Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

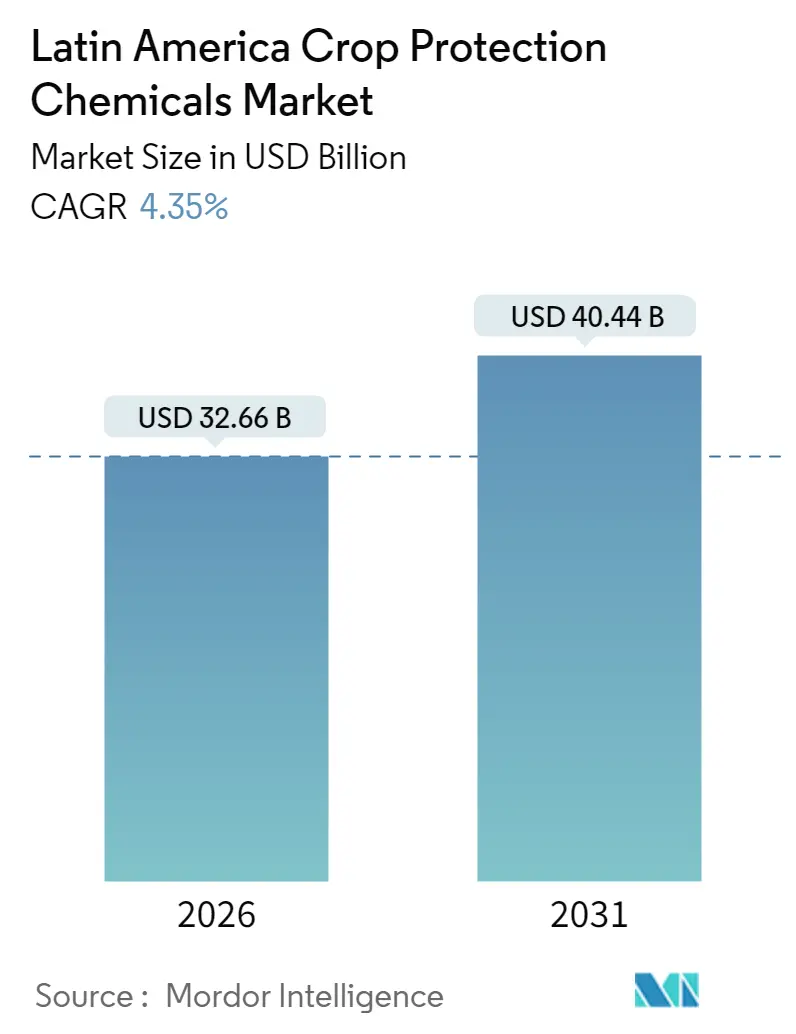

| Market Size (2026) | USD 32.66 Billion |

| Market Size (2031) | USD 40.44 Billion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Crop Protection Chemicals (Pesticides) Market Analysis by Mordor Intelligence

The Latin America crop protection chemicals (Pesticides) market is expected to grow from USD 31.30 billion in 2025 to USD 32.66 billion in 2026 and is forecast to reach USD 40.44 billion by 2031 at 4.35% CAGR over 2026-2031. Steady commodity demand, rising pest pressure, and increasing pest resistance to older chemistries together sustain this momentum. Synthetic herbicides retain volume leadership, yet biological fungicides scale swiftly on export-market residue rules. Multinationals reinforce portfolios with resistance-breaking actives while regional generics compete on price, creating a balanced but dynamic competitive field. Digital prescription spraying, carbon-credit programs, and counterfeit inflows shape both opportunity and risk for suppliers.

Key Report Takeaways

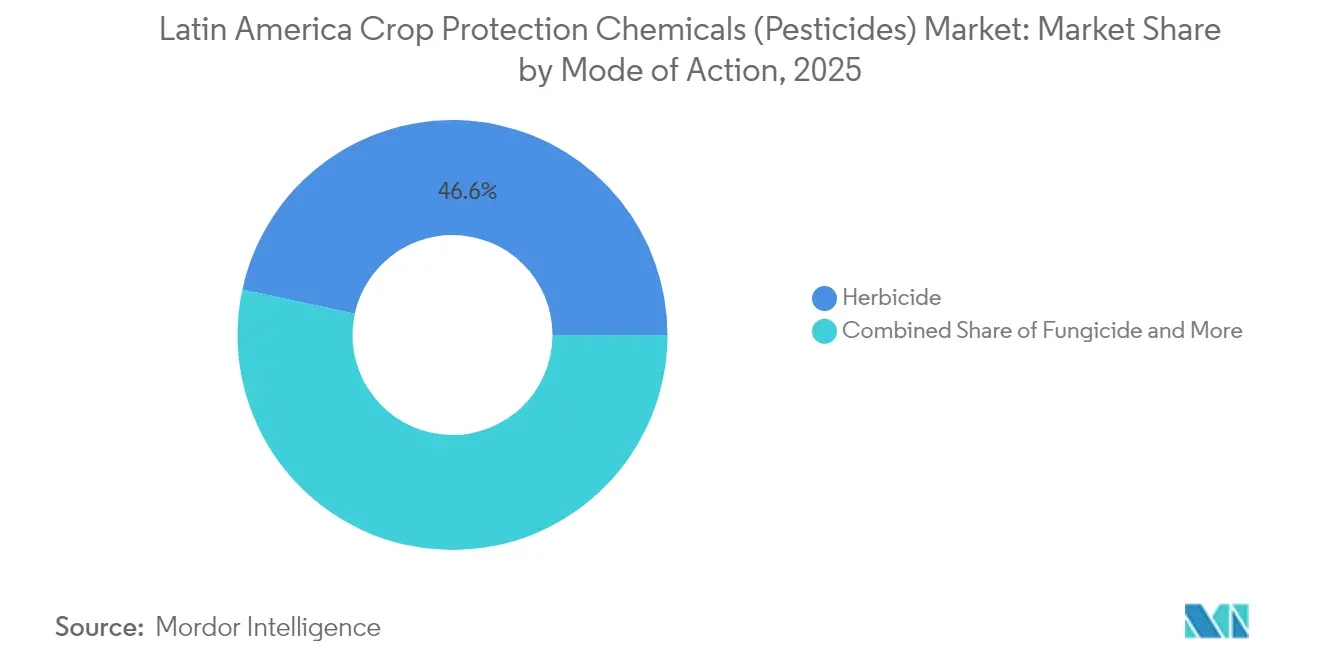

- By mode of action, herbicides led with 46.60% revenue share in 2025, while fungicides are forecast to expand at a 4.95% CAGR to 2031.

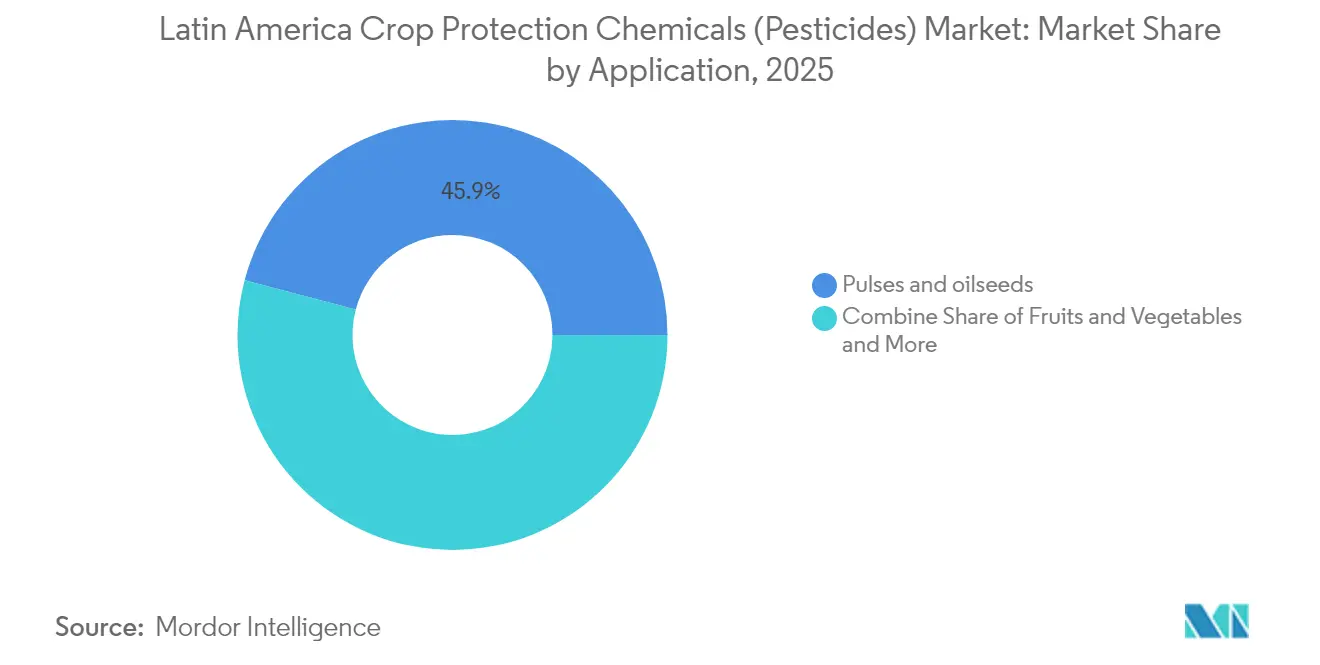

- By application, pulses and oilseeds held 45.90% of the Latin America crop protection chemicals (Pesticides) market share in 2025, and Fruits and vegetables are advancing at 9.55% CAGR through 2026-2031.

- In 2025, Brazil held a dominant 78.10% share of the Latin America crop protection chemicals (Pesticides) market, while Argentina projected a robust growth rate of 4.96% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Latin America Crop Protection Chemicals (Pesticides) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of soybean and corn acreage | +1.2% | Brazil, Argentina, Paraguay, with spillover to Bolivia | Medium term (2-4 years) |

| Increasing pest resistance to older chemistries | +0.9% | Brazil, Argentina, Mexico, Central America | Long term (≥ 4 years) |

| Intensifying pressure from invasive species such as Helicoverpa armigera | +0.7% | Brazil, Argentina, with emerging threats in Colombia, Peru | Short term (≤ 2 years) |

| Growing adoption of stacked-trait Genetically Modified(GM) seeds | +0.8% | Brazil, Argentina, Paraguay, with regulatory approval pending in Colombia | Medium term (2-4 years) |

| Integration of AI-based prescription spraying platforms | +0.5% | Brazil, Argentina, Chile, with pilot programs in Mexico | Long term (≥ 4 years) |

| Carbon-credit programs rewarding yield-boosting inputs | +0.4% | Brazil, Argentina, with early-stage initiatives in Chile, Colombia | GM) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Soybean and Corn Acreage

Brazil added 1.2 million hectares of soybeans in 2024, lifting herbicide demand as glyphosate-tolerant varieties require multiple passes per season[1]Source: USDA Foreign Agricultural Service, “Brazil: Oilseeds and Products Annual,” fas.usda.gov. Argentina’s corn area rebounded, renewing appetite for pre-emergence herbicides. Second-crop corn in Brazil’s Center-West compresses application windows, favoring quick-acting formulations. Acreage growth in Paraguay and Bolivia extends market reach as deforestation-free certification raises input intensity. Together, these trends underpin herbicide volume resilience in the Latin America crop protection chemicals (Pesticides) market.

Increasing Pest Resistance to Older Chemistries

Field research confirmed cyantraniliprole-resistant Fall armyworm in Mato Grosso during 2024, forcing growers into newer diamide options[2]Source: CABI, “Fall Armyworm: Impacts and Implications,” cabi.org. Argentina’s soybean belt battles glyphosate-resistant Palmer amaranth across 30% of area, lifting residual herbicide layering costs by 20% to 25%. Mexico’s vegetable sector reports declining pyrethroid efficacy, accelerating uptake of neonicotinoid seed treatments. Resistance escalates input spending and favors differentiated actives, benefiting innovators in the Latin America crop protection chemicals (Pesticides) market.

Intensifying Pressure from Invasive Species Such as Helicoverpa armigera

Since detection in 2013, Helicoverpa armigera has driven Brazilian cotton growers to double spray counts, now averaging six to eight applications per season. Centre for Agriculture and Bioscience International (CABI) estimates regional Fall armyworm losses could reach USD 4 billion annually without control. Chile’s fruit sector equally faces codling-moth incursions, cementing demand for low-residue insecticides.

Growing Adoption of Stacked-Trait Genetically Modified (GM) Seeds

Intacta 2 Xtend soybeans covered significant area in Brazil in 2024, pairing herbicide tolerance with lepidopteran resistance and driving complementary herbicide use. Argentina’s stacked-trait corn hybrids span 85% of the area, supporting residual herbicide demand. Although Mexico debates GM corn, stacked traits dominate its cotton acreage. Trait adoption differentiates chemical portfolios and sustains herbicide innovation in the Latin America crop protection chemicals (Pesticides) market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent maximum-residue limits in key export markets | -0.6% | Chile, Peru, Mexico, Brazil (fruit and vegetable exporters) | Short term (≤ 2 years) |

| Escalating activist-driven pesticide bans | -0.5% | Mexico, Colombia, Argentina (provincial level), Brazil (municipal level) | Medium term (2-4 years) |

| Tight farm-gate margins amid volatile commodity prices | -0.7% | Brazil, Argentina, Paraguay, with acute pressure in smallholder segments | Short term (≤ 2 years) |

| Cross-border counterfeit product inflows from Asia | -0.4% | Brazil, Argentina, with distribution networks extending to Paraguay, Bolivia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Maximum-Residue Limits in Key Export Markets

EU and North American buyers lowered residue thresholds, compelling Chile’s blueberry sector to swap into biological fungicides despite higher costs. Peru’s avocado exporters saw pre-harvest compliance expenses rise 12% in 2024. Mexico’s berry industry invested in laboratory testing, yet smallholders lag. Export-oriented segments therefore gravitate to premium low-residue products, while domestic growers stay with legacy synthetics, segmenting demand in the Latin America crop protection chemicals (Pesticides) market.

Escalating Activist-Driven Pesticide Bans

Mexico’s 2024 decree restricting glyphosate in tortilla supply chains stimulates glufosinate and 2,4-D promotion. Colombia debates paraquat bans, and Argentine provinces enforce aerial-spray buffer zones, shrinking treatment areas. Municipal curbs within Brazil add compliance complexity. Such patchwork policies raise registration costs and push suppliers toward biological portfolios.

Segment Analysis

By Mode of Action: Herbicides Lead, Fungicides Surge

Herbicides accounted for 46.60% of revenue in 2025, reflecting their foundational role in no-till soybean and corn programs. Regulatory headwinds spur formulators to innovate with lower-volatility dicamba, glufosinate, and novel HPPD inhibitors. Fungicides, although smaller in base, advance at a 4.95% CAGR, outpacing all other categories. Export fruit growers in Chile and Peru deploy Bacillus and botanical blends to satisfy supermarket standards.

Insecticide demand bifurcates, where synthetic pyrethroids taper in vegetables, while diamide classes grow in corn and cotton to combat armyworm. Mode-of-action diversification, therefore, accelerates rotation practices and cushions market value against individual active ingredient bans. Resistance management drives product mix shifts. Growers now rotate triazole, strobilurin, and SDHI fungicides for soybean rust to prolong synthetic efficacy. Suppliers leverage this need with pre-mix packs and tailored stewardship programs, enhancing stickiness within the Latin America crop protection chemicals (pesticides) market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Soybeans Dominate, Horticulture Accelerates

Pulses and oilseeds accounted for 45.90% of the Latin America crop protection chemicals (Pesticides) market share in 2025. Multiple herbicide passes per cycle, plus residual layering, underpin value. Yet fruits and vegetables outpace as export premiums justify intensive protection. Fruits and vegetables, led by berries, avocados, and grapes, are advancing at a 9.55% CAGR during the forecast period. Berry growers in Chile spend over USD 800 per hectare on fungicides and insecticides to maintain shelf life and residue compliance. Grains and cereals absorb high volumes of insecticides to control Fall armyworm, but price sensitivity tempers the value growth. Specialty crops, such as coffee and cocoa, exhibit latent demand for incremental upside for niche suppliers.

Horticulture’s rapid expansion diversifies revenue away from traditional row crops. Suppliers now tailor low-residue and zero-day pre-harvest interval formulations specifically for avocado, mango, and table grape exporters, aligning product pipelines with booming wellness and sustainability trends.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Brazil commands 78.10% of regional demand, supported by double-cropping systems that necessitate near-continuous chemical use. The Latin America crop protection chemicals (Pesticides) market size in Brazil is forecast to rise 4.32% CAGR through 2031 as MATOPIBA expansion and AI-enabled input optimization lift efficiency.

Argentina represents the fastest market with a 4.96% CAGR from 2026 to 2031, but it grapples with volatile macro conditions. Economic strains push growers toward generics, restraining premium adoption. Even so, stacked-trait corn hybrid uptake sustains residual herbicide demand. Provincial spray buffers compel the adoption of seed treatments and inoculants that lower field application frequency. Chile, though smaller in area, posts on the strength of its export horticulture. Its growers invest heavily in microbial fungicides and pheromone-based insect controls to secure EU and Asian shelf space. Government fast-tracking of biological registrations under SAG supports this trajectory. Mexico and Central America show mixed dynamics. Mexico’s glyphosate restrictions skew herbicide portfolios toward glufosinate and mechanical weed control aids. Coffee, bananas, and palm oil dominate Central American demand, where counterfeit inflows challenge regulatory capacity. Caribbean islands remain niche consumers, focusing on high-value vegetables for tourism and export.

Competitive Landscape

Top players hold modest percentage share, denoting moderate concentration. Syngenta leverages breadth across herbicides and fungicides to lead, followed by Bayer, integrating seed and chemistry bundles that lock in customers. BASF’s share pivots on novel fungicide Revysol, now approved for soybeans. Corteva and FMC complete the top tier with insecticide and herbicide innovations to combat resistance.

Regional specialists such as UPL, Nufarm, and ADAMA underprice branded offers by up to 30%, capturing budget-conscious segments. Local Brazilian firms Ihara and Ourofino offer solutions by tailoring formulations for smallholders and investing in R&D. Bioceres’ HB4 trait and associated biologicals broaden competitive dimensions beyond pure chemistry.

Strategic moves underscore integration trends. Syngenta’s Uberlândia plant boosts modern formulations capacity. Bayer’s stake in Elo embeds digital agronomy inside its sales model. BASF’s Revysol registration breaks a six-year fungicide innovation drought, while Corteva’s Enlist E3 soybeans extend multi-herbicide flexibility. FMC’s Campinas insecticide facility lowers supply-chain risk and aligns with sustainability mandates. Partnerships like UPL-Solinftec fuse AI spraying with branded products, signaling a shift toward bundled service ecosystems.

Latin America Crop Protection Chemicals (Pesticides) Industry Leaders

Bayer CropScience AG

Syngenta AG

BASF SE

FMC Corporation

Corteva Agriscience

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2024: FMC Corporation introduced Azugro and Ezanya herbicides for cotton, tobacco, and wheat crops in Brazil. These herbicides contain Isoflex active, FMC's brand name for biozone. Isoflex active, classified as a Group 13 herbicide by the Herbicide Resistance Action Committee (HRAC), represents a novel herbicide formulation for cereal crops.

- April 2024: UPL Brazil has launched Eximia, a selective herbicide for controlling difficult-to-manage weeds in sugarcane crops. The product effectively manages Bermuda grass (Cynodon dactylon) and seashore paspalum (Paspalum maritimum), helping maintain crop productivity and profitability.

- May 2022: ADAMA introduced Cheval® (Glufosinate + S-metolachlor) in Brazil. This dual-action herbicide targets glufosinate-tolerant crops, such as soy. It promises robust weed control, extended residual effects, and serves as a resistance management tool. Priced competitively, 25% lower than some rivals, ADAMA aims to seize market share from the growing herbicide-tolerant (HT) acreage, emphasizing both broad-spectrum burndown and residual weed suppression.

Latin America Crop Protection Chemicals (Pesticides) Market Report Scope

Mode of Action

| Herbicide |

| Fungicide |

| Insecticide |

| Other Modes of Action |

Application

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Commercial Crops |

| Turf and Ornamentals |

Geography

| Brazil |

| Argentina |

| Chile |

| Rest of Latin America |

| Mode of Action | Herbicide |

| Fungicide | |

| Insecticide | |

| Other Modes of Action | |

| Application | Grains and Cereals |

| Pulses and Oilseeds | |

| Fruits and Vegetables | |

| Commercial Crops | |

| Turf and Ornamentals | |

| Geography | Brazil |

| Argentina | |

| Chile | |

| Rest of Latin America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the 2026 value for Latin America crop protection chemicals (Pesticides) ?

Spending totals USD 32.66 billion in 2026 and is projected to reach USD 40.44 billion by 2031.

Which country accounts for the largest share of crop protection demand in the region?

Brazil generates about 78.10% of total spending, driven by expansive soybean and corn acreage.

How do AI-enabled spraying platforms affect pesticide use?

Early adopters in Brazil and Argentina report 15%–20% reductions in herbicide volumes while maintaining control levels.

Which crop segment shows the fastest spending growth through 2031?

Fruits and vegetables, led by berries, avocados, and grapes, are advancing at 9.55% CAGR as exporters meet stricter residue limits.