Market Size of Latin America Cold Chain Logistics Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

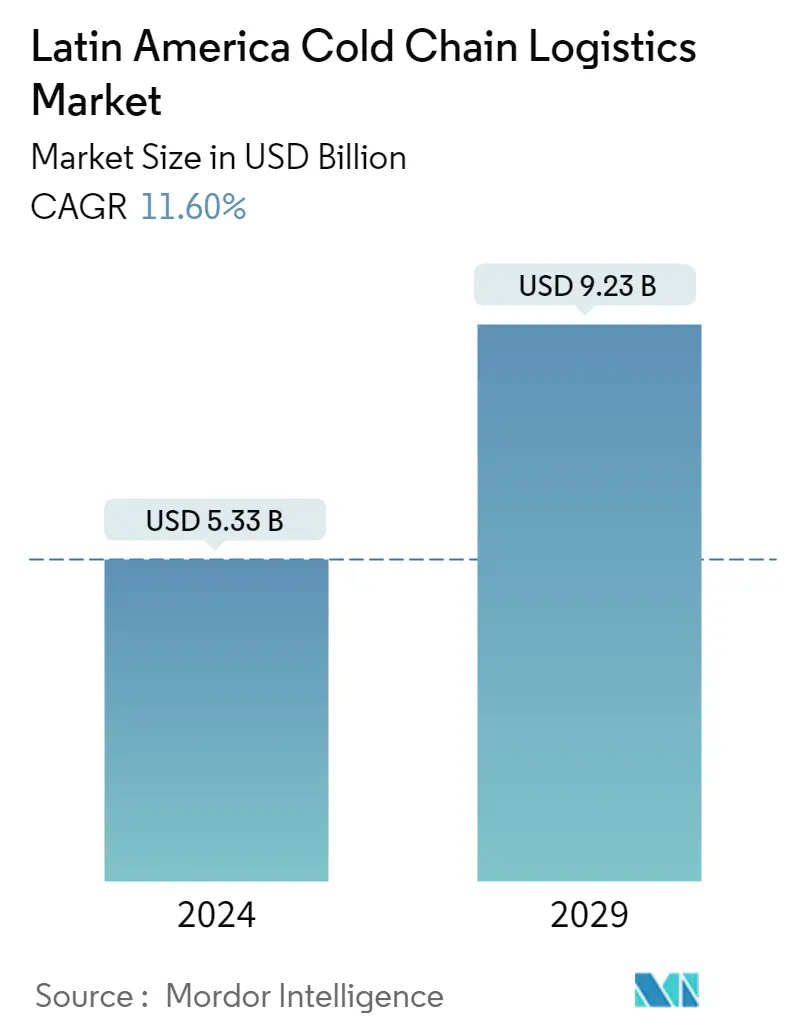

| Market Size (2024) | USD 5.33 Billion |

| Market Size (2029) | USD 9.23 Billion |

| CAGR (2024 - 2029) | 11.60 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Latin America Cold Chain Logistics Market Analysis

The Latin America Cold Chain Logistics Market size is estimated at USD 5.33 billion in 2024, and is expected to reach USD 9.23 billion by 2029, growing at a CAGR of 11.60% during the forecast period (2024-2029).

The characteristics and reality of the Latin American market are highly varied. As a result, businesses from all industries operating in this region must adjust to these conditions to continue doing business. LATAM does not precisely exclude chilled cargo from this obligation due to the difficulties traversing long land expanses between production and marketing hubs. It is crucial to preserve the freshness and quality of the food, medications, and other supplies that must be stored and transported under these conditions by keeping the cold chain at the proper temperatures.

The COVID-19 pandemic initially harmed the cold chain market in Latin America. Still, as the pandemic progressed and more perishable goods were traded internationally, technology advancements in refrigerated transport and storage, government support for infrastructure development, and a surge in MNCs' expansion of food chains, the market for cold chain logistics in LATAM began to grow.

Latin America's perishable food supply chain is still robust, with food traveling to retail establishments. In addition, it is stated that warehouses are operating at total capacity and that a workforce shortage is a problem. These considerations are encouraging the already-established regional players to consolidate and develop technologically to address the region's shortage of refrigerated space.

For instance, in October 2022, Agro-industrial and logistics firm Frigorifico Modelo (Frimosa), based in Montevideo, Uruguay, announced that its cold storage operations would be acquired by Emergent Cold Latin America (Emergent Cold LatAm or the Company), a provider of refrigerated storage and logistics services in Latin America. The main building of Frimosa in Polo Oeste, which includes a warehouse with 22,000 cold storage pallets, a separate bonded warehouse, and a sizable amount of ground for expansion, will be purchased by Emergent Cold LatAm. Additionally, in Asunción, Paraguay, Emergent Cold LatAm will purchase a brand-new 8,400-pallet warehouse.

Latin America Cold Chain Logistics Industry Segmentation

Cold chain logistics combines temperature-controlled transportation with a planned supply chain to preserve products' quality and shelf life, including fresh agricultural produce, seafood, frozen food, and pharmaceutical medications. The research offers a thorough background analysis of the Latin America (LATAM) cold chain logistics market, covering the most recent technology advancements, market trends, in-depth details on significant sectors, and the industry's competitive environment. The study also took into account the effects of COVID-19.

