| Study Period | 2019 - 2030 |

| Market Volume (2025) | 9.22 kilotons |

| Market Volume (2030) | 12.05 kilotons |

| CAGR | 5.50 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Films And Laminates Market Major Players")

Films And Laminates Market Size")

Liquid Crystal Polymer (LCP) Films & Laminates Market Analysis

The Liquid Crystal Polymer Films And Laminates Market size is estimated at 9.22 kilotons in 2025, and is expected to reach 12.05 kilotons by 2030, at a CAGR of greater than 5.5% during the forecast period (2025-2030).

The liquid crystal polymer films and laminates industry is experiencing significant transformation driven by the rapid evolution of the electronics sector. The global electronics industry has shown remarkable resilience, with Asia leading the growth at 10%, followed by America at 9%, and Europe at 7%. The deployment of 5G infrastructure has become a crucial driver, with countries like South Korea investing USD 451 billion in expanding semiconductor packaging material production capabilities. Major players like Sumitomo Chemical are developing specialized liquid crystal polymer variants with low dielectric loss tangent specifically designed for 5G applications, demonstrating the industry's commitment to advancing telecommunications technology.

The automotive sector's transition towards electrification has created new opportunities for liquid crystal polymer films and laminates manufacturers. The industry has witnessed a significant shift in manufacturing priorities, with several automotive manufacturers announcing substantial investments in electric vehicle production facilities. The semiconductor shortage has prompted regional governments to invest heavily in domestic chip production capabilities, with the European Union mobilizing 13 countries to jointly invest in processor and semiconductor packaging material technologies to reduce dependency on Asian markets.

The medical devices sector has emerged as a promising growth avenue for the liquid crystal polymer films and laminates market. According to industry projections, the global medical device sector is expected to witness steady growth, with annual sales anticipated to reach approximately USD 800 billion by 2030. The increasing focus on research in areas such as telemedicine, assistive technologies, and electronic monitoring equipment has created sustained demand for high-performance materials like liquid crystal polymer films and laminates, which offer excellent chemical resistance and sterilization compatibility.

The manufacturing landscape is witnessing a significant geographical shift, particularly in the ASEAN region, which has become a major hub for electrical and electronics manufacturing. The sector contributes approximately USD 268 billion to regional GDP and employs over 2.4 million people. Major investments are flowing into the region, exemplified by Foxconn Technology Group's USD 700 million investment in Vietnam and the establishment of new manufacturing facilities by global electronics giants. This regional manufacturing transformation is complemented by government initiatives like Production Linked Incentive (PLI) Schemes in countries such as Vietnam, Thailand, and India, creating new opportunities for established manufacturers to expand their presence in these emerging markets.

Liquid Crystal Polymer (LCP) Films & Laminates Market Trends

Increasing Demand for Miniaturization of Electrical and Electronic Components

The growing trend toward miniaturization in the electronics industry has become a significant driver for the liquid crystal polymer (LCP) films and laminates market. LCP films offer exceptional electrical and mechanical properties that are crucial for miniaturized electronic components, including a low dielectric constant, high moisture barriers, controllable thermal coefficient of expansion, and superior high-frequency properties. According to the Japan Electronics and Information Technology Industries Association (JEITA), the global electronics and IT industry production reached USD 3.43 trillion in 2022, with a projected growth to USD 3.52 trillion by 2023, indicating the massive scale of potential applications for LCP films in miniaturized components. The increasing complexity of electronic devices, coupled with demands for smaller form factors, has made LCP films indispensable in applications like printed circuit board materials, flexible substrates, substrates for heat-resistant labels, and electrical insulation films.

The miniaturization trend is particularly evident in the development of advanced electronic devices requiring high-performance microwave/millimeter-wave substrates and packaging materials. LCP films and laminates have emerged as ideal materials for these applications due to their unique combination of properties, including excellent dimensional stability and creep resistance at high temperatures. The material's ability to maintain stable performance in miniaturized configurations while offering superior thermal stability up to 250°C has made it essential for next-generation electronic devices. Furthermore, LCP's inherent flame-retardant characteristics without the need for additives have positioned it as an environmentally friendly solution for miniaturized electronic components, aligning with global sustainability initiatives in electronics manufacturing.

