Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

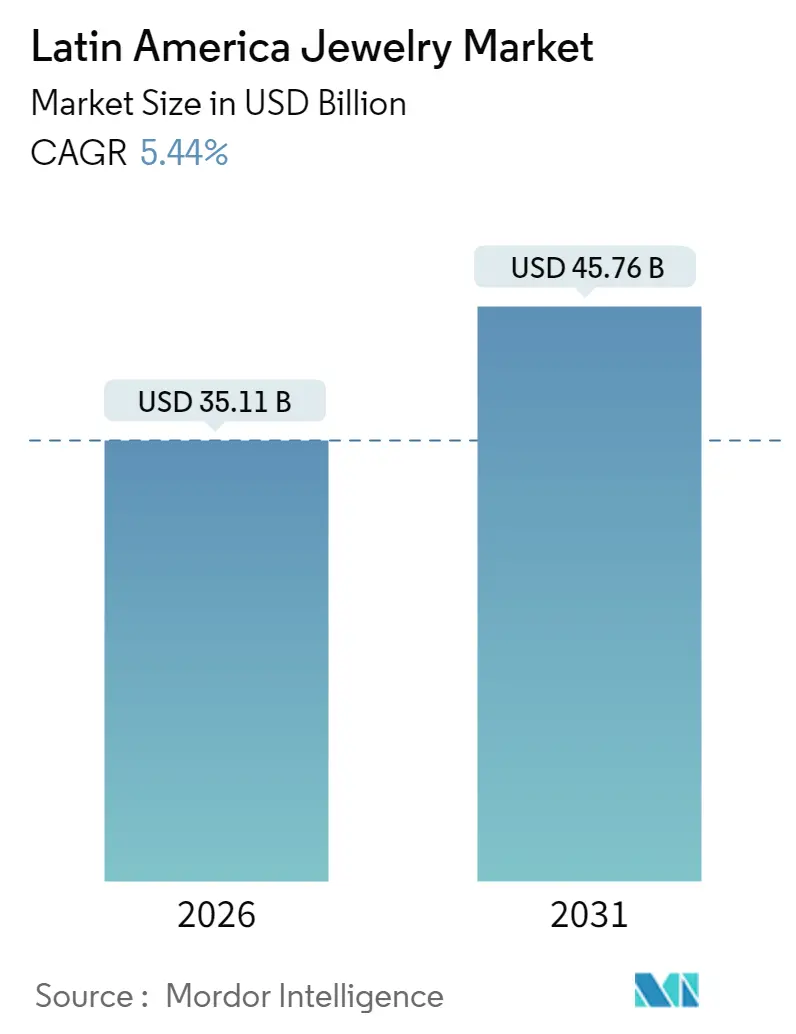

| Market Size (2026) | USD 35.11 Billion |

| Market Size (2031) | USD 45.76 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Latin America Jewelry Market Analysis by Mordor Intelligence

Latin America jewelry market size in 2026 is estimated at USD 35.11 billion, growing from 2025 value of USD 33.30 billion with 2031 projections showing USD 45.76 billion, growing at 5.44% CAGR over 2026-2031. This trajectory reflects structural shifts in consumer behavior, with self-gifting and investment-oriented purchases now accounting for a larger share of transactions than traditional occasion-driven demand. Brazil commands 45.91% of the regional revenue in 2024, yet Argentina is poised to outpace all peers at 6.74% CAGR through 2030, propelled by macroeconomic stabilization and a forecast GDP rebound of around 5.0% in 2025. The divergence between Brazil's mature installed base and Argentina's accelerating growth underscores how currency normalization and policy reforms can unlock latent luxury demand faster than incremental wealth accumulation. Elevated gold and silver prices, the rollout of lab-grown stones, and amplified celebrity marketing are reshaping assortment strategies, while supply-chain transparency moves from premium differentiator to baseline expectation. Omnichannel execution is increasingly decisive because first-time luxury buyers begin their journeys online even when final purchases still occur in stores. Competitive intensity remains high, but formal players that couple retail expansion with responsible sourcing are positioned to consolidate share as regulatory scrutiny rises and informal vendors struggle to meet traceability standards

