Market Overview

| Study Period | 2021 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

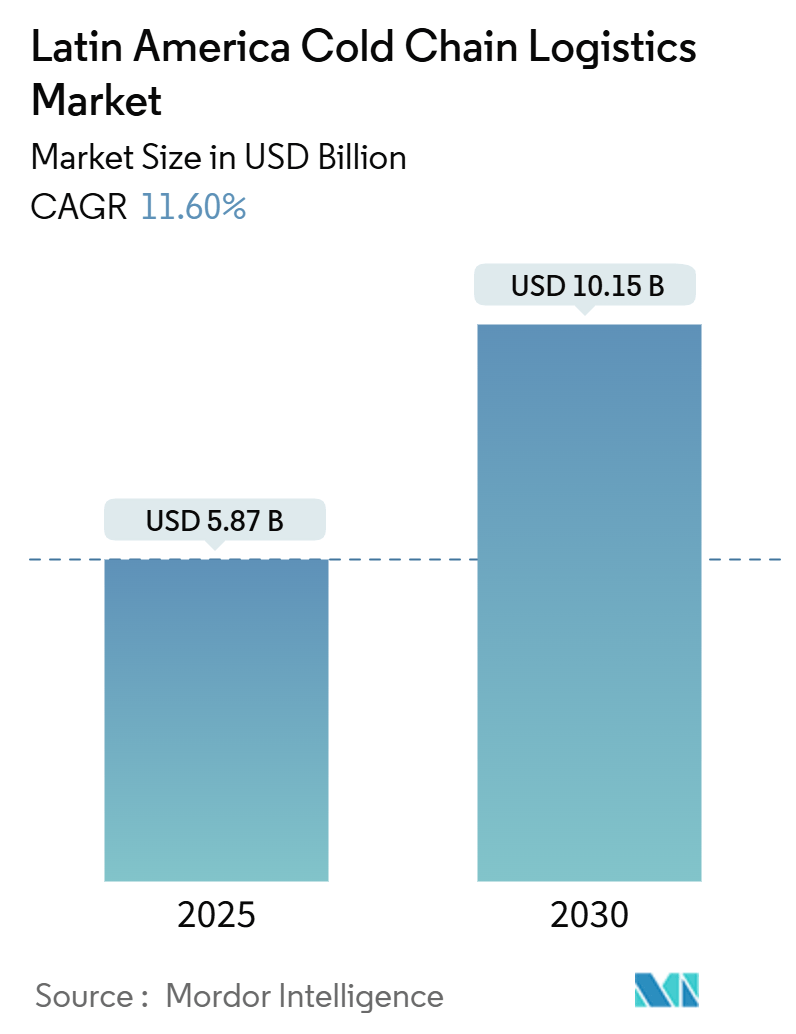

| Market Size (2025) | USD 5.87 Billion |

| Market Size (2030) | USD 10.15 Billion |

| Growth Rate (2025 - 2030) | 11.60% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Latin America Cold Chain Logistics Market Analysis by Mordor Intelligence

The Latin America Cold Chain Logistics Market size is estimated at USD 5.87 billion in 2025, and is expected to reach USD 10.15 billion by 2030, at a CAGR of 11.60% during the forecast period (2025-2030).

The Latin American cold chain logistics landscape is experiencing significant transformation driven by technological advancement and infrastructure development. Major industry players are actively pursuing strategic consolidations to address the region's critical shortage of cold storage space, as exemplified by Emergent Cold Latin America's acquisition of Frigorifico Modelo in October 2022, which added 22,000 cold storage pallets in Montevideo, Uruguay, and 8,400 pallets in Asunción, Paraguay. The modernization of logistics infrastructure is particularly evident in the implementation of advanced cold chain monitoring systems, automated warehouse management solutions, and the integration of blockchain technology for enhanced traceability.

The pharmaceutical cold chain sector is witnessing substantial growth, particularly in Brazil, where the pharmaceutical market has reached a valuation of USD 32 billion, making it one of the largest markets in Latin America. The expansion of pharmaceutical cold chain capabilities is being driven by increasing demand for temperature-sensitive medications, biologics, and vaccines. This has led to significant investments in specialized cold storage facilities and transportation solutions, with companies like CSafe Global establishing new hub operations in strategic locations such as Mexico City to enhance regional distribution capabilities.

The meat and poultry sector is emerging as a crucial driver of cold chain logistics innovation, with Mexico's chicken meat production reaching 3.67 million metric tons, highlighting the growing demand for temperature-controlled logistics solutions. The industry is witnessing a shift toward more sophisticated cold chain solutions, including advanced blast freezing technologies and multi-temperature transport systems. Werner Enterprises' new cross-dock facility in Laredo, Texas, featuring both dry and refrigerated docks, demonstrates the industry's commitment to enhancing cross-border cold chain logistics capabilities between the United States and Latin America.

The retail and e-commerce sectors are catalyzing significant changes in cold chain logistics operations across Latin America. The rise of online grocery shopping and the demand for fresh produce delivery have necessitated the development of more efficient last-mile delivery solutions and urban cold storage facilities. Companies are investing in micro-fulfillment centers and temperature-controlled dark stores in major urban areas to meet the growing demand for rapid delivery of perishable goods. This trend is particularly evident in countries like Brazil and Mexico, where e-commerce penetration in the grocery sector has accelerated, leading to the development of specialized cold chain equipment solutions for urban distribution.

Latin America Cold Chain Logistics Market Trends and Insights

Growing E-commerce and Retail Sector

The rapid expansion of e-commerce platforms and modern retail chains across Latin America has created unprecedented demand for cold chain logistics services. Major retailers are increasingly investing in temperature-controlled warehousing facilities and refrigerated transportation to support their growing online grocery operations and fresh food delivery services. The shift in consumer shopping behavior has led to the development of specialized last-mile delivery solutions for temperature-sensitive products, with retailers implementing innovative cold storage solutions at their distribution centers to maintain product quality and extend shelf life.

The evolution of omnichannel retail strategies has further accelerated investments in cold chain infrastructure, as retailers strive to provide seamless experiences across online and offline channels. Large supermarket chains are expanding their cold storage capacities and implementing advanced inventory management systems to handle the increasing volume of perishable products. This retail transformation has prompted logistics providers to develop customized solutions, including multi-temperature storage facilities and specialized handling procedures for different product categories, from fresh produce to frozen ready-to-eat meals.

Understand The Key Trends Shaping This Market

Download PDF

Technological Advancements and Infrastructure Development

The integration of Internet of Things (IoT) technologies and automation solutions in cold chain logistics has revolutionized temperature monitoring and control capabilities across Latin America. Advanced sensor systems and real-time tracking solutions are being widely adopted to ensure temperature integrity throughout the supply chain, from storage facilities to transportation. Logistics providers are implementing sophisticated warehouse management systems that enable precise temperature control, inventory optimization, and improved operational efficiency through automated handling systems and smart storage solutions.

Infrastructure modernization efforts across the region have supported the expansion of cold chain networks, with significant investments in refrigerated warehouses and specialized logistics facilities. The development of modern cold storage facilities equipped with energy-efficient refrigeration systems and advanced temperature monitoring capabilities has enhanced the industry's ability to maintain product quality and reduce spoilage. These technological improvements have enabled logistics providers to offer value-added services such as blast freezing, temperature-controlled cross-docking, and specialized handling for different temperature zones, meeting the diverse requirements of food, pharmaceutical, and other temperature-sensitive industries.

Growth in Food and Beverage Industry

The expanding food and beverage industry in Latin America has emerged as a crucial driver for cold chain logistics development, particularly due to increasing exports of perishable products and growing domestic consumption of processed foods. Agricultural producers and food manufacturers are investing heavily in cold chain solutions to maintain product quality and extend shelf life, especially for high-value exports such as fruits, vegetables, and meat products. The industry's focus on food safety and quality has led to the implementation of stringent temperature control requirements throughout the supply chain.

