diverse datasets, enabling them to create AI-driven applications with minimal coding and revolutionize their CRM interactions.

- May 2023: Appian advanced low-code into a new era of AI process automation. As an integral part of the progression of the Appian Platform, the company added key elements of artificial intelligence (AI) to its total technology proposition.

Low Code Development Platform Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of Key Macroeconomic Trends on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Need for Rapid Customization and Scalability

- 5.1.2 Increasing Enterprise Mobility

- 5.1.3 Elimination of Gaps in Required IT Skills

-

5.2 Market Challenges

- 5.2.1 Dependency on Vendor-supplied Customization

6. EMERGING TECHNOLOGY TRENDS

7. MARKET SEGMENTATION

-

7.1 By Application Type

- 7.1.1 Web-based

- 7.1.2 Mobile-based

- 7.1.3 Desktop- and Server-based

-

7.2 By Deployment Type

- 7.2.1 On-premise

- 7.2.2 Cloud

-

7.3 By Organization Size

- 7.3.1 Small and Medium Enterprises

- 7.3.2 Large Enterprises

-

7.4 By End-user Vertical

- 7.4.1 BFSI

- 7.4.2 Retail and E-commerce

- 7.4.3 Government and Defense

- 7.4.4 Information Technology

- 7.4.5 Energy and Utilities

- 7.4.6 Manufacturing

- 7.4.7 Healthcare

- 7.4.8 Other End-user Verticals

-

7.5 By Geography

- 7.5.1 North America

- 7.5.2 Europe

- 7.5.3 Asia-Pacific

- 7.5.4 Latin America

- 7.5.5 Middle East and Africa

8. COMPETITIVE LANDSCAPE

-

8.1 Company Profiles*

- 8.1.1 Microsoft Corporation

- 8.1.2 Appian Corporation

- 8.1.3 Oracle Corporation

- 8.1.4 Pegasystems Inc.

- 8.1.5 Magic Software Enterprises Ltd

- 8.1.6 AgilePoint Inc.

- 8.1.7 Outsystems Inc.

- 8.1.8 Mendix Inc.

- 8.1.9 ZOHO Corporation

- 8.1.10 QuickBase Inc.

- 8.1.11 Clear Software LLC

- 8.1.12 Kony Inc. 8.14 ServiceNow Inc.

- 8.1.13 Skuid Inc.

9. VENDOR MARKET POSITIONING ANALYSIS

10. INVESTMENT ANALYSIS

11. FUTURE OF THE MARKET

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Low-code Development Platform Industry Segmentation

A low-code development platform (LCDP) offers a coding environment that enables developers with varying expertise to build applications. It uses a dynamic graphical user interface and configuration with model-driven logic instead of conventional hand-coded computer programming. For specific situations, these platforms may require extensive coding.

The low-code development platform market is segmented by application type (web-based, mobile-based, and desktop and server-based), deployment type (on-premise and cloud), organization size (small and medium enterprises and large enterprises), end-user verticals (BFSI, retail and e-commerce, information technology, energy and utilities, manufacturing, healthcare, government, and defense, and other end-user verticals), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Application Type | Web-based |

| Mobile-based | |

| Desktop- and Server-based | |

| By Deployment Type | On-premise |

| Cloud | |

| By Organization Size | Small and Medium Enterprises |

| Large Enterprises | |

| By End-user Vertical | BFSI |

| Retail and E-commerce | |

| Government and Defense | |

| Information Technology | |

| Energy and Utilities | |

| Manufacturing | |

| Healthcare | |

| Other End-user Verticals | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Low Code Development Platform Market Research FAQs

How big is the Low-code Development Platform Market?

The Low-code Development Platform Market size is expected to reach USD 21.17 billion in 2025 and grow at a CAGR of 30.90% to reach USD 81.35 billion by 2030.

What is the current Low-code Development Platform Market size?

In 2025, the Low-code Development Platform Market size is expected to reach USD 21.17 billion.

Who are the key players in Low-code Development Platform Market?

Salesforce.com Inc., Microsoft Corporation, Appian Corporation, Oracle Corporation and Pegasystems Inc. are the major companies operating in the Low-code Development Platform Market.

Which is the fastest growing region in Low-code Development Platform Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Low-code Development Platform Market?

In 2025, the North America accounts for the largest market share in Low-code Development Platform Market.

What years does this Low-code Development Platform Market cover, and what was the market size in 2024?

In 2024, the Low-code Development Platform Market size was estimated at USD 14.63 billion. The report covers the Low-code Development Platform Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Low-code Development Platform Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Low-code Development Platform Market Research

Mordor Intelligence provides a comprehensive analysis of the low-code development platform market. We leverage our extensive expertise in digital transformation platform research. Our latest report examines the evolving landscape of LCDP solutions. It encompasses both no code development platform and low code development platform technologies. The analysis covers crucial developments in business process automation platform implementations and the rising adoption of citizen developer platform solutions across industries.

Stakeholders seeking insights into the low code development platform market size will find detailed evaluations of rapid application development platform trends and visual programming platform innovations. The report, available for easy download as a PDF, provides an in-depth analysis of enterprise application development platform adoption patterns and business process management platform integration strategies. Our research particularly focuses on how citizen development platform initiatives are reshaping the enterprise development platform landscape. It offers valuable insights for decision-makers navigating the visual development platform ecosystem.