Key Report Takeaways

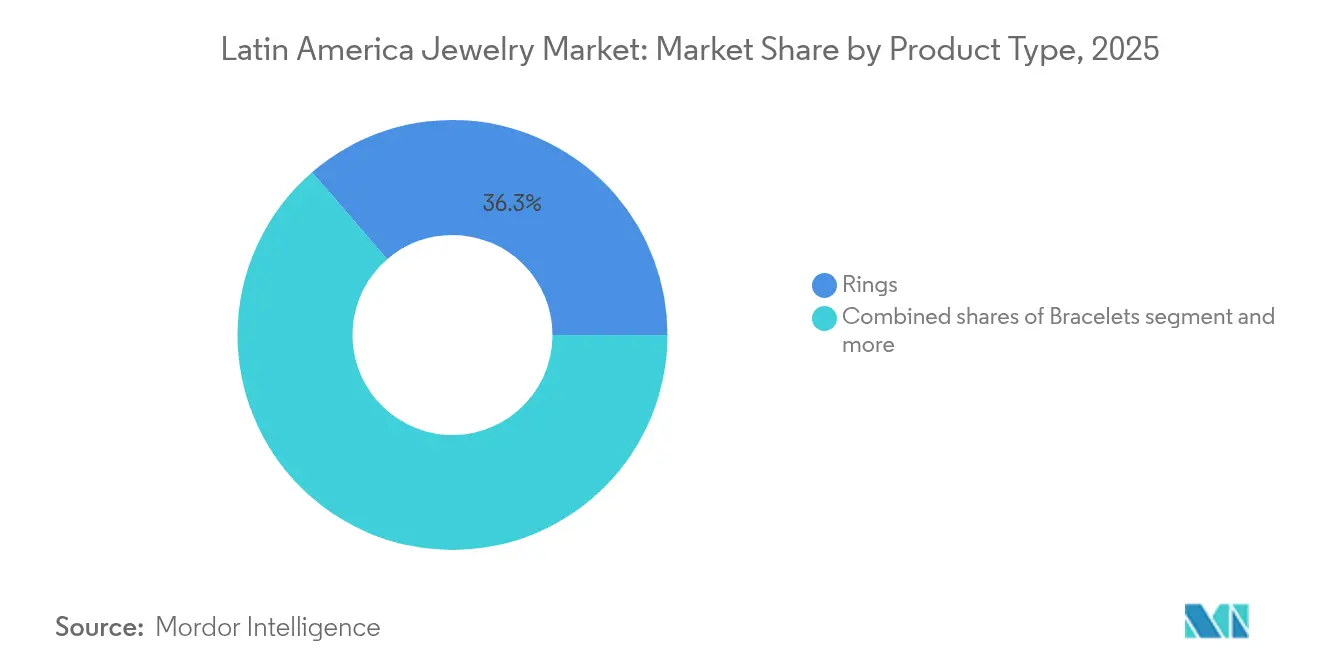

- By product type, rings captured 36.33% of the South America jewelry market share in 2025, while bracelets are forecast to expand at a 6.90% CAGR through 2031.

- By material, precious metals commanded a 64.58% share in 2025; mixed materials are projected to grow at a 6.31% CAGR.

- By category, fine jewelry accounted for 81.72% of the South America jewelry market size in 2025, whereas costume jewelry is advancing at a 6.25% CAGR.

