Life Sciences Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

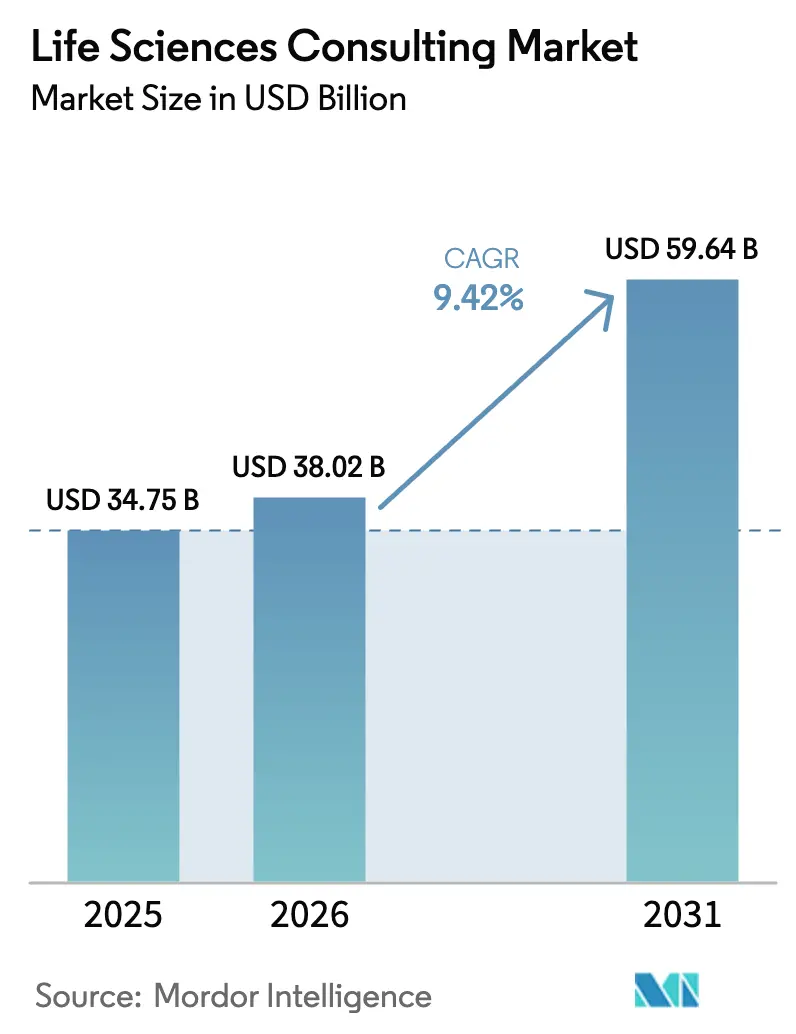

| Market Size (2026) | USD 38.02 Billion |

| Market Size (2031) | USD 59.64 Billion |

| Growth Rate (2025 - 2030) | 9.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Life Sciences Consulting Market Analysis by Mordor Intelligence

The Life Sciences Consulting Market size is expected to grow from USD 34.75 billion in 2025 to USD 38.02 billion in 2026 and is forecast to reach USD 59.64 billion by 2031 at 9.42% CAGR over 2026-2031.

Heightened regulatory complexity, the rapid rollout of generative AI across discovery and development, and mounting pressure to demonstrate real-world value are accelerating spending on external expertise. Pharmaceutical sponsors are channeling more workstreams to consultants, so internal teams can focus on pipeline execution, while biotechnology startups draw on advisory partners to compensate for lean in-house capabilities. Progress in cell and gene therapies, the rise of outcome-based reimbursement, and surging global M&A activity are further broadening the scope of high-value advisory mandates. At the same time, remote collaboration models are reshaping delivery economics, enabling firms to blend specialist knowledge from multiple geographies into a single engagement and to curb travel-related costs.

