| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 0.67 Billion |

| Market Size (2030) | USD 1.67 Billion |

| CAGR (2025 - 2030) | 20.00 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

LED Phosphors Market Analysis

The LED Phosphors Market size is estimated at USD 0.67 billion in 2025, and is expected to reach USD 1.67 billion by 2030, at a CAGR of 20% during the forecast period (2025-2030).

The LED phosphors industry is experiencing significant transformation driven by global sustainability initiatives and energy efficiency mandates. Government regulations worldwide are increasingly mandating the adoption of LED technology, with the United States implementing standards requiring 45 lumens per watt for common light bulbs. The transition from traditional lighting solutions to LEDs is particularly noteworthy, as LEDs demonstrate superior efficiency by delivering 80 to 100 lumens per watt compared to traditional options. According to industry projections, LED penetration in the lighting market is expected to reach 87.4% by 2030, highlighting the technology's growing dominance in the global lighting landscape.

The industry is witnessing remarkable technological advancements in phosphor development and application. Materials scientists have made breakthrough discoveries in composite ceramic materials (Ce3+:YAG-Al2O3), enabling LED systems to preserve 20-30% more energy than commercial alternatives. The U.S. Department of Energy projects that widespread LED adoption could lead to annual energy savings of 569 TWh by 2035, equivalent to the output of 92 1,000 MW power plants. These innovations are particularly significant as they address both environmental concerns and operational efficiency requirements.

The consumer electronics sector is emerging as a crucial growth catalyst for LED phosphors, with applications ranging from display backlighting to automotive lighting solutions. The Indian instruments and consumer electronics industry, for instance, is projected to reach USD 21.18 billion by 2025, indicating substantial growth opportunities for LED phosphors applications. The integration of LED technology in various electronic devices has created new demands for specialized phosphor formulations, particularly in high-performance display applications and automotive lighting systems.

The market is experiencing a shift toward more sophisticated phosphor technologies, exemplified by recent innovations in photoluminescent materials. In December 2022, Toshiba Corporation unveiled a breakthrough in phosphor technology that delivers efficient solubility in polymers or organic solvents, offering enhanced transparency and red-light emissions under UV light. This development has opened new possibilities in LED lighting, displays, deep UV sensing, and security printing applications. The industry is also witnessing significant infrastructure investments, as demonstrated by Essex County Council's commitment to convert 128,000 streetlights to LED-based systems by 2024, representing a broader trend of municipal-level adoption of LED technology.

LED Phosphors Market Trends

Growing Usage of Smart Lighting Systems

The increasing adoption of smart lighting systems has become a significant driver for the LED phosphors market, primarily due to the integration of Internet of Things (IoT) technology in lighting solutions. Smart lighting systems are witnessing unprecedented growth as they offer enhanced control capabilities, energy efficiency, and integration with other smart home and city infrastructure. According to industry experts, LED lights are over 80% more efficient than traditional lighting solutions, with almost 95% of the energy in LEDs converted into light and only 5% wasted as heat. This remarkable efficiency has led many end users to opt for smart LED lighting solutions, particularly in residential and commercial applications where lighting control and energy management are crucial.

The evolution of WiFi-based smart lighting systems in residential establishments has further accelerated market growth. Several platforms have emerged that function with WiFi, such as LIFX, which offers a smart light platform using WiFi connectivity to control entire lighting networks in homes. Additionally, manufacturers are introducing new Bluetooth-based smart lighting solutions that can function without any hub, allowing users to control their lighting systems via iOS/Android apps or with voice assistants like Amazon Echo and Google Home using IFTTT protocols. These technological advancements in smart lighting controls, combined with the increasing capabilities of phosphorescent materials in providing precise color tuning and dimming functions, are creating substantial opportunities for market growth.

Understand The Key Trends Shaping This Market

Download PDF

Advanced Technological Developments in LED Phosphors

The LED phosphors industry has witnessed significant technological advancements, particularly in developing new phosphor compositions and improving existing formulations. Materials scientists have made breakthrough developments in composite ceramic materials, such as Ce3+:YAG-Al2O3, which are solid-state light converters that can be used in ground and aerospace technologies. These advanced LED systems based on molded materials can preserve 20-30% more energy than commercial analogs, representing a significant improvement in efficiency and performance. The continuous innovation in phosphor technology has led to the development of new compositions that offer enhanced color rendition, improved stability, and higher light quality.