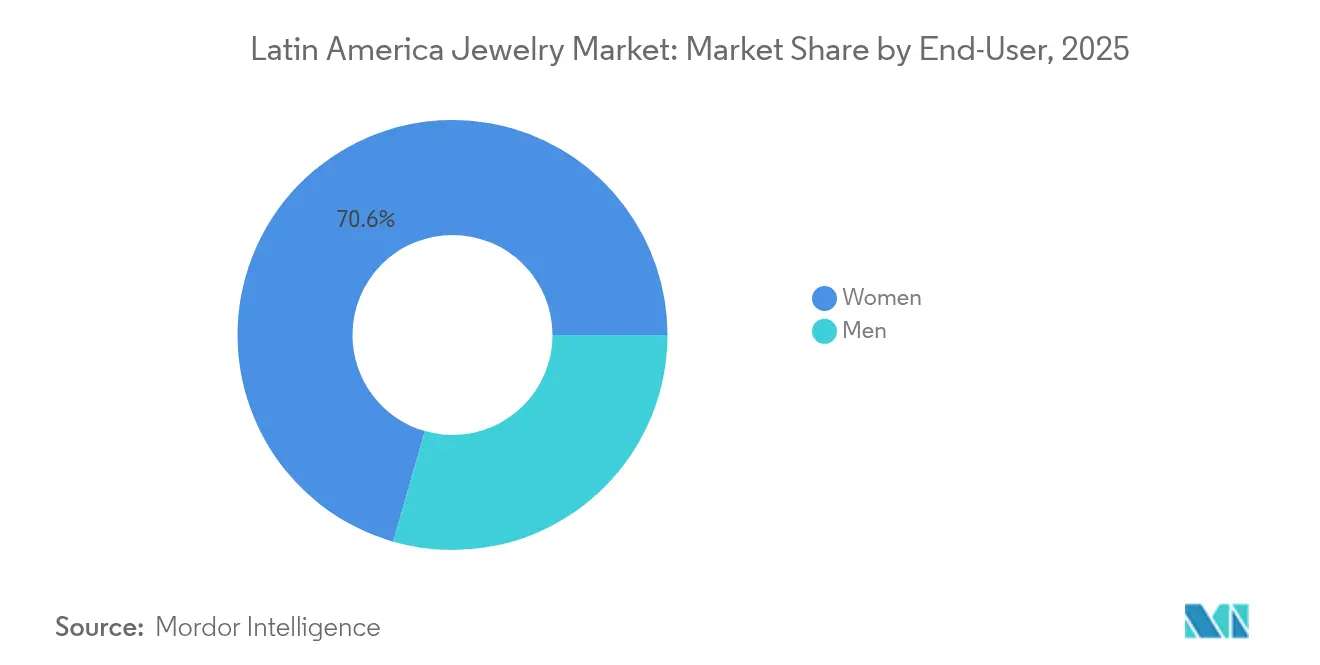

- By end user, women generated 70.55% of 2025 revenue, yet men’s collections are set to rise at a 7.50% CAGR.

- By distribution channel, offline retail stores generated 86.10% of the 2025 revenue; however, online retail stores are set to rise at a 5.79% CAGR.

- By geography, Brazil led with 45.40% revenue share in 2025; Argentina is poised to record a 6.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Latin America Jewelry Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of customized and personalized jewelry pieces | +1.2% | Brazil, Argentina, Chile; strongest in urban centers São Paulo, Buenos Aires, Santiago | Medium term (2-4 years) |

| Celebrity endorsements boost jewelry brand awareness | +0.9% | Global with amplification in Brazil, Mexico, Argentina, via social media and streaming platforms | Short term (≤ 2 years) |

| Demand for ethically sourced and sustainable jewelry | +0.8% | Brazil, Colombia, Peru; driven by urban millennials and Gen Z in São Paulo, Bogotá, Lima | Long term (≥ 4 years) |

| Expansion of retail chains and boutique stores | +1.0% | Brazil, Chile, Colombia; secondary cities Goiânia, Medellín, and Valparaíso are gaining traction | Medium term (2-4 years) |

| Increasing awareness of jewelry as an investment asset | +0.7% | Argentina, Brazil, heightened by currency volatility and inflation hedging behavior | Short term (≤ 2 years) |

| Rising demand for lab-grown and synthetic gemstones | +0.6% | Brazil, Mexico, Argentina; early adopters in São Paulo, Mexico City, Buenos Aires | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Customized and Personalized Jewelry Pieces

Customization has evolved from niche engraving services to full co-design platforms where consumers select metals, stones, and motifs, a shift that increases average transaction values and repeat-purchase rates. H.Stern's Genesis collection, launched in 2025 with price points ranging from USD 2,900 to USD 47,000, exemplifies this trend by offering modular designs that allow buyers to swap colored stones and adjust settings post-purchase. The economics favor brands with flexible manufacturing, as personalized pieces command 20% to 30% premiums over catalog items while reducing inventory risk. Social commerce accelerates adoption, with small and medium-sized jewelers in Brazil leveraging WhatsApp and Instagram to co-create designs with clients, a practice that bypasses traditional retail overhead and compresses time-to-market from weeks to days. This democratization of customization pressures established players to invest in digital configurators and agile supply chains or risk ceding share to artisans who can iterate designs in real time.