The rising demand for frozen and chilled processed foods has created new opportunities for cold chain logistics providers, who are expanding their capabilities to handle diverse temperature requirements. Food manufacturers are increasingly partnering with specialized logistics providers to ensure proper handling and storage of temperature-sensitive ingredients and finished products. This has led to the development of dedicated cold storage facilities and specialized transportation solutions that can maintain multiple temperature zones, catering to different product categories from frozen desserts to chilled dairy products.

Pharmaceutical Industry Expansion

The pharmaceutical sector's growth in Latin America has significantly driven investments in specialized cold chain infrastructure, particularly for temperature-sensitive medications and biologics. Pharmaceutical manufacturers and distributors are implementing stringent temperature control requirements throughout their supply chains, necessitating advanced cold storage solutions and specialized transportation services. The industry's focus on maintaining product efficacy through proper temperature management has led to the development of dedicated pharmaceutical-grade cold storage facilities with precise temperature control capabilities.

The expansion of pharmaceutical manufacturing capabilities in countries like Brazil and Mexico has created increased demand for sophisticated cold chain solutions. Logistics providers are investing in specialized facilities equipped with redundant cooling systems, continuous temperature monitoring, and advanced security features to meet the stringent requirements of pharmaceutical storage and distribution. This has led to the emergence of specialized pharmaceutical logistics services offering end-to-end temperature-controlled logistics solutions, including validated packaging systems and qualified transportation networks designed specifically for pharmaceutical products.

Segment Analysis: By Service

Cold Storage/Refrigerated Warehousing Segment in Latin America Cold Chain Logistics Market

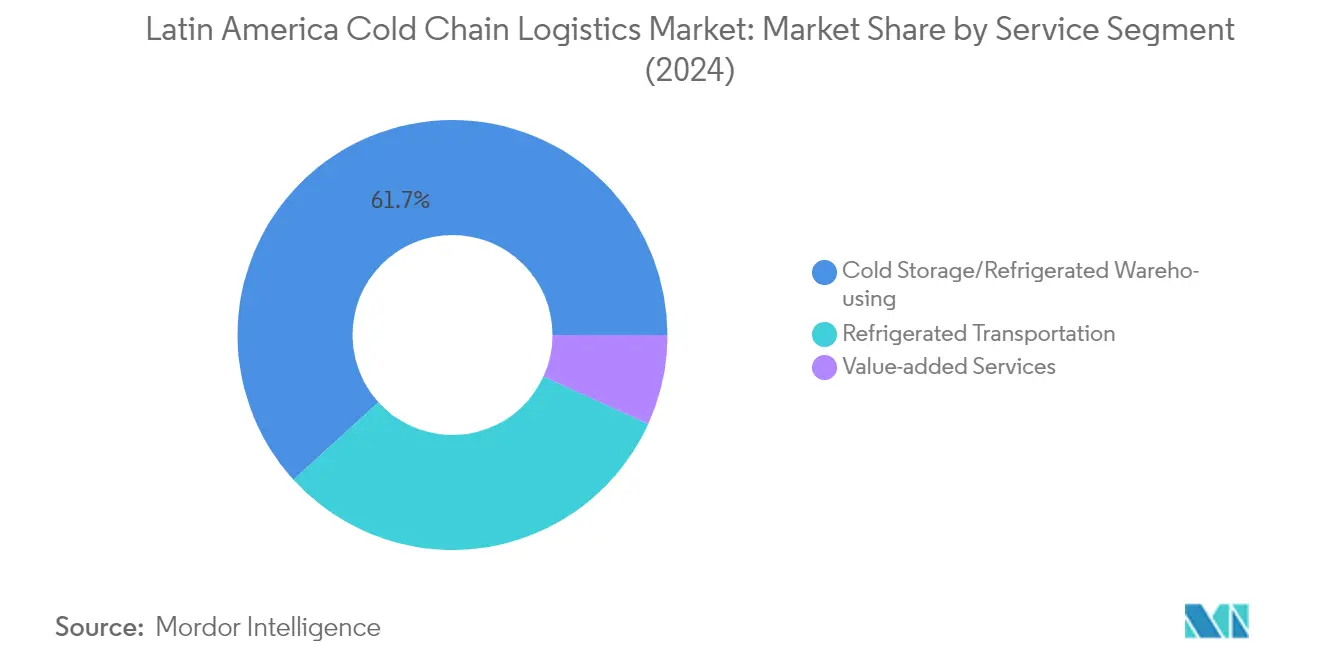

The cold storage/refrigerated warehousing segment dominates the Latin American cold chain logistics market, accounting for approximately 62% of the total market share in 2024. This significant market position is driven by the growing demand from various industries, including pharmaceuticals, food and beverage, and agricultural sectors. The segment's prominence is further strengthened by the expansion of retail chains and increasing international trade of perishable goods across the region. Major players like Frialsa Frigorificos in Mexico and Comfrio Soluções Logísticas in Brazil have established extensive networks of temperature-controlled facilities, contributing to the segment's market leadership. The segment has also seen substantial investments in modern warehousing technologies and automation solutions to improve operational efficiency and maintain precise temperature controls.

Value-added Services Segment in Latin America Cold Chain Logistics Market

The value-added services segment is emerging as the fastest-growing segment in the Latin American cold chain logistics market, with a projected growth rate of approximately 13% during 2024-2029. This rapid growth is primarily driven by increasing demand for specialized services such as order management, blast freezing, labeling, and inventory management. The segment is witnessing significant technological advancement with the integration of warehouse management systems (WMS) and other digital solutions to enhance operational efficiency. Companies are increasingly offering customized value-added services to meet specific client requirements, particularly in the pharmaceutical and food processing sectors. The growth is further supported by the rising adoption of e-commerce platforms and the need for specialized handling of temperature-sensitive products.

Remaining Segments in Latin America Cold Chain Logistics Market Service Segmentation

The refrigerated transportation segment plays a crucial role in completing the cold chain logistics ecosystem in Latin America. This segment encompasses various transportation modes, including road, rail, and maritime services, providing essential connectivity between production centers and end markets. The segment has witnessed significant modernization with the introduction of advanced temperature monitoring systems and real-time tracking capabilities. Companies operating in this segment are increasingly focusing on fleet modernization and route optimization to improve service efficiency and maintain product integrity throughout the transportation process. The segment's development is closely tied to the region's infrastructure improvements and the growing need for seamless cold chain distribution networks.

Segment Analysis: By Temperature

Chilled Segment in Latin America Cold Chain Logistics Market

The chilled segment dominates the Latin American cold chain logistics market, accounting for approximately 63% of the total market share in 2024. This segment primarily caters to temperature-sensitive products requiring storage and transportation between 0°C to 8°C, including fresh produce, dairy products, and certain pharmaceutical items. The segment's dominance is driven by the region's robust agricultural exports, particularly fruits and vegetables, along with growing domestic consumption of fresh products. Major countries like Brazil and Mexico have significantly invested in chilled storage infrastructure and transportation networks to support their agricultural sectors. The increasing demand for fresh food products through modern retail channels and the expansion of organized retail chains have further strengthened this segment's position. Additionally, the pharmaceutical industry's growing requirements for temperature-controlled logistics at chilled temperatures have contributed to the segment's market leadership.

Frozen Segment in Latin America Cold Chain Logistics Market

The frozen segment is experiencing the fastest growth in the Latin American cold chain logistics market, with an expected growth rate of approximately 14% during 2024-2029. This accelerated growth is primarily driven by the increasing demand for frozen food products, particularly in urban areas, and the expansion of quick-service restaurant chains across the region. The segment is benefiting from changing consumer lifestyles and the growing preference for convenience foods, especially in countries like Brazil and Mexico. The frozen segment has also seen substantial investments in advanced freezing technologies and cold storage infrastructure to maintain temperatures below -18°C. The rising exports of frozen meat, seafood, and processed food products to international markets have necessitated the development of sophisticated frozen food logistics networks. Additionally, the segment's growth is supported by the expanding pharmaceutical sector's requirements for ultra-low temperature storage and transportation, particularly for specialized medications and vaccines.

Segment Analysis: By End User

Fish, Meat and Seafood Segment in Latin America Cold Chain Logistics Market

The fish, meat, and seafood segment dominates the Latin American cold chain logistics market, accounting for approximately 36% of the total market share in 2024. This segment's prominence is driven by Latin America's position as a major producer and exporter of meat products, particularly from countries like Brazil, which has emerged as a leading global meat exporter. The region's robust fishing industry, extensive aquaculture operations, and growing meat processing facilities have created substantial demand for cold chain services. The segment's growth is further supported by increasing international trade agreements, stringent food safety regulations, and rising domestic consumption of frozen and chilled meat products across the region. Modern cold storage facilities and refrigerated transportation networks have been developed specifically to cater to this segment's unique requirements, ensuring proper temperature control throughout the supply chain.

Pharmaceutical Segment in Latin America Cold Chain Logistics Market

The pharmaceutical segment is emerging as the fastest-growing segment in the Latin American cold chain logistics market, with an expected growth rate of approximately 19% during 2024-2029. This remarkable growth is primarily driven by the expansion of pharmaceutical manufacturing capabilities in countries like Brazil and Mexico, coupled with increasing healthcare investments across the region. The segment's growth is further accelerated by the rising demand for temperature-sensitive biopharmaceuticals, vaccines, and specialty medicines. Cold chain service providers are increasingly investing in specialized pharmaceutical-grade storage facilities and transportation solutions to meet the stringent regulatory requirements and maintain product integrity. The growing focus on healthcare infrastructure development and the increasing presence of multinational pharmaceutical companies in the region are creating new opportunities for cold chain logistics providers.

Remaining Segments in Latin America Cold Chain Logistics Market End Users

The other significant segments in the Latin American cold chain logistics market include dairy products, fruits and vegetables, bakery and confectionery, and processed food. The dairy products segment maintains a strong presence due to the region's growing dairy industry and increasing consumption of refrigerated dairy products. The fruits and vegetables segment is driven by Latin America's position as a major agricultural exporter, particularly for tropical and exotic fruits. The bakery and confectionery segment is supported by the growing demand for frozen bakery products and temperature-sensitive confectionery items. The processed food segment, while smaller, continues to grow with the increasing adoption of frozen and chilled ready-to-eat products. Each of these segments contributes uniquely to the market's dynamics and requires specialized cold chain solutions to maintain product quality and safety.

Latin America Cold Chain Logistics Market Geography Segment Analysis

Latin America Cold Chain Logistics Market in Brazil

Brazil dominates the Latin American cold chain logistics landscape, commanding approximately 59% of the market share in 2024. The country's extensive cold chain logistics infrastructure, particularly in cold storage and refrigerated warehousing, has been instrumental in supporting its massive agricultural and food processing sectors. Brazil's strategic position as one of the world's largest food producers has necessitated continuous development of its cold supply chain capabilities. The country has witnessed significant investments in modern cold storage facilities, with companies like Comfrio Soluções Logísticas and Superfrio Armazéns Gerais leading the market with their state-of-the-art facilities. The pharmaceutical cold chain segment has also seen substantial growth, driven by the country's position as the largest pharmaceutical market in Latin America. Brazil's cold chain logistics network extends beyond major cities, serving the country's vast agricultural regions and supporting its position as a major food exporter.

Latin America Cold Chain Logistics Market in Colombia

Colombia's cold chain logistics market is projected to grow at an impressive rate of approximately 16% during 2024-2029, emerging as the fastest-growing market in the region. The country's strategic focus on developing its cold chain infrastructure has been driven by its growing agricultural exports and pharmaceutical sector. Colombia has been actively investing in modernizing its cold storage facilities and cold chain transportation networks, particularly in key agricultural regions. The country's commitment to becoming a pharmaceutical hub for the region has led to increased investments in temperature-controlled logistics solutions. The government's initiatives to improve logistics infrastructure and cold chain capabilities have attracted both domestic and international players to the market. Colombia's geographical position and its multiple free trade agreements have further catalyzed the development of its cold chain logistics sector, particularly in supporting the country's growing fresh produce exports.