Recent technological breakthroughs include the development of narrow-band phosphors and the optimization of phosphor delivery systems. For instance, companies like Nichia have introduced innovative solutions such as Dynasolis, a new LED tuning solution that regulates circadian rhythms by simultaneously adjusting melanopic illuminance and color temperature while maintaining high CRI and high efficacy. This advancement has been achieved by combining accumulated phosphor technology with KSF narrow-band red phosphor and TriGain Technology, optimizing the light spectrum and overcoming the traditional trade-off between efficacy and CRI. Furthermore, researchers have made significant progress in developing new luminescent materials that can directly emit white light, addressing one of the key challenges in LED technology where conventional LED materials typically fail to achieve this capability.

The use of rare earth phosphors and quantum dot phosphors is also gaining traction, offering improved color quality and energy efficiency, thereby enhancing the overall performance of LED lighting systems.

Segment Analysis: By Application

Lighting Segment in LED Phosphors Market

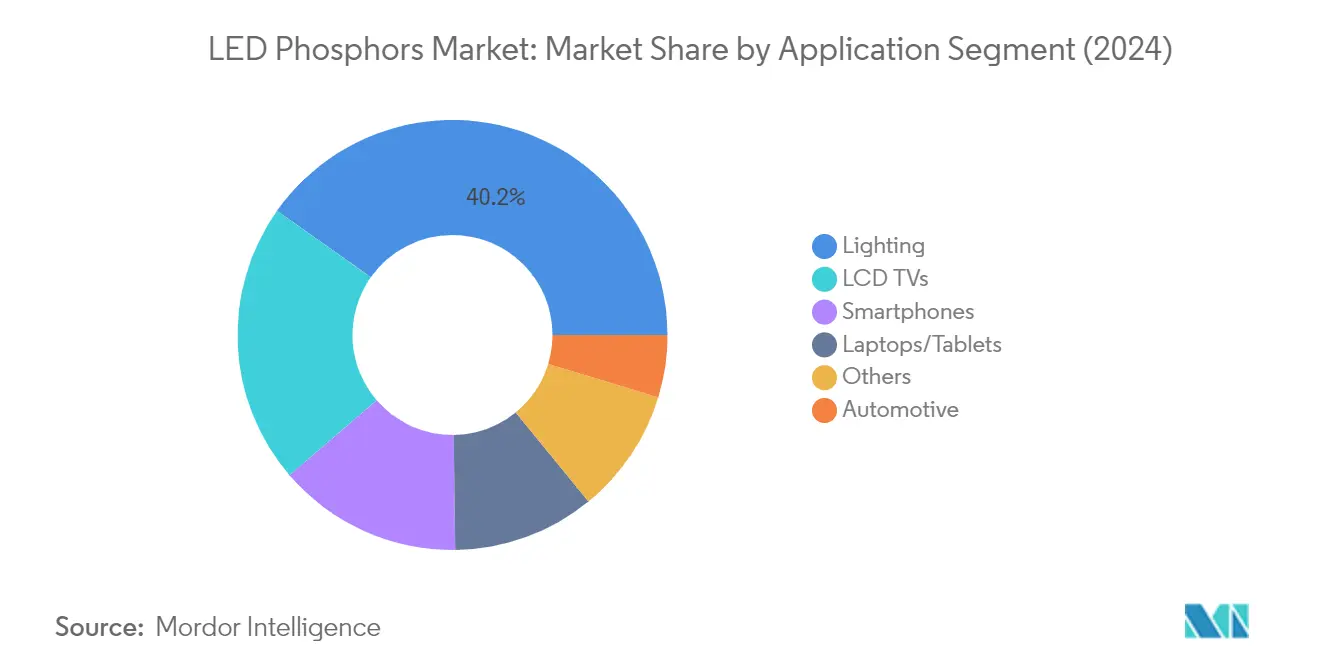

The lighting (residential and industrial) segment maintains its dominant position in the LED phosphors market, commanding approximately 40% market share in 2024. This significant market presence is driven by the widespread adoption of LED lighting solutions across both residential and commercial applications. The segment's growth is further supported by various government initiatives promoting energy-efficient lighting solutions and the increasing focus on sustainable building practices. The development of smart lighting systems and the integration of IoT capabilities have also contributed to the segment's market leadership. Additionally, the declining costs of LED lighting solutions and improvements in light quality through advanced phosphorescent materials have made LED lighting more accessible to a broader consumer base.