Celebrity Endorsements Boosting Jewelry Brand Awareness

Celebrity partnerships now function as demand-generation engines rather than passive brand associations, with measurable sales lifts tied to campaign launches. David Yurman's appointment of Mexican actress Eiza González as global brand ambassador for its Spring 2025 Sculpted Cable campaign signals a strategic pivot toward Latin American and U.S. Hispanic audiences, leveraging González's 8.6 million Instagram followers and her narrative of immigrant heritage to build cultural affinity. Swarovski's naming of Ariana Grande as global ambassador in May 2025 follows a similar playbook, targeting younger consumers who prioritize pop-culture relevance over heritage. The impact extends beyond awareness, as celebrity-endorsed collections often sell out within hours of launch, creating scarcity-driven demand and secondary-market premiums. For Latin American brands, the challenge lies in securing regional ambassadors with cross-border appeal, as evidenced by True Religion's use of Brazilian pop star Anitta in February 2025 to anchor its "Own Your True" platform, a campaign designed to reach music and fashion audiences across Latin America and the U.S. diaspora.

Demand for Ethically Sourced and Sustainable Jewelry

Sustainability credentials have transitioned from marketing differentiators to minimum requirements for brands targeting millennial and Gen Z buyers, who increasingly audit supply chains before purchase. Pandora's commitment to 100% recycled gold and silver by 2025 and its rollout of lab-grown diamonds in Brazil and Mexico reflect this shift, as the company positions traceability as a core value proposition rather than a premium feature. The urgency is amplified by enforcement actions, including Brazil's deployment of forensic technology in December 2024 to trace illicit Amazon gold, a move that could disqualify suppliers unable to prove provenance and force brands to consolidate sourcing around certified refiners. Indigenous Brazilian model Zaya's advocacy for ethical jewelry, often wearing traditional feathered earrings made by artisans, illustrates how cultural narratives around sustainability can drive demand for locally crafted, deforestation-free pieces, creating opportunities for brands that partner with Indigenous communities and NGOs like The Slow Factory. The commercial implication is clear: brands without transparent sourcing risk reputational damage and loss of distribution as retailers impose vendor sustainability audits.

Expansion of Retail Chains and Boutique Stores

Physical retail expansion remains a growth lever despite e-commerce gains, as jewelry purchases above USD 500 still skew toward in-store transactions where buyers can assess quality and fit. Tiffany & Co. opened its São Paulo flagship in January 2025, a 408-square-meter space in Iguatemi mall featuring a dedicated watches area and High Jewelry salon, and announced plans for a fifth store in Goiânia, an agribusiness-driven city where high-net-worth individuals are accumulating wealth faster than in traditional luxury hubs. TOUS opened its largest Latin American store in Chile's Alto Las Condes mall in March 2025 (73 square meters) and followed with a Bogotá location in June 2025, reflecting a strategy to anchor brand presence in secondary cities before competitors saturate the market. Van Cleef & Arpels' October 2024 opening of a 2,701-square-foot boutique in São Paulo's Cidade Jardim signals that ultra-luxury brands view Brazil as a viable market for high-jewelry salons, a format that requires sustained local demand to justify the capital intensity. The geographic dispersion of store openings, from Santiago to Medellín to Goiânia, suggests that wealth creation is no longer concentrated in capital cities, forcing brands to deploy regional real-estate strategies rather than relying on flagship-only models.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High risk of jewelry counterfeiting and imitation products | -0.8% | Brazil, Chile, Argentina; concentrated in e-commerce and informal retail channels | Short term (≤ 2 years) |

| Complex import/export regulations for precious metals | -0.6% | Brazil, Argentina; SISCOMEX licensing and Impuesto País tax create a compliance burden | Medium term (2-4 years) |

| Fluctuating availability of precious stones and metals | -0.7% | Peru, Chile, Colombia; mining output volatility and price spikes compress margins | Short term (≤ 2 years) |

| High competition from local unorganized jewelry vendors | -0.9% | Brazil, Colombia, Peru; artisans and informal sellers capture 40-50% of volume in lower price tiers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Risk of Jewelry Counterfeiting and Imitation Products

