Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

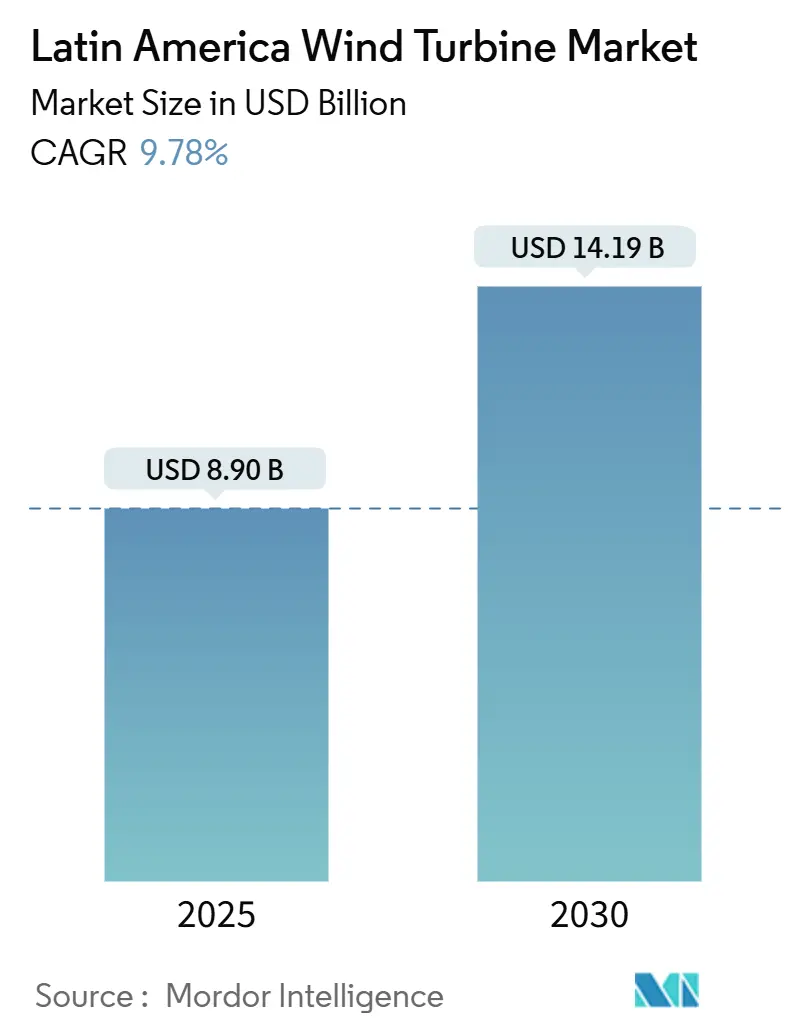

| Market Size (2025) | USD 8.90 Billion |

| Market Size (2030) | USD 14.19 Billion |

| Growth Rate (2025 - 2030) | 9.78% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Latin America Wind Turbine Market Analysis by Mordor Intelligence

The Latin America Wind Turbine Market size is estimated at USD 8.90 billion in 2025, and is expected to reach USD 14.19 billion by 2030, at a CAGR of 9.78% during the forecast period (2025-2030).

This growth reflects a sharp decline in onshore wind generation costs, rising volumes under regional power auction programs, and new demand from the emerging green hydrogen export trade. Developers now see clearer pathways to connect projects thanks to new high-voltage lines in Brazil, Chile, and Colombia, while corporate power-purchase agreements (PPAs) signed by data-center operators tighten near-term visibility on offtake. The Latin America wind turbine market also benefits from state-level incentives that localize blade, nacelle, and tower fabrication in Ceará and Pernambuco, trimming logistics bills by double-digit percentages. Offshore regulation in Brazil and Colombia is poised to unlock gigawatt-scale coastal capacity, thereby upgrading the long-term opportunity set for the Latin American wind turbine market.

Key Report Takeaways

- By location of deployment, on-shore projects commanded 91.1% of the Latin America wind turbine market size in 2024; offshore capacity is forecast to leap at an 18.7% CAGR across 2025-2030.