The Latin America Cold Chain Logistics Market is segmented by service (cold storage/refrigerated warehousing, refrigerated transportation, and value-added services), temperature (chilled, frozen and ambient), end-user (fruits and vegetables, dairy products (milk, butter, cheese, ice cream, etc.), fish, meat, and seafood, processed food, pharmaceutical (includes biopharma), bakery and confectionery, and other end-users), and country (Mexico, Brazil, Chile, Colombia, and rest of Latin America). The report offers Market size and forecasts for Latin America Cold Chain Logistics Market in value (USD) for all the above segments.

| By Service | |

| Cold Storage/Refrigerated Warehousing | |

| Refrigerated Transportation | |

| Value-added Services (Order Management, Blast Freezing, Labeling, Inventory Management, etc.) |

| By Temperature | |

| Chilled | |

| Frozen | |

| Ambient |

| By End User | |

| Fruits and Vegetables | |

| Dairy Products (Milk, Butter, Cheese, Ice Cream, etc.) | |

| Fish, Meat, and Seafood | |

| Processed Food | |

| Pharmaceutical (Includes Biopharma) | |

| Bakery and Confectionery | |

| Other End Users |

| By Country | |

| Mexico | |

| Brazil | |

| Chile | |

| Colombia | |

| Rest of Latin America |

Latin America Cold Chain Logistics Market Size Summary

The Latin America cold chain logistics market is experiencing significant growth, driven by the increasing demand for the preservation of perishable goods such as food and pharmaceuticals. The region's diverse market conditions necessitate that businesses adapt their operations to maintain the integrity of the cold chain, ensuring that products remain fresh and of high quality during transportation. The market's expansion is supported by technological advancements in refrigerated transport and storage, as well as government initiatives aimed at infrastructure development. The COVID-19 pandemic initially posed challenges, but it also accelerated the adoption of cold chain solutions as international trade in perishable goods increased. This has led to a robust supply chain for perishable foods, with warehouses operating at full capacity despite workforce shortages, prompting regional players to invest in technological advancements and consolidation efforts.

The demand for cold warehousing and storage is particularly high in Latin America due to the region's substantial perishable food and pharmaceutical industries. Brazil stands out as the largest market, followed by Mexico, Colombia, Chile, and Argentina, with significant contributions from e-commerce and trade volume growth. The market is characterized by a fragmented landscape with both domestic and international players, and it is witnessing mergers and acquisitions as companies seek to enhance their capabilities. The implementation of advanced technologies such as IoT, cloud storage, and electronic data interchange is improving operational efficiency and communication during transportation. Notable developments include strategic partnerships and expansions by key players like Emergent Cold Latin America, which is enhancing its presence in Brazil and other key locations.

Latin America Cold Chain Logistics Market Size - Table of Contents

-

1. MARKET DYNAMICS AND INSIGHTS

-

1.1 Market Overview (Current Scenario of the Cold Chain Logistics Market)

-

1.2 Impact of COVID-19 on the Cold Chain Logistics Market

-

1.3 Government Regulations (Related to Cold Storage and Transport)

-

1.4 Insights into Refrigerants and Packaging Materials

-

1.5 Market Dynamics

-

1.5.1 Drivers

-

1.5.1.1 Growth in E-commerce

-

1.5.1.2 Healthcare Sector is the market

-

-

1.5.2 Restraints

-

1.5.2.1 Supply Chain Disruptions

-

1.5.2.2 Lack of Temperature- Controlled Warehouses

-

-

1.5.3 Opportunities

-

1.5.3.1 Technological Innovations

-

-

-

1.6 Industry Attractiveness - Porter's Five Forces Analysis

-

1.6.1 Bargaining Power of Suppliers

-

1.6.2 Bargaining Power of Consumers

-

1.6.3 Threat of New Entrants

-

1.6.4 Threat of Substitutes

-

1.6.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 By Service

-

2.1.1 Cold Storage/Refrigerated Warehousing

-

2.1.2 Refrigerated Transportation

-

2.1.3 Value-added Services (Order Management, Blast Freezing, Labeling, Inventory Management, etc.)

-

-

2.2 By Temperature

-

2.2.1 Chilled

-

2.2.2 Frozen

-

2.2.3 Ambient

-

-

2.3 By End User

-

2.3.1 Fruits and Vegetables

-

2.3.2 Dairy Products (Milk, Butter, Cheese, Ice Cream, etc.)

-

2.3.3 Fish, Meat, and Seafood

-

2.3.4 Processed Food

-

2.3.5 Pharmaceutical (Includes Biopharma)

-

2.3.6 Bakery and Confectionery

-

2.3.7 Other End Users

-

-

2.4 By Country

-

2.4.1 Mexico

-

2.4.2 Brazil

-

2.4.3 Chile

-

2.4.4 Colombia

-

2.4.5 Rest of Latin America

-

-

Latin America Cold Chain Logistics Market Size FAQs

How big is the Latin America Cold Chain Logistics Market?

The Latin America Cold Chain Logistics Market size is expected to reach USD 5.33 billion in 2024 and grow at a CAGR of 11.60% to reach USD 9.23 billion by 2029.

What is the current Latin America Cold Chain Logistics Market size?

In 2024, the Latin America Cold Chain Logistics Market size is expected to reach USD 5.33 billion.