Key Report Takeaways

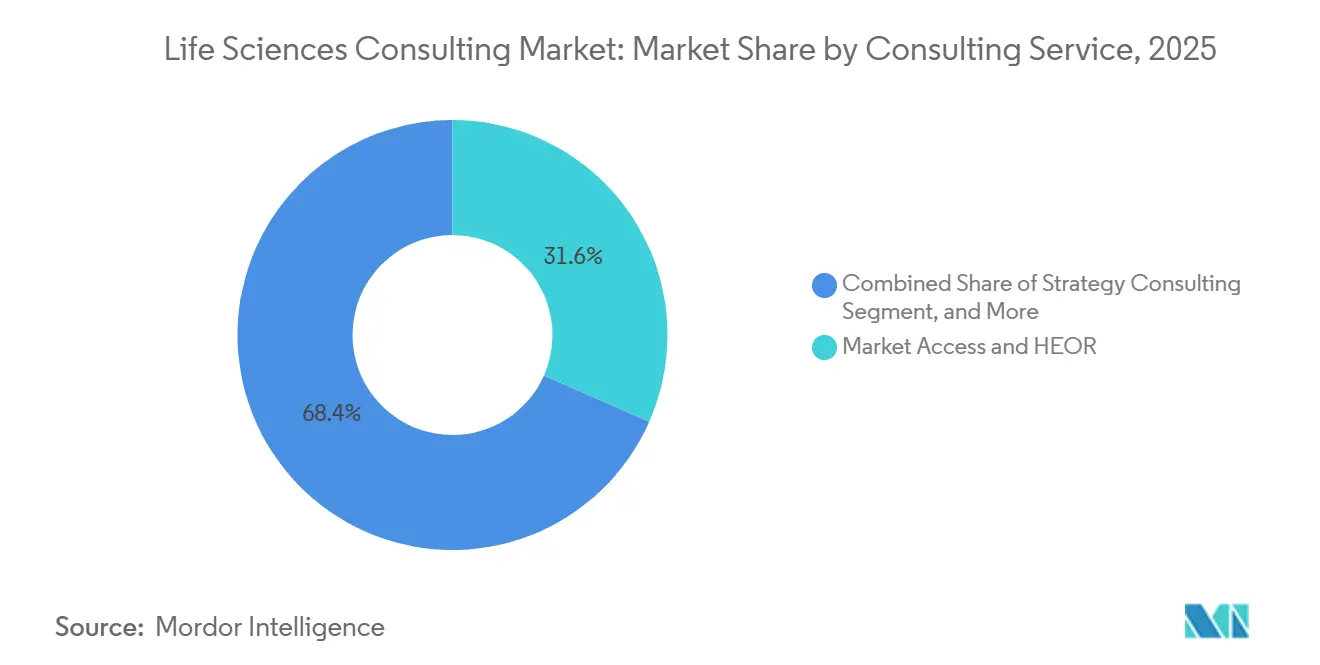

- By consulting service function, Market Access and Health Economics and Outcomes Research commanded 31.62% revenue share in 2025, whereas Real-World Evidence consulting is advancing at a 10.43% CAGR through 2031.

- By end-user, pharmaceutical companies held 40.62% of the life sciences consulting market share in 2025, while biotechnology companies are projected to expand at a 10.12% CAGR through 2031.