Smartphones Segment in LED Phosphors Market

The smartphones segment has emerged as the fastest-growing application area in the LED phosphors market for the period 2024-2029. This remarkable growth is driven by the increasing sophistication of smartphone displays and the growing demand for enhanced visual experiences. The segment's expansion is fueled by technological advancements in LED phosphors materials that enable improved color accuracy, brightness, and energy efficiency in smartphone displays. The integration of advanced display technologies like OLED and AMOLED, which require specialized phosphor materials, further accelerates this growth. Additionally, the rising consumer demand for high-end smartphones with superior display quality and the continuous innovation in mobile display technologies contribute to the segment's rapid expansion.

Remaining Segments in LED Phosphors Market by Application

The LED phosphors market encompasses several other significant application segments, including LCD TVs, laptops/tablets, and automotive applications. The LCD TV segment maintains a strong presence due to the continuous evolution of display technologies and increasing consumer preference for high-quality viewing experiences. The laptops/tablets segment benefits from the growing demand for portable computing devices with enhanced display capabilities. The automotive segment, while smaller, shows promising growth potential driven by the increasing adoption of LED lighting in vehicles, particularly in advanced driving beam applications and interior lighting. These segments collectively contribute to the market's diversification and overall growth, each bringing unique requirements and opportunities for LED phosphor technologies, including silicate phosphors and nitride phosphors.

LED Phosphors Market Geography Segment Analysis

LED Phosphors Market in North America

The North American LED phosphors market, commanding approximately 19% of the global market share in 2024, continues to be driven by robust demand for energy-efficient lighting solutions and advanced automotive lighting systems. The region's market growth is primarily fueled by stringent energy efficiency regulations and widespread adoption of smart lighting technologies across residential and commercial sectors. The United States and Canada lead the regional market with their strong focus on sustainable lighting solutions and digital transformation initiatives. The automotive sector's increasing adoption of advanced LED phosphors lighting systems, particularly in electric vehicles and luxury car segments, further strengthens market growth. The region's emphasis on research and development in fluorescent materials and LED technology, coupled with the presence of major market players and sophisticated manufacturing capabilities, reinforces its position as a key market. Additionally, the growing implementation of smart city projects and infrastructure modernization initiatives across North American cities creates substantial opportunities for LED phosphors applications in street lighting and commercial buildings.

LED Phosphors Market in Europe

The European LED phosphors market has demonstrated remarkable resilience and growth, recording approximately a 21% growth rate from 2019 to 2024. The region's market is characterized by its strong emphasis on sustainable lighting solutions and energy conservation initiatives, particularly in response to ongoing energy security concerns. The European Union's stringent regulations on energy efficiency and environmental protection continue to drive the adoption of LED lighting solutions across various sectors. The region's automotive industry, particularly in Germany, France, and the United Kingdom, represents a significant growth driver for LED phosphors, with increasing implementation in advanced automotive lighting systems. The market benefits from substantial investments in smart city projects and building modernization initiatives across European metropolitan areas. The presence of well-established research institutions and technology centers further supports innovation in luminescent materials and LED phosphor technology. The region's focus on reducing carbon emissions and promoting energy-efficient lighting solutions in both residential and commercial sectors continues to create new opportunities for market expansion.