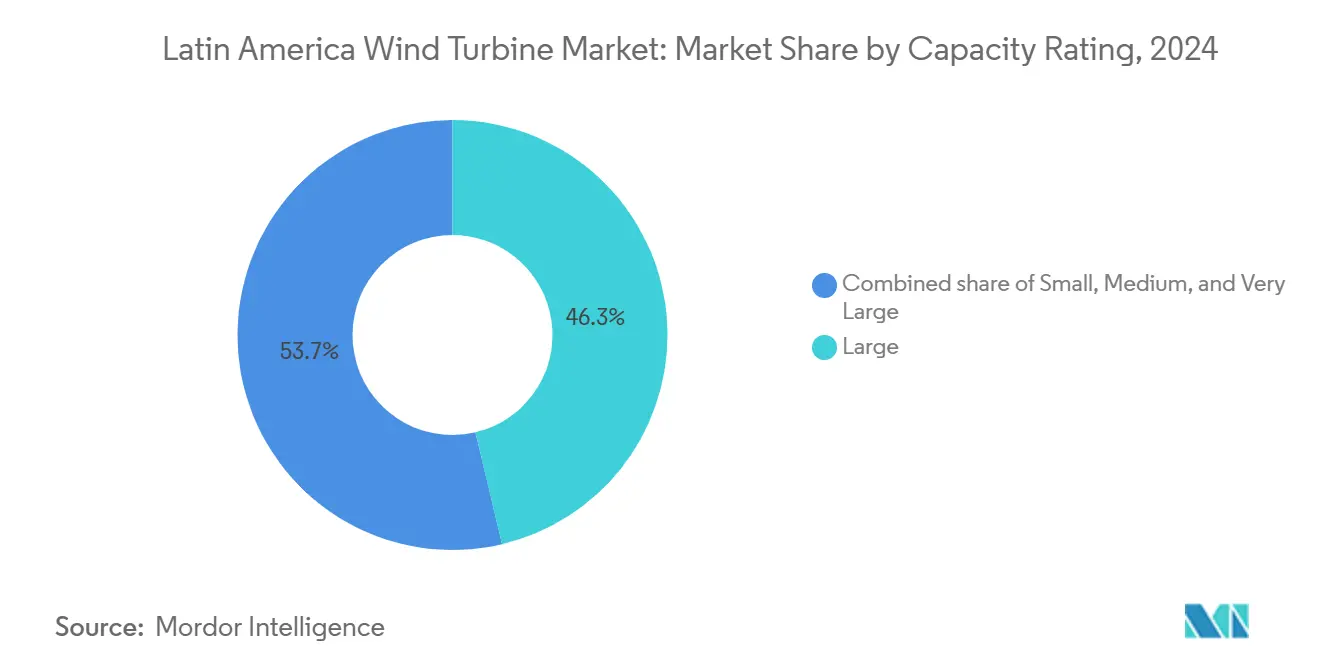

- By capacity rating, 1 to 5 MW turbines held 46.3% of the Latin America wind turbine market size in 2024, whereas machines above 5 MW are on track for a 14.3% CAGR.

- By axis type, horizontal-axis models secured a 90.7% share of installations in 2024; vertical-axis units are expected to expand at a rate of 12.9% per year to 2030.