Understand The Key Trends Shaping This Market

Download PDF

Other Drivers

The adoption of LCP films and laminates has been significantly driven by their expanding applications in emerging technologies, particularly in 5G network infrastructure and advanced automotive electronics. LCP films' exceptional electrical properties, such as low moisture absorption and water vapor transmission rates, make them ideal for high-frequency applications in 5G technology. The material's superior performance in terms of signal integrity and thermal management has led to its increased adoption in antenna substrate materials and other critical 5G infrastructure components. Additionally, the automotive industry's shift toward electric and autonomous vehicles has created new opportunities for LCP films in advanced driver assistance systems (ADAS) and vehicle connectivity solutions.

The medical device sector has emerged as another significant driver for LCP films and laminates, particularly in applications requiring high precision and reliability. The material's biocompatibility, resistance to sterilization processes, and excellent barrier properties make it ideal for medical device components and packaging. Furthermore, the packaging industry has shown increasing interest in LCP films due to their superior barrier properties against oxygen, moisture, and other gases. The material's ability to maintain stability across a wide temperature range while providing excellent chemical resistance has made it particularly valuable in high-performance packaging applications. The combination of these diverse applications, coupled with LCP's unique property profile, continues to drive market growth across multiple industries, including the semiconductor packaging material market and the broader electronic film market.

Segment Analysis: TYPE

LCP Films Segment in Liquid Crystal Polymer Films and Laminates Market

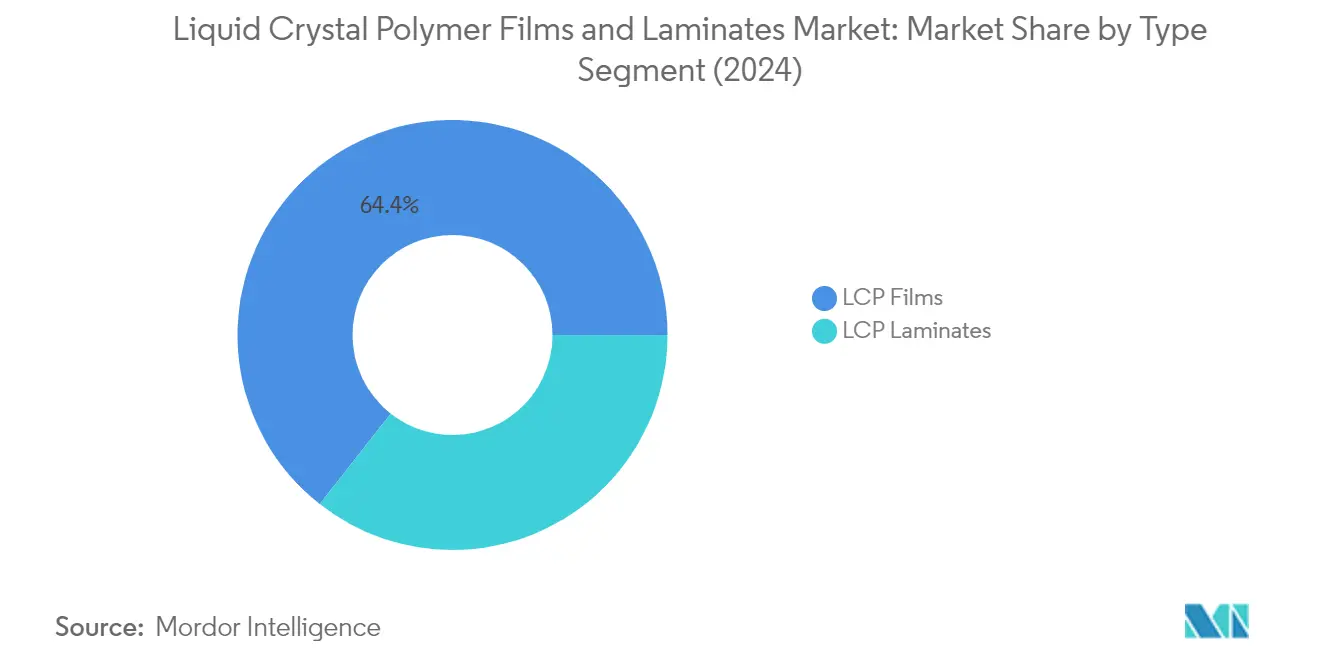

The LCP Films segment continues to dominate the global Liquid Crystal Polymer Films and Laminates market, holding approximately 64% of the total market share in 2024. This significant market position can be attributed to the segment's extensive application in electronics manufacturing, particularly in flexible printed circuits, substrates for heat-resistant labels, substrates for heat-resistant tape, electrical insulation films, and high gas barrier films. The segment's dominance is further strengthened by its exceptional properties, including low moisture absorption and water vapor transmission rates, which minimize many moisture-related problems encountered while using polyimide film as a circuit substrate. Additionally, LCP films' low coefficient of hygroscopic expansion (CHE) helps maintain stability and flatness during moisture level changes, making them particularly valuable in high-precision electronic applications.

LCP Laminates Segment in Liquid Crystal Polymer Films and Laminates Market

The LCP Laminates segment is projected to exhibit the fastest growth in the market during the forecast period 2024-2029, with an expected growth rate of approximately 6% annually. This accelerated growth is driven by the increasing demand for rigid Printed Circuit Boards (PCBs) across various industries. The segment's growth is further propelled by the rising preference for lightweight and sustainable materials in major end-use sectors such as automotive, packaging, and electronics. The segment's expansion is also supported by technological advancements that have paved the way for high-performance, long-lasting laminates that are environmentally friendly, have minimal maintenance costs, and improved performance qualities. The increasing adoption of copper-clad laminates in various electronic applications and the growing demand for high-frequency applications in 5G technology are also significant factors contributing to the segment's rapid growth.

Segment Analysis: APPLICATION

Electronics Segment in Liquid Crystal Polymer (LCP) Films and Laminates Market

The electronics segment dominates the global LCP films and laminates market, accounting for approximately 71% of the total market share in 2024. This significant market share is driven by the extensive use of LCP films and laminates in various electronic applications, including electronic films, substrates for heat-resistant labels, electrical insulation films, and high gas barrier films. The segment's dominance is further strengthened by the increasing demand for miniaturization of electrical and electronic components, particularly in smartphones, tablets, and other consumer electronics. The growing adoption of 5G technology has also boosted the demand for LCP films and laminates due to their excellent electrical properties, low dielectric constant, and superior performance in high-frequency applications. Additionally, the segment is experiencing robust growth with a projected growth rate of around 6% from 2024 to 2029, primarily driven by the expanding electronics manufacturing sector in Asia-Pacific and increasing investments in semiconductor and electronic component production globally.

Remaining Segments in LCP Films and Laminates Market by Application

The automotive and medical devices segments represent significant opportunities in the LCP films and laminates market. The automotive sector utilizes these materials in various applications, including in-vehicle millimeter-wave radar, automobile electronics, safety systems, and monitoring systems, with increasing adoption in both conventional and electric vehicles. The medical devices segment has gained prominence due to the materials' exceptional properties such as biocompatibility, chemical resistance, and ability to withstand various sterilization methods. Other applications include industrial waste bags, high barrier bags, and food packaging, though these represent a smaller portion of the overall market. The growth in these segments is supported by ongoing technological advancements and increasing demand for lightweight, durable materials across various end-use industries.

Liquid Crystal Polymer (LCP) Films And Laminates Market Geography Segment Analysis

Liquid Crystal Polymer (LCP) Films and Laminates Market in Asia-Pacific

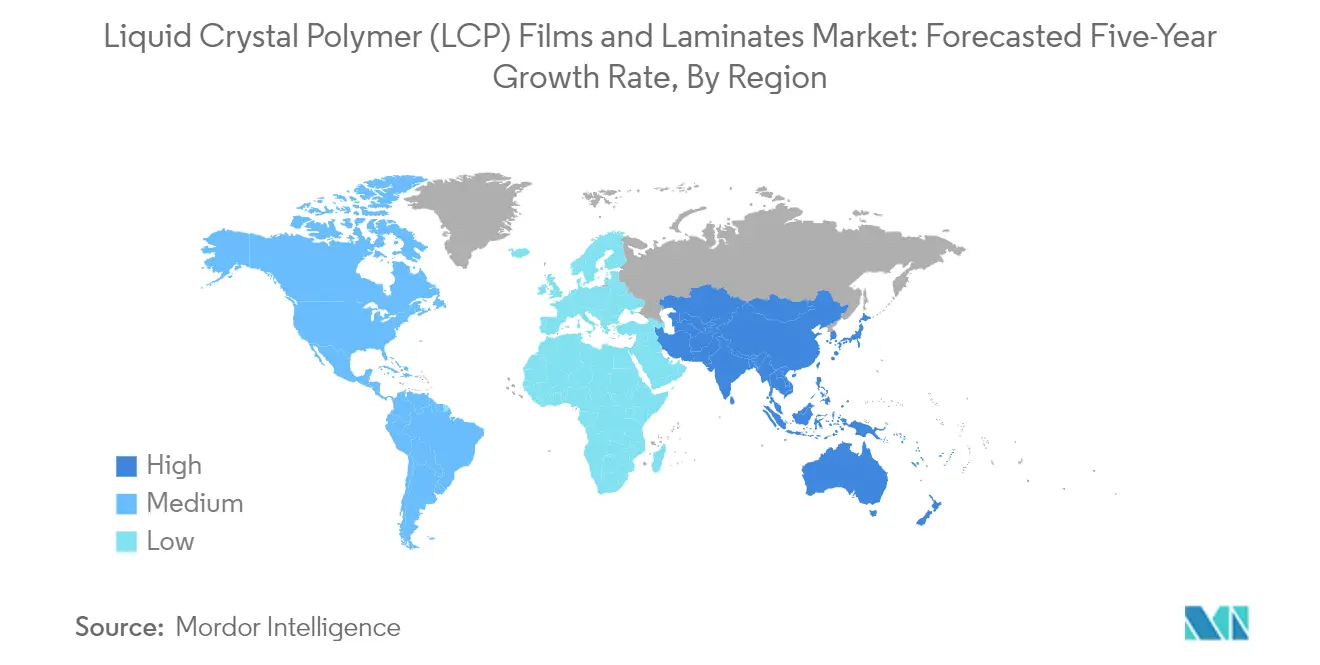

The Asia-Pacific region represents the largest and most dynamic market for liquid crystal polymer films and laminates, driven by the strong presence of electronics manufacturing, automotive production, and medical device industries. Countries like China, Japan, South Korea, and India form the backbone of this market, with each nation contributing uniquely through their specialized manufacturing capabilities and technological advancements. The region benefits from extensive supply chain networks, skilled workforce availability, and supportive government policies promoting high-tech manufacturing sectors. The presence of major electronics manufacturers and increasing adoption of 5G technology has further strengthened the market position of this region.

Liquid Crystal Polymer (LCP) Films and Laminates Market in China

China dominates the Asia-Pacific liquid crystal polymer films and laminates market, holding approximately 67% share of the regional market. The country's market leadership is supported by its massive electronics manufacturing base, being the world's largest producer of consumer electronics and telecommunications equipment. China's strength lies in its integrated supply chain network, advanced manufacturing capabilities, and significant investments in 5G infrastructure development. The country's focus on electric vehicle production and the government's push towards indigenous semiconductor manufacturing through initiatives has further reinforced its position in the market.

Liquid Crystal Polymer (LCP) Films and Laminates Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 7% during 2024-2029. The country's growth is driven by increasing electronics manufacturing activities, supported by government initiatives like "Make in India" and Production Linked Incentive (PLI) schemes. The expansion of domestic smartphone production, rising investments in 5G infrastructure, and a growing automotive electronics sector are key factors propelling market growth. India's position as an emerging manufacturing hub, coupled with increasing foreign direct investments in electronics manufacturing, presents significant opportunities for market expansion in the liquid crystal polymer market.

Liquid Crystal Polymer (LCP) Films and Laminates Market in North America

The North American market for liquid crystal polymer films and laminates is characterized by high technological adoption rates and a strong presence in high-end electronics and automotive applications. The region's market is driven by advanced manufacturing capabilities, robust research and development activities, and increasing demand for high-performance electronic components. The United States, Canada, and Mexico each contribute to the market's growth through their specialized industrial sectors and technological innovations.

Liquid Crystal Polymer (LCP) Films and Laminates Market in United States

The United States leads the North American market with approximately 86% share of the regional market. The country's dominant position is attributed to its advanced electronics manufacturing sector, strong presence in medical device production, and significant investments in 5G infrastructure. The US market benefits from extensive research and development activities, the presence of major technology companies, and growing demand for high-performance electronic components in various industries, including the flexible substrate market.

Liquid Crystal Polymer (LCP) Films and Laminates Market in United States

The United States also demonstrates the highest growth potential in North America, with an expected growth rate of approximately 5% during 2024-2029. This growth is driven by increasing adoption of advanced electronics in automotive applications, expanding 5G infrastructure, and growing demand for miniaturized electronic components. The country's focus on developing next-generation wireless technologies and increasing investments in semiconductor manufacturing capabilities further support market growth in the liquid crystal polymer market.

Liquid Crystal Polymer (LCP) Films and Laminates Market in Europe

The European market for liquid crystal polymer films and laminates is characterized by its strong focus on high-quality electronic components and automotive applications. The region's market dynamics are shaped by countries including Germany, the United Kingdom, France, and Italy, each contributing through their specialized industrial sectors. The market benefits from advanced manufacturing capabilities, strict quality standards, and increasing adoption of electric vehicles.

Liquid Crystal Polymer (LCP) Films and Laminates Market in Germany

Germany stands as the largest market for liquid crystal polymer films and laminates in Europe, driven by its robust automotive industry and strong electronics manufacturing sector. The country's market leadership is supported by its advanced manufacturing capabilities, significant investments in Industry 4.0 initiatives, and a strong presence of automotive OEMs. Germany's focus on electric vehicle production and increasing adoption of advanced electronics in automotive applications continue to drive market growth.

Liquid Crystal Polymer (LCP) Films and Laminates Market in Germany

Germany also leads in terms of growth rate in the European region, supported by its continuous technological advancements and investments in future technologies. The country's strong focus on developing electric vehicles, increasing adoption of 5G technology, and growing demand for high-performance electronic components in industrial applications drive market expansion. The presence of major automotive manufacturers and their increasing focus on electronic components further supports market growth, including the flexible copper clad laminate sector.

Liquid Crystal Polymer (LCP) Films and Laminates Market in South America

The South American market for liquid crystal polymer films and laminates is primarily driven by Brazil and Argentina's industrial sectors. The region's market is characterized by growing electronics manufacturing activities and increasing automotive production. Brazil emerges as both the largest and fastest-growing market in the region, supported by its expanding electronics manufacturing sector and increasing investments in automotive electronics. The market shows potential for growth through increasing industrial activities and technological advancement in manufacturing sectors.

Liquid Crystal Polymer (LCP) Films and Laminates Market in Middle East & Africa

The Middle East & Africa market for liquid crystal polymer films and laminates is experiencing growth through increasing industrialization and technological adoption. Saudi Arabia and South Africa represent key markets in the region, with Saudi Arabia emerging as both the largest and fastest-growing market. The region's growth is driven by increasing investments in electronics manufacturing, automotive sector development, and growing adoption of advanced technologies in industrial applications. Government initiatives to diversify economies and promote manufacturing sectors continue to support market expansion.

Get Analysis on Important Geographic Markets

Download PDF

Liquid Crystal Polymer (LCP) Films and Laminates Industry Overview

Top Companies in Liquid Crystal Polymer (LCP) Films and Laminates Market

The global liquid crystal polymer films and laminates industry is characterized by continuous product innovation and strategic expansion initiatives by key players. Companies are focusing on developing advanced liquid crystal polymer formulations with enhanced thermal, mechanical, and electrical properties to meet the evolving demands of electronics and automotive applications. Operational agility is demonstrated through vertically integrated manufacturing capabilities, allowing companies to maintain better control over the supply chain and quality standards. Strategic moves include capacity expansions, particularly in the Asia-Pacific region, to capitalize on the growing electronics manufacturing base. Market leaders are investing significantly in research and development to introduce new product grades and applications, while simultaneously strengthening their distribution networks across key regions to improve market penetration and customer service capabilities.

Consolidated Market with Strong Regional Players

The LCP films and laminates market exhibits a partially consolidated structure dominated by global chemical conglomerates with diverse product portfolios. These major players possess strong technological capabilities, established brand recognition, and extensive distribution networks spanning multiple continents. The market is characterized by the presence of both integrated manufacturers who produce their own LCP resins and specialized producers focusing solely on films and laminates production. Regional players, particularly in Asia-Pacific, maintain significant market shares in their respective territories through strong customer relationships and localized service capabilities.

The industry demonstrates moderate merger and acquisition activity, primarily driven by larger companies seeking to expand their technological capabilities and geographic presence. Market leaders are increasingly focusing on strategic partnerships and collaborations with end-users to develop customized solutions and secure long-term supply agreements. The high barriers to entry, including substantial capital requirements and technical expertise, have limited the emergence of new players, contributing to the market's consolidated nature. Companies with established positions are leveraging their expertise and resources to maintain their competitive advantage through continuous innovation and operational excellence.

Innovation and Customer Relations Drive Success

Success in the liquid crystal polymer films and laminates industry increasingly depends on companies' ability to innovate and maintain strong customer relationships. Incumbent players must focus on developing next-generation products with improved performance characteristics while simultaneously optimizing their production processes to maintain cost competitiveness. The ability to offer customized solutions, provide technical support, and maintain consistent quality standards is becoming increasingly critical for maintaining market share. Companies need to invest in sustainable manufacturing practices and develop eco-friendly products to align with growing environmental concerns and regulatory requirements.

For contenders looking to gain ground, specialization in specific applications or regional markets presents a viable strategy for market entry and growth. Building strong relationships with electronics manufacturers and automotive OEMs is crucial, as these industries represent significant end-user segments with high product quality requirements. The relatively low threat of substitution from alternative materials, due to LCP's unique property combination, provides stability for market participants. However, companies must remain vigilant about potential regulatory changes regarding chemical manufacturing and environmental protection, which could impact production costs and market dynamics. Success also depends on maintaining efficient supply chains and developing robust risk management strategies to address raw material price volatility and market uncertainties. Additionally, the role of semiconductor packaging materials and polymer laminate solutions is becoming increasingly important in meeting the demands of high-performance applications.

Liquid Crystal Polymer (LCP) Films & Laminates Market Leaders

-

Celanese Corporation

-

KURARAY CO. LTD.

-

Polyplastics Co. Ltd.

-

Sumitomo Chemical Advanced Technologies

-

Shanghai PERT Composites Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

_Films_and_Laminates_Market_-_Market_Concentration.webp)

Need More Details on Market Players and Competiters?

Download PDF

Liquid Crystal Polymer (LCP) Films & Laminates Market News

- August 2022: Polyplastics Co. Ltd. expanded its engineering thermoplastics portfolio and material supply capabilities at the K 2022 exhibition in Düsseldorf, Germany. With the expansion, the company increased its liquid crystal polymer (LCP) sales to Europe, the Middle East, Africa, and the Americas while making timely investments in capacity to better respond to market growth.

- January 2022: Sumitomo Chemical Co., Ltd. built additional production lines for its liquid crystal polymer (LCP) SUMIKASUPERTM at its Ehime Works in Japan. The capacity expansion was scheduled to be completed by the middle of 2023 and will help in increasing the production capacity by approximately 30%.

Liquid Crystal Polymer (LCP) Films & Laminates Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Increasing Demand for Miniaturization of Electrical and Electronic Components

- 4.1.2 Development of Lightweight Materials for Automobile Components

- 4.1.3 Other Drivers

-

4.2 Restraints

- 4.2.1 High Manufacturing and Processing Costs

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

-

5.1 Type

- 5.1.1 LCP Films

- 5.1.2 LCP Laminates

-

5.2 Application

- 5.2.1 Automotive and Transportation

- 5.2.2 Electronics

- 5.2.3 Medical Devices

- 5.2.4 Other Applications (Industrial Machinery, Packaging, etc.)

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Malaysia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Turkey

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Celanese Corporation

- 6.4.2 KGK Chemical Corporation

- 6.4.3 KURARAY CO. LTD.

- 6.4.4 Panasonic Industry Co., Ltd.

- 6.4.5 Polyplastics Co. Ltd.

- 6.4.6 Rogers Corporation

- 6.4.7 RTP Company

- 6.4.8 Sumitomo Chemical Advanced Technologies

- 6.4.9 Syensqo

- 6.4.10 Toray Industries Inc.

- 6.4.11 UENO FINE CHEMICALS INDUSTRY LTD.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Potential in Growth in ASEAN and India Electronics Market

- 7.2 Other Opportunities

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Liquid Crystal Polymer (LCP) Films & Laminates Industry Segmentation

Liquid crystal polymer (LCP) is an engineering plastic with a combination of high strength, modulus, and impact properties, flame retardance, resistance to a wide range of aggressive chemicals, shallow and tailorable coefficients of thermal expansion (CTE), excellent dimensional stability, thin-wall flowability, and unique processability.

The liquid crystal polymer (LCP) films and laminates market is segmented by type, application, and geography. By type, the market is segmented into LCP films and LCP laminates. By application, the market is segmented into automotive, electronics, medical devices, and other applications (industrial machinery, packaging, etc.). The report also covers the market size and forecasts for the liquid crystal polymer (LCP) films and laminates market in 22 countries across major regions.

For each segment, the market sizing and forecasts have been done based on Volume (tons).

| Type | LCP Films | ||

| LCP Laminates | |||

| Application | Automotive and Transportation | ||

| Electronics | |||

| Medical Devices | |||

| Other Applications (Industrial Machinery, Packaging, etc.) | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Indonesia | |||

| Malaysia | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Russia | |||

| Turkey | |||

| NORDIC Countries | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Liquid Crystal Polymer (LCP) Films & Laminates Market Research FAQs

How big is the Liquid Crystal Polymer Films And Laminates Market?

The Liquid Crystal Polymer Films And Laminates Market size is expected to reach 9.22 kilotons in 2025 and grow at a CAGR of greater than 5.5% to reach 12.05 kilotons by 2030.

What is the current Liquid Crystal Polymer Films And Laminates Market size?

In 2025, the Liquid Crystal Polymer Films And Laminates Market size is expected to reach 9.22 kilotons.

Who are the key players in Liquid Crystal Polymer Films And Laminates Market?

Celanese Corporation, KURARAY CO. LTD., Polyplastics Co. Ltd., Sumitomo Chemical Advanced Technologies and Shanghai PERT Composites Co. Ltd are the major companies operating in the Liquid Crystal Polymer Films And Laminates Market.

Which is the fastest growing region in Liquid Crystal Polymer Films And Laminates Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Liquid Crystal Polymer Films And Laminates Market?

In 2025, the Asia-Pacific accounts for the largest market share in Liquid Crystal Polymer Films And Laminates Market.

What years does this Liquid Crystal Polymer Films And Laminates Market cover, and what was the market size in 2024?

In 2024, the Liquid Crystal Polymer Films And Laminates Market size was estimated at 8.71 kilotons. The report covers the Liquid Crystal Polymer Films And Laminates Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Liquid Crystal Polymer Films And Laminates Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Liquid Crystal Polymer (LCP) Films And Laminates Market Research

Mordor Intelligence provides a comprehensive analysis of the liquid crystal polymer films and laminates industry. We leverage decades of expertise in technical materials research. Our extensive report covers the entire ecosystem, from LCP resin manufacturing to advanced applications in flexible printed circuit technology and semiconductor packaging material development. The analysis includes crucial segments such as electronic film applications, electromagnetic shielding film solutions, and flexible copper clad laminate innovations. Detailed insights are available in an easy-to-read report PDF format, ready for download.

This strategic industry assessment offers stakeholders essential insights into thermotropic liquid crystal polymer applications, flexible substrate technologies, and emerging antenna substrate material developments. The report examines various uses of polymer laminate technologies in printed circuit board material manufacturing. It also analyzes the evolving landscape of semiconductor packaging material market dynamics. Our comprehensive coverage aids businesses in navigating the complexities of electronic film market trends and flexible substrate market opportunities. This is supported by a detailed analysis of liquid crystal polymer market developments across global regions.