Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

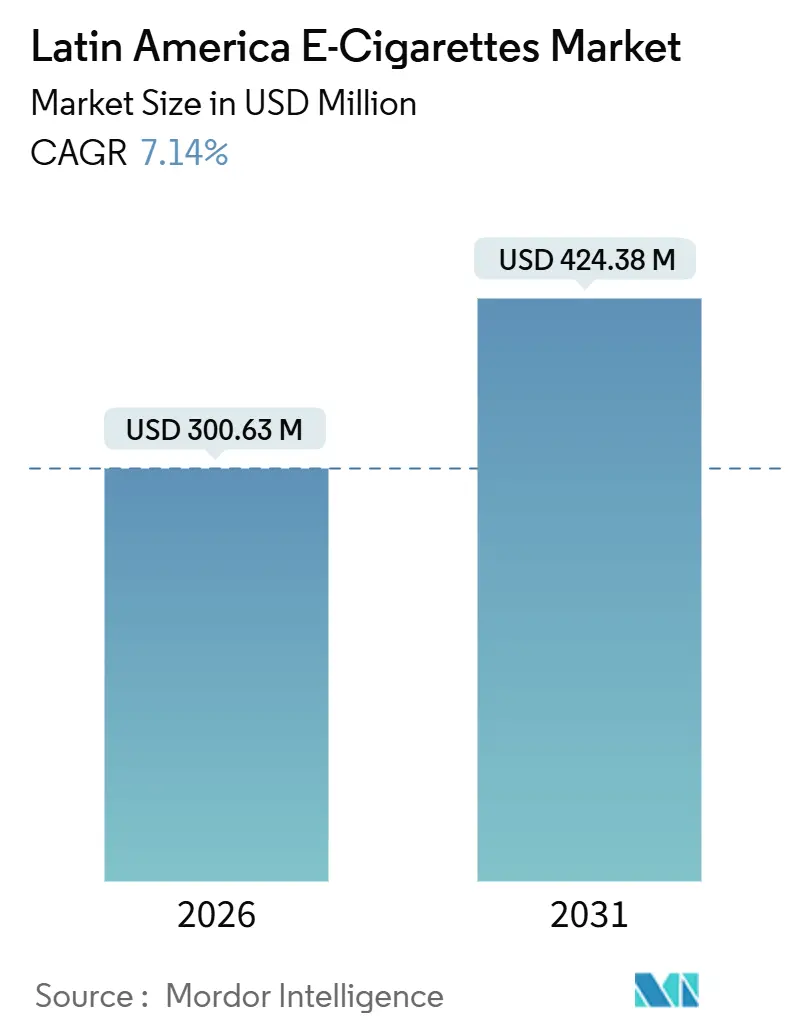

| Market Size (2026) | USD 300.63 Million |

| Market Size (2031) | USD 424.38 Million |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America E-Cigarettes Market Analysis by Mordor Intelligence

The Latin America E-Cigarettes market was valued at USD 300.63 million in 2026, is advancing at a 7.14% CAGR, and is projected to touch USD 424.38 million by 2031. This growth is driven by three interlinked forces: a resilient consumer demand that thrives even amidst bans, a burgeoning gray supply chain that sidesteps formal channels, and cross-border e-commerce networks swiftly transporting goods from Shenzhen and Miami to São Paulo and Mexico City. While disposable pod systems lead initial purchases, it's the refillable devices and e-liquids that are witnessing a quicker unit growth, as budget-savvy repeat users seek lower per-milliliter costs. Major tobacco multinationals wield their capital and lobbying power to influence policy, whereas nimble Chinese OEMs swiftly capitalize on retail gaps, introducing re-branded devices that gain traction through social media buzz. The landscape is further complicated by regulatory disparities: with eight outright bans, thirteen partial regulations, and fourteen regimes with minimal oversight, legal arbitrage emerges, allowing the Latin America E-Cigarettes market to maintain a steady mid-single-digit expansion amidst headline fluctuations.

Key Report Takeaways

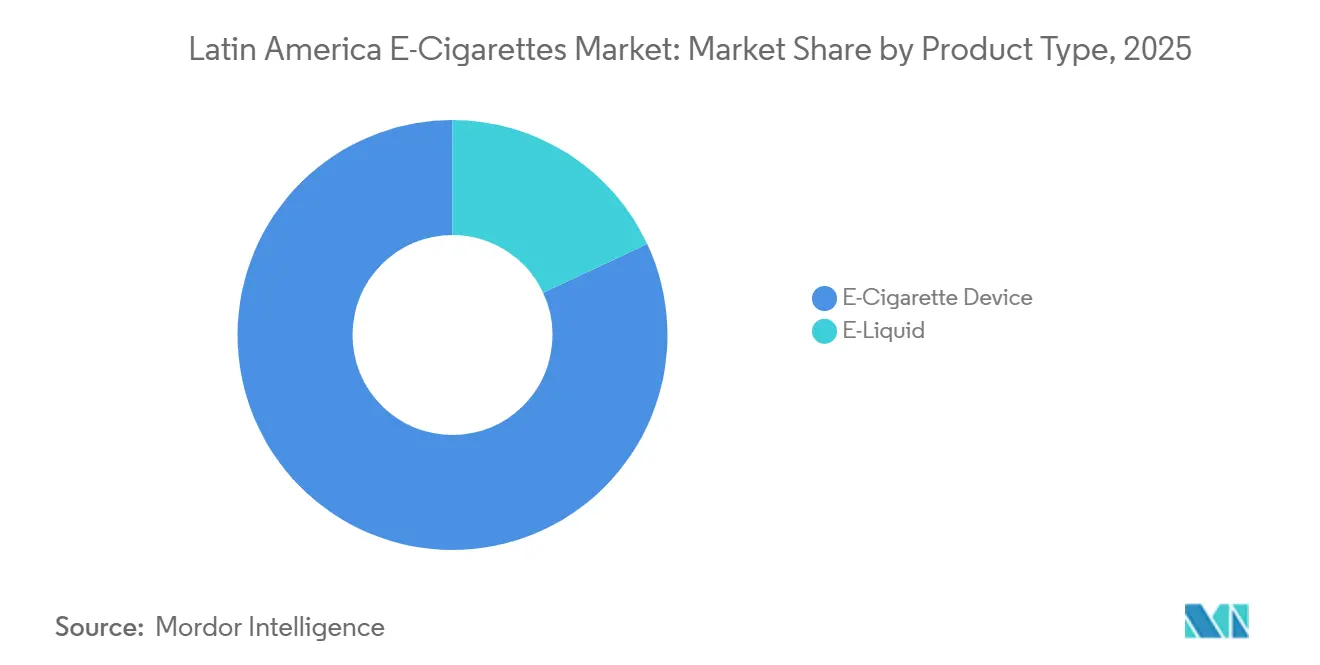

- By product type, E-Cigarette devices held 81.96% of the Latin America E-Cigarettes market share in 2025, while e-liquids are set to grow at a 7.80% CAGR through 2031.

- By category, closed vaping systems commanded 76.74% revenue share of the Latin America E-Cigarettes market in 2025; open systems posted the fastest trajectory at an 8.03% CAGR to 2031.

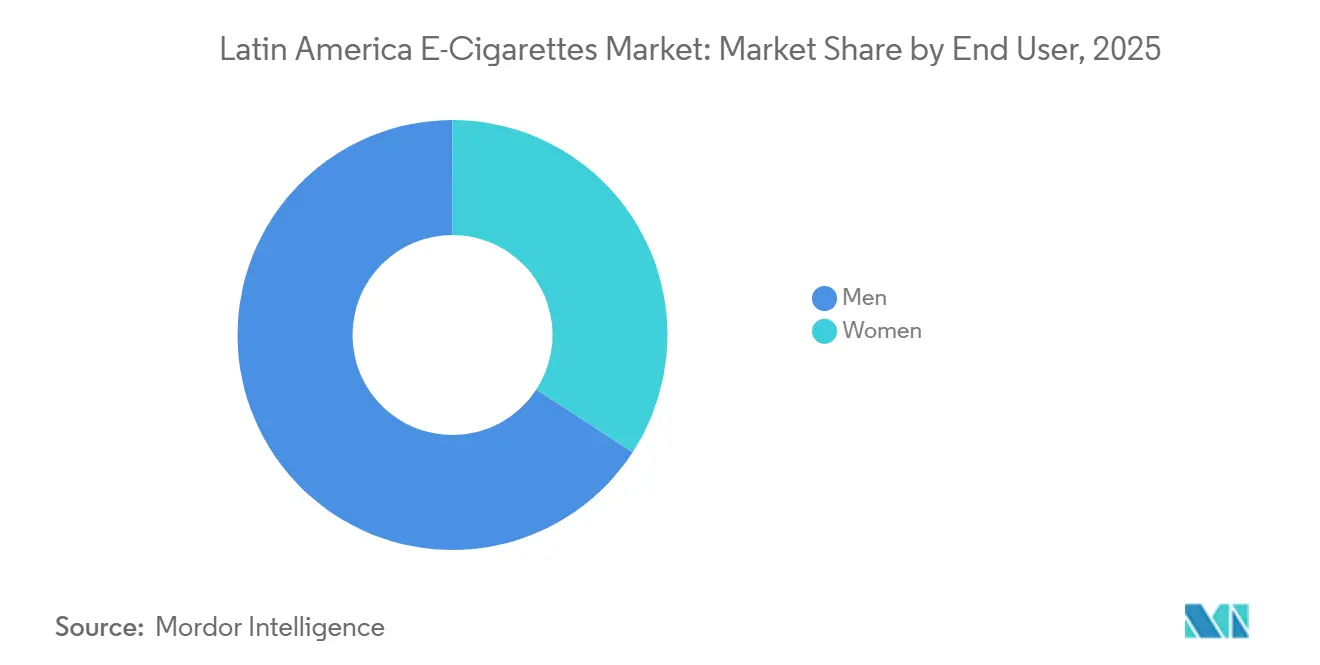

- By end user, men led the Latin America E-Cigarettes market with a 65.82% share in 2025, whereas women represented the highest growth cohort at an 8.78% CAGR from 2025 to 2031.

- By distribution channel, offline retail captured 69.57% share in 2025, but online retail is advancing at a 9.36% CAGR on the back of cross-border logistics innovations.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Latin America E-Cigarettes Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of disposable pod-based devices among Brazilian youth | +1.2% | Brazil, Mexico (the largest markets with ban-evasion dynamics) | Short term (≤2 years) |

| Expansion of cross-border e-commerce logistics reduces price barriers | +0.8% | Regional (54.6% of LatAm shoppers buy from overseas; customs clearance averaging 109 hours) | Short term (≤2 years) |

| Regulatory gray zones allowing nicotine-salt pods to bypass import duties in Mexico | +0.6% | Mexico-specific (Presidential decree enforcement gaps) | Short term (≤2 years) |

| Growing preference for low-nicotine formulations among health-conscious adults | +0.3% | Regional, concentrated in urban centers with higher health literacy | Medium term (2-4 years) |

| Strategic investment by tobacco majors in Latin American vape retail chains | +0.7% | Regional, indirect via advocacy funding (PMI's Foundation for a Smoke-Free World >USD 400M over 7 years) | Medium term (2-4 years) |

| Rise of CBD-infused e-liquids targeting the wellness segment | +0.2% | Regional, nascent adoption in Chile, Colombia, where cannabis frameworks exist | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of disposable pod-based devices among Brazilian youth

In Brazil's illicit vaping market, disposable pod systems reign supreme. Their pre-filled, single-use design sidesteps technical hurdles, making them more accessible to first-time users. Meanwhile, social media, especially Instagram, has become a hotbed for peer-to-peer sales, deftly dodging ANVISA's retail oversight. In Latin America, adolescent ENDS usage hovered around 18.9%. Notably, Brazil saw a rise in self-reported vapers in 2023, despite existing bans[1]Source: Campaign for Tobacco-Free Kids, “Brazil: E-Cigarette Seizures and Usage Trends,” tobaccofreekids.org. The compact design and enticing flavors, mango, strawberry, and mint, of these devices resonate with the youth. Many view vaping as a lesser evil compared to traditional cigarettes, a sentiment bolstered by influencer marketing, which remains a challenge for regulatory bodies to monitor. While seizures of these devices jumped from 21,000 units to a staggering 1.37 million, this figure still pales in comparison to the total imports. Customs officials grapple with the sheer volume of small parcels, especially given the de minimis thresholds: USD 50 for postal shipments and an astonishing USD 0 for couriers. This regulatory gap has paved the way for gray-market distributors, allowing them to cultivate brand loyalty ahead of any potential formal market entry, should the bans be lifted.

Expansion of cross-border e-commerce logistics reducing price barriers

In Latin America, cross-border e-commerce has evolved from a niche market to a dominant force, with most shoppers now buying from international vendors. This shift is largely due to Peru and Uruguay streamlining their export processes, easing customs hurdles for smaller shipments. Panama has solidified its status as a regional hub, capitalizing on its Free Trade Zones, a dollar-based economy, and its prime location. This allows distributors to gather shipments and send them throughout South America. However, it's worth noting that Panama's air cargo facilities lag behind Miami, which serves as a key gateway for northern shipments. Collaborations with giants like Alibaba and Amazon, alongside postal upgrades highlighted in ECLAC's 2023 report, have sped up clearance times[2]Source: ECLAC, “Digital Trade and Logistics in Latin America,” cepal.org. They've also broadened delivery access to gated communities and busy urban areas, challenging traditional retail. This efficiency has significant implications for the vaping industry. For instance, a disposable pod priced at USD 8 in Miami can reach São Paulo for USD 12-15 after shipping and unofficial import charges. This pricing undercuts potential legal retail prices by 30-40%, making enforcement efforts seem economically unviable.

Regulatory gray zones allowing nicotine-salt pods to bypass import duties in Mexico

In May 2022, Mexico's President issued a decree banning e-cigarette sales. However, enforcement was delegated to COFEPRIS. This agency, with its limited inspection capabilities and unclear import classification rules, has inadvertently created loopholes. For instance, nicotine-salt pods are often shipped under the guise of "aromatherapy devices" or "electronic accessories." A study conducted in 2024 revealed that 54.1% of Mexican vapers continued purchasing products even after the ban. Notably, 28.7% of these purchases were made online, utilizing platforms that cleverly routed shipments through fulfillment centers in Texas or California, effectively masking their origin. Nicotine salts, which are modified with benzoic acid, offer higher nicotine concentrations while minimizing throat irritation. This makes them particularly attractive to former smokers in search of quick satisfaction. Yet, Mexico's customs tariff schedule doesn't have a specific Harmonized System code for these nicotine salts. As a result, they're categorized under general "electronic goods," which come with lower duty rates. This classification loophole continues because updating tariff schedules demands coordination between ministries, a process that often lags behind the rapid pace of product innovations. Furthermore, customs officers are at a disadvantage, lacking chemical testing kits to differentiate between nicotine-salt e-liquids and their nicotine-free counterparts upon entry. This gray area is expected to endure until Mexico implements track-and-trace systems. Such systems are akin to Chile's Supreme Decree No. 41, set for September 2024, which enforces health warnings and batch-level serialization.

Growing preference for low-nicotine formulations among health-conscious adults

In urban centers of Latin America, where health literacy is higher and wellness trends are more accessible, a subset of vapers is turning to low-nicotine formulations (3-6 mg/mL). This move is seen as a step towards harm reduction, bridging the gap between quitting smoking and achieving complete nicotine independence. Notably, this demographic aligns with the expanding female end-user category, which is projected to grow at a CAGR of 8.78% through 2031. This growth is fueled by messaging that positions vaping as a controlled-dose alternative, rather than merely a recreational activity. Since 2008, Philip Morris International has poured over USD 14 billion into smoke-free products, delving into research on reduced-risk formulations. However, it's worth noting that their VEEV e-vapor portfolio is predominantly absent from the Latin American landscape. The shift towards lower nicotine levels underscores a significant demographic evolution: the initial wave of vapers, mainly young males drawn by flavor diversity, is now maturing. In their place, a new wave of older, health-conscious individuals is entering the market, bringing distinct priorities. Meanwhile, in Chile and Colombia, e-cigarettes face the same restrictions as tobacco, though they're not outright banned. This regulatory stance allows manufacturers to differentiate products based on nicotine strength, a tactic not available in markets with stringent bans on all variants.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imminent comprehensive vaping ban discussions in Brazil's Congress | -1.5% | Brazil-specific (largest market; spillover effects to Mercosur partners) | Medium term (2-4 years) |

| Counterfeit cartridge proliferation is eroding consumer confidence | -0.9% | Regional, concentrated in Brazil and Mexico, where illicit channels dominate | Short term (≤2 years) |

| Supply-chain disruptions from stricter lithium-battery shipping rules | -0.7% | Global with regional impact; affects air cargo routes from China to Latin America | Short term (≤2 years) |

| Price inflation driven by peso volatility in Argentina | -0.5% | Argentina-specific (nominal prices rose 19.7% annually 2004-2014; real prices fell 0.6%) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Imminent comprehensive vaping ban discussions in Brazil's congress

Brazil's Congress is moving to solidify ANVISA's administrative ban (RDC 855/2024, issued April 2024) into federal law. This effort aims to close existing loopholes that permit judicial challenges and establish a cohesive enforcement framework for state and municipal authorities. While ANVISA's current prohibition bars the manufacture, import, sale, and advertising of e-cigarettes, the lack of criminal penalties for possession means enforcement hinges on product seizures rather than deterring users. A federal ban is poised to introduce criminal penalties for commercial distribution. This move would align Brazil with its neighbors: Venezuela, which in August 2023, banned the manufacture and import of e-cigarettes, and Argentina, which prohibited heated-tobacco products in March 2023. Such alignment could also spark reciprocal actions among Mercosur partners, aiming for a unified approach to tobacco regulations. The economic implications are significant. Brazil stands as the largest market for combustible cigarettes in Latin America, especially for giants like Philip Morris International and British American Tobacco. A formal vaping ban would eliminate any chance of a shift to legal vapor channels, pushing these companies to depend solely on heat-not-burn products, which face less regulatory scrutiny. Furthermore, these ban discussions hint at a broader public health ideology in Brazil, one that leans towards abstinence-only policies over harm-reduction strategies. This stance, while echoed by WHO's Framework Convention on Tobacco Control, stands in contrast to more pragmatic approaches seen in the UK and New Zealand.

Counterfeit cartridge proliferation eroding consumer confidence

Across Latin America's gray market, counterfeit e-liquid cartridges, often filled with substandard nicotine formulations, undisclosed additives, or mislabeled, have surged in prevalence. INTERPOL's Operation Trigger IX, conducted between August and September 2024, seized over 11 million illicit tobacco and vaping products in South America[3]Source: INTERPOL, “Operation Trigger IX,” interpol.int . These counterfeits undermine consumer trust. Users often can't differentiate between genuine and fake products until they experience adverse health effects, such as throat irritation, nausea, or device malfunctions. This leads to a broader negative perception of vaping, rather than a targeted distrust of specific unregulated suppliers. The issue is particularly pronounced in Brazil and Mexico. Here, total bans on vaping products have wiped out legitimate retail channels. As a result, consumers find themselves reliant on social media sellers and cross-border platforms, both of which lack stringent quality-control measures. According to the World Bank, illicit cigarettes in the region are typically priced 50-67% lower than their legal counterparts. This significant price gap is mirrored in counterfeit vape cartridges, making them an economically tempting choice despite the associated quality risks. While track-and-trace systems present a potential solution, Ecuador rolled out a Protocol-compliant system in 2017, Mexico introduced a fiscal mark the same year, and Chile is in the process of adopting a national system; their success hinges on enforcement capabilities, which remain lacking in many areas.

Segment Analysis

By Product Type: Devices Anchor Revenue, Liquids Drive Repeat Engagement

In 2025, E-Cigarette Devices captured 81.96% of the market, driven by disposable pod systems that combine devices and e-liquids into a single SKU. E-Liquids, holding 18.04% of the share, are forecast to grow at a 7.80% CAGR through 2031, outpacing the market's 7.14% growth as users shift to refillable systems with lower per-milliliter costs. Disposable devices dominate sales due to their ease of use, particularly in markets like Brazil and Mexico, where sales bans prevent retail staff from offering product education. Non-disposable devices, such as rechargeable pod systems and advanced vaporizers, attract enthusiasts seeking customization and cost savings but face adoption challenges due to limited retail trial opportunities. As rechargeable devices grow, the device-to-liquid revenue ratio will narrow, with recurring e-liquid purchases driving higher customer lifetime value. Mature markets like the UK show similar trends, where e-liquid sales now surpass device sales. In Chile, regulations (Supreme Decree No. 41, September 2024) mandating health warnings on packaging increase compliance costs, favoring larger manufacturers.

Nicotine-salt formulations (20-50 mg/mL) dominate disposable pods, offering satisfaction similar to cigarettes with reduced harshness. In Mexico, ambiguous import tariff classifications allow gray-market distributors to bypass nicotine-specific duties by labeling shipments as "aromatherapy devices." The integration of devices and liquids in disposables complicates segmentation analysis, as a USD 10 pod typically allocates USD 8 to the device and USD 2 to the liquid, though manufacturers report revenue as a single unit. This bundling obscures e-liquid consumption growth, likely exceeding the reported 7.80% CAGR when refillable systems are included. The segment's trajectory depends on whether regulators classify disposables as devices (subject to electronics waste directives) or consumables (subject to excise taxes), shaping manufacturer strategies in the coming years.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Category: Closed Systems Dominate, Open Systems Gain Among Cost-Conscious Users

In 2025, Closed Vaping Systems held 76.74% of the market share, driven by their plug-and-play design and consistent nicotine delivery through controlled e-liquid formulations. Open Vaping Systems, with a 23.26% share, are projected to grow at an 8.03% CAGR through 2031, as users seek lower costs, refillable tanks cut e-liquid expenses by 40-60% compared to proprietary pods, and greater flavor variety. Closed systems appeal to ex-smokers for their simplicity, using pre-filled pods that avoid handling e-liquids or adjusting coils. However, their proprietary nature locks users into single-brand ecosystems, a strategy led by JUUL Labs in the US but resisted in price-sensitive Latin American markets, allowing bulk e-liquid purchases and coil replacements, lower ownership costs, but requiring technical knowledge, attracting male, tech-savvy users.

Regulatory dynamics also influence the market. Closed systems' tamper-resistant pods reduce contamination risks but limit content verification, complicating counterfeit detection. Open systems offer transparency but expose users to untested third-party liquids. British American Tobacco's FY2024 report noted declining vapor revenue in the Americas, Middle East, and Africa, citing Mexico's Vuse ban (a closed-system product) and illicit vape competition. Regulatory hostility toward closed systems often boosts open-system adoption via gray markets. The category's future depends on whether Latin American regulators adopt Europe's Tobacco Products Directive, capping nicotine at 20 mg/mL and requiring child-resistant packaging, or impose outright bans, nullifying the open-versus-closed distinction.

By End User: Men Lead, Women Accelerate Through Wellness Positioning

In 2025, men accounted for 65.82% of end-users, highlighting vaping's origins in male-dominated enthusiast communities focused on device modification and cloud production. Women, comprising 34.18% of the user base, are projected to grow at an 8.78% CAGR through 2031, the fastest among all segments. This growth is driven by marketing that repositions vaping as a harm-reduction and wellness tool. Globally, the gender gap persists, with UK data showing a 60:40 male-to-female vaper ratio, but it is more pronounced in Latin America, where cultural norms heavily stigmatize female smoking. Women's adoption is accelerating as manufacturers introduce sleeker, pocket-sized devices, such as JUUL's pen-style and RELX's minimalist designs, and as flavor profiles shift from tobacco and menthol to fruit and dessert variants, which female focus groups favor.

Wellness-focused messaging emphasizing controlled nicotine intake, reduced tar exposure, and cessation pathways appeals to health-conscious women. Philip Morris International, having invested over USD 14 billion in smoke-free products since 2008, found that women prioritize discretion and odor reduction over vapor volume, shaping product designs for socially sensitive markets. However, economic constraints also contribute to the gender gap: Women in Latin America earn less than men, making the cost of rechargeable devices and pods a significant barrier. Growth in this segment depends on manufacturers introducing affordable starter kits and subscription models, strategies proven effective in Southeast Asia. Regulatory measures, such as Colombia's May 2024 law mandating plain packaging and gender-neutral marketing for e-cigarettes, may unintentionally slow women's adoption by removing visual cues, like pastel colors and slim designs, that differentiate vaping from traditional cigarettes.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Offline Retail Anchors Access, Online Channels Exploit Enforcement Gaps

In 2025, Offline Retail, including convenience stores, tobacconists, and specialty vape shops, held 69.57% of the market share, driven by consumers' preference for tactile product evaluation and immediate fulfillment. Online Retail, with a 30.43% share, is projected to grow at a 9.36% CAGR through 2031, fueled by Instagram peer-to-peer sales in Brazil and cross-border platforms bypassing local bans via Miami or Panama. Offline Retail benefits from in-person experiences like handling devices and sampling flavors (where legal) but faces challenges in ban-heavy markets where enforcement targets physical stores. For example, despite Mexico's 2022 e-cigarette sales ban, a 2024 study found 28.7% of users purchased online, highlighting digital channels' ability to meet unmet demand. Online platforms exploit enforcement gaps through pseudonymous sellers, mislabeled products, and limited moderation on peer-to-peer marketplaces like Mercado Libre and OLX.

Logistical differences also shape the channel split: offline retail requires distributor networks, licenses, and tax compliance, while online retail leverages postal systems and de minimis thresholds to avoid customs scrutiny. This disparity disadvantages legitimate retailers, pushing markets toward digital channels. ECLAC's 2023 report emphasizes postal modernization and partnerships with platforms like Alibaba and Amazon, which inadvertently facilitate vaping product distribution. The channel's future depends on government enforcement of age-verification, as seen in Chile's Bill 12626-11 (October 2023), and whether payment processors like Visa and PayPal restrict vaping transactions, a strategy effective in curbing online gambling but resisted by e-commerce platforms reliant on transaction fees.

Geography Analysis

Brazil and Mexico are projected to account for 55-60% of Latin America's e-cigarette market volume in 2025, despite sales bans in both countries. This highlights the dominance of illicit channels. Brazil's self-reported vapers rose from 499,000 in 2018 to 2.87 million in 2023, with ANVISA seizures increasing from 21,000 to 1.37 million units annually. However, these figures likely undercount consumption by 30-50% due to undetected social media sales and cross-border shipments. In Mexico, a 2024 study found 54.1% of users purchased e-cigarettes post-ban, with 28.7% buying online via U.S.-based fulfillment centers. These bans limit formal market growth, but gray-market demand drives a 7.14% CAGR through 2031. Argentina, the third-largest market, faces challenges from peso volatility, with the Consumer Price Index for Alcoholic Beverages, Tobacco, and Narcotics rising from 1,977.1 in October to 2,209.6 in November 2023, deterring retail investments.

Chile and Colombia are the region's most promising legal markets, with regulatory frameworks imposing tobacco-equivalent restrictions. Chile's Bill 12626-11 (October 2023) and Supreme Decree No. 41 (September 2024) established licensing, advertising limits, and health warnings. Colombia's May 2024 law aligned e-cigarette regulations with combustible tobacco, allowing licensed retail sales. Philip Morris International reported heat-not-burn gains in Bogota during Q3 2025, showing that regulatory clarity supports brand investment. Smaller markets like Peru, Ecuador, and Uruguay have partial frameworks. Peru's export regime (up to USD 7,500 or 30 kg) supports cross-border e-commerce, while Ecuador's 2017 track-and-trace system for tobacco could extend to e-cigarettes. Venezuela's August 2023 ban on manufacturing and imports eliminates it as a formal market, though cross-border flows from Colombia persist.

The region's growth depends on Brazil's Congress formalizing ANVISA's ban into federal law, which could influence Mercosur partners and hinder legalization. Conversely, Chile's regulatory model, if successful, could inspire balanced policies elsewhere. Urban centers like São Paulo, Mexico City, Buenos Aires, Santiago, and Bogota dominate consumption due to higher incomes, global trend exposure, and dense retail networks. Rural areas remain underserved, with infrastructure challenges like unreliable postal services and limited broadband hindering online retail. Until harmonized policies emerge, the market will remain divided: ban-heavy countries growing via illicit channels and regulatory-framework countries expanding through formal retail.

Competitive Landscape

In the Latin America e-cigarette market, multinational tobacco giants like Philip Morris International, British American Tobacco, Imperial Brands, and RELX Technology lead the heat-not-burn segment, leveraging their regulatory know-how to navigate intricate approval processes. However, these giants face challenges with vapor-specific products, having exited markets due to bans and contending with illicit competition. Meanwhile, Chinese manufacturers such as Smoore International, Shenzhen IVPS, GeekVape, Elf Bar, and RELX Technology provide hardware that gray-market distributors rebrand and sell, allowing these manufacturers to capture volume without the burdens of brand-building or regulatory adherence. Philip Morris International reported a 26.9% year-over-year growth in smoke-free product volumes for Q3 2025, buoyed by the rising market share of IQOS heat-not-burn units in Mexico City and Bogota. Yet, the company's VEEV e-vapor portfolio remains predominantly in Europe and the Middle East, signaling a cautious stance towards the heavily regulated Latin American markets. British American Tobacco's FY2024 results highlighted a dip in vapor revenue across the Americas, Middle East, and Africa, linking the decline to Mexico's Vuse ban and the competition from illicit single-use vapes in North America. This trend underscores the vulnerability of branded players in the face of regulatory challenges. Imperial Brands, with a reported H1 FY2024 net revenue of GBP 538 million from its NGP segment, saw blu vapor contribute GBP 421 million and Pulze heat-not-burn add GBP 117 million. However, the company noted limited activity in Latin America, focusing efforts on Europe and the US where regulatory pathways are clearer.

Strategically, tobacco majors are opting for indirect engagement in markets with stringent bans. Instead of setting up retail chains, they are backing advocacy groups that champion harm-reduction policies. A case in point is Philip Morris International's USD 400 million stake in the Foundation for a Smoke-Free World. This foundation, in turn, allocated over USD 6.4 million to K-A-C, an intermediary bolstering pro-vaping factions in Colombia, Costa Rica, Brazil, Peru, and Panama. Such maneuvers enable these companies to influence regulatory decisions while sidestepping the reputational and legal pitfalls of direct market involvement. In Chile and Colombia, regulatory frameworks allow legal sales, yet major brands haven't cemented their foothold, presenting opportunities for regional distributors and nimble manufacturers adept at navigating compliance.

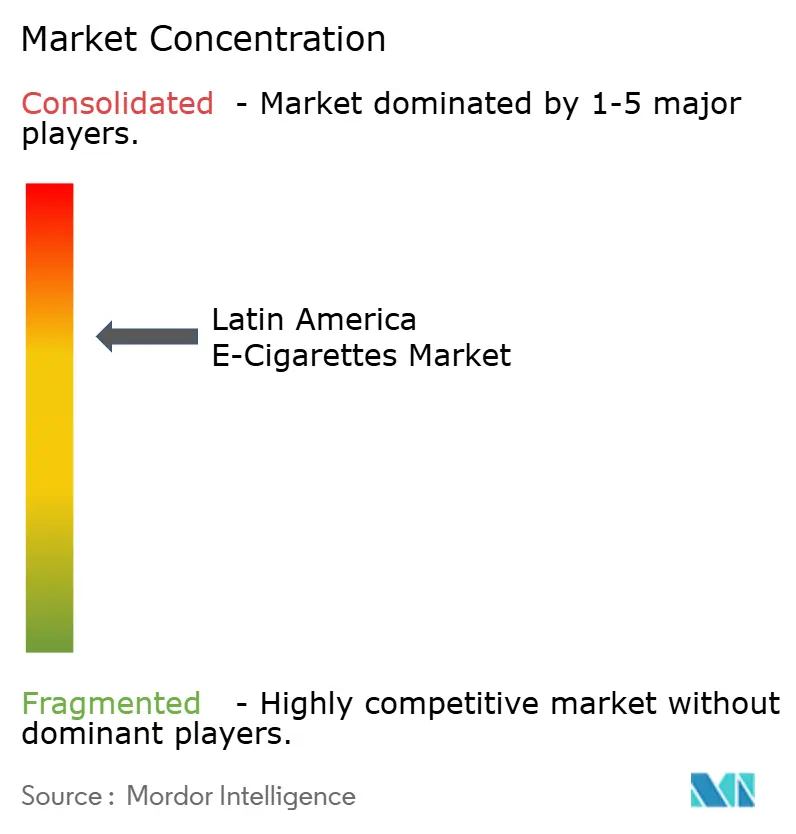

New-age disruptors are emerging, with social-media platforms like Instagram and WhatsApp facilitating peer-to-peer transactions, completely sidestepping traditional retail. This approach allows them to capture margins that established channels, burdened by taxes and licensing fees, can't match. Technology is a key differentiator in this landscape: manufacturers focusing on innovations like mesh-coil technology, enhanced battery efficiency, and leak-resistant designs are winning over repeat customers. However, in markets dominated by counterfeit products, consumers often prioritize price over quality, diminishing the perceived value of these advancements. The competitive arena remains splintered, with no single entity holding more than a 15-20% share. This fragmentation is expected to persist until regulatory harmonization paves the way for brand consolidation, a development not anticipated before 2028-2030 given the current policy disparities across the region.

Latin America E-Cigarettes Industry Leaders

British American Tobacco PLC

Philip Morris Products Inc.

JUUL Labs Inc.

RELX Technology

Imperial Brands PLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Philip Morris International announced its smoke-free products are now available in 100 markets globally, with its VEEV e-vapor portfolio expanding in Europe, the Middle East, and Africa, while Q3 2025 results showed Americas smoke-free product volumes grew 26.9% year-over-year, driven by heat-not-burn unit offtake share gains in Mexico City and Bogota, signaling strategic prioritization of HTU over vapor in Latin America's ban-heavy regulatory environment.

- March 2025: British American Tobacco (BAT) introduced the Vuse Ultra as its latest innovation in the vapor category. The device features a ClearView display for monitoring battery and e-liquid levels, and Bluetooth connectivity for the MyVuse app, allowing users to adjust cloud and flavor settings.

- December 2024: ELFBAR launched BC10000. this device featured two editions: the Sunit Edition (12 mixed fruit flavors) and the Dinmol Edition (11 single fruit flavors). It includes an upgraded design with a real-time power and e-liquid display.

Latin America E-Cigarettes Market Report Scope

An e-cigarette (electronic cigarette) is a battery-powered device that heats a liquid solution, typically containing nicotine, flavorings, and other chemicals. The Latin America e-cigarette market is segmented by product type, category, end user, and distribution channel. By product type, the market is segmented into e-cigarette devices and e-liquids. By category, the market is segmented into open vaping systems and closed vaping systems. By end user, the market is segmented into men and women. By distribution channel, the market is segmented into offline retail and online retail. The Market Forecasts are Provided in Terms of Value (USD).

Product Type

| E-Cigarette Device | Disposable |

| Non-Disposable | |

| E-Liquid |

Category

| Open Vaping Systems |

| Closed Vaping Systems |

End User

| Men |

| Women |

Distribution Channel

| Offline Retail |

| Online Retail |

| Product Type | E-Cigarette Device | Disposable |

| Non-Disposable | ||

| E-Liquid | ||

| Category | Open Vaping Systems | |

| Closed Vaping Systems | ||

| End User | Men | |

| Women | ||

| Distribution Channel | Offline Retail | |

| Online Retail |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Latin America E-Cigarettes market?

The market stood at USD 300.63 million in 2026 and is forecast to hit USD 424.38 million by 2031.

How fast is the sector growing?

It is advancing at a 7.14% CAGR, paced by disposable pod adoption and cross-border e-commerce.

Which product segment is expanding the quickest?

E-liquids are growing at a 7.80% CAGR as refillable systems gain popularity among repeat users.

Why are online channels important?

Online retailers bypass local bans, leverage de minimis import thresholds, and are growing at a 9.36% CAGR.

Which countries permit legal retail sales?

Chile and Colombia allow regulated sales, whereas Brazil, Mexico, and Venezuela enforce comprehensive bans.

Who are the leading companies?

Philip Morris International, British American Tobacco, and Imperial Brands dominate formal channels, while RELX and Elf Bar drive hardware supply through gray networks.