| Study Period | 2019 - 2030 |

| Market Volume (2025) | 0.69 Thousand LCE kilotons |

| Market Volume (2030) | 1.96 Thousand LCE kilotons |

| CAGR | 23.22 % |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Lithium Carbonate Market Analysis

The Lithium Carbonate Market size is estimated at 0.69 thousand lce kilotons in 2025, and is expected to reach 1.96 thousand lce kilotons by 2030, at a CAGR of 23.22% during the forecast period (2025-2030).

The lithium carbonate industry is experiencing significant transformation driven by technological advancements and sustainability initiatives. Major industry players are increasingly focusing on developing more efficient and environmentally friendly lithium processing methods to address the growing demand while minimizing environmental impact. According to the International Energy Agency (IEA), the demand for automotive Li-ion batteries witnessed a remarkable surge of 65% in 2022, reaching 550 GWh from 330 GWh in 2021, highlighting the accelerating transition towards electric mobility and clean energy solutions.

The industry landscape is being reshaped by strategic consolidations and partnerships aimed at strengthening supply chain resilience. In 2023, significant mergers and acquisitions took place, including the formation of Arcadium Lithium through the merger of Allkem and Livent, creating a leading global integrated lithium chemicals producer with a projected production capacity of 250 kilotons per annum. These strategic moves are complemented by substantial investments in research and development, focusing on improving production efficiency and product quality while reducing environmental footprint.

The market is witnessing a dramatic expansion in production capacity through new facility investments worldwide. According to Rystad Energy, the annual battery energy storage system (BESS) capacity is projected to grow tenfold from 43 GWh in 2022 to 421 GWh by 2030, driving substantial demand for lithium carbonate. This growth is supported by numerous manufacturing facility announcements, such as ProLogium Technology's EUR 5.2 billion investment in a solid-state battery manufacturing plant in France and Northvolt's approval for a substantial EUR 902 million German state aid package for its EV battery production plant in January 2024.

The industry is also experiencing significant developments in the metallurgical sector, which presents additional growth opportunities. According to the United States Geological Survey (USGS), global smelter production of aluminum reached 70,000 metric tons in 2023, marking a growth of over 2% from 2022. This growth is further supported by major investments in steel production, exemplified by ArcelorMittal Luxembourg's plans to construct a new electric arc furnace at its Belval site and Voestalpine Group's EUR 1.5 billion investment for new electric arc furnaces at its Linz and Donawitz sites, announced in March 2023.

Lithium Carbonate Market Trends

Growing Demand from Lithium-Ion Batteries

The surging adoption of electric vehicles globally has created unprecedented demand for lithium-ion battery materials, consequently driving the lithium carbonate market. According to EV Volumes, global electric vehicle sales witnessed a remarkable increase of 15.8% in 2023, reaching 14.1 million units compared to 10.5 million units in 2022. This substantial growth in EV adoption has directly impacted the demand for automotive lithium battery materials, which experienced a dramatic 65% increase in 2022, reaching 550 GWh from 330 GWh in 2021, as reported by the International Energy Agency (IEA). The expansion of battery manufacturing capabilities worldwide further reinforces this trend, with several major investments announced in 2023, including Forge Nano, Inc.'s USD 165 million investment in a new lithium battery component manufacturing plant and LG Energy Solution's USD 5.5 billion investment in constructing a battery manufacturing complex in Arizona.

The application of lithium battery materials extends beyond electric vehicles, with significant growth observed in energy storage systems and renewable energy applications. These batteries are increasingly being employed in solar energy battery bank applications within photovoltaic systems, valued for their lightweight properties, low self-discharge characteristics, minimal maintenance requirements, and high scalability. According to Rystad Energy's 2023 report, the annual battery energy storage system (BESS) market is projected to expand tenfold between 2022 and 2030, with new global BESS installations expected to surge from 43 GWh in 2022 to 421 GWh by 2030. Additionally, technological advancements continue to drive market growth, as evidenced by the breakthrough development announced in February 2023 by researchers at the Illinois Institute of Technology and the U.S. Department of Energy's Argonne National Laboratory—a lithium-air battery capable of powering electric vehicles for over a thousand miles on a single charge.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Investments in the Glass and Ceramics Industry

The glass and ceramics industry has witnessed substantial investments and expansion projects, driving the demand for lithium carbonate as a crucial raw material. Lithium mining plays a vital role in this sector due to its exceptional bonding properties with silicates and other compounds, enabling the creation of vibrant glazes, durable sealants, and heat-resistant glasses. In the ceramics and glass manufacturing processes, lithium carbonate serves as a critical component for controlling thermal expansion, particularly in the production of specialized glass and ceramics. When incorporated into ceramics, it enhances the viscosity of coatings while improving the luster, color, and strength of glazes, making it an indispensable material for manufacturers.

Recent developments in the industry showcase the growing investment trend, with several significant projects announced in 2023. For instance, QSIL Ceramics GmbH announced a substantial investment in an expansion building in August 2023, demonstrating the industry's commitment to growth. In the glass sector, leading South Korean flat glass producer KCC Glass began constructing a new flat glass plant in Indonesia with an installed capacity of 428,000 tons per annum, scheduled for completion in 2024. These investments, coupled with the material's ability to lower both the melting point and viscosity of glasses during heat treatments, continue to drive the demand for lithium battery components in the glass and ceramics industry. The material's versatility in applications ranging from ceramic glazes to specialized glass manufacturing processes further reinforces its importance in this sector.

Segment Analysis: By Grade

Battery Grade Segment in Lithium Carbonate Market

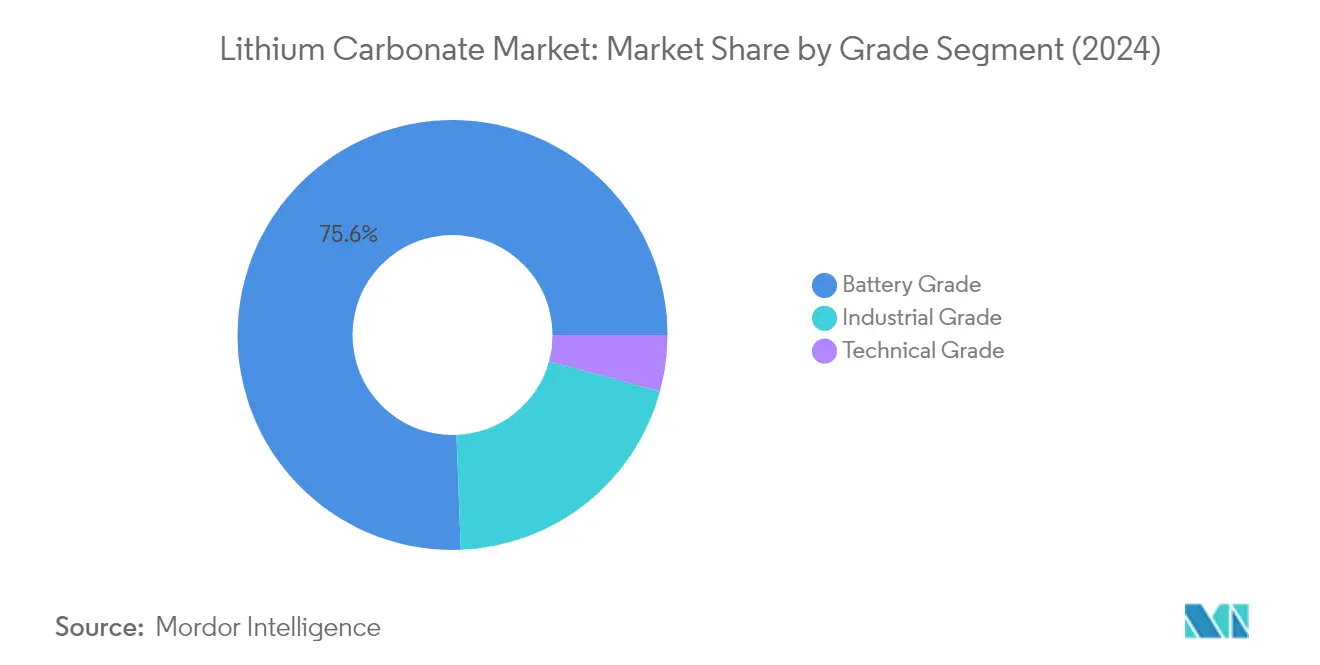

The battery-grade segment dominates the global lithium carbonate market, commanding approximately 76% of the total market share in 2024. This substantial market position is primarily driven by its superior properties, such as extended battery life and enhanced energy density, making it essential for lithium-ion battery production. The segment's growth is further bolstered by the dramatic increase in demand from electric vehicle manufacturers and energy storage systems. Battery-grade lithium carbonate, with its controlled particle size distribution and high purity levels of 99.5-99.9%, has become indispensable in producing cathode materials for lithium-ion batteries. The segment's prominence is particularly evident in major markets like China, where significant investments in battery manufacturing facilities continue to drive demand. The segment is also witnessing increased adoption in portable electronic devices, grid storage applications, and industrial equipment, further cementing its position as the market leader.

