Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

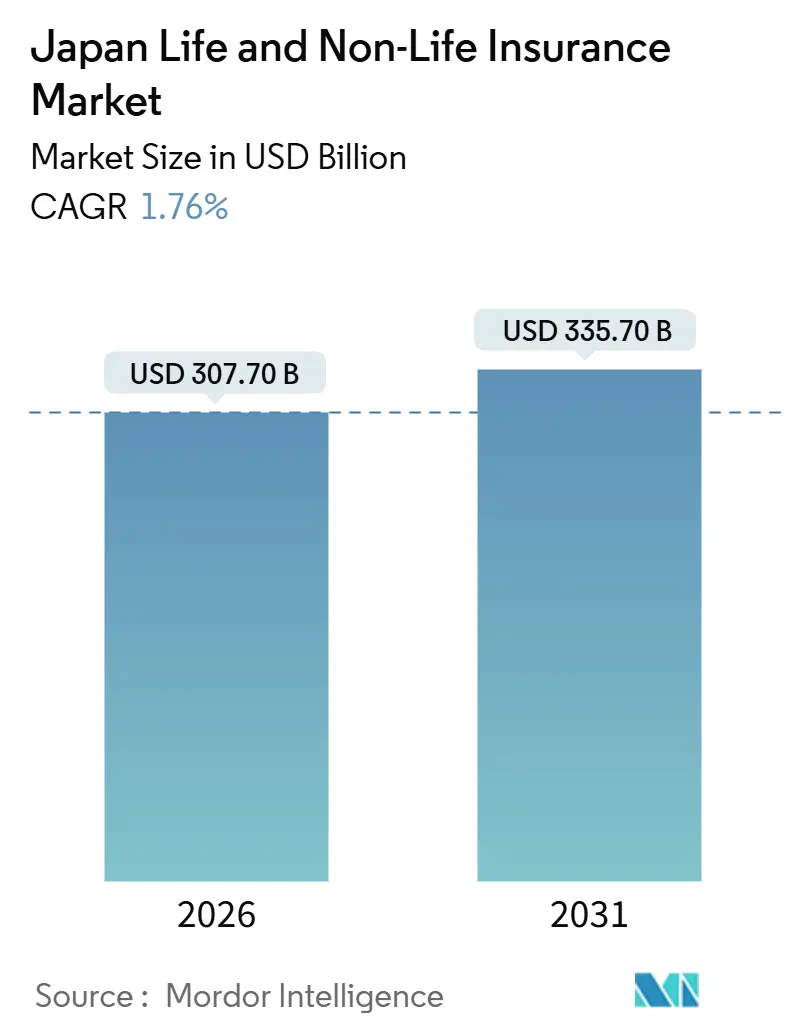

| Market Size (2026) | USD 307.70 Billion |

| Market Size (2031) | USD 335.70 Billion |

| Growth Rate (2026 - 2031) | 1.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Life And Non-Life Insurance Market Analysis by Mordor Intelligence

Japan's life and non-life insurance market is expected to grow from USD 307.7 billion in 2026 to USD 335.71 billion by 2031, with a CAGR of 1.76%. An aging population, with a significant portion aged 65 or older, drives demand for life, health, nursing care, and post-retirement income products. Policy rate normalization since 2024 has revitalized savings-type life products, as insurers can now invest in yen assets with yields better aligned to assumed rates, improving product economics and competitiveness[1]Bank of Japan, “Change in the Guideline for Money Market Operations,” Bank of Japan, boj.or.jp. Regulatory changes, including the transition to an economic value-based solvency framework and a 2025 shift in agent incentive supervision emphasizing customer outcomes, are enhancing market confidence. Natural disasters such as earthquakes, typhoons, and floods sustain non-life insurance demand and encourage investments in reinsurance and catastrophe risk transfer. Technology adoption has accelerated in underwriting, claims, and service operations, with financial institutions leveraging conventional and generative AI to improve efficiency. However, direct customer-facing AI deployment remains limited due to explainability and accuracy concerns.