Counterfeiting has escalated from low-quality knockoffs to near-perfect replicas that deceive even trained buyers, eroding brand equity and diverting revenue from legitimate channels. U.S. Customs and Border Protection intercepted USD 3.5 million in counterfeit Van Cleef & Arpels jewelry in October 2025, while INTERPOL's Operation Crete II seized 2,478 counterfeit items valued at USD 523,000 in Chile between August and September 2024, demonstrating that Latin America is both a destination and transit route for fake goods [1]Source: U.S. Customs and Border Protection, "Counterfeit Jewelry", cbp.gov. The proliferation of counterfeit jewelry on e-commerce platforms and social media marketplaces forces brands to invest in authentication technologies such as blockchain provenance tracking and micro-engraving, raising operational costs without directly generating revenue. For consumers, the risk of purchasing counterfeits undermines confidence in online channels, slowing the shift to digital retail and reinforcing the importance of authorized dealer networks. Brands that fail to police their trademarks or educate buyers on authentication cues risk permanent damage to pricing power, as widespread availability of convincing fakes establishes a lower reference price in consumers' minds.

Complex Import/Export Regulations for Precious Metals

Brazil's SISCOMEX import licensing system imposes duties ranging from 10 to 35% on jewelry and precious metals, supplemented by IPI (excise tax), ICMS (state VAT), PIS, and COFINS (social-contribution taxes), creating a cumulative tax burden that can exceed 50% of the declared value [2]Source: Brazil Customs, "SISCOMEX", gov.br. Licenses carry a 90-day validity window, forcing importers to synchronize shipments with demand forecasts or risk inventory obsolescence. Argentina's foreign-exchange controls, including the Impuesto País tax on dividend repatriations and BOPREAL instruments for managing capital flows, complicate cross-border transactions and delay payments to international suppliers, straining working capital for brands dependent on imported components [3]Source: Argentina Central Bank, "Statistical Bulletin", bcra.gob.ar. These regulatory frictions favor vertically integrated players like Vivara, which operates gold-recycling programs to source raw materials domestically and bypass import duties, over pure importers that lack manufacturing capabilities. The compliance burden also deters smaller international brands from entering Latin America, reducing competitive intensity in the premium segment and allowing established players to maintain pricing power.

Segment Analysis

By Product Type: Stackable Bracelets Drive Volume Growth

Bracelets are forecast to expand at a 6.90% CAGR from 2026 to 2031, the fastest rate among product types, as stackable designs encourage consumers to purchase multiple units and layer them for personalized looks. Rings held 36.33% market share in 2025, anchored by engagement and wedding bands that benefit from stable demographic demand, yet the category's maturity limits incremental growth. Necklaces and chains with pendants appeal to gifting occasions and self-purchase, with pendant modularity allowing buyers to refresh existing chains by swapping charms, a strategy that increases lifetime customer value. Earrings remain a staple, particularly in markets like Brazil, where pierced ears are near-universal among women, though innovation has stagnated relative to bracelets and rings. Other product types, including decorative hair jewelry and anklets, occupy niche segments but are gaining traction among younger consumers influenced by festival fashion and social-media trends.

The shift toward bracelets reflects broader changes in how consumers wear jewelry, with stacking enabling self-expression and signaling affiliation with brands or causes through charm selection. Pandora's Essence collection, launched in 2024, capitalizes on this trend by offering beads that represent values such as courage and compassion, allowing buyers to curate bracelets that tell personal stories. The commercial implication is that brands must design for modularity and cross-selling, as consumers increasingly view jewelry purchases as building blocks for evolving collections rather than standalone items. This dynamic favors players with broad SKU assortments and loyalty programs that incentivize repeat purchases, while pressuring single-product specialists to expand into adjacent categories or risk commoditization.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Mixed Materials Capture Younger Cohorts

Mixed materials, combining precious metals with ceramics, leather, or lab-grown stones, are forecast to grow at a 6.31% CAGR from 2026 to 2031, outpacing precious metals and base metals. The appeal lies in differentiation and affordability, as mixed-material pieces offer design complexity to 30 to 50% Gen Z buyers entering the market. Precious metals retain dominance in fine jewelry, driven by investment demand and cultural preferences for gold in gifting, yet the segment's growth is constrained by input-cost inflation, with gold prices. Base metals serve the costume-jewelry segment, where rapid trend cycles and disposable pricing models prioritize aesthetics over durability, though environmental concerns around mining and waste are prompting some brands to explore recycled base metals.

Pandora's commitment to 100% recycled gold and silver by 2025 signals that sustainability is becoming a material-selection criterion alongside cost and aesthetics, particularly for brands targeting environmentally conscious consumers. The rise of lab-grown diamonds and synthetic gemstones further blurs material boundaries, as these stones can be set in both precious and mixed-material designs, allowing brands to offer diamond jewelry at accessible price points. For Latin American consumers, mixed materials resonate because they enable participation in jewelry trends without the financial commitment of pure precious-metal pieces, a dynamic that is particularly relevant in Argentina and Colombia, where currency volatility and income uncertainty make aspirational purchases more discretionary. The challenge for brands is maintaining perceived quality, as mixed materials risk being dismissed as costume jewelry unless marketing emphasizes craftsmanship and design rather than material purity.

By Category: Fine Jewelry Anchors Revenue, Costume Segment Gains Share

Fine jewelry commanded 81.72% market share in 2025, reflecting Latin America's cultural affinity for gold and precious stones in weddings, religious ceremonies, and milestone celebrations. Costume or fashion jewelry is forecast to grow at a 6.25% CAGR from 2026 to 2031, driven by fast-fashion retailers and social-media-driven trend cycles that encourage frequent purchases of lower-priced items. The bifurcation creates distinct competitive dynamics, with fine jewelry dominated by heritage brands and regional champions that emphasize provenance and resale value, while costume jewelry is contested by fast-fashion players, online marketplaces, and influencer-led brands that prioritize speed-to-market and viral aesthetics. Vivara's Life brand, positioned as an accessible line within its portfolio, illustrates how established fine-jewelry players are defending share in the costume segment by leveraging brand equity and distribution networks to compete with pure-play fashion jewelry vendors.

The growth of costume jewelry also reflects changing consumer behavior, as buyers increasingly maintain dual wardrobes, fine pieces for special occasions and costume items for daily wear, rather than wearing expensive jewelry regularly and risking loss or damage. This segmentation is most pronounced among younger consumers, who allocate discretionary income across multiple categories (apparel, electronics, travel) and view jewelry as one of many self-expression tools rather than a primary status symbol. For brands, the implication is that omnichannel strategies must accommodate both high-touch, consultative sales for fine jewelry and frictionless, impulse-driven transactions for costume pieces, requiring distinct retail formats, inventory management, and marketing approaches within a single organization. The risk is brand dilution, as extending into costume jewelry can undermine the exclusivity that underpins fine-jewelry pricing power, a tension that Kering's jewelry Houses navigate by maintaining separate brand identities for high jewelry (Boucheron) and accessible luxury (Pomellato).

By End User: Men's Jewelry Surges on Celebrity Influence

Men's jewelry is forecast to expand at a 7.50% CAGR from 2026 to 2031, the fastest growth rate among end-user segments, as chains, rings, and bracelets transition from niche accessories to mainstream wardrobe staples. Women held 70.55% market share in 2025, anchored by engagement rings, earrings, and necklaces that benefit from entrenched gifting traditions and higher average transaction values. Children's jewelry occupies a small but stable segment, concentrated in gold bracelets and necklaces purchased for baptisms and birthdays, with demand closely tied to birth rates and cultural practices. The surge in men's jewelry reflects multiple converging forces, including celebrity endorsements that normalize wearing visible accessories, the rise of athleisure and casual dress codes that accommodate jewelry, and social-media platforms where male influencers showcase layered chains and statement rings as part of personal branding.

David Yurman's appointment of Eiza González as global brand ambassador for its Spring 2025 Sculpted Cable campaign explicitly highlights the collection's cross-gender appeal, with González noting that the Cable motif attracts both men and women. The commercial opportunity is substantial, as men's jewelry penetration remains low relative to women's, creating headroom for brands that can overcome historical stigma and educate male consumers on styling and occasion-appropriate wear. For Latin American brands, the challenge is balancing masculine aesthetics, thicker chains, larger rings, muted colors, with the craftsmanship and material quality that justify premium pricing, as men are less likely than women to purchase jewelry for its own sake and more likely to view it as a functional accessory that signals status or affiliation. The growth trajectory suggests that brands investing in men's-specific collections, targeted marketing, and retail environments that feel welcoming to male shoppers will capture disproportionate share in the coming years.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Offline Dominance Persists Despite E-Commerce Gains

Offline retail stores held 86.10% market share in 2025, reflecting jewelry's high-involvement purchase process, where consumers prioritize tactile evaluation, fit testing, and in-person consultation before committing to transactions above USD 500. Online retail stores are forecast to grow at a 5.79% CAGR from 2026 to 2031, driven by improved product visualization tools, augmented-reality try-on features, and the proliferation of brand-owned e-commerce sites that offer seamless returns and authentication guarantees. The persistence of offline dominance is most pronounced in fine jewelry, where trust and perceived risk remain barriers to online conversion, while costume jewelry has migrated more rapidly to digital channels due to lower price points and reduced purchase anxiety. Pandora's addition of 70 stores in Brazil over 18 months, bringing its total to 161 locations, underscores that even digitally native brands recognize the importance of physical touchpoints for building brand awareness and capturing high-value transactions.

E-commerce penetration varies by country, with Brazil's digital-buyer base exceeding 100 million and the broader e-commerce market reaching USD 81.74 billion, creating infrastructure and consumer familiarity that reduce friction for online jewelry purchases. MercadoLibre's dominance in Latin American e-commerce provides a ready-made distribution channel for brands willing to cede some control over customer experience in exchange for access to its 140 million active users, though luxury brands remain cautious about marketplace presence due to concerns about counterfeiting and brand dilution. The future likely involves hybrid models where consumers research online, visit stores to evaluate products, and complete purchases through whichever channel offers the best combination of convenience, price, and assurance, forcing brands to integrate inventory, pricing, and customer data across channels or risk losing sales to competitors with superior omnichannel execution. Tiffany & Co.'s January 2025 opening of a São Paulo flagship with dedicated watches and High Jewelry spaces signals that even digitally sophisticated brands view physical retail as essential for ultra-premium categories where experiential elements and personal service justify the real-estate investment.

Geography Analysis

Brazil captured 45.40% of Latin America jewelry revenue in 2025, anchored by a high-net-worth population of approximately 1.3 million individuals projected to reach 1.5 million by 2030. The country's dominance reflects not just population scale but also the concentration of wealth in São Paulo and Rio de Janeiro, where flagship stores from Tiffany, Van Cleef & Arpels, and H.Stern anchor luxury shopping districts. However, secondary cities like Goiânia are emerging as hotspots, driven by agribusiness wealth that is creating new cohorts of affluent consumers outside traditional metropolitan areas, prompting brands to expand beyond coastal hubs. Vivara's plan to open 40 to 50 stores in 2025 illustrates how domestic champions leverage local knowledge and supply-chain integration, including gold recycling, to compete against international luxury houses.

Argentina is forecast to grow at a 6.62% CAGR from 2026 to 2031, the fastest rate in the region, propelled by macroeconomic stabilization. The country's mining exports surged 32.9% year-over-year to USD 4.213 billion in the first nine months of 2025, with gold accounting for USD 2.911 billion and prices exceeding USD 4,000 per ounce, creating wealth effects that filter into luxury consumption. The unwinding of foreign-exchange controls, including the Impuesto País tax, is expected to ease capital flows and improve access to imported goods, reducing the premium that Argentine consumers pay relative to neighboring countries. However, the market remains fragmented, with informal vendors capturing a significant share due to consumers' historical preference for cash transactions and distrust of institutions, a dynamic that will take years to reverse even as the formal economy stabilizes.

Chile, Colombia, and Peru collectively represent emerging opportunities, with Chile benefiting from political stability and a mature retail infrastructure that attracted TOUS to open its largest Latin American store in Santiago's Alto Las Condes mall in March 2025. Colombia's jewelry market is shaped by artisanal traditions and the presence of emerald mines, though security concerns and illicit gold flows, including the theft of 3 tons of gold from the Buriticá mine in November 2024, complicate supply-chain transparency. Peru's role as a major gold and silver producer positions the country as a supply hub, with Compañía de Minas Buenaventura reporting a realized silver price hike in the third quarter of 2025, yet domestic jewelry consumption remains constrained by income levels and limited retail infrastructure outside Lima. The rest of Latin America, including Ecuador, Bolivia, and Paraguay, accounts for a small share of regional revenue but offers long-term potential as GDP growth and urbanization expand the addressable market for accessible luxury and costume jewelry.

Competitive Landscape

The Latin America jewelry market registers a low concentration, indicating extreme fragmentation where global luxury conglomerates, regional champions, and thousands of unorganized artisans compete across overlapping price tiers and distribution channels. Vivara's revenue of (USD 516 million) positions the company as the largest organized player, yet its planned opening of 40 to 50 stores in 2025 signals that even dominant domestic brands see room to capture share from informal vendors who avoid VAT and labor regulations.