Industrial Grade Segment in Lithium Carbonate Market

The industrial-grade segment of the lithium carbonate market demonstrates robust growth potential, with applications spanning multiple industries, including industrial lithium carbonate synthesis, steel continuous casting, electrolytic aluminum, lithium bromide air conditioners, ceramics, glaze, enamel, optical glass, lubricating grease, and molecular sieves. This segment's versatility in industrial applications has positioned it as a crucial component in various manufacturing processes. The industrial lithium carbonate, with its minimum 99.0 wt% purity and maximum 0.5 wt% water content, continues to find new applications in emerging industrial processes. The segment's growth is particularly driven by increasing demand from the metallurgical industry, where it serves as a deoxidizer in industrial copper and nickel smelting processes and as a sulfur cleaner in various applications. The segment also plays a vital role in the production of specialized alloys, including magnesium-lithium aluminum alloy, which finds applications in the aerospace and telecommunications sectors.

Technical Grade Segment in Lithium Carbonate Market

The technical-grade segment, while smaller in market share, maintains its significance in specific industrial applications where high purity is not a critical requirement. This grade of lithium carbonate, typically containing 99.0% purity, serves essential functions in the glass and ceramics industry, where it helps reduce melting points and control thermal expansion properties. The segment finds particular utility in manufacturing fiberglass, general glass applications, and enamel products. Additionally, technical-grade lithium carbonate serves as a catalyst in esterification processes and as an additive in aluminum electrolysis melts. The segment also plays a crucial role in the construction industry, where it functions as an additive for quick-setting cements and grouts, demonstrating its versatility across various industrial applications.

Segment Analysis: By Application

Li-Ion Battery Segment in Lithium Carbonate Market

The Li-ion battery segment dominates the global lithium carbonate market, commanding approximately 90% of the total market share in 2024. This segment's prominence is primarily driven by the exponential growth in electric vehicle adoption and energy storage systems worldwide. The segment's dominance is further reinforced by significant investments in battery manufacturing facilities across major regions, particularly in Asia-Pacific and North America. Major automotive manufacturers and battery producers are establishing gigafactories to meet the surging demand for lithium-ion batteries. The segment's growth is also supported by the increasing adoption of portable electronic devices and the growing focus on renewable energy integration, which requires efficient energy storage solutions. Additionally, technological advancements in battery chemistry and manufacturing processes continue to drive the demand for high-purity lithium carbonate in this segment. The segment is expected to maintain its leading position through 2029, growing at a rate of around 24% annually from 2024 to 2029, driven by ambitious electric vehicle adoption targets and expanding energy storage applications.

Remaining Segments in Lithium Carbonate Market by Application

The remaining segments in the lithium carbonate market include glass and ceramics, pharmaceuticals and dental, aluminum production, cement industry, and other applications. The glass and ceramics segment represents a significant application area where lithium compounds are used to control thermal expansion and enhance the properties of specialty glass and ceramic products. In the pharmaceutical and dental sector, lithium salts serve as a crucial component in the treatment of bipolar disorder and other mental health conditions. The aluminum production segment utilizes Li2CO3 to optimize production processes and reduce energy consumption. The cement industry employs lithium carbonate as an accelerant in quick-setting cement applications. Other applications include air conditioning systems, lubricating greases, and various industrial processes where lithium carbonate's unique properties provide specific advantages in manufacturing and processing operations.

Lithium Carbonate Market Geography Segment Analysis

Lithium Carbonate Market in Asia-Pacific

The Asia-Pacific region dominates the global lithium carbonate market, driven by significant investments in electric vehicle battery manufacturing and energy storage systems. Countries like China, India, Japan, and South Korea are making substantial strides in developing their lithium-ion battery production capabilities. The region's growth is supported by government initiatives promoting electric vehicle adoption, expanding renewable energy integration, and increasing focus on sustainable energy solutions. The presence of major battery manufacturers and growing domestic demand for electric vehicles has established Asia-Pacific as the primary hub for lithium carbonate consumption.

Lithium Carbonate Market in China

China leads the Asia-Pacific region's lithium carbonate market, commanding approximately 83% of the regional market share in 2024. The country's dominance is attributed to its extensive lithium processing facilities and position as the world's largest producer of lithium-ion batteries, accounting for nearly 75% of global production. China's robust supply chain infrastructure, from raw material processing to end-product manufacturing, has established it as a crucial player in the global market. The country's commitment to electric vehicle adoption and energy storage solutions, coupled with significant investments in battery manufacturing capacity, continues to drive market growth. The presence of major battery manufacturers and ongoing capacity expansion projects further strengthens China's position in the regional market.

Growth Dynamics in Chinese Market

China is projected to maintain its position as the fastest-growing market in the Asia-Pacific region, with an expected growth rate of approximately 26% during 2024-2029. The country's growth trajectory is supported by its National Blueprint for Lithium Batteries, which aims to achieve 1,811 GWh of lithium battery production capacity by 2025. The expansion of electric vehicle manufacturing, coupled with increasing investments in renewable energy storage systems, continues to drive demand. China's focus on technological advancement in battery manufacturing and its strategic initiatives to secure lithium resources further contribute to its rapid market growth. The country's commitment to reducing carbon emissions and promoting clean energy solutions reinforces its position as a key driver of regional market expansion.

Lithium Carbonate Market in North America

The North American lithium carbonate market is experiencing significant growth, driven by increasing investments in electric vehicle battery manufacturing and energy storage solutions. The United States, Canada, and Mexico are actively developing their domestic battery production capabilities to reduce dependency on imports. The region's market is characterized by growing government support for electric vehicle adoption, expanding battery manufacturing infrastructure, and increasing focus on renewable energy integration. Strategic investments in lithium processing and battery production facilities across these countries are reshaping the regional market landscape.

Lithium Carbonate Market in United States

The United States dominates the North American market, accounting for approximately 90% of the regional market share in 2024. The country's market leadership is supported by substantial investments in battery manufacturing facilities and growing domestic demand for electric vehicles. The U.S. government's ambitious target for electric vehicles to comprise 50% of new passenger car and light truck sales by 2030 further drives market growth. The presence of major automotive manufacturers and their increasing focus on electric vehicle production continues to boost demand for lithium carbonate in the country.

Growth Dynamics in United States Market

The United States is set to maintain its position as the fastest-growing market in North America, with a projected growth rate of approximately 30% during 2024-2029. The country's rapid market expansion is driven by increasing investments in battery manufacturing facilities and growing adoption of electric vehicles. The implementation of government initiatives supporting domestic battery production and electric vehicle infrastructure development further accelerates market growth. The establishment of new battery manufacturing plants and ongoing research and development activities in battery technology contribute to the country's strong growth trajectory.

Lithium Carbonate Market in Europe

The European lithium carbonate market is witnessing substantial growth, driven by the region's aggressive push toward electric vehicle adoption and renewable energy storage solutions. Countries including Germany, the United Kingdom, France, and Italy are actively developing their battery manufacturing capabilities and establishing domestic supply chains. The region's market is supported by strong environmental regulations, government incentives for electric vehicle adoption, and increasing investments in battery production facilities. The European Union's focus on achieving carbon neutrality and reducing dependency on battery imports continues to shape the market landscape.

Lithium Carbonate Market in Germany

Germany leads the European lithium carbonate market, establishing itself as the region's primary hub for battery manufacturing and electric vehicle production. The country's strong automotive industry, coupled with significant investments in battery production facilities, drives market growth. Germany's commitment to transitioning toward electric mobility and its robust industrial infrastructure have attracted major investments from battery manufacturers and automotive companies. The country's strategic focus on developing a comprehensive battery value chain, from raw material processing to end-product manufacturing, reinforces its market leadership.

Growth Dynamics in German Market

Germany demonstrates the strongest growth potential in the European market, supported by its ambitious plans for battery manufacturing capacity expansion and electric vehicle production. The country's automotive industry's rapid transition toward electric vehicles and increasing investments in battery technology drive market growth. Germany's focus on research and development in battery technology, coupled with government support for sustainable mobility solutions, contributes to its market expansion. The establishment of new battery manufacturing facilities and growing collaboration between automotive and battery manufacturers further accelerates market development.

Lithium Carbonate Market in South America

The South American lithium carbonate market is characterized by its rich lithium resources and growing focus on value-added lithium products. Brazil and Argentina are the key markets in the region, with Argentina leading in terms of market size and growth potential. The region benefits from its vast lithium reserves and increasing investments in lithium processing capabilities. Brazil's growing electric vehicle market and Argentina's expanding lithium production capacity are driving regional market growth. The establishment of new lithium processing facilities and increasing focus on domestic battery production capabilities continue to shape the market landscape.