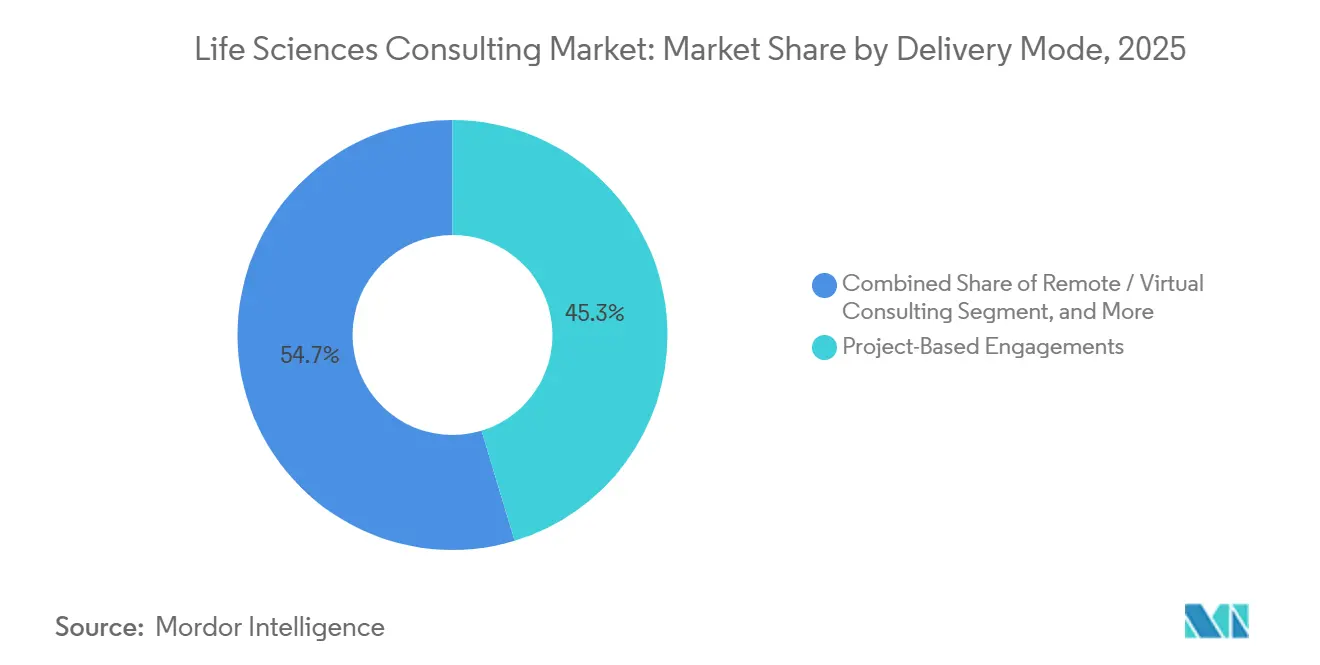

- By delivery mode, project-based engagements accounted for 45.32% of 2025 revenue, and remote consulting is forecast to grow at a 10.06% CAGR through 2031.

- By therapeutic area, oncology accounted for 37.32% of 2025 spending, and infectious diseases consulting is on track for a 10.17% CAGR through 2031.

- By geography, North America accounted for 54.76% of 2025 revenue, while Asia-Pacific is projected to grow at a 10.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Life Sciences Consulting Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI and GenAI Implementation Projects | +2.8% | Global, concentrated in North America and Europe | Medium term (2–4 years) |

| Expansion of Real-World Evidence Analytics for Market Access | +2.3% | Global, notable in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Growing Demand for Advanced Therapies Consulting | +1.9% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Increasing M&A Activity Driving Due-Diligence Support | +1.5% | Global, led by North America | Short term (≤ 2 years) |

| Regulatory Modernization Increasing Pathway Complexity | +1.2% | Global | Medium term (2–4 years) |

| Shift Toward Direct-to-Consumer Channel Strategy Advisory | +0.9% | North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in AI and GenAI Implementation Projects

Life-science companies are embedding generative AI across target identification, protocol design, and regulatory documentation, and they increasingly need consultants who can validate algorithm outputs against Good Manufacturing Practice and Good Clinical Practice standards. The U.S. Food and Drug Administration issued guidance in January 2025 on AI applications in drug manufacturing, providing clearer guardrails that have spurred enterprise adoption. Leading advisory firms report double-digit growth in AI-focused bookings as sponsors look for end-to-end support, including data engineering, model governance, and submission readiness reviews.[1]Accenture, “Fiscal 2025 Annual Report,” accenture.com Europe is taking a similar path, with the European Medicines Agency running a pilot program to assess AI-generated clinical study. Together, these moves are cementing AI implementation consulting as a premium, capability-intensive service line within the life sciences consulting market.

Expansion of Real-World Evidence Analytics for Market Access

Health technology assessment bodies now accept observational data for reimbursement, prompting a pivot from classic health economics models to large-scale patient-level analytics. The National Institute for Health and Care Excellence updated its methods guide in 2024 to formally include real-world evidence.[2]National Institute for Health and Care Excellence, “NICE Methods Guide Update 2024,” nice.org.uk Consulting practices are reacting by acquiring electronic health record aggregators and text-mining vendors that can extract structured insights from clinical notes. Firms with depth in biostatistics and epidemiology are winning multi-year programs that marry causal inference designs with payer-ready economic modeling, especially in oncology and rare diseases. European Medicines Agency guidance published in September 2024 strengthened this momentum, encouraging international clients to line up consulting partners early in development.