Pandora's addition of 70 stores in Brazil over 18 months, bringing its total to 161 locations, demonstrates how international players are deploying capital-intensive retail expansion to build brand awareness and compete on convenience, while Richemont's Americas sales grew in fiscal 2025, driven by Jewellery Maisons and the September 2024 acquisition of Vhernier, which adds high-jewelry capabilities to its portfolio. Kering's jewelry Houses, Boucheron and Pomellato, achieved double-digit growth in the first half of 2024, with the group explicitly prioritizing exclusive distribution and intensified communications to nurture desirability, a strategy that reduces wholesale partnerships and concentrates sales in directly operated boutiques.

Technology is emerging as a competitive differentiator, with brands deploying augmented-reality try-on tools, blockchain provenance tracking, and dynamic pricing algorithms to reduce friction and build trust in online channels, though adoption remains nascent relative to other luxury categories. The persistence of unorganized competition, estimated at 40 to 50% of unit volume in lower price tiers, creates a long-term formalization opportunity for brands that can offer warranties, resale programs, and quality assurance that informal vendors cannot credibly match. Regulatory compliance, particularly Brazil's forensic technology for tracing illicit gold deployed in December 2024, is raising the bar for supply-chain transparency and could consolidate sourcing around certified refiners, disadvantaging smaller players unable to afford auditing costs.

Latin America Jewelry Industry Leaders

-

Vivara Participações S.A.

-

HStern Indústria e Comércio SA

-

Pandora A/S

-

Compagnie Financière Richemont SA

-

LVMH Moët Hennessy Louis Vuitton SE

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: H&M, the Swedish fast-fashion titan, made its Brazilian debut with the opening of its inaugural brick-and-mortar store. In tandem, the retailer also kicked off its online operations in the nation. Significantly, H&M had been locally producing select items in Brazil, including footwear, beachwear, and accessories. The flagship store, nestled in a posh shopping mall in São Paulo, primarily showcased women's fashion.

- December 2024: Tiffany & Co. has unveiled its newest flagship store in Brazil, situated in the upscale Iguatemi São Paulo. The store, covering 408 square meters across two levels, draws design inspiration from the House's iconic Fifth Avenue flagship, The Landmark. This flagship brings a host of exclusive experiences to Brazil, including a dedicated section for Tiffany & Co. watches, an "All About Love" area highlighting the brand's signature engagement rings, and a bespoke High Jewelry salon.

Latin America Jewelry Market Report Scope

Jewelry refers to the personal ornaments of men and women, typically used to accessorize oneself. The Latin American jewelry market is segmented by product type, category, material, distribution channel, and geography. By product type, the market is segmented into necklaces, rings, earrings, and more. By category, the market is segmented into fine jewelry and costume jewelry. By material, the market is segmented into precious metals, base metals, and mixed materials. By end-user, the market is segmented into women, men, and children. By distribution channel, the market is segmented into offline retail stores and online retail stores, and geography (Brazil, Argentina, and more). The market forecasts are provided in terms of value (USD).

Product Type

| Necklaces |

| Rings |

| Earrings |

| Bracelets |

| Chains and Pendants |

| Other Product Types |

Material

| Precious Metals |

| Base Metals |

| Mixed Materials |

Category

| Fine Jewelry |

| Costume/Fashion Jewelry |

End User

| Women |

| Men |

| Children |

Distribution Channel

| Offline Retail Stores |

| Online Retail Stores |

Geography

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| Product Type | Necklaces |

| Rings | |

| Earrings | |

| Bracelets | |

| Chains and Pendants | |

| Other Product Types | |

| Material | Precious Metals |

| Base Metals | |

| Mixed Materials | |

| Category | Fine Jewelry |

| Costume/Fashion Jewelry | |

| End User | Women |

| Men | |

| Children | |

| Distribution Channel | Offline Retail Stores |

| Online Retail Stores | |

| Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Latin America jewelry market in 2026?

The market stands at USD 35.11 billion and is projected to reach USD 45.76 billion by 2031.

Which product type is growing fastest?

Bracelets lead, forecast to post a 6.90% CAGR through 2031 thanks to the popularity of stackable designs.

Why is Argentina the fastest-growing country?

Macroeconomic stabilization and mining-driven wealth effects support a 6.62% CAGR between 2026 and 2031.