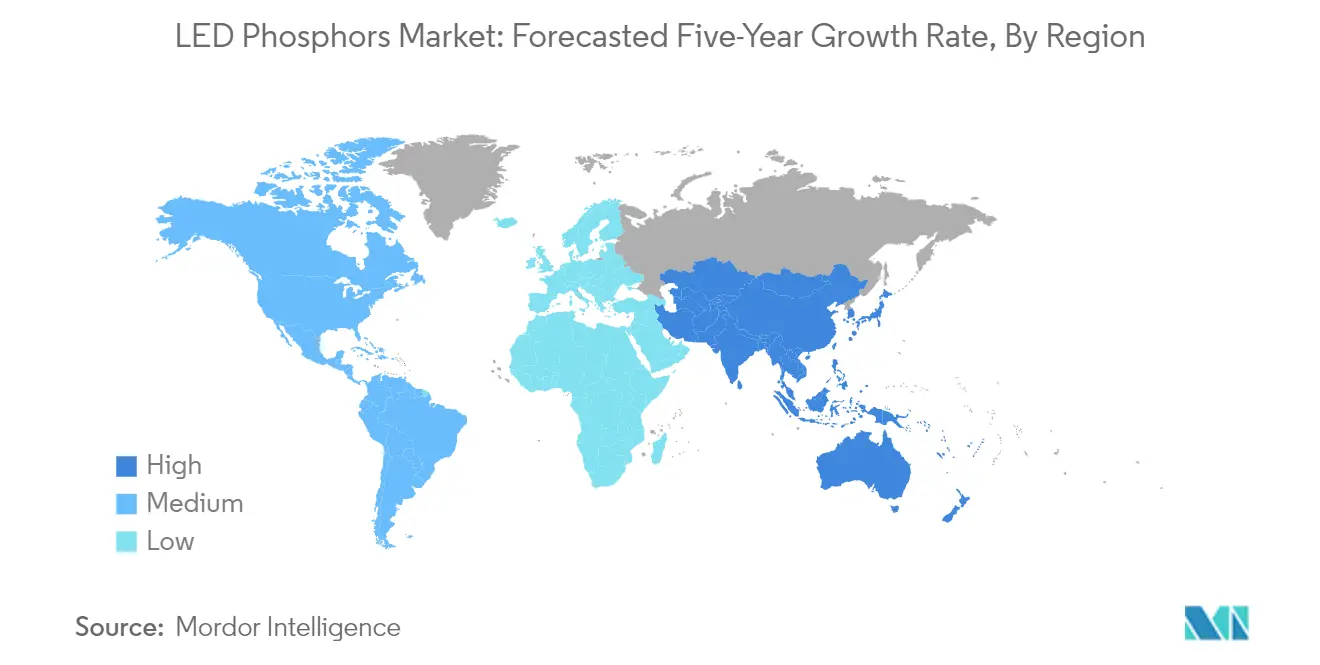

LED Phosphors Market in Asia-Pacific

The Asia-Pacific LED phosphors market is positioned for exceptional growth, with a projected growth rate of approximately 21% during 2024-2029. The region maintains its position as the global manufacturing hub for LED products, with China, Japan, and South Korea leading in technological innovations and production capabilities. The market benefits from the presence of major electronic manufacturing facilities and robust supply chain networks across the region. Rapid urbanization, particularly in emerging economies like India and Southeast Asian nations, drives the demand for LED lighting in residential and commercial construction projects. The region's automotive manufacturing sector, especially in Japan and South Korea, contributes significantly to market growth through increased adoption of advanced LED lighting systems. The strong government support for energy-efficient lighting solutions, coupled with initiatives to reduce carbon emissions, creates a favorable environment for market expansion. Additionally, the region's growing consumer electronics industry and increasing adoption of smart lighting systems in both urban and rural areas continue to drive market growth.

LED Phosphors Market in Rest of the World

The LED phosphors market in the Rest of the World, encompassing Latin America, the Middle East, and Africa, demonstrates increasing adoption of LED lighting technologies driven by urbanization and infrastructure development initiatives. The region shows growing awareness of energy-efficient lighting solutions, particularly in commercial and residential construction projects. Middle Eastern countries are increasingly incorporating LED lighting in their smart city initiatives and sustainable urban development projects. Latin American markets are witnessing growing demand for LED phosphors in automotive applications and street lighting projects. The region's focus on reducing energy consumption and modernizing lighting infrastructure creates opportunities for market expansion. Government initiatives promoting energy-efficient lighting solutions and increasing investments in public infrastructure projects further support market growth. The growing adoption of smart lighting systems in commercial buildings and the hospitality sector also contributes to market development in these regions.

Get Analysis on Important Geographic Markets

Download PDF

LED Phosphors Industry Overview

Top Companies in LED Phosphors Market

The LED phosphors market features established players like Beijing Yuji International, Intematix Corporation, Phosphor Tech Corporation, Denka Co., Nichia Corporation, and Mitsubishi Chemical Corporation leading the innovation landscape. Companies are focusing on developing advanced phosphor formulations and innovative delivery systems to enhance LED efficiency and light quality. Strategic partnerships and licensing agreements for phosphor technology have become increasingly common, as seen with companies like Bridgelux licensing PFS phosphor technology. Operational excellence is being pursued through investments in manufacturing capabilities and supply chain optimization, with many players maintaining facilities across multiple regions. Companies are expanding their product portfolios to address specific applications such as horticulture, automotive lighting, and smart lighting systems, while also emphasizing environmental sustainability in their operations.

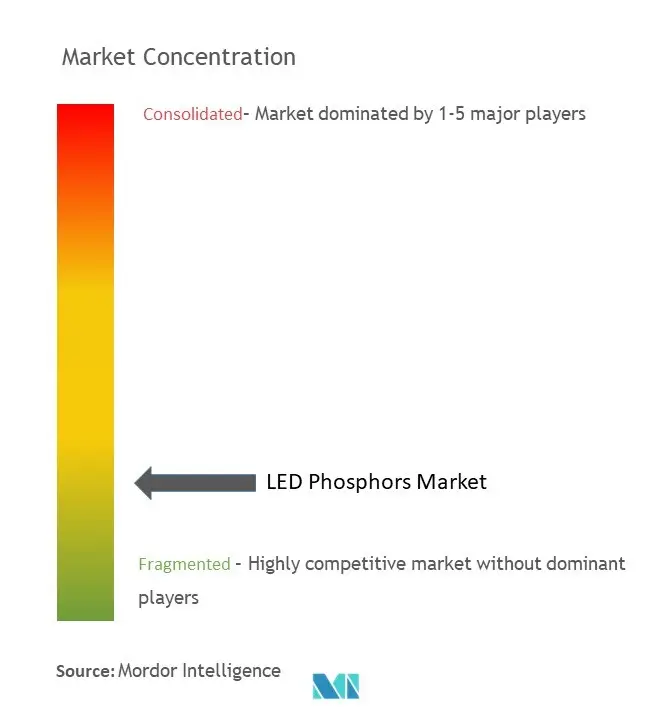

Fragmented Market with Strong Regional Players

The LED phosphor market exhibits a fragmented structure with a mix of global conglomerates and specialized manufacturers competing across different regions. Large chemical and electronics corporations like Mitsubishi Chemical and Philips Lumileds leverage their extensive R&D capabilities and established distribution networks to maintain market positions. Regional specialists, particularly in Asia-Pacific markets like China and Japan, have carved out strong niches through their focus on specific applications and local market knowledge. The market has witnessed increased consolidation through strategic acquisitions, as demonstrated by AMS AG's acquisition of Osram and various other regional deals in Europe and Asia.

The competitive dynamics are characterized by a strong manufacturing presence in Asia, particularly in China and Japan, where companies benefit from proximity to major LED manufacturing hubs. Market participants are increasingly pursuing vertical integration strategies to control the entire value chain from raw materials to final products. While some players focus on high-performance specialty phosphors for premium applications, others compete in the mass market segment through cost-effective solutions. The industry has seen the emergence of technology-focused startups and specialized players who are challenging established companies through innovative phosphor solutions and application-specific products.

Innovation and Customization Drive Market Success

Success in the LED phosphors market increasingly depends on companies' ability to develop customized solutions for specific applications while maintaining cost competitiveness. Market leaders are investing heavily in research and development to create phosphor formulations that offer improved efficiency, color quality, and thermal stability. Companies are also focusing on building strong relationships with LED manufacturers and end-users through technical support and collaborative development programs. The ability to scale production while maintaining quality consistency has become crucial, particularly as demand grows from automotive and smart lighting applications. Successful players are those who can balance innovation with manufacturing efficiency while maintaining strong intellectual property portfolios.

Market contenders are finding opportunities by focusing on emerging applications and underserved market segments. Companies are developing specialized phosphor solutions for growing applications like horticulture lighting and automotive displays, where performance requirements are becoming more stringent. Environmental regulations and energy efficiency standards are creating opportunities for companies that can develop eco-friendly phosphor solutions with improved performance characteristics. Success also depends on building robust supply chain relationships and establishing strong technical support networks to serve customers across different regions. Companies that can combine technical expertise with market responsiveness while maintaining cost competitiveness are better positioned for long-term success.

LED Phosphors Market Leaders

-

Beijing Yuji International Co. Ltd

-

Intematix Corporation

-

Phosphor Tech Corporation

-

Denka Co. Ltd

-

Nichia Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

LED Phosphors Market News

- August 2023: Signify announced the opening of its biggest LED lighting manufacturing site in the world in Jiujiang, Jiangxi Province, China. The new factory of Signify's joint venture company, Zhejiang Klite Lighting Holdings Co., Ltd, will manufacture high-quality branded LED lighting products for China and the global market.

- May 2022: At ISE, Samsung unveiled its 2022 model of The Wall (IWB), an innovative modular Micro LED display that provided immersive viewing experiences in a high-resolution, large-screen format.

LED PhosphorsMarket Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Growing Usage of Smart Lighting Systems

- 5.1.2 Advanced Technological Developments in LED Phosphors

-

5.2 Market Challenges

- 5.2.1 Lack of Awareness and High Cost

6. MARKET SEGMENTATION

-

6.1 By Application

- 6.1.1 Smartphones

- 6.1.2 LCD TVs

- 6.1.3 Laptops/Tablets

- 6.1.4 Automotive

- 6.1.5 Lighting (Residential and Industrial)

- 6.1.6 Other Applications

-

6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Beijing Yuji International Co. Ltd.

- 7.1.2 Intematix Corporation

- 7.1.3 Phosphor Tech Corporation

- 7.1.4 Denka Co. Ltd.

- 7.1.5 Nichia Corporation

- 7.1.6 Mitsubishi Chemical Corporation

- 7.1.7 Philips Lumileds Lighting Company

- 7.1.8 Luming Technology Group Co. Ltd.

- 7.1.9 Citizen Electronics Co. Ltd

- 7.1.10 Cree LED Inc. (SMART Global Holdings Inc.)

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

LED Phosphors Industry Segmentation

A phosphor is a material that produces bright light when it comes into contact with infrared, ultraviolet radiation, or an electron beam source. In order to satisfy some of the performance criteria, a phosphor structure and composition may be carefully tuned so as to obtain an appropriate spectral content. Therefore, phosphors are frequently used in the electronics and lighting industry so that applications like e.g., displays, fluorescent lights, or blue LEDs can be achieved. Most white LEDs consist of a chip that emits Blue light with a narrow spectrum from 440 to 470 nm and is covered by either yellow, green, or red phosphors. Some of the blue light from that LED die is to be absorbed by phosphors. The phosphor light creates a white light, which is perceived by the human eye as blue, in addition to the remaining blue light that leaks out of the phosphor layer.

The LED phosphors market is segmented by applications (smartphones, LCD TVs, laptops, and tablets), automotive, lighting (residential and industrial), and geography (North America, Europe, Asia Pacific, and the Rest of the World).

The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Application | Smartphones |

| LCD TVs | |

| Laptops/Tablets | |

| Automotive | |

| Lighting (Residential and Industrial) | |

| Other Applications | |

| By Geography | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

LED PhosphorsMarket Research FAQs

How big is the LED Phosphors Market?

The LED Phosphors Market size is expected to reach USD 0.67 billion in 2025 and grow at a CAGR of 20% to reach USD 1.67 billion by 2030.

What is the current LED Phosphors Market size?

In 2025, the LED Phosphors Market size is expected to reach USD 0.67 billion.

Who are the key players in LED Phosphors Market?

Beijing Yuji International Co. Ltd, Intematix Corporation, Phosphor Tech Corporation, Denka Co. Ltd and Nichia Corporation are the major companies operating in the LED Phosphors Market.

Which is the fastest growing region in LED Phosphors Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in LED Phosphors Market?

In 2025, the Asia-Pacific accounts for the largest market share in LED Phosphors Market.

What years does this LED Phosphors Market cover, and what was the market size in 2024?

In 2024, the LED Phosphors Market size was estimated at USD 0.54 billion. The report covers the LED Phosphors Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the LED Phosphors Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

LED Phosphors Market Research

Mordor Intelligence provides a comprehensive analysis of the LED phosphors industry. We leverage our extensive experience in researching fluorescent materials and phosphorescent materials markets. Our expert analysts offer detailed insights into the evolving landscape of luminescent materials and photoluminescent materials. This gives stakeholders a thorough understanding of market dynamics. The report examines various technologies, such as rare earth phosphors, quantum dot phosphors, silicate phosphors, and nitride phosphors, providing a complete industry perspective.

Stakeholders gain access to actionable intelligence through our easily downloadable report PDF. It features in-depth analysis of supply chains, technological innovations, and growth opportunities. The report delivers valuable insights into regional market developments, pricing trends, and competitive landscapes across the LED phosphor market. Our research methodology combines primary data collection with rigorous secondary research. This ensures that decision-makers have access to reliable data for strategic planning and investment decisions in this rapidly evolving industry.