Laboratory Filtration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

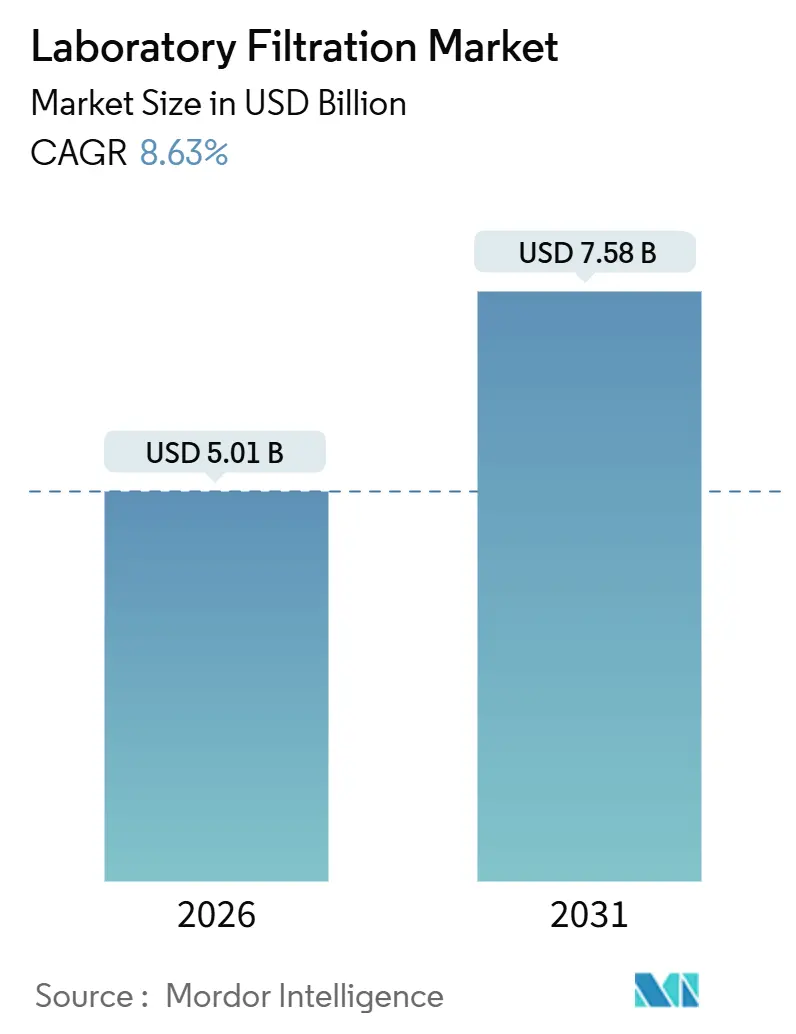

| Market Size (2026) | USD 5.01 Billion |

| Market Size (2031) | USD 7.58 Billion |

| Growth Rate (2026 - 2031) | 8.63% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laboratory Filtration Market Analysis by Mordor Intelligence

The Laboratory Filtration Market size is estimated at USD 5.01 billion in 2026, and is expected to reach USD 7.58 billion by 2031, at a CAGR of 8.63% during the forecast period (2026-2031).

Cell- and gene-therapy scale-up replaces stainless-steel loops with disposable capsules, which reduce cross-contamination risk and validation time. Meanwhile, biopharma R&D spending drives contract labs to secure annual media contracts, stabilizing demand. Miniaturized high-throughput screening rigs increase accessory consumption because every 96-well plate incorporates discrete 0.2-µm filters, strengthening the connections between filtration suppliers and instrumentation OEMs. Viral-safety mandates now require orthogonal barriers, so monoclonal-antibody manufacturers embed 20-nm nanofiltration steps that lift consumable value per batch, turning compliance into a clear revenue accelerant. Competitive dynamics favor vertically integrated vendors capable of casting membranes, assembling sterile capsules, and shipping within 48 hours; yet, white space persists in nanoliter-scale devices and hybrid ceramic-polymer media that resist caustic cleaning, leaving the laboratory filtration market open for niche innovators.

Key Report Takeaways

- By product type, Filtration Media led with 57.31% revenue share in 2025, whereas Filtration Accessories are forecast to expand at a 10.92% CAGR through 2031.

- By technique, microfiltration accounted for 39.68% of the laboratory filtration market share in 2025, while nanofiltration and reverse osmosis are projected to grow at a 9.54% CAGR through 2031.

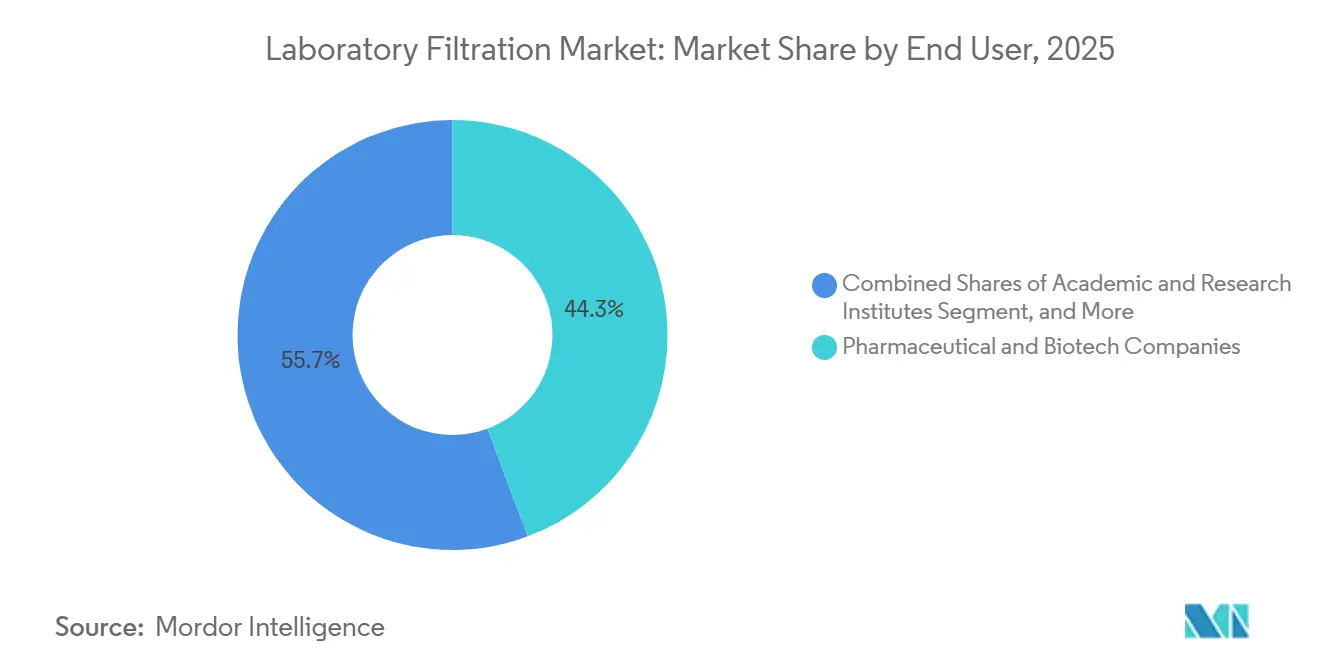

- By end user, pharmaceutical and biotechnology companies held a 44.26% share in 2025, but academic and research institutes are advancing at a 12.51% CAGR over the forecast window.

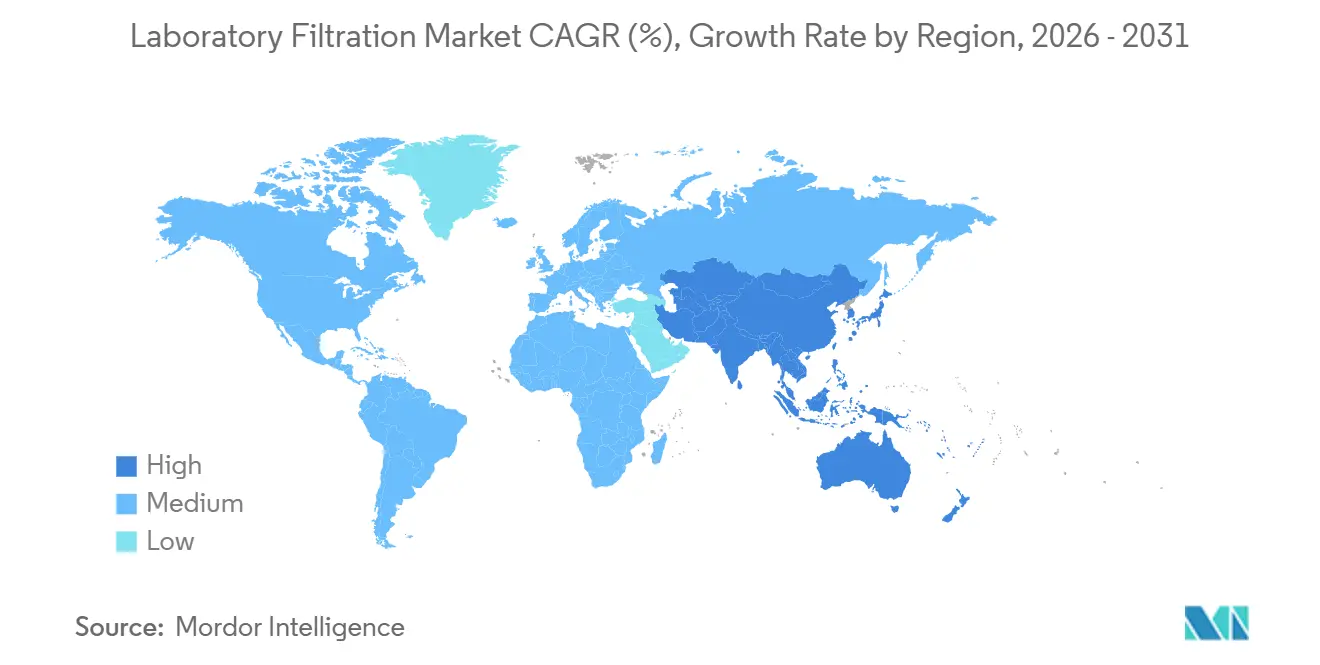

- By geography, North America commanded a 36.24% share in 2025, whereas the Asia-Pacific region is poised for an 11.63% CAGR through 2031, as China and India license dozens of biosimilar plants.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laboratory Filtration Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Biopharma R&D Spend | +2.3% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Expansion of Cell & Gene Therapy Manufacturing | +2.1% | North America, Europe, Asia-Pacific (China, Japan, South Korea) | Long term (≥ 4 years) |

| Rapid Adoption of Single-Use Filtration Assemblies | +1.8% | Global, led by North America & Western Europe | Short term (≤ 2 years) |

| Miniaturized High-Throughput Screening Driving Microfiltration Demand | +1.4% | North America, Europe, Asia-Pacific research hubs | Medium term (2-4 years) |

| Growth of CROs & CDMOs Boosting Cost-Effective Filtration Assemblies | +1.6% | Asia-Pacific core, spill-over to Latin America & MEA | Medium term (2-4 years) |

| Technological Advancements in Laboratory Filtration | +1.2% | Global, early adoption in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Biopharma R&D Spend

Global pharmaceutical R&D reached USD 244 billion in 2025, a 7.5% increase year-over-year, with biologics accounting for 62% of this expenditure.[1]Pharmaceutical Research and Manufacturers of America, “Biopharmaceutical Research Industry Profile 2025,” phrma.org Each investigational new drug submission now triggers 15–20 sterility and viral clearance validation runs, which translates into a membrane area equivalent to three to five production batches. Contract laboratories experienced a 28% increase in sample throughput for stability testing, prompting procurement managers to negotiate long-term filtration-media agreements that secure price and availability. Regulators continue to refine guidance on process validation, prompting sponsors to repeat studies to meet evolving sterility benchmarks, thereby sustaining membrane consumption. The upshot is a durable baseline of recurring orders that helps the laboratory filtration market weather macroeconomic swings.

Expansion of Cell & Gene Therapy Manufacturing

Approved cell- and gene-therapy products climbed to 37 by end-2025, and 180 programs advanced to Phase II/III, doubling the installed base of GMP suites dedicated to viral-vector work.[2]U.S. Food and Drug Administration, “Guidance for Industry: Sterile Drug Products Produced by Aseptic Processing,” fda.gov Lentiviral and AAV purification depend on tangential-flow filtration, with each 50-L bioreactor run consuming around 12 m² of hollow-fiber membrane. Sartorius reported that cell-therapy customers rose from 11% to 19% of its bioprocess revenue between 2023 and 2025, underlining how the segment reshapes order books.[3]Sartorius AG, “Investor Relations – Annual Reports,” sartorius.com Commercial-scale expansion will require a tenfold increase in filtration capacity by 2028, compelling CDMOs to pre-qualify multiple suppliers. Vendors able to furnish viral-retention data across diverse serotypes enjoy a widening moat in the laboratory filtration market.

Rapid Adoption of Single-Use Filtration Assemblies

Single-use systems accounted for 58% of new filtration installations in 2025, up from 41% in 2022, as operators eliminated cleaning validation and reduced turnaround time from 18 hours to under 2 hours. Danaher’s Cytiva unit reported 34% growth in single-use filtration, nearly triple the pace of its reusable line, confirming the demand from small-volume, multi-product campaigns. Although per-liter consumable costs are higher, the total cost of ownership breaks even below 500 L, covering most clinical and niche commercial lots. Waste-disposal rules remain a hurdle, but industry consortia are piloting take-back schemes that reduce landfill volumes, sustaining momentum for disposables in the laboratory filtration market.

Miniaturized High-Throughput Screening Driving Microfiltration Demand

Drug-discovery robots now process 50,000 compounds per week, and each well requires a dedicated filter to prevent carryover, multiplying accessory volumes far faster than media footage. Agilent’s 2025 launch of Captiva Premium syringe filters reduced ion suppression in LC-MS workflows by 18%, demonstrating how performance differentiation can command price premiums in otherwise commoditized formats. Academic core facilities are following the trend, acquiring microplate filter inserts to streamline sample preparation for metabolomics. This surge underpins the laboratory filtration market’s accessory boom and helps offset margin pressure in standard cartridges.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Volatility for High-Grade Membrane Polymers | -1.2% | Global, acute in Asia-Pacific polymer production hubs | Short term (≤ 2 years) |

| Waste-Disposal Compliance Costs for Single-Use Plastics | -0.7% | Europe & North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Price Pressure from Commoditization of Syringe Filters | -0.6% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Emerging PFAS Regulations Limiting PTFE Filter Use | -0.9% | North America & Europe, potential spill-over to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Volatility for High-Grade Membrane Polymers

Polyvinylidene fluoride and polyethersulfone resins originate from just three Asian producers, so any disruption cascades through lead times of 8 to 12 weeks for finished rolls. A typhoon shut down a Taiwan PVDF plant in August 2025, reducing availability by 18% and driving up spot prices for pharmaceutical-grade PES by 23%. Large vendors hedge with multi-year offtake contracts, but mid-tier assemblers endure allocation cuts that erode margins. Regulatory dossiers name specific membrane chemistries, making emergency substitutions costly. Vertical integration, such as Sartorius’ 2024 acquisition of a PES compounder, partially insulates top players; however, supply shocks remain a structural headwind for the laboratory filtration market.

Waste-Disposal Compliance Costs for Single-Use Plastics

Europe’s Waste Framework Directive amendments and several U.S. state laws impose extended producer responsibility fees on single-use plastics made from bioplastics. Disposal costs add 3–7¢ per liter of processed biologic, prompting CDMOs to consider reuse options. Suppliers counter with take-back programs that pelletize spent capsules for energy recovery, but logistics remain complex. Until harmonized guidelines emerge, compliance expenditures will clip near-term margin expansion in the laboratory filtration market.

Segment Analysis

By Product Type: Media Dominates, Accessories Surge on Automation

Filtration Media captured 57.31% of revenue in 2025, underscoring the centrality of membrane rolls, pleated cartridges, and capsule filters to every stage of bioprocessing. Commoditization of 0.22-µm discs compresses margins, so suppliers differentiate through hydrophilic coatings and charged layers that command 20% premiums. Filtration Accessories, though smaller in value, are forecast to expand at a 10.92% CAGR to 2031 as laboratories automate liquid handling. A single screening robot can process 10,000 syringe filters per day, making accessories the fastest-growing segment of the laboratory filtration market.

Media stays on top because each biologics batch consumes square meters of membrane, but accessories now drive incremental profit. Bundling precision filters with pipetting decks locks in aftermarket revenue and discourages third-party alternatives. Filtration Assemblies, which include plug-and-play capsules and tangential-flow skids, sit between the two extremes, winning favor at CDMOs that prioritize rapid tech transfer over bespoke engineering. The laboratory filtration market size for assemblies is poised to increase in line with the uptake of single-use products; however, its growth rate lags behind the accessory boom due to longer unit replacement cycles.

Note: Segment shares of all individual segments available upon report purchase

By Technique: Microfiltration Leads, Nanofiltration Gains on Viral Safety

Microfiltration held 39.68% of technique revenue in 2025, reflecting its versatility in clarifying harvests and ensuring sterile fill-finish. Standard 0.2-µm capsules are commodity items, but vendors now embed pressure sensors that feed real-time data into batch-record software, lifting the laboratory filtration market size by pairing hardware with analytics. Nanofiltration and reverse-osmosis units are expected to rise at a 9.54% CAGR as regulators demand additional viral-clearance barriers. A USD 1,500 disposable nanofilter that averts a USD 50 million contamination event is an easy sell, so nanofiltration’s value proposition transcends price.

Ultrafiltration tracks biologics output, concentrating proteins and exchanging buffers, yet its growth is steadier. Vacuum and depth filtration serve small-molecule QC and environmental labs where cost sensitivity caps ASPs. Hybrid techniques, such as electrofiltration, hover below a 5% share but command premium pricing because they shorten the downstream processing. The laboratory filtration market share mix will inch toward tighter-pore solutions as viral-safety culture spreads beyond monoclonals to vaccines and gene therapies.

By End User: Pharmaceutical & Biotechnology Labs Retain Leadership

Pharmaceutical & Biotechnology Companies generated 44.26% of 2025 revenue, as a single commercial monoclonal can burn through USD 3 million in membranes annually. GMP mandates ensure recurrent orders, and corporate QA departments prize suppliers that deliver lot traceability and change-control transparency. Academic & Research Institutes will rise at a 12.51% CAGR, helped by a 31% growth in NIH funding for infectious-disease and synthetic-biology labs between 2024 and 2025. University core facilities favor pre-sterilized accessories that bypass autoclave queues, aligning with the growing demand for accessories in the laboratory filtration market.

Food & Beverage Testing, along with Environmental Testing, accounts for approximately 18% of the value. EPA revisions to the Lead and Copper Rule lift water-testing volumes, but municipal budgets cap spending on premium filters. Forensic and petrochemical labs form a modest “Others” bucket, adopting filtration only when particle counts jeopardize analytical detection. The laboratory filtration industry thus straddles high-growth academic niches and stable industrial segments, with the pharmaceutical industry still anchoring absolute demand.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America held 36.24% revenue in 2025, backed by more than 1,200 GMP suites and the world’s densest cluster of cell-therapy developers. U.S. CDMOs trial next-generation membranes first, so suppliers channel pilot lots to local customers, reinforcing the region’s status as an early adopter. Canada’s vaccine initiative funnels grants into single-use, ready-to-pilot plants, expanding the pull of accessories.

The Asia-Pacific region is the growth engine, with an 11.63% CAGR projected through 2031. China licensed 47 biosimilar plants in 2024, and India approved 29 biologics facilities in 2025 that standardized on disposable trains to satisfy U.S. FDA export norms. Samsung Biologics and WuXi Biologics added over 400,000 L of capacity, selecting partners who can deliver within 48 hours. Japan retrofits stainless steel lines with hybrid single-use modules to reduce cleaning and validation downtime, spurring demand for capsule filters.

Europe expands steadily, driven by EMA guidance on continuous manufacturing, which heightens the need for inline filtration. Germany and Switzerland are pivoting to autologous CAR-T platforms, so each patient lot requires dedicated filters, which lifts per-lot spend by up to 50%. The United Kingdom’s post-Brexit convergence with EU standards eases supplier compliance. The Middle East & Africa are smaller today, yet Gulf states pledged USD 1 billion in 2025 for local biopharma, importing filtration assemblies until regional conversion plants emerge. South America’s Brazil and Argentina push vaccine self-reliance; Fiocruz opened a 50,000-L complex in 2025 fitted with tangential-flow disposables. Across all regions, greenfield facilities leapfrog to single-use, accelerating the adoption of premium capsules and assemblies in the laboratory filtration market.

Competitive Landscape

The top five vendors, Sartorius, Danaher (Cytiva & Pall), Merck KGaA, Thermo Fisher, and Repligen, control around a significant portion of global revenue, placing the laboratory filtration market in the mid-concentration band. Vertical integration distinguishes leaders: Sartorius owns membrane-casting lines and cleanrooms, enabling 48-hour ship times, while Danaher’s Cytiva-Pall combo spans upstream to final fill, making one-stop procurement viable. Merck embeds NFC tags in filters to automate lot traceability, extracting premiums of 12–15% as QA teams adopt digital batch records.

White space remains in nanoliter-scale filtration for organ-on-chip devices, where current syringe filters waste precious samples. Hybrid ceramic-polymer membranes that tolerate caustic cleaning also beckon; multiple MIT-licensed startups target the niche. Digital service add-ons differentiate challengers: a cloud integrity-test dashboard cut downtime by 18% at pilot users. Meanwhile, niche firms like Porvair and GVS thrive by focusing on sintered-polymer depth filters and serum-clarification pre-filters, product lines too small for global giants to prioritize.

Patent velocity is brisk; the USPTO granted 127 filtration patents in 2025, with 34% focused on low-binding surfaces and 28% on single-use integrity testing. Acquisitions also reshape the map: Repligen acquired Polymem in August 2025 to secure hollow-fiber capacity, while Thermo Fisher expanded its Singapore capsule plant to protect Asia's customer lead times. The laboratory filtration market, therefore, balances scale economies with innovation niches, encouraging both titans and newcomers to invest.

Laboratory Filtration Industry Leaders

Merck KgaA

Danaher Corporation

Sartorius AG

GVS S.p.A

3M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Agilent Technologies released Captiva Premium syringe filters featuring low-extractables PES membranes validated for LC-MS workflows

- February 2025: Porvair obtained ISO 13485 certification for its Vyon depth filters, widening access to medical-device OEMs.

- January 2025: Parker Hannifin launched the Balston Nexus integrity-test module, performing diffusion tests in under five minutes with Bluetooth data export.

- December 2024: GVS expanded its Maine cleanroom by 25,000 ft² to scale sterile syringe-filter output.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the laboratory filtration market as the sale of disposable and reusable media, assemblies, and accessories used to separate particulates from liquids or gases inside research, quality-control, and diagnostic laboratories. The valuation includes units supplied to pharmaceutical, biotechnology, academic, and clinical settings and is expressed in end-user spending terms. According to Mordor Intelligence analysts, this scope places the 2025 global market at USD 4.70 billion.

Exclusion: Industrial process filters, large-volume water or HVAC cartridges, and single-use bioprocess systems sold for commercial manufacturing are outside the frame.

Segmentation Overview

- By Product Type

- Filtration Media

- Filtration Assemblies

- Filtration Accessories

- By Technique

- Microfiltration

- Ultrafiltration

- Nanofiltration & Reverse Osmosis

- Vacuum / Depth Filtration

- Others

- By End User

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Food & Beverage Testing Laboratories

- Environmental Testing Laboratories

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Telephone interviews and short surveys with laboratory managers, quality officers at CRO/CDMOs, procurement heads in biotech start-ups, and regional distributors across North America, Europe, and Asia-Pacific validated usage intensity, replacement cycles, and emerging media preferences. These expert conversations filled gaps on discount structures and confirmed the relative uptake of nanofilters versus classic microfiltration membranes.

Desk Research

We first mapped the universe of laboratories by mining open datasets such as OECD Main Science & Technology Indicators, NIH RePORT, and Eurostat R&D expenditure tables. We then cross-checked filter import volumes on UN Comtrade and national customs dashboards. Standards documents from bodies such as the US USP, European Pharmacopeia, and WHO guidelines clarified regulatory drivers behind technology shifts. Company 10-Ks, investor decks, and conference proceedings supplied recent average selling prices and channel mixes. Paid repositories, such as D&B Hoovers for company sales trends and Dow Jones Factiva for real-time deal news, added depth. The sources cited are illustrative; numerous additional public and proprietary references supported data gathering and clarification.

Market-Sizing & Forecasting

A top-down reconstruction starts with the population of operational labs, applies penetration rates for each filtration technique, and pairs those volumes with region-specific ASPs, which are then stress-tested through selective bottom-up supplier roll-ups. Key inputs include active biotech pipeline counts, average R&D spend per bench scientist, lab automation adoption ratios, membrane throughput yields, and cartridge change-out norms. Multivariate regression links these drivers to historic sales, and scenario analysis adjusts for shifts in biologics funding or macroeconomic slowdowns. Where respondent data were thin, conservative interpolation bridged the gap before final reconciliation.

Data Validation & Update Cycle

Model outputs pass variance checks versus independent trade data, and anomalies trigger second-round expert calls. Senior Mordor reviewers sign off only after currency conversion parity and growth-rate sanity checks. The dataset refreshes annually, with interim adjustments if material events, such as supply disruptions or major capacity additions, arise.

Why Our Laboratory Filtration Baseline Inspires Confidence

Published market numbers rarely match because firms choose different product buckets, price benchmarks, and forecast cadences. Mordor's disciplined scope, dual-path modeling, and yearly refresh reduce those variances for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.70 Bn (2025) | Mordor Intelligence | |

| USD 4.10 Bn (2024) | Global Consultancy A | excludes accessories and assumes one global ASP |

| USD 3.61 Bn (2022) | Industry Association B | relies on historical sales only and limited regional coverage |

The comparison shows that narrower scopes, older base years, or uniform pricing explain most gaps, whereas Mordor's mixed-method approach and timely updates deliver a balanced, transparent baseline clients can trust.

Key Questions Answered in the Report

How large is the laboratory filtration market today?

The laboratory filtration market size is USD 5.01 billion in 2026 and is projected to reach USD 7.58 billion by 2031, growing at a 8.63% CAGR.

Which product category is growing fastest within laboratory filtration?

Filtration Accessories, such as precision syringe filters and microplate inserts, are projected to rise at a 10.92% CAGR through 2031.

What is driving nanofiltration adoption in biopharma labs?

Stricter viral-safety guidance from regulators now requires an extra 20-nm polishing step before final formulation, making nanofiltration indispensable despite higher consumable costs.

Why are academic labs becoming important filtration customers?

National grant programs for pandemic preparedness and synthetic biology have funded new BSL-3 suites and pilot plants, boosting academic demand at a 12.51% CAGR.

Which region offers the highest growth potential for suppliers?

The Asia-Pacific region, led by China, India, South Korea, and Japan, is expected to expand at a 11.63% CAGR as dozens of biosimilar and cell-therapy facilities come online.

Page last updated on: