Market Size of Latin America Data Center Construction Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

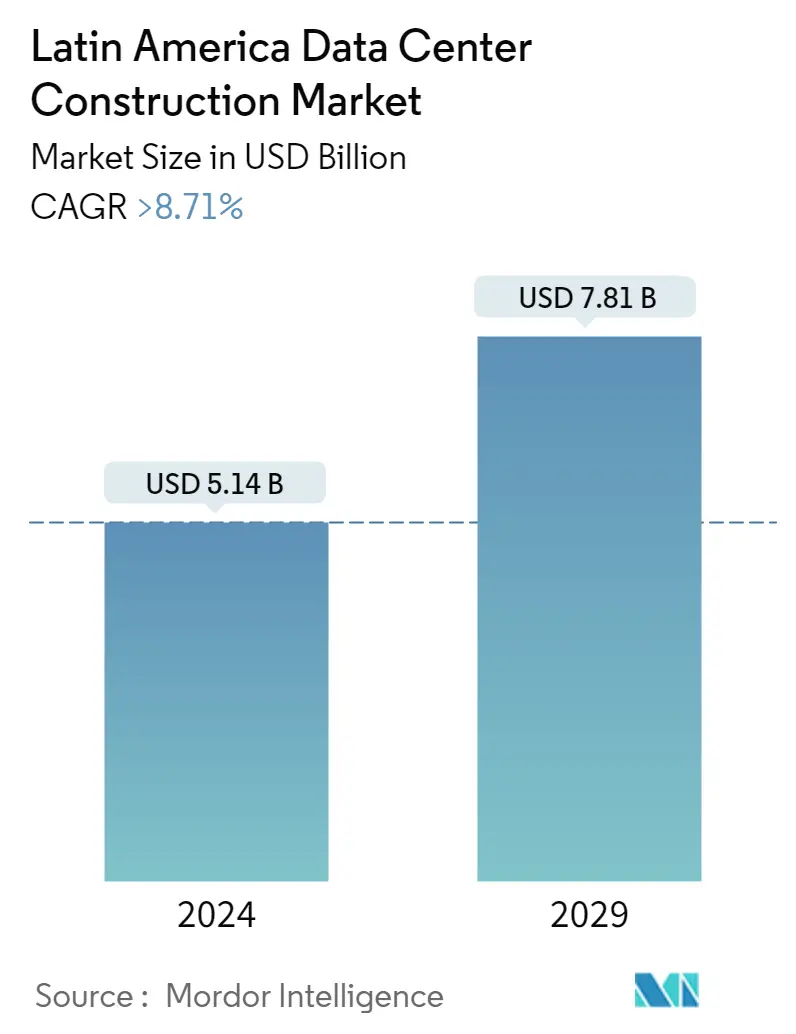

| Market Size (2024) | USD 5.14 Billion |

| Market Size (2029) | USD 7.81 Billion |

| CAGR (2024 - 2029) | 8.71 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Latin America Data Center Construction Market Analysis

The Latin America Data Center Construction Market size is estimated at USD 5.14 billion in 2024, and is expected to reach USD 7.81 billion by 2029, growing at a CAGR of greater than 8.71% during the forecast period (2024-2029).

The growth of advanced technologies such as software-defined data centers, the Internet of Things (IoT), and disaster recovery fed the demand for the construction of data centers in Latin America.

- Data center construction is a very complex task requiring extensive planning of electrical, location, and mechanical requirements. Moreover, the data centers carry out mission tasks, due to which any imperfection in power management to building design could be catastrophic and could result in increased costs to the companies.

- The need for data centers has increased in recent years, with the growth of digital infrastructure due to the high adoption of cloud services. During that period, the widespread expansion of cloud services was restrained by the limited storage available at the data centers.

- Subsequently, the concept of hyperscale data centers and colocation data centers emerged. The construction of hyperscale data centers and colocations data centers is expected to drive the demand for data center construction in the future.

- The rapid proliferation of mobile devices and high-speed broadband connectivity is attributed to the growth of the data center construction market in the Latin American region. Moreover, the increasing demand for connected devices and the introduction of new technologies, such as IoT, cloud-based services, and big data analytics, are boosting the demand for new facilities in the region.

- In September 2023, Saala Data Centers, one of the leading Latin American platforms of sustainable data centers in the Hyperscale market, announced its role as the exclusive Sustainability Partner at Datacloud USA 2023. The collaboration with Datacloud USA reinforces sustainable initiatives and underscores scala's hyperscale sustainable data center evolution in Latin America

- The increasing investment in building new data centers in Latin American countries, such as Brazil, is expected to drive market growth over the forecast period. Brazilian company AMT (Agência Moderna Tecnologia) selected CenturyLink to meet its growing demand for cloud services as part of business expansion with management systems provider Sankhya for data center services in Rio de Janeiro. The CenturyLink modular data center in Rio de Janeiro provides customers with a processing environment designed to offer high levels of availability, improved quality, and greater access speeds to the rest of the world.

- The investments in data centers and advanced information processing structures have accelerated in Latin America, despite the COVID-19 crisis. Various companies in the market have announced their moves for the construction of data centers.

Latin America Data Center Construction Industry Segmentation

Datacenter construction materially builds a data center facility connecting construction standards data center operational environment needs. The market comprises Tier-1, Tier-2, Tier-3, and Tier-4, which are used in small, medium, and large-scale enterprises.

The Latin America data center construction market is segmented into infrastructure type (electrical infrastructure, mechanical infrastructure, general construction), tier type (tier-I and -II, tier-III, and tier-IV), size of enterprise (small and medium-scale enterprises, large-scale enterprises), end user (BFSI, IT and telecommunications, government and defense, healthcare), and country (Mexico, Brazil, Argentina, Rest of Latin America). The report offers market forecasts and size in value (USD) for all the above segments.

| Infrastructure Type | |||||

| |||||

| |||||

| General Construction |

| Tier Type | |

| Tier-I and II | |

| Tier-III | |

| Tier-IV |

| Size of Enterprise | |

| Small and Medium-scale Enterprise | |

| Large-Scale Enterprise |

| End User | |

| Banking, Financial Services, and Insurance | |

| IT and Telecommunications | |

| Government and Defense | |

| Healthcare | |

| Other End Users |

| Country | |

| Mexico | |

| Brazil | |

| Argentina | |

| Rest of Latin America |

Latin America Data Center Construction Market Size Summary

The Latin America Data Center Construction Market is experiencing significant growth, driven by the increasing demand for advanced technologies such as software-defined data centers, IoT, and disaster recovery solutions. The expansion of digital infrastructure, fueled by the high adoption of cloud services, has necessitated the construction of new data centers. This demand is further amplified by the proliferation of mobile devices and high-speed broadband connectivity, which are essential for supporting the region's growing digital economy. The emergence of hyperscale and colocation data centers is expected to continue driving market growth, as these facilities offer the necessary capacity and flexibility to meet the rising needs of businesses and consumers alike.

Investment in data center construction is on the rise across Latin America, with countries like Brazil leading the charge. The region's market is characterized by a high level of competitive rivalry, with key players such as AECOM, Cisco Systems, and Dell Technologies actively expanding their presence through strategic partnerships and technological innovations. The Brazilian government's initiatives, including the General Data Protection Act, are also playing a crucial role in shaping the market by encouraging the development of local data center infrastructure. As companies increasingly seek to enhance data sovereignty and comply with regulatory requirements, the demand for data centers is expected to grow, supported by the ongoing digital transformation and the need for hybrid multi-cloud ecosystems.

Latin America Data Center Construction Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Growth in Network Connectivity and Increased Adoption of Digital Transformation Related Technologies in the Region

-

1.2.2 Favorable tax Incentive Structure Introduced by Local Governments has Led to the Higher Participation from International Players

-

1.2.3 Ongoing Consolidation Efforts by Major Data Center Construction Companies to Aid their Expansion Activities

-

1.2.4 Growing Awareness on Modular Deployments and Increasing Rack Density

-

-

1.3 Market Challenges (Cost and Infrastructural Concerns)

-

1.3.1 Cost and Infrastructural Concerns Continue to be a Concern

-

1.3.2 Workforce-Related Challenges

-

-

1.4 Market Opportunities

-

1.4.1 Technological Advancements in Power, Cooling & Energy Segments to Drive Construction Activity

-

1.4.2 Growing Demand for Edge Data Center Deployments

-

1.4.3 Brazil & Mexico to Continue their Emergence as the Largest Markets in the Region

-

-

1.5 Impact of COVID-19 on the Data center Construction Industry

-

1.6 Industry Attractiveness -Porter's Five Forces Analysis

-

1.6.1 Bargaining Power of Suppliers

-

1.6.2 Bargaining Power of Consumers

-

1.6.3 Threat of New Entrants

-

1.6.4 Threat of Substitutes

-

1.6.5 Intensity of Competitive Rivalry

-

-

1.7 Technology Snapshot

-

-

2. MARKET SEGMENTATION

-

2.1 Infrastructure Type

-

2.1.1 Electrical Infrastructure

-

2.1.1.1 UPS Systems

-

2.1.1.2 Others Electrical Infrastructure

-

-

2.1.2 Mechanical Infrastructure

-

2.1.2.1 Cooling Systems

-

2.1.2.2 Racks

-

2.1.2.3 Other Mechanical Infrastructure

-

-

2.1.3 General Construction

-

-

2.2 Tier Type

-

2.2.1 Tier-I and II

-

2.2.2 Tier-III

-

2.2.3 Tier-IV

-

-

2.3 Size of Enterprise

-

2.3.1 Small and Medium-scale Enterprise

-

2.3.2 Large-Scale Enterprise

-

-

2.4 End User

-

2.4.1 Banking, Financial Services, and Insurance

-

2.4.2 IT and Telecommunications

-

2.4.3 Government and Defense

-

2.4.4 Healthcare

-

2.4.5 Other End Users

-

-

2.5 Country

-

2.5.1 Mexico

-

2.5.2 Brazil

-

2.5.3 Argentina

-

2.5.4 Rest of Latin America

-

-

Latin America Data Center Construction Market Size FAQs

How big is the Latin America Data Center Construction Market?

The Latin America Data Center Construction Market size is expected to reach USD 5.59 billion in 2025 and grow at a CAGR of greater than 8.71% to reach USD 8.48 billion by 2030.

What is the current Latin America Data Center Construction Market size?

In 2025, the Latin America Data Center Construction Market size is expected to reach USD 5.59 billion.