Market Size of Latin America Defense Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

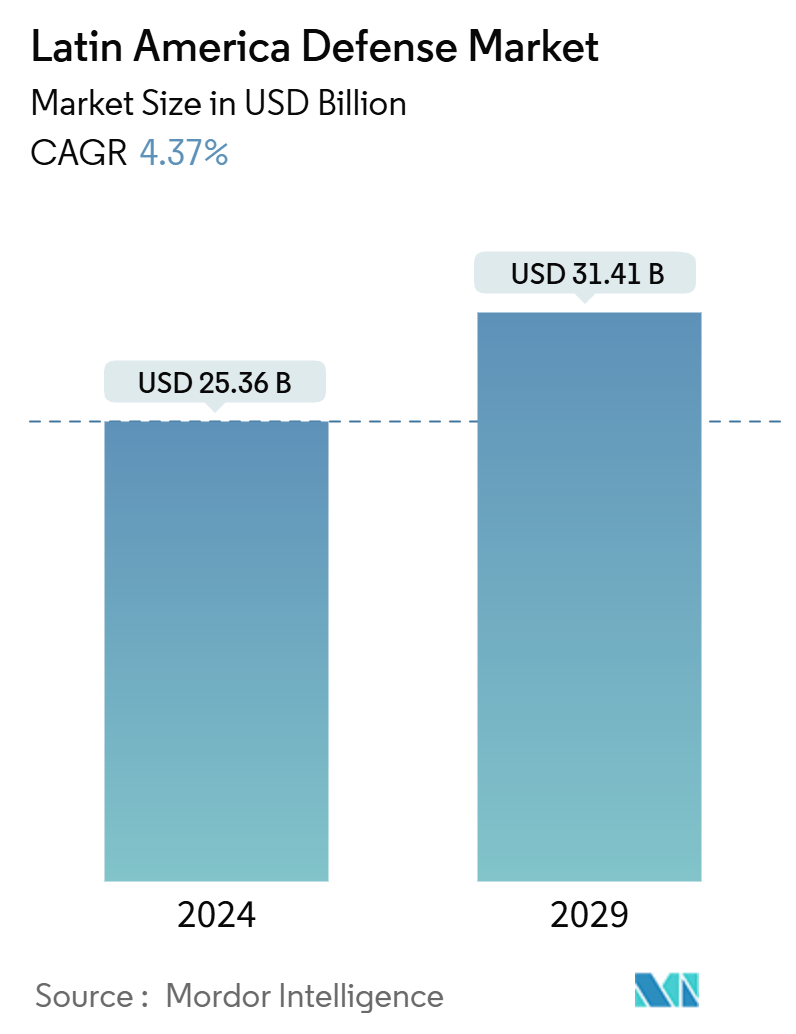

| Market Size (2024) | USD 25.36 Billion |

| Market Size (2029) | USD 31.41 Billion |

| CAGR (2024 - 2029) | 4.37 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Latin America Defense Market Analysis

The Latin America Defense Market size is estimated at USD 25.36 billion in 2024, and is expected to reach USD 31.41 billion by 2029, at a CAGR of 4.37% during the forecast period (2024-2029).

The Latin American defense market is characterized by a mix of established global defense contractors and emerging local firms. This market encompasses various products, including aircraft, naval vessels, armored vehicles, and cybersecurity systems. In 2023, military expenditures reached USD 62.48 billion, and projections indicate steady growth driven by modernization efforts and regional security challenges.

Many Latin American nations are actively modernizing their military capabilities to address both conventional and asymmetrical threats. Notably, Brazil and Colombia are making significant investments to upgrade their air and naval fleets, incorporating advanced technologies such as UAVs and network-centric warfare systems.

Given their extensive maritime borders, countries like Chile and Brazil strongly emphasize naval enhancements. A testament to this is Brazil's PROSUB program (Submarine Development Program), which aims to bolster its submarine fleet. This program includes the notable construction of the nuclear-powered submarine Alvaro Alberto.

Cybersecurity has become a paramount concern as military operations become increasingly digitized. In response, nations are enhancing their cyber defenses through strategic investments and collaborations with global tech firms. Furthermore, integrating AI, machine learning, and data analytics into defense systems is reshaping operational strategies and bolstering advantages in intelligence, surveillance, and reconnaissance (ISR) capabilities.

Latin America Defense Industry Segmentation

The Latin American defense market involves procuring, developing, and deploying military equipment, technologies, and services throughout the region. This market encompasses the sale and production of defense assets, including aircraft, naval vessels, armored vehicles, unmanned systems, and cybersecurity solutions. Furthermore, it covers the R&D of advanced defense technologies and the training, maintenance, and upgrades of military systems. The market strongly emphasizes strategic partnerships, technology transfers, and regional cooperation with international allies. Influenced by regional security needs, geopolitical dynamics, and economic conditions, the market is pivotal in shaping defense spending and policymaking across Latin America.

The Latin American defense market is segmented by end-user, type, and geography. By end-users, the market is segmented into army, navy, air force, law enforcement, disaster response, and others. The other segments include rescue, coast guard, etc. By type, the market is segmented into armored vehicles, military aircraft and helicopters, naval vessels, ammunition, weapons, radar systems, unmanned systems, protective equipment, and others. The report provides market sizes and forecasts for the defense market in major Latin American countries. For each segment, the market size is provided in terms of value (USD).

| End-User | |

| Army | |

| Navy | |

| Air Force | |

| Law Enforcement | |

| Disaster Response | |

| Others (Rescue, Coast Guards, etc.) |

| Type | |

| Armoured Vehicles | |

| Military Aircraft and Helicopters | |

| Naval Vessels | |

| Ammunition | |

| Weapons | |

| Radar Systems | |

| Unmanned Systems | |

| Protective Equipment | |

| Others |

| Country | |

| Brazil | |

| Mexico | |

| Chile | |

| Argentina | |

| Colombia | |

| Rest of Latin America |

Latin America Defense Market Size Summary

The Latin America defense market is experiencing a period of growth, driven by the need for military modernization and the enhancement of defense capabilities. Despite economic challenges, countries in the region are prioritizing the upgrade of military equipment to address geopolitical tensions, border disputes, and issues related to illegal trafficking. The push for modernization is further fueled by rapid technological advancements, prompting nations to innovate to maintain strategic advantages. While domestic suppliers play a significant role in providing missile systems and firearms, Latin American countries heavily rely on imports for advanced equipment such as aircraft, armored vehicles, and submarines, primarily from the United States, Germany, and France. This reliance on imports, coupled with potential supply chain disruptions due to component shortages and price fluctuations, underscores the dynamic nature of the market.

Brazil stands out as a dominant force in the Latin American defense sector, being the largest defense spender in the region. The country is actively enhancing its military capabilities, with significant investments in naval and land forces. Recent initiatives include the procurement of advanced armored vehicles and artillery systems, reflecting Brazil's commitment to modernizing its defense infrastructure. The market is characterized by a mix of local and international players, with companies like Embraer SA, The Boeing Company, and Northrop Grumman Corporation holding substantial market shares. Despite the strong presence of state-owned enterprises catering to domestic needs, international firms continue to influence the market through strategic partnerships and technology transfers. This fragmented yet competitive landscape presents opportunities for growth, particularly in the areas of ammunition manufacturing and advanced defense technologies.

Latin America Defense Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 End-User

-

2.1.1 Army

-

2.1.2 Navy

-

2.1.3 Air Force

-

2.1.4 Law Enforcement

-

2.1.5 Disaster Response

-

2.1.6 Others (Rescue, Coast Guards, etc.)

-

-

2.2 Type

-

2.2.1 Armoured Vehicles

-

2.2.2 Military Aircraft and Helicopters

-

2.2.3 Naval Vessels

-

2.2.4 Ammunition

-

2.2.5 Weapons

-

2.2.6 Radar Systems

-

2.2.7 Unmanned Systems

-

2.2.8 Protective Equipment

-

2.2.9 Others

-

-

2.3 Country

-

2.3.1 Brazil

-

2.3.2 Mexico

-

2.3.3 Chile

-

2.3.4 Argentina

-

2.3.5 Colombia

-

2.3.6 Rest of Latin America

-

-

Latin America Defense Market Size FAQs

How big is the Latin America Defense Market?

The Latin America Defense Market size is expected to reach USD 25.36 billion in 2024 and grow at a CAGR of 4.37% to reach USD 31.41 billion by 2029.

What is the current Latin America Defense Market size?

In 2024, the Latin America Defense Market size is expected to reach USD 25.36 billion.