Growing Demand for Advanced Therapies Consulting

Cell and gene therapy approvals in the United States jumped to 16 in 2024, intensifying the need for Chemistry, Manufacturing, and Controls expertise alongside outcomes-based reimbursement design. Consulting firms are recruiting former regulators and vector manufacturing specialists to steer clients through emerging standards on viral vector potency, chain-of-custody traceability, and confirmatory evidence collection. Advisory work now extends to payer negotiations that balance multimillion-dollar treatment prices against durable efficacy, requiring multidisciplinary teams spanning regulatory affairs, health economics, and actuarial science. Dedicated advanced-therapy practices launched by leading consultancies in 2025 illustrate the expanding revenue pool for niche technical support.

Increasing M&A Activity Driving Due-Diligence Support

Biopharmaceutical deal value reached USD 156 billion in 2024, and buyers are requesting deeper diligence on regulatory risk, payer acceptance, and real-world effectiveness to justify valuations. Consultants are integrating AI screening of clinical trial registries and claims datasets to benchmark pipeline assets, identify comparator standards, and forecast peak-sales erosion scenarios.[3]Deloitte, “Life Sciences Procurement Survey 2025,” deloitte.com Post-acquisition, the same advisors orchestrate integration of commercial footprints and digital platforms, anchoring clients’ synergy capture plans. This deal wave looks set to reinforce the life sciences consulting market through at least 2027, even as overall capital market volatility persists.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| In-house Capability Building by Large Pharma | -1.8% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Intensifying Price Compression from Multi-Sourcing | -1.3% | Global | Medium term (2–4 years) |

| Data-Security and Privacy Concerns in Data-Heavy Projects | -0.9% | Global, acute in Europe | Short term (≤ 2 years) |

| Shortage of AI-Native Life-Sciences Talent | -0.7% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

In-house Capability Building by Large Pharma

Blue-chip pharmaceutical groups are poaching senior consultants and purchasing boutique advisory firms to internalize strategic planning and analytics. Pfizer’s internal consulting unit, launched in 2024 with 35 hires from top firms, exemplifies the shift toward self-reliance.[4]Pfizer, “Internal Consulting Group Establishment,” pfizer.com Market access and real-world analytics are especially vulnerable, as sponsors seek perpetual control over payer negotiations and value dossiers. Consultants are pivoting toward projects that demand external validation, specialized regulatory knowledge, or proprietary data assets, but the structural headwind remains significant across the life sciences consulting market.

Intensifying Price Compression from Multi-Sourcing

Procurement functions are disaggregating large transformation programs into discrete work packages awarded to multiple vendors, amplifying price pressure. A 2025 survey found that 62% of life-science companies now deploy three or more consultancies on flagship initiatives. Modular contracting limits cross-sell opportunities and curbs scale efficiencies that historically underpinned premium pricing. Some advisors are experimenting with outcome-based arrangements, yet client appetite remains patchy due to the operational complexity involved. Aggregate fee rates, therefore, face a structural squeeze even as overall demand climbs.

Segment Analysis

By Consulting Service Function: Real-World Evidence Pulls Ahead

Real-World Evidence engagements delivered a 10.43% CAGR through 2031, surpassing legacy health economics models as sponsors and payers coalesce around longitudinal data to substantiate product value. Market Access and HEOR consulting still led with a 31.62% life sciences consulting market share in 2025, but its growth is moderating as real-world analytics overtakes traditional scenario modeling. Firms boasting proprietary patient registries and natural language processing engines are edging out rivals on complex oncology and immunology projects that require causal inference designs. The life sciences consulting market size attributed to Real-World Evidence offerings is therefore projected to climb steadily, anchoring many multi-year managed services contracts.

Strategy, regulatory, and digital transformation advisory continues to underpin the broader service function mix. Regulatory affairs work is growing around accelerated approval dossiers, while operations consultants tackle supply-chain resilience improvements triggered by pandemic disruptions. Technology teams are embedding cloud-native clinical trial platforms, further intertwining IT implementation with core advisory recommendations. This convergence underscores how data-centric capabilities will dominate future competitive differentiation inside the life sciences consulting industry.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Venture-Backed Biotech Fuels Expansion

Pharmaceutical companies accounted for 40.62% of 2025 spending, reflecting their scale and the omnipresent pipeline challenges. However, biotechnology clients represent the fastest-growing pool, expanding at a 10.12% CAGR as USD 38 billion in 2024 venture funding translates into accelerated regulatory and market-access workstreams. The life sciences consulting market size accruing to early-stage biotechs is set to widen as new capital enters cell, gene, and RNA modalities. Advisory teams must therefore craft full-lifecycle programs, ranging from Investigational New Drug submissions to global launch planning, unlike the modular mandates typical in large pharma.

Medical device manufacturers and healthcare providers are forming smaller but growing segments, mainly through software-as-a-medical-device filings and real-world data infrastructure projects linked to value-based care. Consultants that can transpose drug-side expertise into medical technology workflows are positioned to capture these adjacencies. Overall, the diversification of end-user demand reinforces resilience in the broader life sciences consulting market.

By Delivery Mode: Remote Engagement Models Normalize

Project-based scopes still held 45.32% share in 2025, yet remote consulting grew at a 10.06% CAGR as pandemic-era digital collaboration became entrenched. More than two-thirds of 2025 engagements blended virtual delivery with limited on-site presence, proof that distributed workforces can meet regulatory and client security thresholds. The life sciences consulting market for fully remote models will expand further as cloud collaboration platforms integrate secure data-room functionality.

Managed services are also scaling, especially for pharmacovigilance monitoring and regulatory intelligence. These long-term contracts stabilize revenue and improve utilization, allowing firms to redeploy high-cost specialists to new project starts. Remote staffing widens access to niche therapeutic-area experts, a competitive necessity as advanced therapies proliferate. Nonetheless, facility inspections and due diligence walkthroughs still require in-person visits, ensuring a hybrid approach endures.

Note: Segment shares of all individual segments available upon report purchase

By Therapeutic Area: Infectious Diseases Gains Momentum

Oncology consulting accounted for 37.32% of 2025 spend, driven by complex biomarker strategies and intense payer scrutiny of high-priced immunotherapies. However, infectious-disease mandates are expanding at a 10.17% CAGR as pandemic preparedness funds spur vaccine and antiviral pipelines. The life sciences consulting market share tied to infectious diseases, therefore, looks set to widen, especially for manufacturing readiness assessments and expedited regulatory submissions.

Immunology and metabolic disorder projects also trend upward amid a raft of autoimmune biologics and obesity therapeutics. Cross-indication synergies allow consultants to port methodological playbooks between fields, strengthening utilization. Meanwhile, oncology retains a premium fee profile because of the stringent confirmatory evidence required under accelerated approval frameworks and increasing reliance on real-world data to support outcomes-based reimbursement.

Geography Analysis

North America generated 54.76% of 2025 revenue, underpinned by U.S. regulatory leadership and the dense cluster of biopharmaceutical headquarters. Former FDA officials now populate many consulting benches, providing clients with nuanced submission strategies that resonate globally. The region’s venture-capital ecosystem also funnels early-stage mandates into advisory pipelines, while large pharma sustains a baseline of transformation work.

Asia-Pacific is forecast to grow at a 10.54% CAGR through 2031, reflecting China’s ambitions to become a discovery hub and India’s expansion of clinical trial capacity. China’s National Medical Products Administration approved 48 innovative drugs in 2024, driving consulting demand for local regulatory navigation. Firms are doubling staff in Shanghai and Singapore to advise multinationals on market entry, pricing corridors, and post-approval surveillance. As local biotech start-ups secure capital, domestic advisory needs span Chemistry, Manufacturing, and Controls planning, reimbursement dossier development, and cross-border licensing assessments.

Europe remains a core market centered on Germany, the United Kingdom, and France, where European Medicines Agency submissions and health technology assessment negotiations sustain steady advisory volumes. Harmonization initiatives launched after the agency’s relocation to Amsterdam aim to streamline pan-EU requirements, indirectly tempering the need for country-specific consulting. South America and the Middle East and Africa are emerging, propelled by regulatory reforms such as Brazil’s 2024 accelerated review pathways that shorten time-to-approval for priority therapies. Collectively, the geographic diversification of client spend mitigates cyclical shocks in any single region.

Competitive Landscape

Life-sciences consulting remains moderately fragmented, with Big Four accounting firms, global strategy houses, and pure-play specialists each controlling distinct service niches. Accenture, Deloitte, and IQVIA continue to scale proprietary AI engines and patient-level datasets, widening their differentiation in regulatory automation and real-world evidence analytics. Deloitte’s 2025 collaboration with Microsoft to deploy Azure-native trial optimization tools exemplifies the convergence of technology and advisory services.

