Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

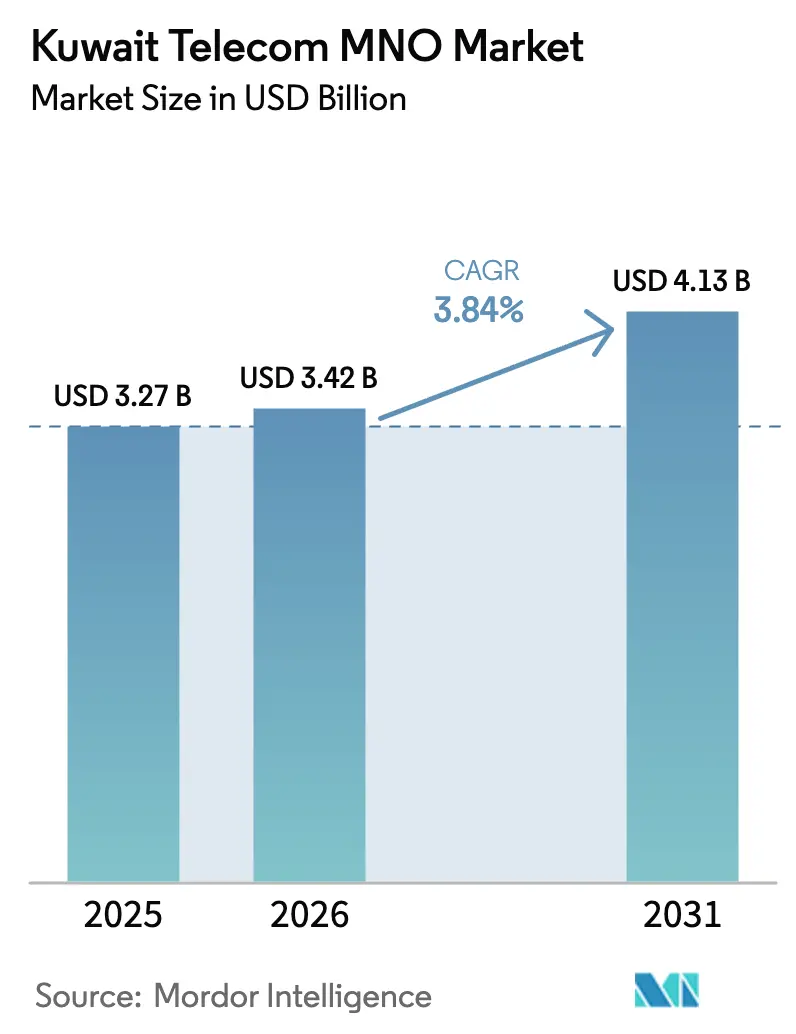

| Base Year Market Size (2025) | USD 3.27 Billion |

| Market Size (2026) | USD 3.42 Billion |

| Market Size (2031) | USD 4.13 Billion |

| Growth Rate (2026 - 2031) | 3.84% CAGR |

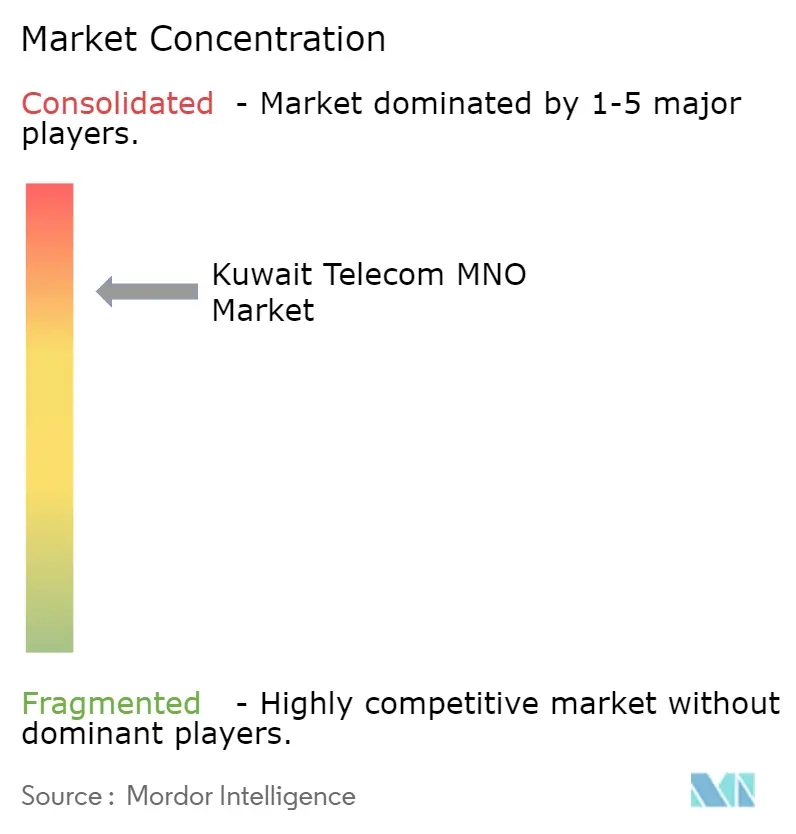

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kuwait Telecom MNO Market Analysis by Mordor Intelligence

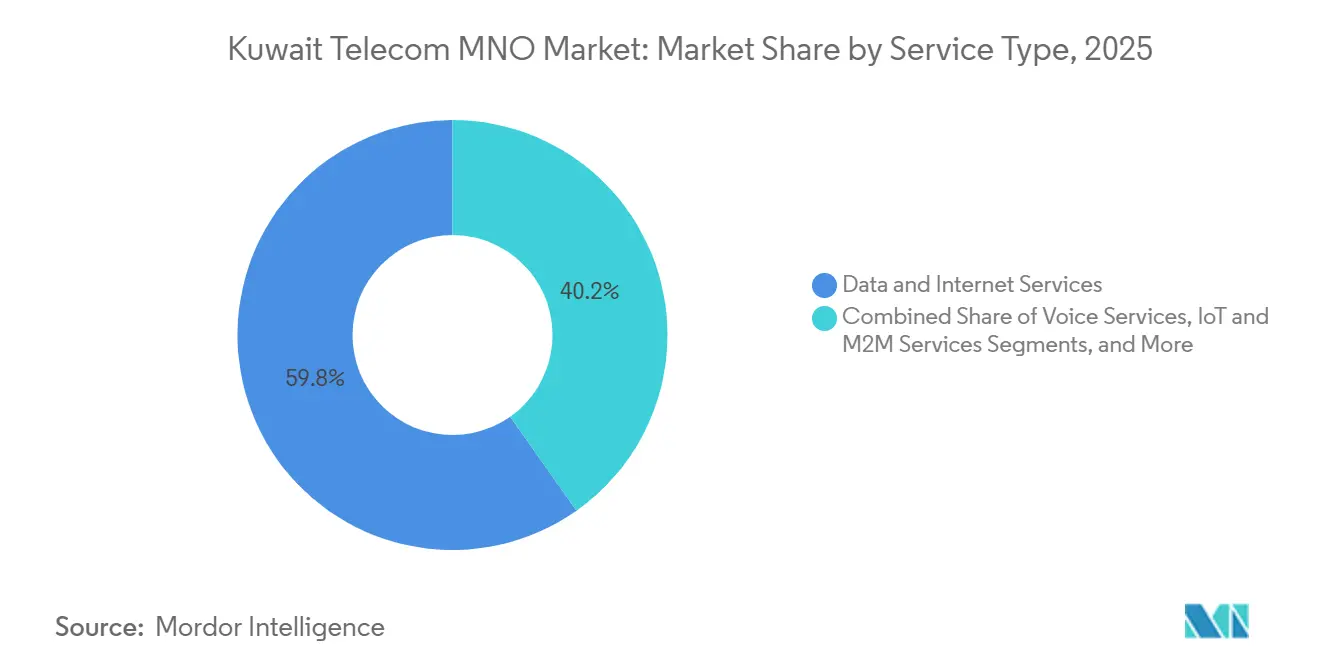

The Kuwait Telecom MNO market size is expected to increase from USD 3.27 billion in 2025 to USD 3.42 billion in 2026 and reach USD 4.13 billion by 2031, growing at a CAGR of 3.84% over 2026-2031. Mobile subscriber penetration stood above 181% in 2025, so revenue expansion now depends more on monetizing 5G standalone networks, network intelligence, and enterprise digitization than on adding new human connections. Operators are shifting capex toward 5G-Advanced features such as network slicing, edge computing, and artificial intelligence so they can sell low-latency, high-throughput connections for oil and gas automation, cloud gaming, and private campus networks. Data and Internet Services already accounted for 59.78% of revenue in 2025, but the fastest-growing line is cellular IoT that links machines, sensors, and vehicles. Government programmes under Kuwait Vision 2035, including an USD 800 million digital-oilfield plan, are accelerating demand for managed connectivity, cloud gateways, and cyber-secure private 5G, enlarging the commercial field for service providers.

Key Report Takeaways

- By service type, Data and Internet Services led with 59.78% Kuwait Telecom MNO market share in 2025. IoT and M2M Services are projected to expand at a 3.97% CAGR through 2031.

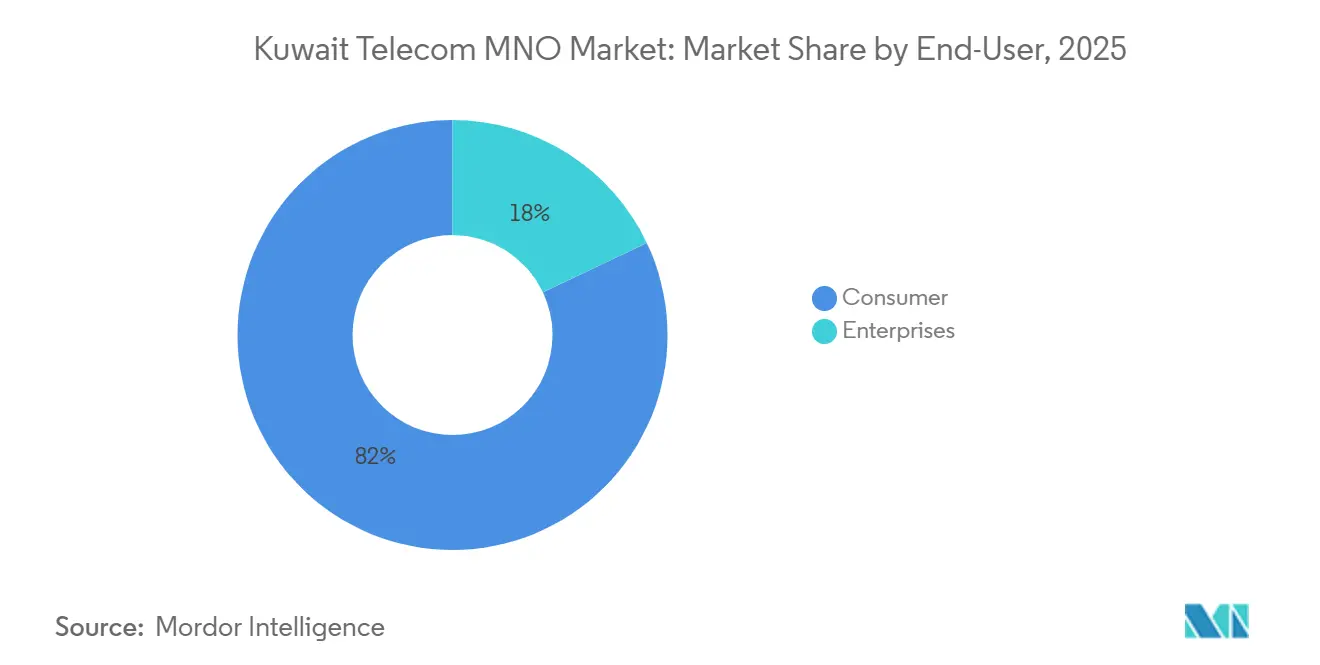

- By end user, the Consumer segment held 82.03% revenue in 2025. The Enterprise segment is forecast to grow at a 4.03% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kuwait Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercial Deployment of 5G Standalone | +1.2% | Capital Governorate and Ahmadi Governorate | Medium Term (2–4 Years) |

| Kuwait Vision 2035 Digital Infrastructure | +1.0% | Capital, Ahmadi, Jahra Governorate | Long Term (≥4 Years) |

| Rising Data Traffic from High Smartphone Use | +0.9% | Urban Districts Nationwide | Short Term (≤2 Years) |

| Growing Demand for Cloud Gaming and AR/VR | +0.6% | Kuwait City and Hawalli | Medium Term (2–4 Years) |

| Enterprise IoT in Oil and Gas and Logistics | +0.7% | Ahmadi and Shuwaikh Port | Medium Term (2–4 Years) |

| Regulatory Push for Infrastructure Sharing | +0.4% | Nationwide | Long Term (≥4 Years) |

| Source: Mordor Intelligence | |||

Commercial Deployment of 5G Standalone Networks Enabling Network Slicing

All three operators activated 5G standalone cores in 2025, giving them the ability to partition bandwidth into virtual slices that guarantee latency and throughput for distinct applications. stc Kuwait demonstrated sustained over-3 Gbps throughput, while an earlier Zain Kuwait test reached 10 Gbps peak speeds.[1]RCR Wireless News, “Zain Kuwait completes 5.5G test with Huawei,” rcrwireless.com The slicing function lets enterprises contract premium connectivity tiers for autonomous drilling rigs, remote robotics, or mission-critical video feeds, transforming the Kuwait Telecom MNO market from flat-rate data to outcome-based pricing. Ooredoo Kuwait’s partnership with NVIDIA adds edge inference to the connectivity bundle, showing how 5G slices and GPU instances can be sold together to serve generative-AI workloads.[2]Developing Telecoms, “Ooredoo teams with Nvidia to develop AI-ready platform for MENA,” developingtelecoms.com Success now relies on building domain-specific solutions teams, because equipment vendors alone cannot deliver vertical expertise.

Government Vision 2035 Investments in Digital Infrastructure

Vision 2035 earmarks multiyear funding for cloud data centers, smart-port logistics, and digital oilfield projects. CITRA’s land-lease with Google will bring a hyperscale zone that needs low-latency backhaul, providing fresh wholesale revenue for operators.[3]Communication and Information Technology Regulatory Authority, “CITRA announced 2024 marked exceptional successes,” citra.gov.kw ZainTECH and Microsoft placed ExpressRoute nodes in Kuwait during 2025, allowing ministries to procure private links that satisfy stringent data-residency requirements. Fiber build-outs financed by the Ministry of Communications feed 5G small-cell densification, while oil companies deploy thousands of LTE-M sensors that later migrate to 5G massive machine-type communication. These actions create a long-tail market for managed services, cybersecurity, and analytics that stretches beyond the connectivity fee, amplifying the growth arc of the Kuwait Telecom MNO market.

Rising Data Traffic From High Smartphone Penetration and Affordable Data Packages

Mobile data consumption continues to climb even though the subscriber base is saturated. Postpaid 5G internet bundles offer up to 1 TB for KWD 15 (USD 49), an affordability level that sits far below the United Nations two-percent-of-income threshold. Such low marginal cost stimulates video streaming, social media reels, and fixed-wireless substitution, prompting operators to upgrade spectrum utilization and deploy carrier aggregation. While headline traffic growth supports the capacity narrative, unlimited plans compress per-gigabyte yields, so operators pin revenue hopes on value-added layers including cloud storage, gaming passes, and insurer-backed cybersecurity apps. In practice, the Kuwait Telecom MNO market is shifting from volumetric billing toward a freemium model where content and digital-lifestyle bundles generate incremental margin.

Growing Demand for Cloud Gaming and Immersive AR/VR Applications

Consumer spending on immersive media hit USD 120 million in H1 2025, powered by low-latency 5G and high-resolution devices. Ooredoo’s ProPing plan prioritizes gaming packets to keep latency below 10 ms, illustrating how network quality can be productized. The GSMA expects 5G-Advanced multicast and satellite augmentation to remove bottlenecks for multiplayer sessions. Kuwait’s young, digitally native population clusters in Kuwait City and Hawalli, giving operators a concentrated but lucrative target market. Although the absolute contribution to revenue is modest today, the segment exerts strategic influence by pushing operators to deploy edge compute nodes and forge content distribution alliances, technologies that in turn underpin future enterprise propositions such as digital twins and remote training.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturated Mobile Subscriber Base | -0.8% | Nationwide | Short Term (≤2 Years) |

| Intensifying Price Competition Depressing ARPU | -0.6% | Nationwide | Short Term (≤2 Years) |

| Delayed 6 GHz Spectrum Availability | -0.3% | Nationwide | Medium Term (2–4 Years) |

| Revenue Volatility from Expatriate Policy Shifts | -0.4% | Ahmadi Governorate and Farwaniya Governorate | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Saturated Mobile Subscriber Base Exceeding 180 Percent Penetration

Multi-SIM ownership pushed penetration above 181% in 2025, meaning further unit growth is arithmetically limited.[4]nternational Telecommunication Union, “Measuring digital development: The affordability of ICT services 2024,” itu.int, International Telecommunication Union, “Data explorer - ITU DataHub,” itu.int Operators collectively serve about 7.8 million connections in a nation of roughly 4.3 million residents, amplifying churn management costs. Expatriate visas account for most prepaid churn, and any labour-policy tightening quickly erodes subscriber counts. To counter stagnation, carriers are building B2B salesforces and reskilling consumer teams to sell IoT bundles, but enterprise deal cycles stretch 9-18 months, delaying revenue lift for the Kuwait Telecom MNO market.

Intensifying Price Competition Driving Down ARPU

Unlimited 5G bundles priced between KWD 15 (USD 29) and KWD 20 (USD 65) slashed per-gigabyte charges in 2025. ITU surveys show that Kuwait’s mobile-data baskets cost less than 0.6% of monthly gross national income, positioning data as a commodity. Zain’s quarterly revenue stayed flat despite surging traffic, signalling that extra gigabytes do not translate into proportionate cash flow. Unless operators monetise differentiated services such as cyber-secure IoT or GPU edge compute, the Kuwait Telecom MNO market risks a profit squeeze.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: IoT Connectivity Gains as Voice and Messaging Plateau

Data and Internet Services dominated 2025 revenue, yet IoT and M2M traffic is set to post the strongest growth. Zain’s Global M2M platform lets industrial OEMs deploy a single International Mobile Subscriber Identity across multiple Middle East footprints, simplifying logistics while locking clients into long-term contracts. stc Kuwait’s fleet-management suite layers analytics and predictive maintenance on top of SIM connectivity, pushing average contract values higher. Voice and legacy SMS continue to decline as over-the-top apps capture interpersonal traffic. Operators cushion that erosion by bundling PayTV and streaming rights, but such add-ons are primarily churn-reduction tools rather than standalone growth engines. Regulatory cuts in termination rates further squeeze traditional minutes. As a result, IoT’s USD-per-bit economics look modest, yet its multiyear contract structure stabilises revenues and feeds demand for private 5G slices, strengthening the long-term profile of the Kuwait Telecom MNO market.

In fixed wireless access, 5G customer-premises equipment fills fibre gaps, particularly in newly built suburbs where civil works lag demand. Although still a sub-scale business, operators package FWA with unlimited plans, mesh Wi-Fi, and smart-home sensors, anchoring households that may eventually adopt paid cloud-storage or security monitoring. Other services, wholesale backhaul, interconnect, and Ethernet lines, offer steady cash flows, though CITRA’s drive to reduce international transit costs keeps price ceilings tight. Collectively, service-mix evolution underscores a pivot away from human voice toward machine-centric and platform-centric revenue, a defining change for the Kuwait Telecom MNO market.

By End User: Enterprise Segment Outpaces Consumer Despite Smaller Base

Consumer lines yielded 82.03% of 2025 revenue, but enterprise demand is rising fastest. Oil majors are digitising wells and refineries under an USD 800 million programme that depends on low-latency private 5G, geospatial analytics, and AI video surveillance. Logistics firms in Shuwaikh deploy IoT trackers that require persistent, low-power cellular links to meet customs and cold-chain regulations. Government agencies, spurred by data-sovereignty mandates, procure private ExpressRoute circuits through operator marketplaces, embedding telcos deeper in public-sector transformation. Although enterprise projects involve longer sales cycles and higher professional-services ratios, their gross margins are structurally richer than consumer prepaid bundles. Operators therefore funnel resources into solution-integration teams and partner ecosystems, including hyperscaler marketplaces and specialised system integrators. Over 2026-2031, enterprise accounts are forecast to absorb an expanding slice of capex, reshaping skill profiles and go-to-market strategies across the Kuwait Telecom MNO market.

For consumers, premium tiers remain important. Ooredoo’s gaming-optimized ProPing and Zain’s mesh Wi-Fi bundles aim to protect ARPU through experience differentiation rather than raw speed. Nonetheless, expatriate prepaid users remain price elastic, so operators segment offers by language, employment sector, and remittance-linked perks to mitigate churn. The result is a bifurcated market where mass consumer connectivity is a defensive play, while enterprise transformation offers the offensive growth vector.

Geography Analysis

Kuwait’s small landmass masks marked regional patterns that influence network rollout. The Capital Governorate hosts financial headquarters, ministries, and hyperscale data centers, prompting operators to prioritise dense small-cell grids and redundant fibre rings. 5G coverage exceeded 95% here by late 2025. Ahmadi, home to upstream oil operations, demands ultra-reliable low-latency links for drilling automation and environmental monitoring. Operators deploy hardened base stations with edge servers to satisfy these mission-critical needs. Jahra and Farwaniya contain larger expatriate communities and labour camps, yielding high prepaid SIM density but lower ARPU, so carriers rely on macro cells and sharing agreements to cap costs.

Internationally, Kuwait’s terrestrial corridor to Frankfurt through Iraq lowers latency to European cloud zones, an important advantage as ministries migrate workloads. Cross-border IoT roaming is also vital: Zain’s Global M2M lets freight trucks move from Kuwait through Saudi Arabia to Bahrain without SIM swaps, cutting logistics downtime. Ooredoo’s regional GPU fabric allows Kuwaiti developers to burst AI workloads into Qatar or Tunisia when local capacity peaks, underscoring how regional infrastructure enhances domestic service value.

Spectrum policy shapes future growth. While operators utilise the 3.5 GHz band for 5G, CITRA has yet to release contiguous 6 GHz blocks, constraining mid-band capacity. Consequently, carrier aggregation with 2.6 GHz and millimetre wave trials becomes essential for handling surges in cloud gaming and extended-reality traffic around stadiums and shopping malls. The regulatory push for passive-infrastructure sharing yields nationwide tower-pooling deals, but active-network differentiation remains, so carriers concentrate beamforming and massive-MIMO upgrades in high-traffic urban cells. Altogether, geography affects both the cost profile and revenue focus of the Kuwait Telecom MNO market, not by provincial licensing differences but by economic-activity clusters and spectrum policy.

Competitive Landscape

The Kuwait Telecom MNO market is an oligopoly with three licensees sharing 100% of subscribers. Zain Kuwait, stc Kuwait, and Ooredoo Kuwait each claim roughly one-third of the market, but differentiation goes beyond headcount. Zain leverages its regional presence to sell cross-border IoT, and its ExpressRoute partnership positions it as a hybrid-cloud gateway for ministries. stc concentrates on 5G-Advanced benchmarks, marketing 3-Gbps speeds and low-latency slices to industrial automation clients. Ooredoo’s tie-up with NVIDIA turns its network into a GPU-rich edge-cloud, letting enterprises train models locally to meet data-residency laws.

Capital allocation trends show rising software and data-center investment relative to radio access gear. All incumbents reported double-digit year-on-year jumps in IT capex during 2025, while radio upgrades plateaued after nationwide 5G coverage completion. Strategic deals include tower-company carve-outs and sale-leasebacks that free balance-sheet capacity for cloud and AI ventures. Competitive threats come less from new telco entrants and more from hyperscalers. Google’s land-lease data-center plan, Microsoft’s ExpressRoute nodes, and Amazon Web Services’ Outposts pilots could bypass carrier networks by integrating satellite backhaul. In anticipation, carriers join GSMA Open Gateway to expose quality-on-demand, device-location, and SIM-swap APIs, hoping to embed telco functions into developer workflows and thus keep a share of digital-platform value.

Regulation maintains high entry barriers. New full-band mobile licences are unlikely, but private spectrum for factory or campus networks could emerge, letting oil majors run self-managed 5G. If such licensing materialises, incumbents will compete as managed-service providers rather than exclusive spectrum holders. Overall, consolidation remains steady, yet strategic horizons extend toward platform economics and API marketplaces, redefining what counts as competitive advantage inside the Kuwait Telecom MNO market.

Kuwait Telecom MNO Industry Leaders

Zain Kuwait (Mobile Telecommunications Company K.S.C.P.)

stc Kuwait (Kuwait Telecommunications Company K.S.C.P.)

Ooredoo Kuwait

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ITRA posted KD 75 million (USD 243.4 million) revenue for H1 FY 2024-2025 and finalized a land-lease agreement with Google for hyperscale data centers.

- December 2025: The Central Agency for Public Tenders awarded KD 2.022 million (USD 6.6 million) contract for a nationwide smart-meter communications network.

- October 2025: ZainTECH, Zain Kuwait and Zain Omantel International listed Microsoft Azure ExpressRoute in the Kuwait Azure Marketplace.

- September 2025: Knetco became implementation partner for Huawei 5G-Advanced upgrades across all three Kuwaiti operators.

- June 2025: stc Kuwait commercially launched 5G-Advanced services delivering speeds above 3 Gbps.

Kuwait Telecom MNO Market Report Scope

Telecom or Telecommunication is the long-range transmission of information by electromagnetic means.

The Kuwait Telecom MNO Market Report is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, IoT and M2M Services, OTT and PayTV Services, and Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, Rest of Service Type)), End-User (Enterprises, and Consumer), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services) |

End-User

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What revenue did the Kuwait Telecom MNO market generate in 2025?

It recorded USD 3.27 billion in 2025, with forecasts pointing to USD 4.13 billion by 2031.

Which segment is growing fastest?

IoT and M2M Services, projected to post a 3.97% CAGR through 2031.

How many mobile network operators serve Kuwait?

Three licensed operators, Zain Kuwait, stc Kuwait, and Ooredoo Kuwait, cover 100% of connections.

Why is ARPU under pressure?

Unlimited 5G bundles priced at KD 15-20 per month intensified price competition, lowering per-user yields.

What government program most boosts enterprise demand?

Kuwait Vision 2035, particularly the USD 800 million digital-oilfield initiative that relies on private 5G and IoT.

How does 5G-Advanced support new services?

Network slicing and edge computing enable guaranteed low-latency links for applications such as cloud gaming and autonomous machinery.

Page last updated on: