LATAM Oilfield Chemicals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

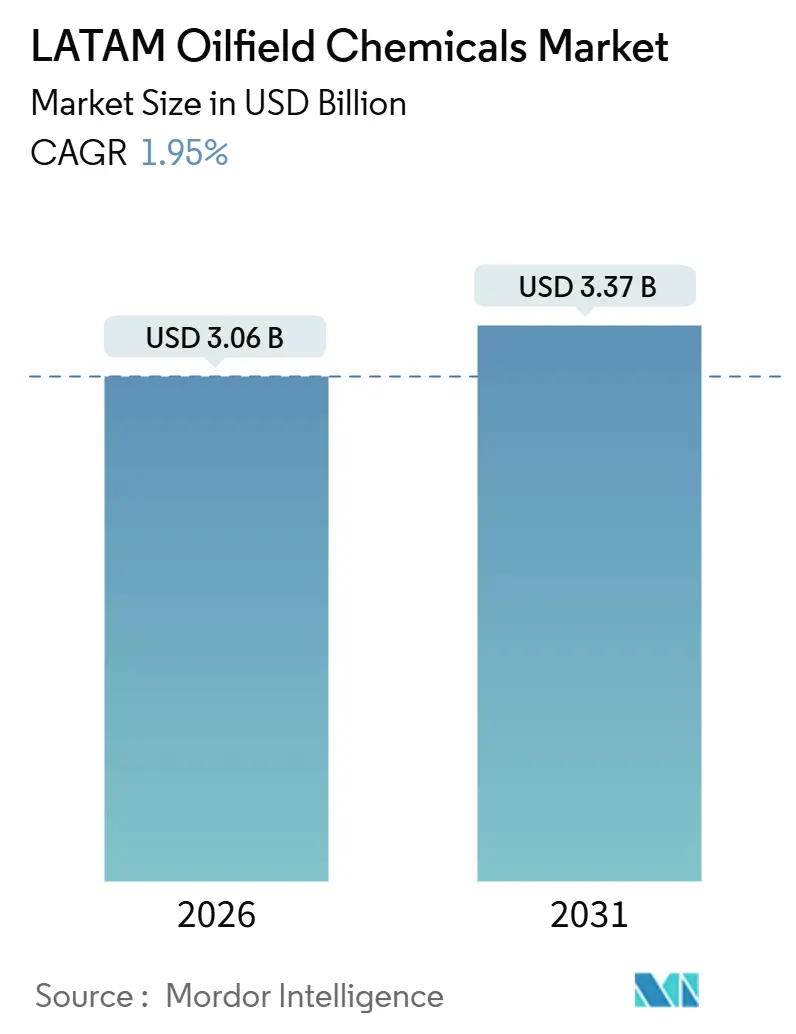

| Market Size (2026) | USD 3.06 Billion |

| Market Size (2031) | USD 3.37 Billion |

| Growth Rate (2026 - 2031) | 1.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LATAM Oilfield Chemicals Market Analysis by Mordor Intelligence

The LATAM Oilfield Chemicals Market size is estimated at USD 3.06 billion in 2026, and is expected to reach USD 3.37 billion by 2031, at a CAGR of 1.95% during the forecast period (2026-2031). This measured expansion mirrors the shift from high-volume conventional plays toward technically demanding ultra-deepwater and shale reservoirs that rely on premium chemical formulations. Pre-salt projects in Brazil, shale stimulation in Argentina, and mature-field programs in Mexico continue to elevate per-well chemical consumption, while local-content rules are reshaping supply chains. Volatile Brent prices, stretched product-approval cycles, and labor shortages for advanced stimulation chemistries temper the growth outlook, yet rising deepwater activity and enhanced-oil-recovery (EOR) pilots underpin steady demand for corrosion inhibitors, demulsifiers, and low-dosage hydrate inhibitors. Competitive differentiation hinges on subsea-rated corrosion packages, thermally stable polymers, and digital dosage-optimization platforms as operators prioritize uptime and HSE compliance across complex assets.

Key Report Takeaways

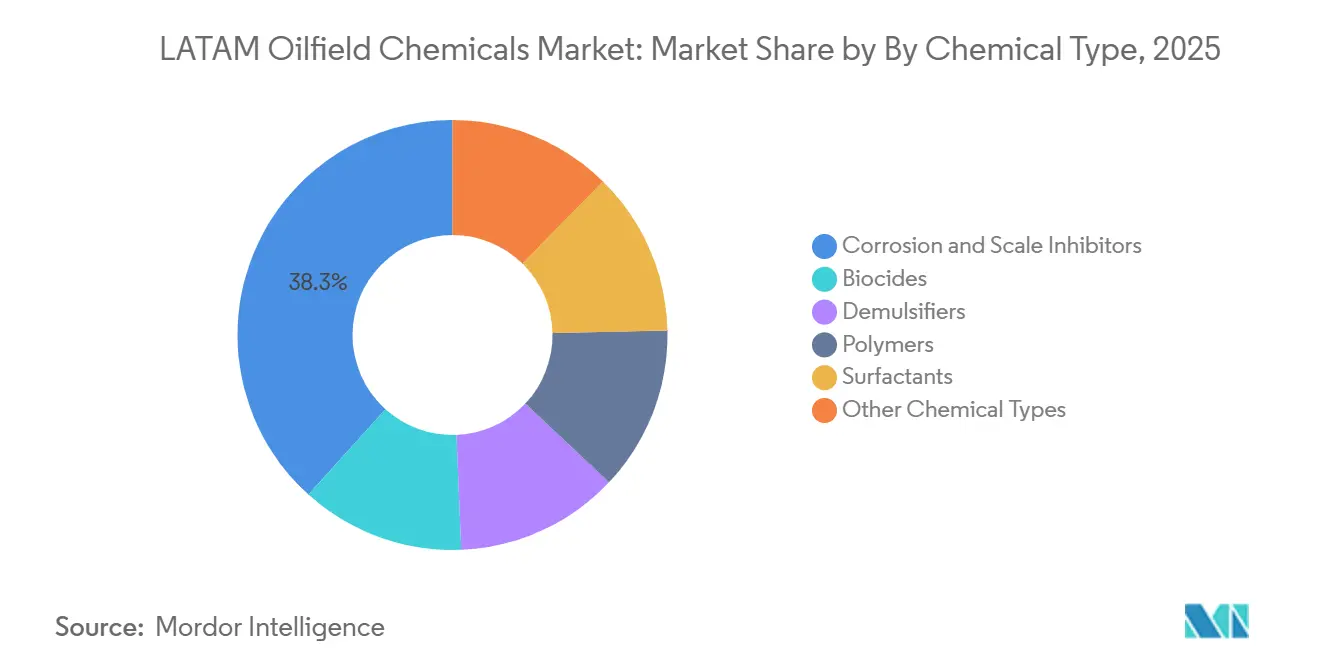

- In 2025, corrosion and scale inhibitors accounted for 38.32% of the LATAM oilfield chemicals market, reflecting their dominant position by chemical type. Demulsifiers are projected to grow at a compound annual growth rate (CAGR) of 2.07% during the forecast period, extending through 2031.

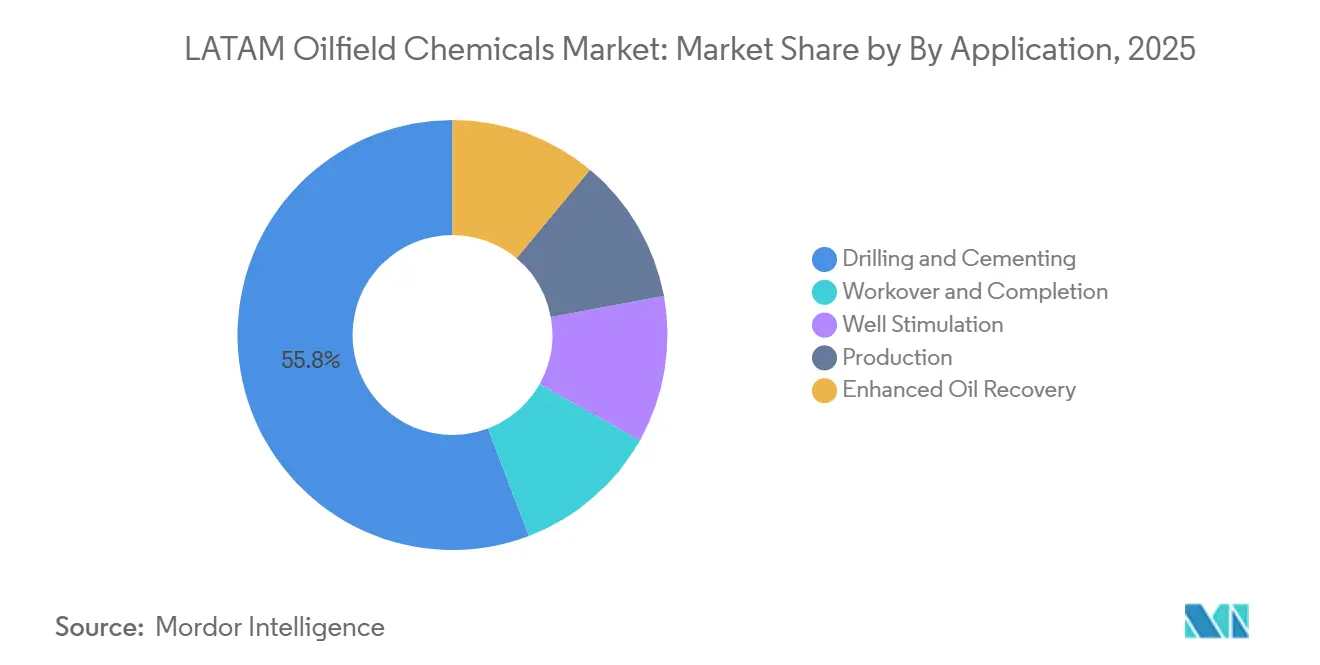

- By application, drilling and cementing emerged as the leading segment in 2025, capturing 55.79% of the market share. Production chemicals are expected to expand at a CAGR of 2.18% between 2026 and 2031, highlighting their growth potential in the coming years.

- Geographically, Brazil led the LATAM oilfield chemicals market in 2025, holding a 36.09% share. The country is forecast to grow at a CAGR of 3.61% through 2031, underscoring its significance in the regional market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

LATAM Oilfield Chemicals Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continued deep-water projects in Brazil pre-salt basins | +0.8% | Brazil (Santos Basin, Campos Basin) | Long term (≥ 4 years) |

| Accelerated mature-field EOR programs in Mexico | +0.4% | Mexico (Cantarell, Ku-Maloob-Zaap) | Medium term (2-4 years) |

| Shale pilot successes in Vaca Muerta | +0.6% | Argentina (Neuquén Province) | Medium term (2-4 years) |

| National content rules fostering local chemical manufacturing | +0.3% | Brazil, Mexico | Long term (≥ 4 years) |

| Low-dosage hydrate inhibitors replacing methanol in ultra-deepwater tie-backs | +0.4% | Brazil, Colombia (offshore) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Continued Deep-Water Projects in Brazil Pre-Salt Basins

Brazil’s pre-salt output rose to 2.1 million b/d in early 2026 as Petrobras brought five FPSOs online between 2024 and 2026[1]Petrobras, “Pre-Salt Production Update,” PETROBRAS.COM.BR. Extreme temperature and corrosive conditions below 2,000 m of water and 5,000 m of salt drive continuous injection of scale and corrosion inhibitors, while kinetic hydrate inhibitors at 0.5%–1% dosage have replaced bulk methanol on assets such as Búzios and Bacalhau. Revised ANP discharge limits, effective 2024, compel suppliers to reformulate with biodegradable surfactants, raising development costs but opening opportunities for “green” chemistries. Subsea systems capable of multi-stream chemical delivery now cost USD 5 million–10 million per well, yet they extend tubing life and cut unplanned downtime.

Accelerated Mature-Field EOR Programs in Mexico Post-Energy Reform

Pemex initiated polymer-flood pilots at Cantarell in 2024 and surfactant-polymer trials at Ku-Maloob-Zaap in 2025, targeting 50 kb/d of incremental recovery. High-temperature, high-salinity reservoirs degrade standard polyacrylamides, prompting the adoption of sulfonated copolymers that retain viscosity above 90 °C, now codified in Pemex procurement guidelines. Private operators remain cautious, favoring primary production, yet national-content rules requiring 35% domestic supply onshore have catalyzed joint ventures that localize blending and cut logistics costs.

Shale Pilot Successes in Neuquén (Vaca Muerta) Driving Chemical Demand

YPF drilled some 400 wells in 2025, employing dual-stage fracturing that consumes 25% more friction reducers than single-stage designs. Slickwater systems with polyacrylamide friction reducers enable higher pump rates, while mobile blending units combine guar, biocides, and clay stabilizers on location. Completion schedules depend on trained chemical engineers; Argentina produced fewer than 200 petroleum engineers in 2024, compelling service firms to import talent at high cost. Infrastructure upgrades such as the VMOS pipeline shortened trucking distances and lowered delivered chemical prices by 15%–20%.

National Content Rules Fostering Local Chemical Manufacturing (Brazil/Mexico)

ANP lifted offshore-chemical local-content thresholds to 50% in 2025, compelling multinationals to invest in Macaé and Rio de Janeiro blending facilities[2]Agência Nacional do Petróleo, “Resolution 2025,” ANP.GOV.BR . Baker Hughes opened a USD 25 million plant in March 2025, while ChampionX doubled capacity at its Rio site in February 2025. Mexico’s CNH set a 35% requirement in 2024, accelerating partnerships between global formulators and domestic distributors. The mandates lengthen product-approval cycles by 6–9 months but guarantee demand for locally sourced commodities, even where imports would be cheaper.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Brent price below USD 70 delaying CAPEX approvals | -0.4% | Colombia, Ecuador, Peru | Short term (≤ 2 years) |

| Skilled-labor shortages for advanced stimulation chemistries | -0.2% | Argentina (Neuquén), Mexico | Medium term (2-4 years) |

| Lengthy product-registration cycles with ANP and CNH | -0.2% | Brazil, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Brent Price Below USD 70 Delaying CAPEX Approvals

Brent traded in the USD 65–72 band in early 2025, prompting Ecopetrol to postpone the Uchuva-2 appraisal well and other regional projects. Operators shifted to short-cycle infill workovers that require fewer drilling and cementing additives, compressing demand for high-margin chemistries. Month-to-month supply contracts protect cash flows but inflate suppliers’ working-capital needs.

Skilled-Labor Shortages for Advanced Stimulation Chemistries

Vaca Muerta requires on-site engineers to adjust friction-reducer ratios in real time, yet local graduation rates cover less than half the basin’s staffing needs. Service firms rotate North American crews, adding USD 50,000–80,000 per well in mobilization costs. Similar gaps in Mexico’s polymer-flood pilots delay rollout and heighten the risk of mis-blended fluids that can damage formations or breach environmental rules.

Segment Analysis

By Chemical Type: Corrosion Inhibitors Anchor Mature-Field Economics

Corrosion and scale inhibitors retained 38.32% of the LATAM oilfield chemicals market share in 2025, reflecting their central role in protecting tubulars and subsea hardware exposed to high CO₂ and H₂S streams. Demulsifiers are set to record the fastest 2.07% CAGR through 2031 as crude-quality specifications tighten and water cuts climb in aging offshore assets. Petrobras alone injected more than 12,000 t of scale inhibitors into pre-salt wells in 2025. Specialty low-dosage hydrate inhibitors, grouped under “other chemical types,” command USD 8–12 kg yet lower storage volumes by up to 70%, an attractive trade-off for ultra-deepwater tie-backs. ANP discharge standards, effective 2024, are steering investment toward biodegradable surfactants, bolstering demand for green formulations.

Polymers captured about 18% of the LATAM oilfield chemicals market size, concentrated in Vaca Muerta and Mexican EOR pilots. Surfactants accounted for a mid-teens share, primarily in drilling fluids, where they improve cuttings transport in high-angle wells. Biocides, although a smaller segment, remain critical to mitigate sulfate-reducing bacteria that accelerate corrosion and sour production streams. Digital dosage-optimization tools deployed on FPSOs reduced corrosion-inhibitor use by 12% in 2025 without compromising asset integrity.

Note: Segment shares of all individual segments available upon report purchase

By Application: Drilling Intensity Sustains Chemical Volumes

Drilling and cementing represented 55.79% of the LATAM oilfield chemicals market share in 2025 because deepwater wells in Brazil and appraisal wells in Argentina consume up to 1,200 t of fluids and additives per well. Production chemicals will grow fastest at a 2.18% CAGR to 2031 as operators pivot from exploration toward maximizing output from existing assets. A single Santos Basin well demands 6–8 identified chemical streams for corrosion control, scale prevention, and hydrate mitigation, locking in recurring demand. Conversely, rig counts fell 8% in Colombia and Ecuador during 2025, echoing Brent volatility and trimming drilling-fluid volumes.

Workover and completion fluids occupy a mid-single-digit slice of the LATAM oilfield chemicals market size but benefit from Pemex’s shut-in well reactivations. Enhanced-oil-recovery chemistries remain small yet outpace the headline market as Mexico scales polymer-flooding pilots. Application mix varies by water depth: offshore projects allocate 60% of spend to drilling and cementing, while onshore campaigns tilt 60% toward production. CNH now mandates annual disclosure of chemical use by application, sharpening demand visibility for suppliers.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Brazil anchors the LATAM oilfield chemicals market, accounting for 36.09% of the 2025 market size and is projected to grow at a 3.61% CAGR through 2031 on the back of new FPSOs and higher output from Búzios and Mero. Operators deploy subsea chemical-injection systems that cost up to USD 10 million per well yet ensure real-time delivery of corrosion inhibitors, scale inhibitors, and LDHIs. Equinor sources 60% of Bacalhau chemicals locally to satisfy ANP rules.

Mexico followed with a significant consumption, sustained by Pemex’s mature-field EOR pilots and private shallow-water developments. Argentina’s oilfield demand is driven by Vaca Muerta, where chemical intensity per barrel triples that of conventional plays. Colombia, Peru, and Ecuador are witnessing rising demand for oilfield chemicals; Colombia leads on the strength of heavy-oil production, although delayed offshore campaigns restrain short-term growth.

Competitive Landscape

The LATAM oilfield chemicals market is moderately consolidated, with the top five players accounting for a significant market share. Local-content mandates open space for regional formulators who supply commodity biocides and demulsifiers at 15%–20% lower prices. Baker Hughes’ Macaé facility cuts delivery times from eight to two weeks and secures ANP preference. Brazilian independents such as Quimidrol have earned ANP certification for corrosion inhibitors, challenging multinational price points. Patent filings stayed under 50 across Brazil and Mexico during 2024–2025, indicating that execution and regulatory fluency outweigh proprietary chemistry in driving share. Technology trends center on smart chemical-management systems, green surfactants, and subsea-qualified LDHIs that deliver higher value per kilogram.

LATAM Oilfield Chemicals Industry Leaders

SLB

Baker Hughes Company

ChampionX

Clariant AG

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Baker Hughes opened a USD 25 million chemical plant in Macaé with 15,000 t / yr capacity for corrosion inhibitors, demulsifiers, and scale inhibitors, meeting ANP’s 50% local-content rule.

- February 2025: ChampionX doubled Rio de Janeiro blending capacity by 8,000 t / yr, adding a quality-control lab to speed ANP approvals.

- January 2025: SLB (Schlumberger) secured a five-year, USD 180 million chemical-supply contract with Petrobras covering pre-salt corrosion, hydrate, and demulsifier packages, including deployment of the ChemWatcher digital platform on 15 FPSOs.

LATAM Oilfield Chemicals Market Report Scope

Oilfield chemicals are critical to optimizing operations across the oil and gas lifecycle, including exploration, drilling, production, and transportation. These formulations enhance operational efficiency, maximize resource recovery, protect equipment, and effectively manage fluid-related challenges such as corrosion, scaling, and water separation.

The LATAM Oilfield Chemicals market is segmented by chemical type, application, and geography. By chemical type, the market is segmented into biocide, corrosion and scale inhibitor, demulsifier, polymers, surfactants, and other chemical types. By application, the market is segmented into drilling and cementing, workover and completion, well stimulation, production, and enhanced oil recovery. The report also covers the market sizes and forecasts in 6 major countries across Latin America. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Biocides |

| Corrosion and Scale Inhibitors |

| Demulsifiers |

| Polymers |

| Surfactants |

| Other Chemical Types |

| Drilling and Cementing |

| Workover and Completion |

| Well Stimulation |

| Production |

| Enhanced Oil Recovery |

| Mexico |

| Brazil |

| Colombia |

| Argentina |

| Peru |

| Ecuador |

| Rest of Latin America |

| By Chemical Type | Biocides |

| Corrosion and Scale Inhibitors | |

| Demulsifiers | |

| Polymers | |

| Surfactants | |

| Other Chemical Types | |

| By Application | Drilling and Cementing |

| Workover and Completion | |

| Well Stimulation | |

| Production | |

| Enhanced Oil Recovery | |

| By Country | Mexico |

| Brazil | |

| Colombia | |

| Argentina | |

| Peru | |

| Ecuador | |

| Rest of Latin America |

Key Questions Answered in the Report

What is the current value of the LATAM oilfield chemicals market?

The LATAM oilfield chemicals market size reached USD 3.06 billion in 2026.

Which country leads regional demand for oilfield chemicals?

Brazil commands 36.09% of regional demand, driven by large pre-salt developments.

Which chemical type holds the largest share in Latin America?

Corrosion and scale inhibitors held 38.32% of the market share in 2025.

What application segment grows fastest through 2031?

Production chemicals are forecast to expand at a 2.18% CAGR as operators maximize existing assets.

How do local-content rules affect suppliers?

Brazil’s 50% and Mexico’s 35% thresholds oblige global suppliers to invest in local blending facilities to qualify for tenders.

Which technology trend is reshaping chemical consumption offshore?

Digital dosage-optimization platforms such as ChemWatcher reduce chemical use by about 12% while maintaining asset integrity.