IQVIA maintains a defensible moat through its longitudinal database covering over 1 billion individuals, enabling unparalleled observational study design and payer submissions. Smaller firms such as Certara and L.E.K. Consulting exploit white spaces in biosimulation and direct-to-consumer strategy, respectively, by embedding data scientists and former payer executives into project teams. Boutiques with deep advanced-therapy know-how are in high demand as sponsors race to commercialize cell and gene pipelines.

AI-native entrants are a rising threat, automating document generation and site-selection algorithms at lower cost. However, rigorous data-governance requirements create entry barriers, favoring established firms that hold ISO-27001 certifications and mature security processes. Strategic alliances with cloud hyperscalers and electronic health record vendors are multiplying, giving consultancies access to compute, de-identified data, and embedded analytics that clients cannot easily replicate internally. Overall, sustained investment in proprietary platforms and specialized talent will determine future share gains inside the life sciences consulting market.

Life Sciences Consulting Industry Leaders

Accenture Plc

McKinsey & Company

IQVIA Holdings Inc.

Parexel International Corporation

Deloitte

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Deloitte expanded its life-sciences consulting practice in Singapore, adding 85 professionals focused on Southeast Asian regulatory strategy and market access.

- December 2025: IQVIA acquired a European health-economics consultancy, bringing 120 specialists into its practice.

- November 2025: Accenture partnered with a cloud hyperscaler to build AI-driven regulatory submission tools that cut report preparation time by 30%.

- November 2025: Accenture partnered with a cloud hyperscaler to build AI-driven regulatory submission tools that cut report preparation time by 30%.

- October 2025: McKinsey created an advanced-therapies consulting unit staffed by 15 former FDA officials.

Global Life Sciences Consulting Market Report Scope

The Life Sciences Consulting Market Report is Segmented by Consulting Service Function (Strategy Consulting, Operations Consulting, IT and Digital Transformation Consulting, Regulatory Affairs Consulting, Market Access and HEOR Consulting), End-user (Pharmaceutical Companies, Biotechnology Companies, Medical Device Manufacturers, Healthcare Providers), Delivery Mode (Project-Based Engagements, Managed Services, Remote/Virtual Consulting), Therapeutic Area (Oncology, Immunology, Metabolic Disorders, Infectious Diseases), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| IT and Digital Transformation Consulting |

| Regulatory Affairs Consulting |

| Market Access and HEOR Consulting |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Medical Device Manufacturers |

| Healthcare Providers |

| Project-Based Engagements |

| Managed Services |

| Remote / Virtual Consulting |

| Oncology |

| Immunology |

| Metabolic Disorders |

| Infectious Diseases |

| North America | United States |

| Canada | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Consulting Service Function | Strategy Consulting | |

| Operations Consulting | ||

| IT and Digital Transformation Consulting | ||

| Regulatory Affairs Consulting | ||

| Market Access and HEOR Consulting | ||

| By End-user | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Medical Device Manufacturers | ||

| Healthcare Providers | ||

| By Delivery Mode | Project-Based Engagements | |

| Managed Services | ||

| Remote / Virtual Consulting | ||

| By Therapeutic Area | Oncology | |

| Immunology | ||

| Metabolic Disorders | ||

| Infectious Diseases | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected size of the life sciences consulting market by 2031?

The market is forecast to reach USD 59.64 billion by 2031.

Which consulting service function is growing the fastest?

Real-World Evidence consulting is advancing at a 10.43% CAGR through 2031.

Why are biotechnology companies driving consulting demand?

Venture funding of USD 38 billion in 2024 has accelerated biotech pipelines, and startups need external expertise for regulatory filings and market access.

How is remote consulting changing delivery models?

Around 68% of projects in 2025 used at least some virtual delivery, cutting travel costs and widening access to specialist talent.

Which geography offers the highest growth rate?

Asia-Pacific is expanding at a 10.54% CAGR thanks to China’s regulatory progress and India’s clinical-trial infrastructure.

What competitive edge do leading firms hold?

Proprietary patient databases, AI-enabled platforms, and ISO-certified data-security frameworks help leading consultancies secure high-value mandates.