Market Size of Liquid Roofing Industry

| Study Period | 2019 - 2029 |

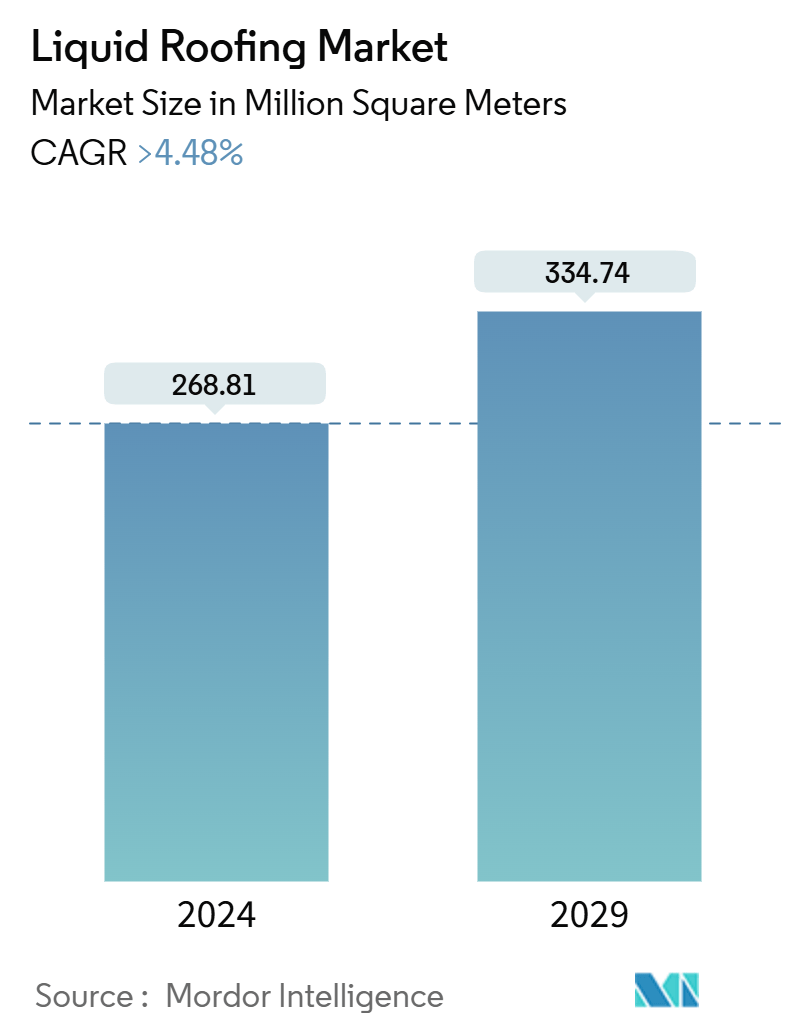

| Market Volume (2024) | 268.81 Million square meters |

| Market Volume (2029) | 334.74 Million square meters |

| CAGR (2024 - 2029) | > 4.48 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Liquid Roofing Market Analysis

The Liquid Roofing Market size is estimated at 268.81 Million square meters in 2024, and is expected to reach 334.74 Million square meters by 2029, at a CAGR of greater than 4.48% during the forecast period (2024-2029).

The initial impact of COVID-19 was a demand slump in the liquid roofing market in 2020. However, the market showed signs of recovery in 2021 and 2022, and the long-term outlook appears positive.

- Increasing construction and renovation activities and superior properties over existing alternatives drive the demand for the liquid roofing market.

- However, stringent building codes and regulatory standards may hinder the growth of the liquid roofing market in the near future.

- The growing demand for eco-friendly roofing solutions is likely to provide opportunities for the liquid roofing market over the next five years.

- The Asia-Pacific region dominates the liquid roofing market, owing to the increasing consumption of liquid roofing from countries like China, India, etc.

Liquid Roofing Industry Segmentation

Liquid roofing is a liquid material applied to a roof or top surface of a construction to create a watertight layer or membrane. It is highly used for flat roofs, pitched roofs, and, in some cases, domed roofs. Liquid roofing is mainly made from acrylics, polyurethane, bitumen, silicone, and epoxy materials and is used for roofs and top surfaces of residential, commercial, industrial, and institutional buildings and infrastructure.

Liquid roofing Market is segmented into type, application, end-user industry, and geography. By type, the market is segmented into polyurethane coatings, acrylic coatings, bituminous coatings, silicone coatings, epoxy coatings, and other types (modified silane polymers, liquid butyl rubber, elastomeric liquid coatings, and cementitious liquid membranes). By application, the market is segmented into domed roofs, pitched roofs, and flat roofs. By end-user industry, the market is segmented into residential, commercial, industrial/institutional, and infrastructure. The report also covers the market size and forecasts for the Liquid Roofing Market in 27 countries across the Asia-Pacific region. For each segment, the market sizing and forecasts were made on the basis of volume (square meters).

| Type | |

| Polyurethane Coatings | |

| Acrylic Coatings | |

| Bituminous Coatings | |

| Silicone Coatings | |

| Epoxy Coatings | |

| Other Types (Modified Silane Polymers, EPDM Rubbers, Elastomeric Membranes, Cementitious Membranes, and Epoxy Coatings) |

| Application | |

| Domed Roofs | |

| Pitched Roof | |

| Flat Roofed |

| End-user Industry | |

| Residential | |

| Commercial | |

| Industrial/Institutional | |

| Infrastructure |

| Geography | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

Liquid Roofing Market Size Summary

The liquid roofing market is poised for significant growth over the forecast period, driven by increasing consumer awareness of its benefits, such as extended lifespan, temperature regulation, and low maintenance requirements. The residential sector is the dominant segment, largely due to the extensive use of liquid roofing in construction. The market's expansion is supported by the growing need to reduce carbon footprints, which presents new opportunities. However, fluctuations in raw material costs pose potential challenges to market growth. The Asia-Pacific region leads the market, with countries like China and India contributing to the rising demand due to their robust construction and remodeling activities. The market is characterized by the adoption of silicone coatings, which offer advantages like weathering resistance and UV protection, making them a preferred choice over traditional roofing solutions.

The global construction industry's anticipated growth is a key driver for the liquid roofing market, with significant contributions from major economies such as China, India, the United States, and Indonesia. Government initiatives and infrastructure development plans in various countries are expected to further propel market expansion. The liquid roofing systems' durability, cost-effectiveness, and energy efficiency align with the increasing demand for sustainable building solutions. The market is partially fragmented, with major players like Kemper System Ltd, Johns Manville, GAF, Saint-Gobain Weber, and BASF SE leading the charge. Recent innovations, such as Langley's new PU Liquid Waterproofing system and BASF's partnership with Oriental Yuhong, highlight the industry's focus on enhancing product offerings to meet evolving market demands.

Liquid Roofing Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Drivers

-

1.1.1 Increasing Construction and Renovation Activities

-

1.1.2 Superior Properties Over Existing Alternatives

-

-

1.2 Restraints

-

1.2.1 Stringent Building Codes and Regulatory Standards

-

-

1.3 Industry Value Chain Analysis

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Suppliers

-

1.4.2 Bargaining Power of Buyers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products

-

1.4.5 Degree of Competition

-

-

-

2. MARKET SEGMENTATION (Market Size in Volume)

-

2.1 Type

-

2.1.1 Polyurethane Coatings

-

2.1.2 Acrylic Coatings

-

2.1.3 Bituminous Coatings

-

2.1.4 Silicone Coatings

-

2.1.5 Epoxy Coatings

-

2.1.6 Other Types (Modified Silane Polymers, EPDM Rubbers, Elastomeric Membranes, Cementitious Membranes, and Epoxy Coatings)

-

-

2.2 Application

-

2.2.1 Domed Roofs

-

2.2.2 Pitched Roof

-

2.2.3 Flat Roofed

-

-

2.3 End-user Industry

-

2.3.1 Residential

-

2.3.2 Commercial

-

2.3.3 Industrial/Institutional

-

2.3.4 Infrastructure

-

-

2.4 Geography

-

2.4.1 Asia-Pacific

-

2.4.1.1 China

-

2.4.1.2 India

-

2.4.1.3 Japan

-

2.4.1.4 South Korea

-

2.4.1.5 Malaysia

-

2.4.1.6 Thailand

-

2.4.1.7 Indonesia

-

2.4.1.8 Vietnam

-

2.4.1.9 Rest of Asia-Pacific

-

-

2.4.2 North America

-

2.4.2.1 United States

-

2.4.2.2 Canada

-

2.4.2.3 Mexico

-

-

2.4.3 Europe

-

2.4.3.1 Germany

-

2.4.3.2 United Kingdom

-

2.4.3.3 France

-

2.4.3.4 Italy

-

2.4.3.5 Spain

-

2.4.3.6 NORDIC Countries

-

2.4.3.7 Turkey

-

2.4.3.8 Russia

-

2.4.3.9 Rest of Europe

-

-

2.4.4 South America

-

2.4.4.1 Brazil

-

2.4.4.2 Argentina

-

2.4.4.3 Colombia

-

2.4.4.4 Rest of South America

-

-

2.4.5 Middle-East and Africa

-

2.4.5.1 Saudi Arabia

-

2.4.5.2 South Africa

-

2.4.5.3 Nigeria

-

2.4.5.4 Qatar

-

2.4.5.5 Egypt

-

2.4.5.6 UAE

-

2.4.5.7 Rest of Middle-East and Africa

-

-

-

Liquid Roofing Market Size FAQs

How big is the Liquid Roofing Market?

The Liquid Roofing Market size is expected to reach 268.81 million square meters in 2024 and grow at a CAGR of greater than 4.48% to reach 334.74 million square meters by 2029.

What is the current Liquid Roofing Market size?

In 2024, the Liquid Roofing Market size is expected to reach 268.81 million square meters.