Key Report Takeaways

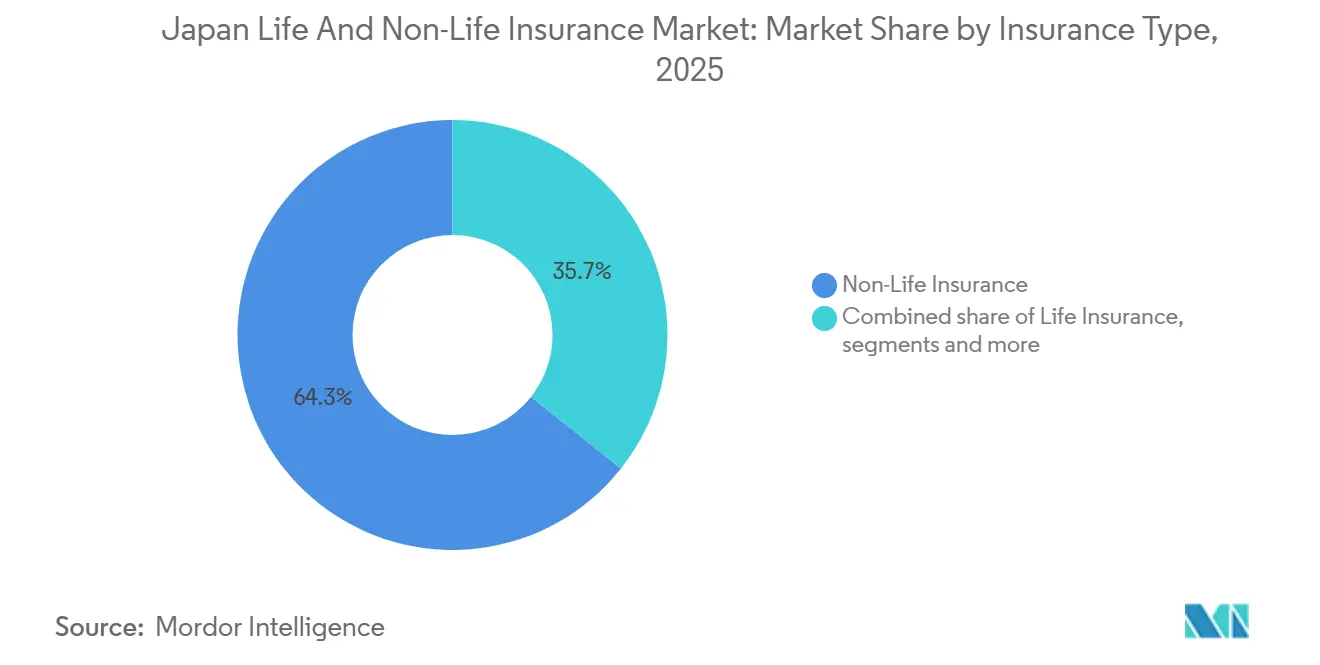

- By insurance type, non-life led with 64.34% of the Japan life and non-life insurance market share in 2025, while life insurance is projected to expand at a 2.65% CAGR through 2031.

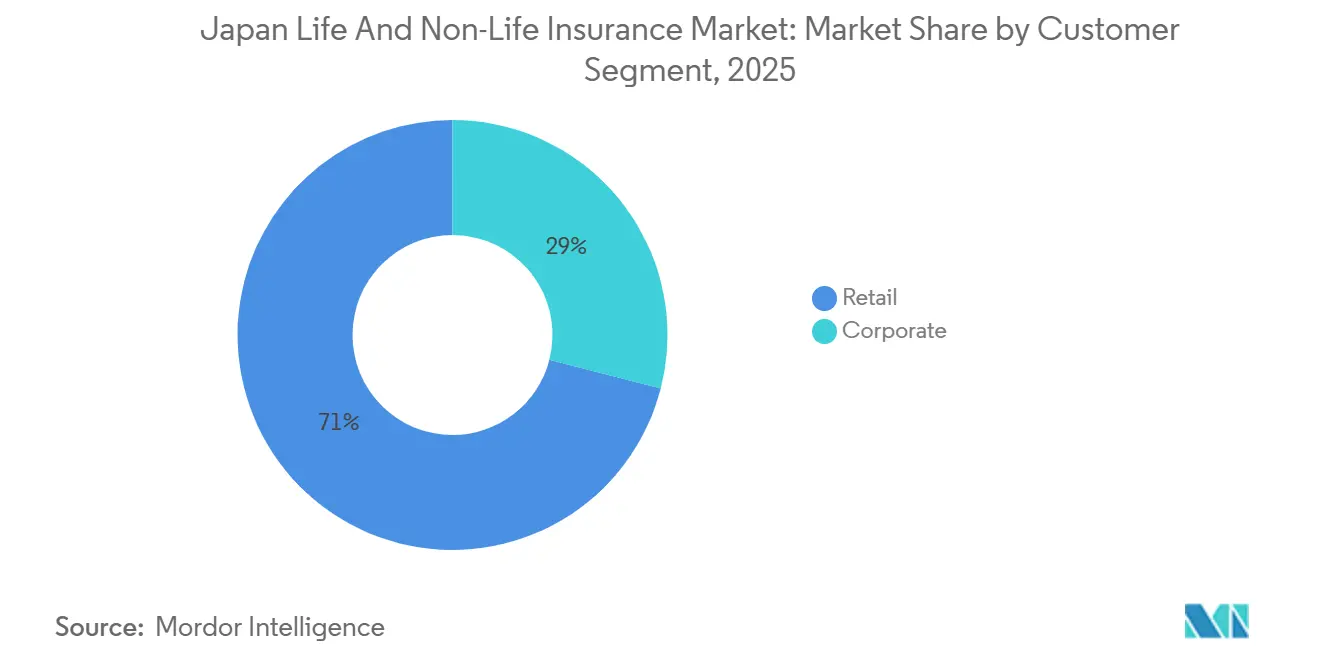

- By customer segment, retail held a 71% of the Japan life and non-life insurance market share in 2025, while corporate is forecast to grow at a 3.78% CAGR through 2031.

- By distribution channel, brokers and agents accounted for 87.65% of the Japan life and non-life insurance market share in 2025, while direct sales are expected to advance at a 3.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Life And Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Super-aged population and increasing longevity are raising demand for life, medical, nursing care, and annuity products | +0.8% | National, with concentrated demand in urban prefectures and high centenarian ratios in western regions | Long term (≥ 4 years) |

| Growing retirement and long-term care needs beyond public pension and health systems | +0.5% | National, with acute pressure in municipalities facing fiscal strain | Long term (≥ 4 years) |

| High insurance penetration and a strong role of life insurance in household financial planning | +0.2% | National: a large share of household assets in insurance and pensions | Medium term (2-4 years) |

| High exposure to earthquakes, typhoons, and floods is sustaining demand for property and catastrophe coverage | +0.4% | National core, with the highest risk concentration in Pacific coastal zones and metropolitan areas | Short term (≤ 2 years) |

| Strong FSA risk-based supervision and solvency monitoring supporting confidence and stability | +0.1% | National; FSA jurisdiction across the regulated sector | Medium term (2-4 years) |

| Product diversification into flexible protection, health, and retirement solutions tailored to demographic change | +0.3% | National, with early adoption by major life insurers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Super-Aged Population and Increasing Longevity Raising Demand for Life, Medical, Nursing Care, and Annuity Products

Japan is already a super-aged society, and the share of older adults is rising, which supports steady demand for life, medical, nursing care, and annuity offerings. The Cabinet Office projects the elderly share will continue to increase, which shifts household financial planning toward income longevity, health-related contingencies, and care needs that last decades. This demographic structure widens the gap between desired retirement income and public benefits, which heightens the role of private annuities and long-duration protection in the Japan life and non-life insurance market. The number of individual annuity policies in force and the amount in force increased in fiscal 2024, signalling renewed household preference for guaranteed income products as interest rates normalize[2]The Life Insurance Association of Japan, “Life Insurance Fact Book 2025,” The Life Insurance Association of Japan, seiho.or.jp. Household interest in product features that adjust income upon major health events remains strong, and many consumers indicate openness to annuities and critical illness coverage that link benefits to health status, which aligns product design with the realities of longer lives. Aging also raises the need for wellness and prevention services that help extend healthy life expectancy, which encourages insurers to combine protection with health engagement tools in the Japan life and non-life insurance market.

High Exposure to Earthquakes, Typhoons, And Floods Sustaining Demand for Property and Catastrophe Coverage

Japan’s location along the Pacific Ring of Fire drives constant attention to earthquakes and related perils, and the government-backed household earthquake scheme continues to underpin resilience in the property line. Penetration of household earthquake coverage attached to fire policies is high, and the government’s pooling mechanism limits private sector burdens at defined layers, which stabilizes underwriting outcomes in severe events. Historical payouts for major earthquakes and recent regional events highlight the concentration of risk and the importance of robust catastrophe modelling and reinsurance for both household and commercial exposures in the Japan life and non-life insurance market. Urban flood risk adds another layer of exposure, and updated analysis of low-lying wards in the Tokyo metropolitan area has reinforced the need for granular hazard mapping and preventive measures that reduce loss severity. Supervisory scenario analysis led by the FSA and industry groups has found increasing acute physical risks as climate change progresses, which keeps capital management and risk transfer central to non-life strategies in the Japan life and non-life insurance market. These risk dynamics push carriers to refine pricing, adopt parametric features, and maintain diversified reinsurance programs to protect balance sheets against clustered events.

Strong FSA Risk-Based Supervision and Solvency Monitoring Supporting Confidence and Stability

Regulatory modernization is a defining feature of the current cycle, and the FSA’s move to an economic value-based solvency framework from fiscal 2026 aligns Japan with global best practices on capital adequacy. The framework reflects market-consistent valuation of assets and liabilities and links quantitative capital standards to governance and disclosure expectations, which tightens the feedback loop between risk appetite and capital deployment. International convergence has advanced as well, with alignment to the Insurance Capital Standard that supports comparability for internationally active groups based in Japan[3]International Association of Insurance Supervisors, “Insurance Capital Standard Economic Impact Assessment Report,” IAIS, iais.org. Independent assessments have found broad observance of core supervisory principles and recommended further shifts toward proactive, risk-based inspection patterns, which the FSA has already begun to emphasize in its monitoring cycle. Distribution oversight is also tightening, and 2025 supervisory updates prohibit excessive conveniences to agents and recalibrate commissions toward customer-oriented quality, which aligns incentives with suitability and fairness goals in the Japan life and non-life insurance market. The regulator’s AI discussion paper clarifies expectations for explainability and data governance while highlighting the strategic risk of inaction, which sets guardrails for safe adoption of AI in underwriting, claims, and service processes.