Lithium Carbonate Market in Middle East & Africa

The Middle East & Africa lithium carbonate market is gradually evolving, with Saudi Arabia and South Africa emerging as key markets in the region. Saudi Arabia leads in terms of market size, while South Africa demonstrates the highest growth potential. The region's market is driven by increasing investments in electric vehicle manufacturing, growing focus on renewable energy storage solutions, and expanding pharmaceutical industry. Government initiatives promoting industrial diversification and sustainable development contribute to market growth. The establishment of new manufacturing facilities and increasing adoption of electric vehicles continue to drive market development across the region.

Get Analysis on Important Geographic Markets

Download PDF

Lithium Carbonate Industry Overview

Top Companies in Lithium Carbonate Market

The global lithium carbonate market is characterized by intense innovation and strategic developments among key players like SQM SA, Albemarle Corporation, and Ganfeng Lithium. Companies are focusing on expanding their production capacities through technological advancements in extraction and processing methods, particularly in battery-grade lithium carbonate manufacturing. Strategic partnerships with electric vehicle manufacturers and battery producers have become increasingly common to secure long-term supply agreements. Operational agility is demonstrated through vertical integration initiatives, with companies controlling everything from mining operations to final product distribution. Geographic expansion, particularly in lithium-rich regions of South America and Australia, continues to be a priority for major players. Companies are also investing heavily in research and development to improve product quality and reduce production costs while maintaining environmental sustainability standards.

Consolidated Market with Strong Regional Players

The lithium carbonate market structure exhibits a high degree of consolidation, dominated by large multinational corporations with significant vertical integration capabilities. These major players possess substantial control over lithium products and processing facilities, creating high barriers to entry for new market participants. Regional players, particularly in China and South America, maintain strong positions in their respective markets through government support and proximity to raw material sources. The market has witnessed significant merger and acquisition activity, with companies seeking to strengthen their position through strategic consolidations and joint ventures.

The competitive dynamics are shaped by the increasing demand from the electric vehicle sector and energy storage applications, driving companies to secure their supply chains through backward integration. Market leaders are establishing strong partnerships across the value chain, from mining operations to end-user industries. The industry has seen a trend toward consolidation through strategic mergers, such as the formation of Arcadium Lithium, demonstrating the importance of scale and resource access in maintaining competitive advantage. Local players in key markets are increasingly partnering with global leaders to enhance their technological capabilities and market reach.

Innovation and Sustainability Drive Future Success

For established players to maintain and expand their market share, focus must be placed on developing more efficient extraction technologies and sustainable production methods. Companies need to invest in research and development to improve product quality while reducing environmental impact. Building strong relationships with end-users, particularly in the electric vehicle and energy storage sectors, will be crucial for long-term success. Vertical integration and supply chain optimization will continue to be key strategies for maintaining competitive advantage. Investment in digital technologies and automation will also be essential for improving operational efficiency and maintaining cost competitiveness.

New entrants and smaller players can gain ground by focusing on niche markets and developing innovative extraction technologies. Strategic partnerships with established players or end-users can provide access to markets and technologies. Companies must also prepare for potential regulatory changes, particularly regarding environmental standards and resource nationalism in key producing countries. The development of alternative lithium chemicals and recycling capabilities could provide opportunities for new market entrants. Success will depend on the ability to secure reliable raw material sources while maintaining cost-effective and environmentally sustainable operations.

Lithium Carbonate Market Leaders

-

Albemarle Corporation

-

SQM S.A.

-

Ganfeng Lithium Group Co., Ltd

-

Tianqi Lithium Industry Co., Ltd

-

Arcadium Lithium

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Lithium Carbonate Market News

- January 2024: Allkem and Livent completed an all-stock merger to form Arcadium Lithium. This merger is a strategic move to incorporate the existing resources and expand the production and supplier scale. Arcadium focuses on highly complementary assets and a vertically integrated business model focused on enhancing operational flexibility and predictability while lowering costs.

- October 2023: General Motors Holdings LLC (GM) executed a second tranche subscription agreement to which GM will purchase Lithium Americas (NewCo) shares of USD 329.85 million. Through this agreement, GM has 100% exclusive rights to Thacker Pass Phase 1 production for ten years, which produces lithium chemicals, including lithium carbonate.

- May 2023: SQM SA and Ford Motor Company announced a long-term strategic agreement to supply high-quality battery-grade lithium carbonate, which is an essential component for the manufacturing of high-performance electric vehicle batteries.

Lithium Carbonate Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Growing Demand From Lithium-ion Batteries

- 4.1.2 Increasing Investments in the Glass and Ceramics Industry

-

4.2 Market Restraints

- 4.2.1 Constraints in Lithium Extraction and Geographical Restriction of Lithium Mines

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size in Volume)

-

5.1 By Grade

- 5.1.1 Technical Grade

- 5.1.2 Battery Grade

- 5.1.3 Industrial Grade

-

5.2 By Application

- 5.2.1 Li-ion Battery

- 5.2.2 Pharmaceuticals and Dental

- 5.2.3 Glass and Ceramics

- 5.2.4 Aluminum Production

- 5.2.5 Cement Industry

- 5.2.6 Other Applications

-

5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Albemarle Corporation

- 6.4.2 Arcadium Lithium

- 6.4.3 Jiangxi Ganfeng Lithium Group Co. Ltd

- 6.4.4 Levertonhelm Limited

- 6.4.5 Lithium Americas Corp.

- 6.4.6 Lithium Argentina Corp.

- 6.4.7 Shandong Ruifu Lithium Co. Ltd

- 6.4.8 SQM SA

- 6.4.9 Tianqi Lithium Industry Co. Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Opportunity in the Metallurgy Industry

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Lithium Carbonate Industry Segmentation

Lithium carbonate (Li2CO3) is a white powder, carbonate salt of lithium. It is used as cathode and electrolyte precursor materials for lithium iron phosphate (LFP) batteries, which have applications in portable electronic devices (such as cell phones and laptops) and electric vehicles (EVs).

The global lithium carbonate market is segmented by grade, application, and geography. By grade, the market is segmented into technical grade, battery grade, and industrial grade. By application, the market is segmented into Li-ion battery, pharmaceuticals and dental, glass and ceramic, aluminum production, cement industry, and other applications (air conditioning and treatment, lubricating grease, metallurgical industry, etc.). The report also covers the market sizes and forecasts for the global lithium carbonate market in 15 countries across major regions. For each segment, the market sizing and forecasts are provided based on volume (kilotons).

| By Grade | Technical Grade | ||

| Battery Grade | |||

| Industrial Grade | |||

| By Application | Li-ion Battery | ||

| Pharmaceuticals and Dental | |||

| Glass and Ceramics | |||

| Aluminum Production | |||

| Cement Industry | |||

| Other Applications | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Lithium Carbonate Market Research FAQs

How big is the Lithium Carbonate Market?

The Lithium Carbonate Market size is expected to reach 0.69 thousand LCE kilotons in 2025 and grow at a CAGR of 23.22% to reach 1.96 thousand LCE kilotons by 2030.

What is the current Lithium Carbonate Market size?

In 2025, the Lithium Carbonate Market size is expected to reach 0.69 thousand LCE kilotons.

Who are the key players in Lithium Carbonate Market?

Albemarle Corporation, SQM S.A., Ganfeng Lithium Group Co., Ltd, Tianqi Lithium Industry Co., Ltd and Arcadium Lithium are the major companies operating in the Lithium Carbonate Market.

Which is the fastest growing region in Lithium Carbonate Market?

North America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Lithium Carbonate Market?

In 2025, the Asia-Pacific accounts for the largest market share in Lithium Carbonate Market.

What years does this Lithium Carbonate Market cover, and what was the market size in 2024?

In 2024, the Lithium Carbonate Market size was estimated at 0.53 thousand LCE kilotons. The report covers the Lithium Carbonate Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Lithium Carbonate Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Lithium Carbonate Market Research

Mordor Intelligence provides a comprehensive analysis of the lithium carbonate industry. We leverage our extensive expertise in lithium mining and lithium processing research to deliver this detailed report. It examines the complete value chain, from lithium mineral extraction to the production of lithium compounds and lithium derivatives. The analysis includes Li2CO3 manufacturing processes, lithium salts formation, and the development of lithium chemicals for various applications. These applications encompass lithium battery materials and other lithium products.

Stakeholders gain crucial insights into lithium carbonate price trends and lithium mining industry dynamics through our detailed report. This report is available as an easy-to-download PDF. The analysis covers industrial lithium carbonate applications, lithium compounds market developments, and the growing demand for components for lithium batteries. Our research thoroughly examines the lithium derivatives market, lithium mining market size, and the evolving landscape of materials for lithium-ion batteries. It provides stakeholders with actionable intelligence for informed decision-making in this rapidly expanding sector.