Latin America Cold Chain Logistics Market in Mexico

Mexico's cold chain logistics market has established itself as a crucial link in the North American supply chain network. The country's strategic location and strong trade relationships with the United States have driven significant investments in cold chain infrastructure. Mexico's cold chain capabilities have been particularly crucial in supporting its substantial agricultural exports and growing pharmaceutical sector. The country has seen notable developments in refrigerated transportation and cold storage facilities, especially near major agricultural production zones and border regions. The implementation of advanced technology in cold chain operations, including temperature monitoring systems and automated warehousing solutions, has enhanced the efficiency of Mexico's cold chain logistics network. The country's cold chain infrastructure has also been instrumental in supporting its growing food processing industry and increasing domestic demand for temperature-sensitive products.

Latin America Cold Chain Logistics Market in Chile

Chile has established itself as a significant player in the Latin American cold chain logistics market, particularly in supporting its robust fruit export industry. The country's cold chain infrastructure has been developed with a strong focus on maintaining the quality of its agricultural exports to international markets. Chile's cold chain network is characterized by its advanced temperature-controlled storage facilities and efficient transportation systems, particularly around its major ports and agricultural regions. The country has implemented stringent quality control measures and international standards in its cold chain operations, making it a preferred choice for international trade partners. The pharmaceutical sector has also contributed to the development of Chile's cold chain capabilities, with increasing investments in specialized storage and transportation solutions. The country's commitment to technological advancement in cold chain operations has resulted in the adoption of sophisticated monitoring and tracking systems.

Latin America Cold Chain Logistics Market in Other Countries

The cold chain logistics market in other Latin American countries, including Panama, Argentina, Peru, and Ecuador, demonstrates varying levels of development and specialization. These markets are characterized by their unique geographical challenges and economic priorities, with each country focusing on specific aspects of cold chain development. Panama, leveraging its strategic position and the Panama Canal, has developed specialized cold chain capabilities for transit and distribution. Argentina's cold chain infrastructure primarily supports its substantial meat and dairy industries. Countries like Peru and Ecuador have been investing in cold chain facilities to support their growing agricultural export sectors. The development of cold chain infrastructure in these markets has been influenced by factors such as urbanization, changing consumer preferences, and increasing international trade requirements. Regional cooperation and trade agreements have played a crucial role in shaping the cold chain landscape across these countries.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in Latin American Cold Chain Logistics Market

The Latin American cold chain logistics market features prominent players like Frialsa Frigorificos, Comfrio, Superfrio Armazéns Gerais, and Friozem Armazens Frigorificos leading the industry. Companies across the region are increasingly focusing on technological integration, implementing advanced warehouse management systems, RFID tracking, and IoT-enabled solutions to enhance operational efficiency. Strategic expansion through new facility development and modernization of existing infrastructure has become a key trend, particularly in major markets like Brazil and Mexico. The industry is witnessing a strong push toward value-added services, including blast freezing, specialized handling, and customized cold storage solutions. Market leaders are also emphasizing sustainability initiatives and energy-efficient cold storage solutions while strengthening their last-mile delivery capabilities to serve the growing e-commerce sector.

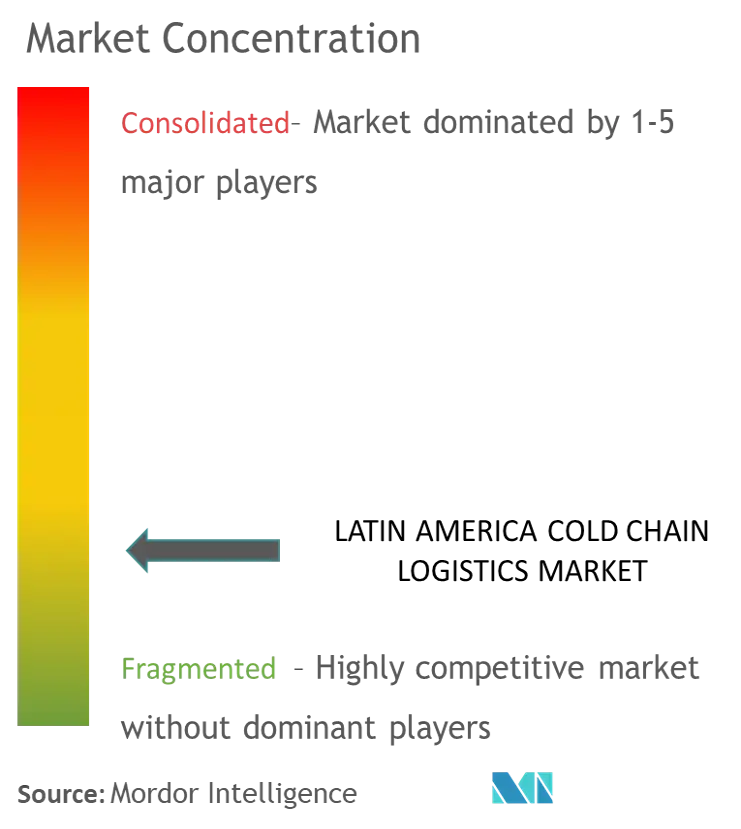

Fragmented Market with Growing Consolidation Trends

The Latin American cold chain logistics market exhibits a highly fragmented structure, particularly dominated by domestic players in key markets like Brazil and Mexico. Regional specialists with deep local market knowledge and established distribution networks hold significant market share, while global players like Americold are expanding their presence through strategic partnerships and acquisitions. The market is witnessing increased consolidation activities, exemplified by Americold's joint venture with SuperFrio in Brazil and the formation of Qualianz through multiple acquisitions in Mexico, indicating a shift toward a more organized market structure.

The competitive dynamics vary significantly across different countries, with Brazil featuring a more mature market led by domestic players, while Mexico shows a mix of both local and international operators. Market consolidation is driven by the need for operational scale, technology investments, and comprehensive service offerings. Companies are increasingly focusing on specialized services for different industry verticals, particularly in the pharmaceutical and food sectors, while also expanding their geographical presence through strategic alliances and network optimization.

Innovation and Service Integration Drive Success

Success in the Latin American refrigerated logistics market increasingly depends on companies' ability to offer integrated end-to-end solutions while maintaining operational excellence. Market leaders are investing in advanced technology platforms, developing specialized handling capabilities, and expanding their service portfolios to include value-added services. The ability to serve multiple industry verticals, maintain compliance with international quality standards, and offer flexible storage solutions has become crucial for maintaining a competitive advantage. Companies are also focusing on developing sustainable practices and energy-efficient operations to meet growing environmental concerns and regulatory requirements.

For new entrants and growing players, success lies in identifying and serving niche markets, developing specialized expertise in handling specific product categories, and building strong relationships with local customers. The market presents opportunities for companies that can offer innovative solutions in areas such as last-mile delivery, temperature-controlled logistics, and quality assurance. Strategic partnerships with technology providers, investment in automation solutions, and a focus on customer-centric services are becoming increasingly important for gaining market share. Companies must also navigate regulatory requirements, maintain high service quality standards, and develop robust risk management practices to succeed in this competitive landscape.

Latin America Cold Chain Logistics Industry Leaders

-

Frialsa Frigorificos SA

-

Comfrio SoluCoes LogIsticas

-

Friozem Armazéns Frigorificos

-

Superfrio Armazéns Gerais

-

Americold Logistics

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2024: Emergent Cold LatAm, a large provider of temperature-controlled food logistics in Latin America, has inaugurated its new warehouse in Callao, Peru, reaffirming its commitment to the country's economic growth and strengthening the food supply chain in the region. This modern facility, with a capacity of 79,000 cubic meters and space for 12,000 pallets, increases Emergent Cold LatAm's storage capacity in Peru by 120%. Emergent Cold LatAm already has six plants with EDGE Advanced certification in Latin America, including the Callao plant.

- June 2023: Canadian Pacific announced a strategic partnership to co-host American warehouse facilities on Canadian Pacific's (CPKC) network. Supported by rail transportation, the goal is to construct the first facility on CPKC's network in Kansas City (Mo.), Kansas, to combine cold storage and added-value services with accelerated intermodal transport solutions connecting key markets in the U.S., Midwest, and Mexico.

Latin America Cold Chain Logistics Market Report Scope

A cold chain is a seamless logistical and operational process that facilitates the controlled temperature production, transportation, storage, and distribution of goods, notably food, pharmaceuticals, and other temperature-sensitive products. According to the Food and Agriculture Organization of the United Nations (FAO), the cold chain encompasses pre-cooling, storage, transportation, distribution, retail, and even domestic refrigeration stages.

A complete background analysis of the Latin America Cold Chain Logistics market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The Latin America Cold Chain Logistics Market is segmented by service (cold storage/refrigerated warehousing, refrigerated transportation, and value-added services), temperature (chilled, frozen and ambient), end-user (fruits and vegetables, dairy products (milk, butter, cheese, ice cream, etc.), fish, meat, and seafood, processed food, pharmaceutical (includes biopharma), bakery and confectionery, and other end-users), and country (Mexico, Brazil, Chile, Colombia, and rest of Latin America). The report offers Market size and forecasts for Latin America Cold Chain Logistics Market in value (USD) for all the above segments.

By Service

| Cold Storage/Refrigerated Warehousing |

| Refrigerated Transportation |

| Value-added Services (Order Management, Blast Freezing, Labeling, Inventory Management, etc.) |

By Temperature

| Chilled |

| Frozen |

| Ambient |

By End User

| Fruits and Vegetables |

| Dairy Products (Milk, Butter, Cheese, Ice Cream, etc.) |

| Fish, Meat, and Seafood |

| Processed Food |

| Pharmaceutical (Includes Biopharma) |

| Bakery and Confectionery |

| Other End Users |

By Country

| Mexico |

| Brazil |

| Chile |

| Colombia |

| Rest of Latin America |

| By Service | Cold Storage/Refrigerated Warehousing |

| Refrigerated Transportation | |

| Value-added Services (Order Management, Blast Freezing, Labeling, Inventory Management, etc.) | |

| By Temperature | Chilled |

| Frozen | |

| Ambient | |

| By End User | Fruits and Vegetables |

| Dairy Products (Milk, Butter, Cheese, Ice Cream, etc.) | |

| Fish, Meat, and Seafood | |

| Processed Food | |

| Pharmaceutical (Includes Biopharma) | |

| Bakery and Confectionery | |

| Other End Users | |

| By Country | Mexico |

| Brazil | |

| Chile | |

| Colombia | |

| Rest of Latin America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Latin America Cold Chain Logistics Market?

The Latin America Cold Chain Logistics Market size is expected to reach USD 5.87 billion in 2025 and grow at a CAGR of 11.60% to reach USD 10.15 billion by 2030.

What is the current Latin America Cold Chain Logistics Market size?

In 2025, the Latin America Cold Chain Logistics Market size is expected to reach USD 5.87 billion.

Who are the key players in Latin America Cold Chain Logistics Market?

Frialsa Frigorificos SA, Comfrio SoluCoes LogIsticas, Friozem Armazéns Frigorificos, Superfrio Armazéns Gerais and Americold Logistics are the major companies operating in the Latin America Cold Chain Logistics Market.

What years does this Latin America Cold Chain Logistics Market cover, and what was the market size in 2024?

In 2024, the Latin America Cold Chain Logistics Market size was estimated at USD 5.19 billion. The report covers the Latin America Cold Chain Logistics Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Latin America Cold Chain Logistics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: