Market Size of Korea Semiconductor Device Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

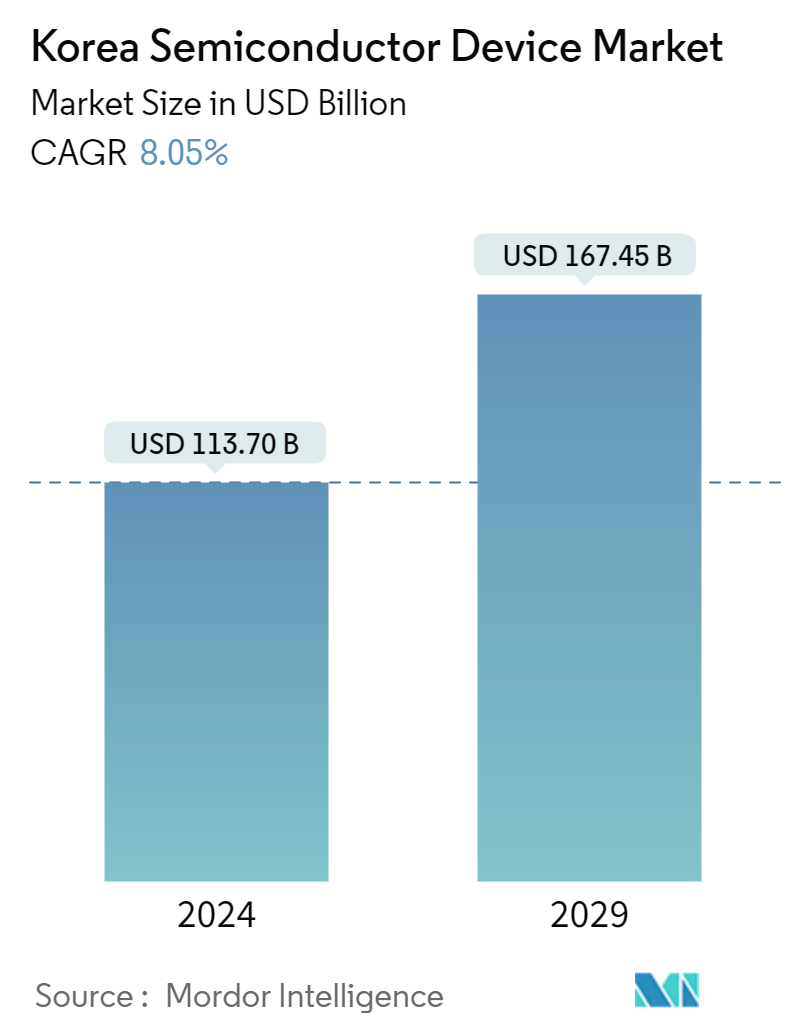

| Market Size (2024) | USD 113.70 Billion |

| Market Size (2029) | USD 167.45 Billion |

| CAGR (2024 - 2029) | 8.05 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Korea Semiconductor Device Market Analysis

The Korea Semiconductor Device Market size is estimated at USD 113.70 billion in 2024, and is expected to reach USD 167.45 billion by 2029, growing at a CAGR of 8.05% during the forecast period (2024-2029).

- The increasing demand for semiconductor devices from the electronics and automotive industries is expected to contribute significantly to revenue generation in the coming years; however, a shortage of skilled labor-intensive tasks may impede industry expansion in the coming years.

- The South Korean Government is taking several steps to strengthen its semiconductor landscape. For instance, in 2022, the Ministry of Trade, Industry, and Energy announced that chip exports are anticipated to double to USD 200 billion by 2030.

- Further, the Korean Government seeks to build a "K-Semiconductor belt" that stretches several kilometers south of Seoul and brings together chip designers, manufacturers, and suppliers. These plants are aimed to sharpen South Korea's competitive edge in the global semiconductor industry as well as localize primary semiconductor materials and equipment supplies with key semiconductor companies and their suppliers working in clusters in the midst of a global chip shortage.

- In Sep 2022, the South Korean Government announced several strategies to boost its automotive industry, including South Korea to invest KRW 95 trillion in the automobile industry over the next five years. The Government plans to produce 3.3 million electric vehicles by 2030.

- In March 2023, South Korea unveiled plans to utilize USD 234 billion in private investment to create the world's largest semiconductor cluster in the Seoul metropolitan area. The cluster would be located in the Gyeonggi province and completed by 2042. The cluster would be located in the Gyeonggi province and completed by 2042. South Korea's Trade and Industry Ministry also revealed its plans to build five high-tech semiconductor factories and attract up to 150 sub-manufacturers and fabless companies.

- Moreover, in August 2022, Hyundai Motor Group of South Korea announced that it had opted to develop its own automotive semiconductors. Hyundai Mobis, the automaker's car components business, is now ramping up its efforts to manufacture its own semiconductors. The move is considered part of a strategy to deal with the concerns of semiconductor supply shortages, which have made internal semiconductor production more critical than ever before, especially with the shift to electric vehicles. Such developments would offer lucrative opportunities for the market players.

- On the flip side, the semiconductor industry is considered to be one of the most complex industries, not only due to over 500 processing steps involved in the manufacturing and several products but also the harsh environment it faces, for instance, the volatile electronic market and the unpredictable demand.

- Depending on the complexity of the manufacturing process, there can be around 1,400 process steps in the overall manufacturing of semiconductor wafers alone. Transistors are formed on the lowest layer, but the process is repeated as numerous layers of circuits are formed to create the final product. The complexity of manufacturing semiconductor devices is likely to restrain the growth of the studied market.

- Further, according to the Korea Automotive Technology Institute or Katech, the global shortage of automotive semiconductors that started around the end of the year 2020 continued to affect the global car industry for the first half of the year 2022. Even after 2023, some companies may still feel its effects.

Korea Semiconductor Device Industry Segmentation

A semiconductor device is an electronic component that relies on the electronic properties of semiconductor material for its function.

The Korean semiconductor device market is segmented by device type (discrete semiconductors, optoelectronics, sensors, integrated circuits (analog, logic, memory, micro (microprocessors, microcontrollers, digital signal processors)), by end-user vertical (automotive, communication (wired and wireless), consumer, industrial, computing/data storage).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Device Type | ||||||||||

| Discrete Semiconductors | ||||||||||

| Optoelectronics | ||||||||||

| Sensors | ||||||||||

|

| By End-user Vertical | |

| Automotive | |

| Communication (Wired and Wireless) | |

| Consumer | |

| Industrial | |

| Computing/Data Storage |

Korea Semiconductor Device Market Size Summary

The Korean semiconductor device market is poised for significant growth, driven by increasing demand from the electronics and automotive sectors. The government's proactive measures, such as the establishment of the "K-Semiconductor belt" and substantial investments in semiconductor clusters, aim to enhance South Korea's competitive position in the global market. These initiatives are designed to localize semiconductor production and supply chains, addressing the ongoing global chip shortage. The automotive industry's shift towards electric vehicles further fuels the demand for semiconductors, with companies like Hyundai Motor Group investing in in-house semiconductor production to mitigate supply chain vulnerabilities. Despite these positive trends, the industry faces challenges, including a shortage of skilled labor and the complex, multi-step manufacturing processes that could hinder market expansion.

The market is characterized by a diverse range of applications, from discrete semiconductors used in power management and consumer electronics to advanced semiconductor technologies supporting smart manufacturing and Industry 4.0 initiatives. The integration of digital and physical manufacturing processes, along with the rise of industrial robots, is transforming the Korean industrial landscape, driving demand for semiconductor devices. Companies such as SK Hynix and Samsung Electronics are making significant investments in new fabrication plants and cutting-edge technologies to maintain their market leadership. The market's fragmentation is evident with major players like Intel, NXP Semiconductors, and Toshiba actively pursuing strategic partnerships and technological advancements. These developments, coupled with the government's support for small and medium-sized enterprises, are expected to sustain the market's growth trajectory in the coming years.

Korea Semiconductor Device Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Threat of New Entrants

-

1.2.4 Intensity of Competitive Rivalry

-

1.2.5 Threat of Substitutes

-

-

1.3 Technological Trends

-

1.4 Value Chain Analysis

-

1.5 Assessment of Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Device Type

-

2.1.1 Discrete Semiconductors

-

2.1.2 Optoelectronics

-

2.1.3 Sensors

-

2.1.4 Integrated Circuits

-

2.1.4.1 Analog

-

2.1.4.2 Logic

-

2.1.4.3 Memory

-

2.1.4.4 Micro

-

2.1.4.4.1 Microprocessors (MPU)

-

2.1.4.4.2 Microcontrollers (MCU)

-

2.1.4.4.3 Digital Signal Processors

-

-

-

-

2.2 By End-user Vertical

-

2.2.1 Automotive

-

2.2.2 Communication (Wired and Wireless)

-

2.2.3 Consumer

-

2.2.4 Industrial

-

2.2.5 Computing/Data Storage

-

-

Korea Semiconductor Device Market Size FAQs

How big is the Korea Semiconductor Device Market?

The Korea Semiconductor Device Market size is expected to reach USD 113.70 billion in 2024 and grow at a CAGR of 8.05% to reach USD 167.45 billion by 2029.

What is the current Korea Semiconductor Device Market size?

In 2024, the Korea Semiconductor Device Market size is expected to reach USD 113.70 billion.