Product Diversification into Flexible Protection, Health, and Retirement Solutions Tailored to Demographic Change

Product design is evolving toward blended value propositions that combine protection, savings, and wellness, which matches consumer preferences in a super-aged society. Annualized premiums for the third sector, which includes health, specified disease, long-term care, and premium waiver benefits, increased in fiscal 2024 for both policies in force and new business, showing the resilience of need-based protection. Insurers are integrating rewards for healthy behaviours through wearables, medical checkups, and app-based engagement to encourage preventive care and connect underwriting with risk mitigation in the Japan life and non-life insurance market. The interest rate backdrop supports savings-type life products, and Japan Post Insurance increased assumed rates of return for its lump-sum whole life in 2025, which improved product attractiveness and pricing flexibility. Individual annuity new policies rose in fiscal 2024, and the mix of fixed and variable annuities reflects households’ desire for guaranteed income with optional upside, which supports steady premium flows in the Japan life and non-life insurance market. Coverage is also expanding for advanced medical care recognized by the health ministry, which responds to treatment trends and reinforces the complementary role of private insurance alongside universal coverage.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| The shrinking and aging overall population is reducing the long-term pool of policyholders | -0.3% | National, with acute contraction in rural prefectures | Long term (≥ 4 years) |

| Persistently low interest rates are compressing investment returns and profitability in insurers' portfolios | -0.2% | National, moderating after policy normalization | Medium term (2-4 years) |

| Very competitive market with many players and stagnant or declining volumes in several lines | -0.2% | National, with intense rivalry in commercial lines and traditional channels | Short term (≤ 2 years) |

| Expected medium- to long-term shrinkage of automobile insurance due to technology and demographic change | -0.1% | National core, with an earlier onset in dense urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shrinking and Aging Overall Population Reducing the Long-Term Pool of Policyholders

A declining birthrate and rising longevity reshape the future pool of policyholders and reduce the pace of volume expansion, especially in regions with advanced depopulation. The elderly share of the population is set to climb further through the 2030s and 2040s, which increases per-capita protection and care needs while narrowing the base of working-age premium payers. Urban centres maintain relatively stable demand due to the concentration of households and corporate assets, yet rural prefectures face a smaller and older policyholder mix that challenges renewal momentum and distribution economics in the Japan life and non-life insurance market. Carriers are responding by reallocating capital to product lines aligned with longevity and health needs while broadening international exposure to diversify revenue sources and balance demographic headwinds at home. Balance sheet tools such as asset-intensive reinsurance are also in use to reshape liability profiles for in-force blocks, which helps manage risks associated with guarantees and longevity. Over the long term, refined underwriting, regionalized distribution, and product personalization will be needed to defend persistency rates in an aging and shrinking population base in the Japan life and non-life insurance market.

Persistently Low Interest Rates Compressing Investment Returns and Profitability on Insurers' Portfolios

The legacy effects of the negative interest rate regime that ended in March 2024 continue to weigh on investment portfolios as older assets yield near-zero coupons. Policy normalization took the overnight call rate to 0.75% in December 2025, which improves reinvestment economics, but the transition takes time to flow through to portfolio averages in the Japan life and non-life insurance market. Long-duration Japanese government bond yields rose during 2025, and investors in life portfolios, who hold a large share of outstanding JGBs, have adjusted allocations and risk balances in response to interest rate and inflation dynamics. Positive spreads are widening for some carriers as yen rates rise and hedging costs decline, which supports solvency and allows selective re-risking or liability management actions. Insurers are also rebalancing equity exposure and extending yen fixed-income holdings to steady returns and reduce capital market sensitivity under the new economic value-based capital framework. The alignment with international capital standards and the supervisory focus on risk-based management practices should temper market stress transmission to insurer balance sheets during future volatility episodes.

Segment Analysis

By Insurance Type: Life Segment Positioned For Faster Growth Despite Non-Life Dominance

Non-life insurance holds 64.34% of Japan's life and non-life insurance market share, driven by demand for catastrophe, property, and liability risk coverage. The public-private household earthquake insurance system, integrated with fire policies, limits private sector financial burdens, enhancing resilience and underwriting capacity. While non-life dominates, life insurance is projected to grow at a 2.65% CAGR through 2031, fueled by the renewed appeal of savings-type products due to normalized policy rates and improved yen asset yields. Insurers now align returns with assumed rates, and a leading life carrier raised assumed return rates for lump-sum whole life in 2025, boosting product appeal. Fiscal 2024 saw increased individual annuity new business, with balanced demand for fixed and variable annuities reflecting household preferences for income certainty and upside potential.

Catastrophic risks shape non-life insurance strategies, influencing capital allocation, risk transfer, and product innovation. Health and medical benefits in life and supplemental lines address out-of-pocket costs unmet by Japan's universal health system, with products expanding to include wellness and preventive care features that improve claims experience and add value for policyholders. The evolving solvency regime drives insurers to refine pricing for blocks with embedded guarantees and explore asset-intensive reinsurance for legacy liabilities, as seen in a significant 2024 longevity transaction for an in-force annuity block. Yield-sensitive demand in life products and catastrophe exposure in non-life provide clear growth drivers for Japan's insurance market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Customer Segment: Corporate Buyers Fuel Fastest Expansion Amid Retail Maturity

Retail customers accounted for 71% of Japan's life and non-life insurance market share in 2025, reflecting the importance of protection products in household financial strategies. Japanese households allocate a significant portion of financial assets to insurance and pensions, ensuring a stable flow of recurring premiums. The aging population is driving demand for annuities, long-term care, and critical illness coverage, increasing interest in third-sector and hybrid products that combine income security with health benefits. Consumer research highlights strong demand for annuities with adjustable payouts after major health events, emphasizing the need for flexible, health-linked features. Wearable-driven engagement programs that track activity and health metrics enhance prevention efforts and policyholder retention when they deliver tangible value.

The corporate segment is expected to grow at a 3.78% CAGR from 2026 to 2031, driven by rising risks from natural disasters, cyber threats, business interruptions, and supply-chain vulnerabilities. Corporate buyers are increasingly adopting parametric options for faster claims settlements aligned with broader risk management goals. Regulatory focus on risk-based management and transparency improves underwriting quality and strengthens corporate risk managers' confidence. Japanese insurers are expanding into specialty and international markets, enhancing expertise in complex corporate lines and improving domestic service quality and product diversity. This combination of escalating risks and evolving insurance solutions positions the corporate segment as a key growth driver for Japan's life and non-life insurance market during the forecast period.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Agent Dominance Persists While Direct Sales Accelerate Through Digital Innovation

Brokers and agents dominate Japan's life and non-life insurance market, accounting for 87.65% of distribution in 2025. This reflects a reliance on face-to-face advisory and established channel structures. Major life groups utilize large, tied salesforces and alliances to extend product reach. Supervisory reforms in 2025 mandate customer-oriented agent incentives and prohibit excessive conveniences, enhancing advice quality and governance. Regulatory changes, such as reduced minimum-security deposits and fee charging in commercial lines, encourage broader broker participation while maintaining oversight. AI-enabled tools improve agent productivity and help carriers meet explainability and fairness standards.

Direct channels are projected to grow at a 3.21% CAGR through 2031, driven by digital onboarding and simplified product suites catering to online buyers. Open, consultative storefronts representing multiple carriers make independent advice accessible, benefiting retail customers seeking aggregated comparisons. Insurers prioritize agent-led advice for complex or long-duration products while developing direct and hybrid journeys for standardized coverage. This multichannel approach enhances consumer choice, supports premium growth, and preserves agents' trusted role in critical areas.

Geography Analysis

Regional risk and demand patterns vary across Japan's unitary national market, despite centralized regulation and consistent supervisory policies. Metropolitan areas like Tokyo, with dense populations and significant insurable assets, drive higher adoption of life and non-life insurance. Low-lying wards in Tokyo face flood risks, prompting insurers and clients to focus on updated modeling and mitigation strategies. Supervisory climate risk scenarios highlight rising acute physical risks, emphasizing resilience planning and capital buffers at the regional and national levels. Household earthquake insurance and public-private risk sharing stabilize catastrophe-prone areas, influencing pricing, product mix, and reinsurance strategies in the Japan life and non-life insurance market.

Rural prefectures face aging populations and out-migration, shrinking premium pools, and shifting demand toward longevity and care coverage. Older properties and vacant homes in these areas are vulnerable to severe weather and seismic events, increasing underwriting complexity and the need for risk surveys. Urban centers demand extensive commercial coverage, while rural markets focus on household-driven property and medical coverage. Insurers optimize capacity and service levels through regional strategies, ensuring nationwide access and efficient network economics. Investments in data, satellite imagery, and hazard mapping enhance underwriting precision and advisory capabilities, differentiating carriers in retail and corporate sales.

Geography significantly impacts claims outcomes, underscoring the need for broad coverage and effective risk transfer. Major earthquakes over the past decade led to substantial payouts, while recent events highlight the importance of seismic preparedness and product innovation. Typhoons and wind events in western and southern prefectures cause significant losses, validating regionally tailored pricing and advisory rate updates. Investments in catastrophe research and urban resilience are critical as climate patterns evolve. Centralized supervision and public-private risk sharing enable carriers to balance regional volatility with capital strength and portfolio diversification, ensuring the Japan life and non-life insurance market's resilience through the forecast period.

Competitive Landscape

Japan's life and non-life insurance market balances moderate concentration among leading groups with strong competition across lines and channels. Top domestic carriers maintain diversified portfolios, robust solvency, and risk management practices under the FSA's evolving economic value-based framework. These groups strategically pursue overseas expansion in insurance and asset management, diversifying growth and enhancing domestic capabilities. For instance, a leading group acquired a global closed-book operator in 2024 to strengthen international earnings and scale core product platforms. Another major life group is investing in asset management and protection segments, targeting medium-term growth in overseas contributions. Domestically, strategies focus on product modernization, channel quality, and tech-driven service transformation.

Technology investments and ecosystem partnerships are accelerating capability building. A global insurance software provider plans to invest USD 60 million in Japan by 2025, focusing on cloud and AI to improve underwriting and claims precision[4]Global Insurance Technology Leader Guidewire to Invest $60 Million to Accelerate Insurance Innovation and Cloud Transformation in Japan,” Guidewire, ir.guidewire.com. Similarly, a major tech firm launched a Japan-specific insurance cloud platform in late 2025, tailored to local regulatory and business needs. Partnerships in telematics and data-driven risk services are expanding, such as a trading company’s collaboration with a carrier-affiliated insurtech to develop AI-driven auto coverage. These initiatives enhance product agility, operational efficiency, prevention, and claims resolution.

Capital management and balance sheet optimization are critical as insurers adapt to the economic value-based solvency framework. Strategies include asset-intensive reinsurance of in-force annuities to reduce longevity risk, as seen in a major 2024 transaction, and increased yen fixed-income allocations to improve yields and reduce market sensitivity. Distribution governance reforms are elevating advisory standards, aligning compensation with customer outcomes, and encouraging broader broker participation in commercial lines. These trends favor incumbents with strong capital and technology while creating opportunities for specialized players offering unique expertise or data-driven solutions.

Japan Life And Non-Life Insurance Industry Leaders

Nippon Life Group

Dai-ichi Life Group

Meiji Yasuda Life Group

Sumitomo Life Group

Japan Post Insurance Group (Kampo)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Fujitsu, in partnership with SAP Fioneer, launched the Japan Edition of SAP Fioneer Cloud for Insurance to support product, policy, and claim management with configurations for Japanese regulations, enabling faster digital transformation across life and non-life carriers. The platform provides a cloud-native core with insurance-specific components and integration to peripheral systems, which reduces time to market. Early adoption is focused on standardizing processes, improving data quality, and preparing for analytics-driven operations.

- April 2025: Guidewire announced a USD 60 million investment over five years to scale its Japan presence, focusing on cloud transformation and embedded AI that helps carriers raise underwriting accuracy and claims efficiency while reducing technical debt. The move supports faster product iteration and better data integration across the insurance value chain. It also expands the local ecosystem of skilled implementation partners.

- March 2025: Sompo Japan, a subsidiary of Sompo Holdings, secured USD 150 million in reinsurance for Japanese typhoon and flood risks via the Sakura Re Ltd. (Series 2025-1) catastrophe bond. Priced at the lower end of guidance, this issuance replaces coverage from the maturing Sakura 2021-1 bond, reflecting the company’s continued reliance on catastrophe bond markets.

Japan Life And Non-Life Insurance Market Report Scope

The Japan life and non-life insurance market refers to the organized industry of insurance products and services across the country, encompassing life, health, property, motor, liability, and other coverage lines. It plays a critical role in household financial planning and corporate risk management, supported by strong regulatory supervision from the Financial Services Agency (FSA) and high insurance penetration levels. The market is shaped by demographic change, climate risk exposure, and evolving consumer needs, with insurers diversifying into flexible protection, health, and retirement solutions tailored to Japan’s super‑aged population.

The market is segmented by insurance type, customer segment, and distribution channel. By insurance type, it includes life insurance, non‑life insurance, motor insurance, health insurance, property insurance, liability insurance, and other insurance categories, reflecting the breadth of coverage across personal and commercial risks. By customer segment, the market is divided into retail and corporate, highlighting differences in product design, demand drivers, and service models. By distribution channel, the market covers brokers and agents, banks, direct sales, and other channels, capturing both traditional and digital pathways to reach policyholders. The report offers Market size and forecasts for the Life and Non-Life Insurance Market in Japan, in value (USD Billion) for all the above segments.

By Insurance Type

| Life Insurance | |

| Non-Life Insurance | Motor Insurance |

| Health Insurance | |

| Property Insurance | |

| Liability Insurance | |

| Other Insurance | |

| By Customer Segment | Retail |

| Corporate | |

| By Distribution Channel | Brokers/Agents |

| Banks | |

| Direct Sales | |

| Other Channels |

| By Insurance Type | Life Insurance | |

| Non-Life Insurance | Motor Insurance | |

| Health Insurance | ||

| Property Insurance | ||

| Liability Insurance | ||

| Other Insurance | ||

| By Customer Segment | Retail | |

| Corporate | ||

| By Distribution Channel | Brokers/Agents | |

| Banks | ||

| Direct Sales | ||

| Other Channels | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and outlook for the Japan life and non-life insurance market?

The market has a market size of USD 307.7 billion in 2026 and is projected to reach USD 335.71 billion by 2031, reflecting a 1.76% CAGR as demographic aging, regulatory modernization, and technology adoption shape demand and operations.

Which segment is expanding fastest within the Japan life and non-life insurance market?

Life insurance is forecast to grow at a 2.65% CAGR through 2031 due to revived demand for savings-type products under higher yen yields and steady appetite for annuities and health-related protection.

Which customer segment leads premiums in the Japan life and non-life insurance market?

Retail held a 71% share in 2025, supported by the deep role of protection in household financial planning and an aging population that requires nursing care and longevity solutions.

How do distribution channels compare in the Japan life and non-life insurance market?

Brokers and agents held 87.65% of distribution in 2025, while direct channels are projected to grow at a 3.21% CAGR as digital onboarding, core platform upgrades, and AI tools expand online purchasing.

What regulatory changes are most important for the Japan life and non-life insurance market?

The FSA is implementing an economic value-based solvency framework from fiscal 2026 and has updated distribution supervision to align incentives with customer-oriented quality while setting clear expectations for responsible AI use.

How does catastrophe risk affect the Japan life and non-life insurance market?

High exposure to earthquakes and severe weather sustains strong non-life demand, drives risk transfer strategies, and encourages investment in modelling and prevention, underpinned by a public-private earthquake scheme that supports market stability.