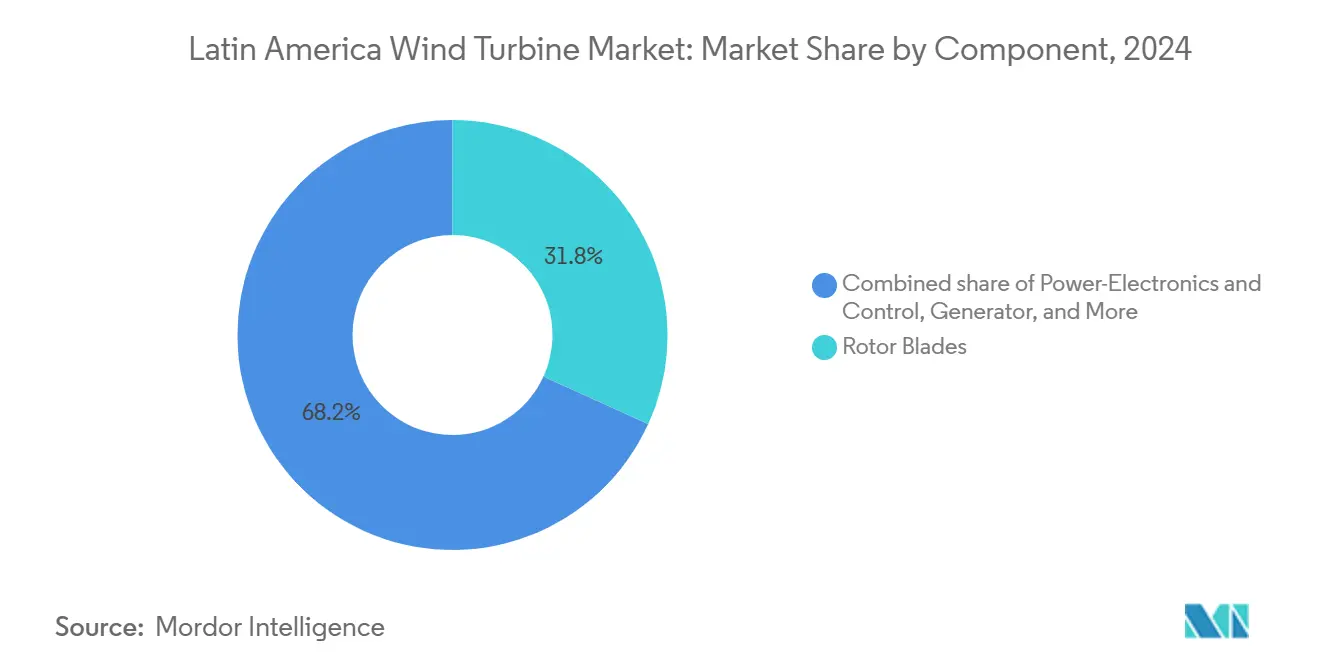

- By component, rotor blades led with 31.8% revenue share in 2024, while power electronics and control systems are advancing at a 12.1% CAGR.

- By end-use application, utility-scale projects captured 85.5% of the installed capacity in 2024; commercial & industrial installations are expected to accelerate at a 14.8% CAGR through 2030.

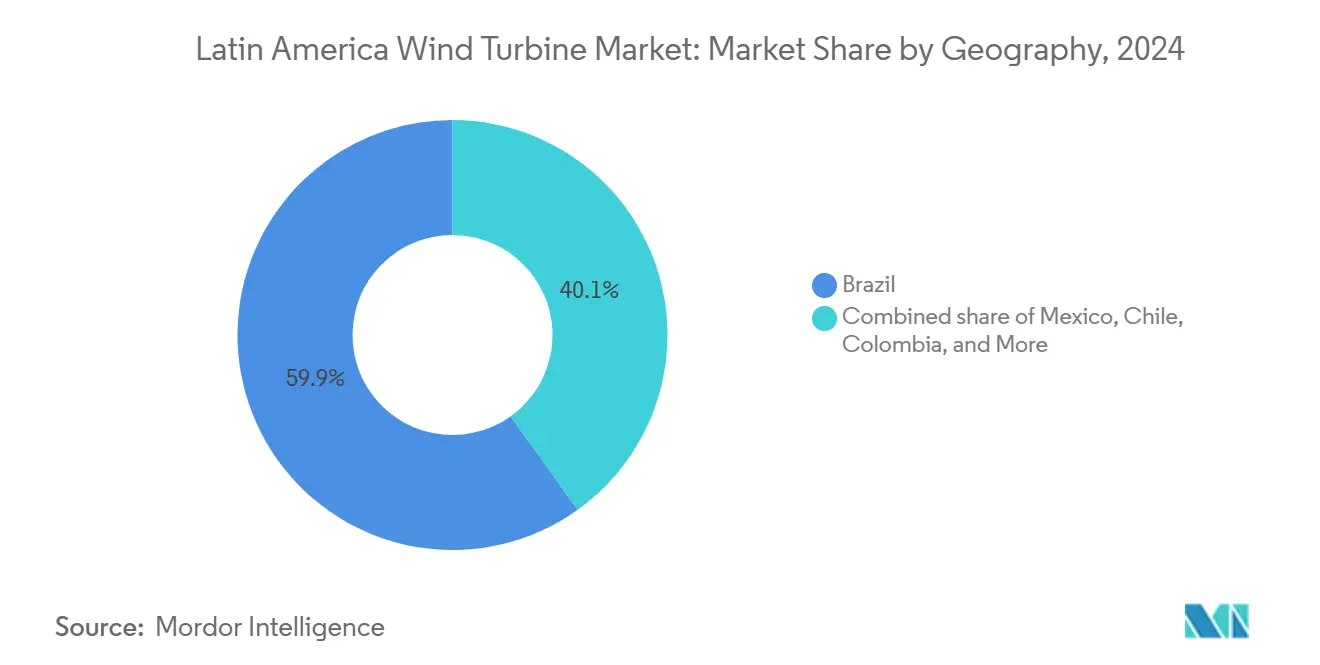

- By geography, Brazil led the Latin American wind turbine market with a 59.9% market share in 2024, while Chile is projected to post the fastest growth rate of 12.5% CAGR through 2030.

Latin America Wind Turbine Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining LCOE for On-shore Wind | +2.8% | Brazil, Chile, Mexico | Medium term (2-4 years) |

| Accelerating Renewable-PPA & Auction Pipeline | +2.1% | Brazil, Colombia, Chile | Short term (≤ 2 years) |

| National Decarbonisation Targets (NDC-aligned) | +1.6% | Global | Long term (≥ 4 years) |

| Green-Hydrogen Export Hubs in Patagonia & NE Brazil | +1.3% | Chile, Argentina, Brazil | Long term (≥ 4 years) |

| Data-centre-led Transmission Upgrades (Amazon, MSFT) | +0.9% | Brazil, Mexico, Chile | Medium term (2-4 years) |

| State-level Manufacturing Incentives in Ceará & Pernambuco | +0.6% | Brazil | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining LCOE for On-shore Wind

Wind auctions in Brazil cleared at prices below USD 30/MWh in 2024, the lowest ever recorded for the technology in Latin America. Similar bids in Chile undercut combined-cycle gas and helped the nation sharpen its green-hydrogen cost target of USD 1.05/kg by 2030. Turbine makers stretch rotor diameters beyond 80 meters, boosting capacity factors above 45% across Northeast Brazil. Chinese OEM Goldwind invested USD 28.6 million in a local plant, slicing import duties and creating fresh, skilled jobs. These interlinked cost declines widen the customer pool to energy-intensive miners, steel mills, and hyperscale data centers, thereby expanding the Latin American wind turbine market.

Accelerating Renewable-PPA & Auction Pipeline

Latin American energy ministries have refined auction designs, striking a balance between seller revenue security and consumer price discipline. Brazil held its first 1 GW offshore tender in 2024.[1]Greenberg Traurig, "Latin America Energy Updates: September and October 2024," gtlaw.com Colombia’s December 2024 auction attracted Equinor and Iberdrola to La Guajira’s high-speed corridors. Parallel corporate PPAs signed by Amazon and Microsoft provide an extra layer of demand certainty. These contracts lower project risk premiums, resulting in cheaper capital and quicker build times for the Latin American wind turbine market.

National Decarbonisation Targets (NDC-aligned)

Brazil’s net-zero roadmap targets 110–195 GW of cumulative wind by 2050. Chile enshrined carbon neutrality by 2050, elevating wind as the backbone of both domestic power and hydrogen exports. Mexico’s policy path is less settled but still targets 45% clean electricity by 2030, keeping development options alive despite state-utility quotas.[2]Baker Institute, “Sheinbaum’s Energy Policies,” BAKERINSTITUTE.ORG These targets anchor long-term demand and sustain political backing across economic cycles, further stabilizing the Latin America wind turbine market.

Green-Hydrogen Export Hubs in Patagonia & NE Brazil

Chile’s Magallanes region hosts HNH Energy’s planned 5 GW wind-to-hydrogen complex, designed to output 255,000 t annually. Argentina’s Río Negro aims for 2.2 million t by 2030 via an USD 8.4 billion Fortescue facility. Ceará’s Pecém port is branding itself as Latin America’s first large-scale hydrogen export terminal.[3]Recharge News, “Offshore Hydrogen Platforms,” RECHARGENEWS.COM These mega-schemes raise demand for new turbines, high-load-factor sites, and advanced power-conversion kits, expanding the Latin America wind turbine market beyond power generation into industrial feedstocks.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid Congestion & Curtailment in NE Brazil | -1.8% | Brazil Northeast | Short term (≤ 2 years) |

| Turbine-component Port & Logistics Bottlenecks | -1.3% | Brazil, Chile, Colombia | Medium term (2-4 years) |

| Mexican Regulatory Uncertainty post-2024 Elections | -0.9% | Mexico | Short term (≤ 2 years) |

| Indigenous-community Opposition (Oaxaca, La Guajira) | -0.6% | Mexico, Colombia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion & Curtailment in NE Brazil

Curtailment exceeded 11% of potential output in Rio Grande do Norte in 2024, eroding revenue streams and pushing loan covenants close to breach limits. The National Electric System Operator forecasts at least three further summers of transmission deficit until new 500 kV lines enter service in 2027. Although Brasília has approved compensation rules, guidelines on payment caps remain unclear, clouding near-term cash flow forecasts. Lenders now require dynamic curtailment modeling as part of due diligence, which raises transaction costs for developers.

Turbine-Component Port & Logistics Bottlenecks

Blades longer than 80 m now test wharf cranes at Rio Grande and Pecém. Siemens Gamesa’s 21 MW prototype utilizes 140 m long blades, which could require broader roads and taller overpasses. Port queues add three weeks of lead-time risk and raise transport insurance premiums, slowing turbine arrival schedules for the Latin America wind turbine market.

Segment Analysis

By Location of Deployment: Offshore Acceleration Despite On-shore Dominance

Onshore farms owned 91.1% of the Latin American wind turbine market in 2024, equivalent to 21 GW of installed capacity in Brazil alone. Offshore projects, although still in their early stages, are forecast to grow at an 18.7% CAGR, potentially increasing their share of the Latin America wind turbine market size to approximately USD 2.3 billion by 2030. Brazil’s 189 GW pipeline, under environmental review, demonstrates policy traction under Law 14,286/2021. Colombia’s La Guajira auction offers 30-year concession rights with corporate tax holidays, attracting European utilities.

Fixed-bottom units lead today’s installations, but floating designs will access deeper waters with 50 – 60% capacity factors. Yard operators in Rio Grande are adapting dry-docks for monopile fabrication. Developers expect to receive the first steel by 2028, subject to offtake deals with future hydrogen export plants. Each milestone enhances supply-chain visibility and shifts the Latin America wind turbine market toward a more balanced split between land-based and offshore installations.

By Capacity Rating: Technology Migration Toward Larger Turbines

Machines rated 1 to 5 MW contributed 46.3% to the Latin American wind turbine market size in 2024, benefiting from established lift capacity limits on road cranes. Yet turbines above 5 MW will expand at a rate of 14.3% annually, driven by developers seeking higher energy output per foundation. Siemens Gamesa’s 21 MW concept could raise annual energy capture by one-third.

Smaller units, ranging from 100 kW to 1 MW, address rural microgrids from Patagonia to the Amazon. Meanwhile, Goldwind’s Ceará plant will assemble 6 to 8 MW nacelles with 90% local content, unlocking BNDES credit at a rate below Brazil’s SELIC rate. That financing edge should further swell the Latin America wind turbine market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Axis Type: Horizontal Dominance with Vertical Niche Growth

Horizontal-axis turbines accounted for 90.7% of 2024 installations, favored for their aerodynamic efficiency and mature supply chain. Vertical-axis designs are projected to climb 12.9% per year, driven by the integration of rooftop and street-lamp systems in urban hubs where noise limits hinder conventional rotor designs. Start-ups are trialing 10 kW helical units on top of high-rise complexes in São Paulo.

Grid codes now reward reactive-power support, and vertical units with power-electronics upgrades can supply this service, creating micro-niches that add incremental demand to the Latin America wind turbine market.

By Component: Rotor Blades Lead with Power Electronics Advancing

Rotor blades claimed 31.8% of component revenue in 2024. Carbon-fiber spars and segmented mold technology cut weight by 18%, curbing tower-top mass. Power electronics and control systems are expected to register a 12.1% CAGR, as inverter size must scale with turbine ratings, and grid operators increasingly request synthetic inertia.[4]Vestas, “Annual Report 2024,” VESTAS.COM

Direct-drive generator adoption rises in parallel, reducing gearbox maintenance call-outs and improving uptime, key for the Latin American wind turbine market, where remote projects often face lengthy repair times.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-Use Application: Utility-Scale Dominance with Commercial & Industrial Uptick

Utility-scale projects remained the backbone, accounting for an 85.5% share in 2024, as state auctions sought the lowest-cost megawatt hours. Yet commercial & industrial (C&I) buyers now sign 10- to 15-year PPAs, spurring a 14.8% CAGR in that segment. Amazon’s latest 620 MW Brazilian PPA bundled hourly matching, a first for the region.

Smaller mining camps in the Atacama Desert are installing micro-grids that pair 5 MW wind arrays with batteries, broadening the Latin American wind turbine market beyond centralized dispatch.

Geography Analysis

Brazil anchors 59.9% of 2024 installations and hosts Latin America’s most complete turbine supply chain. Its Northeast states deliver capacity factors above 45% thanks to year-round trade winds. Employment stood at 260,000 in 2024, and the domestic content rule spurred WEG to source 90% of nacelle parts locally. Still, grid curtailment shaved 4 TWh from potential generation in 2024, prompting Brasília to fast-track 765 kV corridors and a USD 2.2 billion compensation fund.

Chile, with a 12.5% forecast CAGR, couples world-class wind in Magallanes with solar in Atacama, creating hybrid export platforms. AES Andes secured clearance for its 1.2 GW Pampas Hybrid Park, a USD 800 million venture that combines wind, solar, and storage. ENGIE’s 342 MW Lomas del Taltal came online in early 2025, demonstrating Chile’s project-execution depth.[5]EVWind, “ENGIE Completes Taltal,” EVWIND.ES

Mexico’s cap of 9,550 MW renewable capacity by 2030 clouds investor visibility. Sempra’s 320 MW Cimarron farm still reached notice-to-proceed in 2024, but financiers priced in regulatory risk premia. Colombia’s La Guajira coastline could host 109 GW offshore, and Ecopetrol’s 1,087 MW Jemeiwaa Ka’I cluster signals oil-sector pivot toward wind. Argentina’s Patagonia sees USD 8.4 billion pledged for Fortescue’s hydrogen megaproject, aligning transmission proposals with export terminals. Across smaller markets, such as Uruguay and Peru, asset swaps by ACCIONA Energía and others keep balance-sheet rotation active, laying the groundwork for cross-border interconnectors that may one day widen the Latin American wind turbine market.

Note: Segment shares of all individual segments available upon report purchase

Competitive Landscape

The top five OEMs—Vestas, Siemens Gamesa, GE Vernova, Nordex, and Goldwind—controlled roughly 70% of 2024 shipments. Each firm bundles service contracts spanning 20-plus years, exchanging guaranteed availability for recurring fees. Goldwind’s new Ceará factory secures low-cost shipping to Argentina and Chile, closing price gaps with incumbent Western suppliers. Siemens Gamesa’s 21 MW offshore prototype highlights the arms race in turbine scale and digitalization.

Developers now chase platform synergies. AES Andes pairs wind with solar and 250 MWh of batteries, enabling firm power delivery without the need for gas peakers. Invenergy and Patria Investments acquired a 600 MW Brazilian portfolio from ContourGlobal, prioritizing projects eligible for 100% merchant exposure. Oil major Petrobras issued seabed survey tenders in June 2025, eyeing floating-wind pilots that could leverage FPSO supply chains. Ecopetrol copied the playbook by purchasing Enel’s wind assets in July 2025.

Digital twins and predictive analytics differentiate service offerings. Vestas’ 2024 annual report cites EUR 17.3 billion in revenue from 17 GW orders, crediting its data platform for a 2-percentage-point margin improvement. OEMs open spare-parts depots in Recife and Buenos Aires to cut turbine downtime, further professionalizing the Latin America wind turbine market.

Latin America Wind Turbine Industry Leaders

-

Vestas Wind Systems A/S

-

Siemens Gamesa Renewable Energy SA

-

GE Vernova (GE Renewable Energy)

-

Nordex SE

-

Goldwind

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: Petrobras launched survey tenders for its offshore wind pilot project, marking the state oil company’s entry into renewable energy development and potentially accelerating Brazil’s offshore wind sector growth.

- July 2025: Ecopetrol acquired a wind power project from Enel in Colombia, demonstrating the oil sector’s strategic diversification into renewables and expanding the addressable market for wind energy development.

- May 2025: CBA acquired stakes in wind power plants from Auren and Casa dos Ventos in Brazil, reflecting continued consolidation activity in the country’s wind energy sector.

- March 2025: Nordex Group secured a 112 MW order from Auren Energia in Brazil, indicating sustained demand for wind turbine equipment in the region’s largest market.

Latin America Wind Turbine Market Report Scope

The Latin America wind turbine market report includes:

By Location of Deployment

| Onshore | |

| Offshore | Fixed-bottom |

| Floating |

By Capacity Rating

| Small (Below 100 kW) |

| Medium (100 kW to 1 MW) |

| Large (1 to 5 MW) |

| Very Large (Above 5 MW) |

By Axis Type

| Horizontal Axis |

| Vertical Axis |

By Component

| Rotor Blades |

| Nacelle and Drivetrain |

| Generator |

| Tower |

| Power-Electronics and Control |

By End-Use Application

| Utility-Scale |

| Commercial and Industrial |

| Residential and Micro-grid |

By Geography

| Brazil |

| Mexico |

| Chile |

| Argentina |

| Colombia |

| Rest of Latin America |

| By Location of Deployment | Onshore | |

| Offshore | Fixed-bottom | |

| Floating | ||

| By Capacity Rating | Small (Below 100 kW) | |

| Medium (100 kW to 1 MW) | ||

| Large (1 to 5 MW) | ||

| Very Large (Above 5 MW) | ||

| By Axis Type | Horizontal Axis | |

| Vertical Axis | ||

| By Component | Rotor Blades | |

| Nacelle and Drivetrain | ||

| Generator | ||

| Tower | ||

| Power-Electronics and Control | ||

| By End-Use Application | Utility-Scale | |

| Commercial and Industrial | ||

| Residential and Micro-grid | ||

| By Geography | Brazil | |

| Mexico | ||

| Chile | ||

| Argentina | ||

| Colombia | ||

| Rest of Latin America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Latin America wind turbine market?

The Latin America wind turbine market size is USD 8.90 billion in 2025 and is projected to reach USD 14.19 billion by 2030.

Which country dominates installations?

Brazil holds 59.9% of 2024 capacity, supported by 21 GW already connected to its grid.

Where is the fastest growth expected?

Chile is forecast to expand at a 12.5% CAGR thanks to supportive hydrogen and export-energy policies.

Which turbine class is expanding quickest?

Units above 5 MW are set to grow 14.3% annually as developers chase higher energy per foundation.

Why are offshore projects gaining interest?

New frameworks in Brazil and Colombia and capacity factors above 50% make offshore wind attractive for power and hydrogen export projects.

What hurdle most affects near-term growth?

Grid congestion in Northeast Brazil triggers curtailment, cutting revenues until new high-voltage lines come online in 2027.

Page last updated on: