Jeddah Commercial Real Estate Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

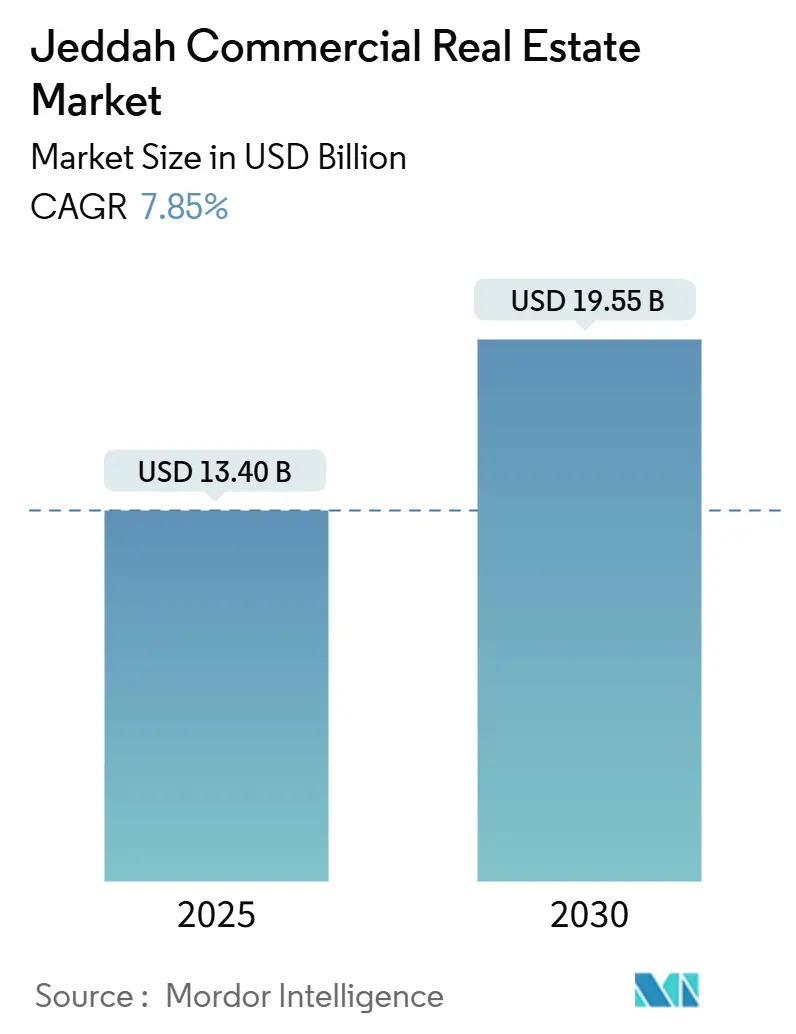

| Market Size (2025) | USD 13.40 Billion |

| Market Size (2030) | USD 19.55 Billion |

| Growth Rate (2025 - 2030) | 7.85% CAGR |

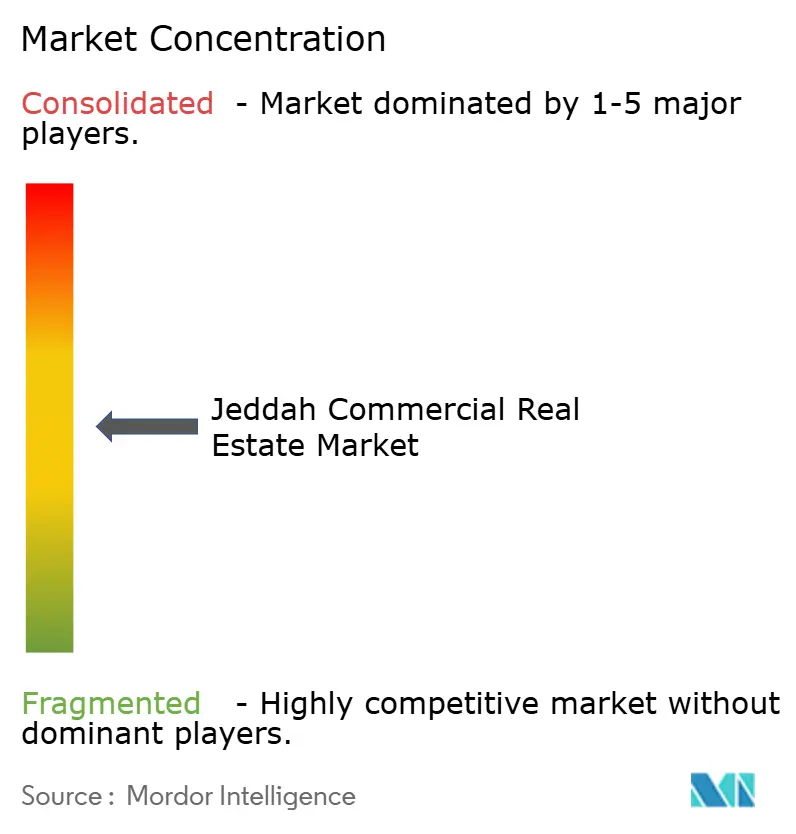

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Jeddah Commercial Real Estate Market Analysis by Mordor Intelligence

The Jeddah Commercial Real Estate Market size stood at USD 13.40 billion in 2025 and is projected to reach USD 19.55 billion by 2030, advancing at a 7.85% CAGR. The expansion rests on Vision 2030-aligned infrastructure outlays, a widening logistics footprint anchored by Jeddah Islamic Port, and ongoing capital-market reforms that channel institutional funds into income-generating assets. Elevated demand for Grade-A offices, a surge in logistics parks, and sustained hospitality openings underscore resilient occupier fundamentals, while REIT listings, foreign-ownership liberalization, and green-building mandates collectively deepen the investment pool. Developers increasingly pursue mixed-use formats featuring retailtainment, coworking, and lifestyle amenities, which bolster rental premiums and elevate absorption rates amid intensifying digitalization. Infrastructure megaprojects—among them the SAR 75 billion (USD 20 billion) Jeddah Central development are reshaping land values across the waterfront and peripheral districts, positioning the Jeddah commercial real estate market as a pivotal gateway for regional trade and tourism.

Key Report Takeaways

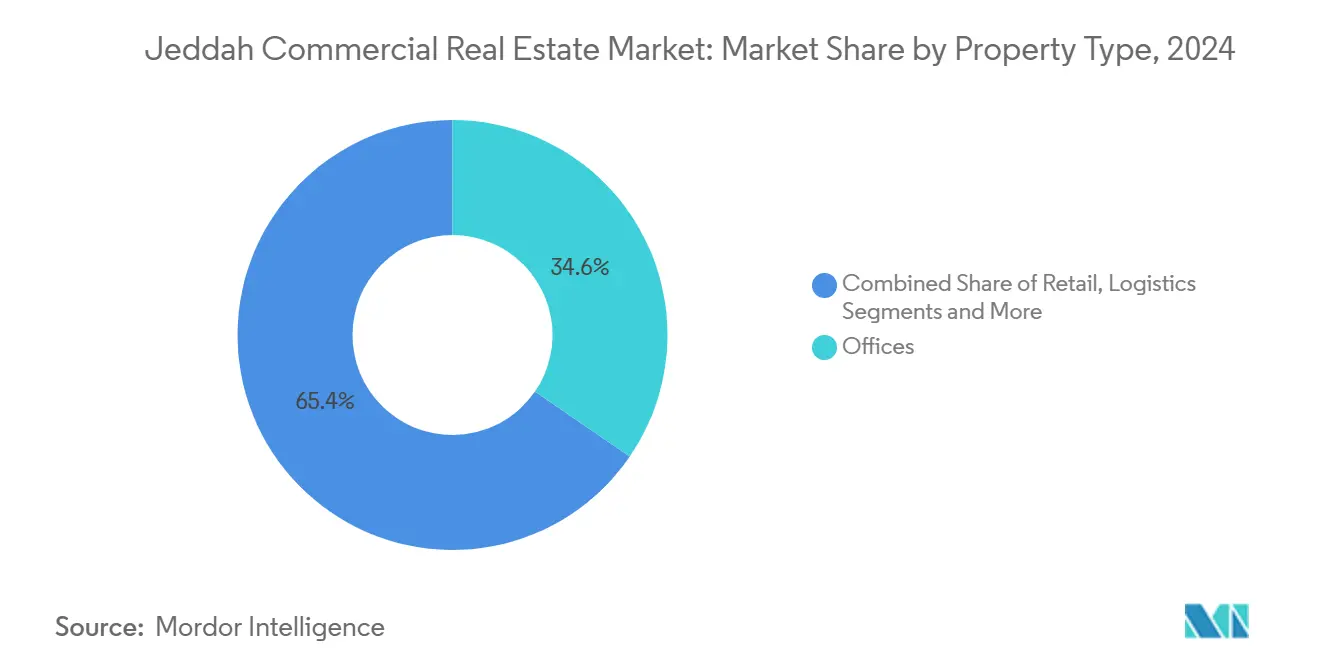

- By property type, offices led with 34.56% of Jeddah commercial real estate market share in 2024, while logistics facilities are forecast to expand at a 9.43% CAGR to 2030.

- By business model, rental operations held 68.98% share of the Jeddah commercial real estate market size in 2024; investment sales are projected to grow at 8.30% CAGR through 2030.

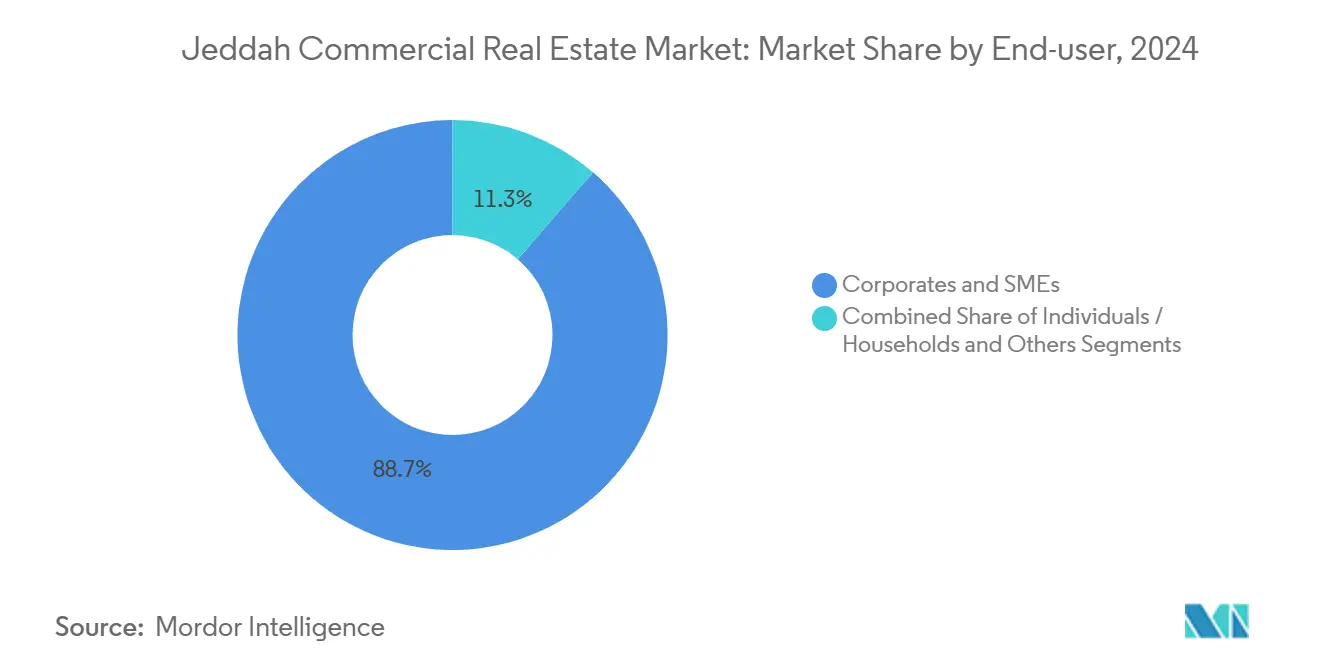

- By end-user, corporates and SMEs accounted for 88.67% of demand in 2024, whereas individual and household purchases are advancing at a 9.03% CAGR to 2030.

- By geography, the Central Business District commanded 34.56% share of the Jeddah commercial real estate market in 2024, yet the Rest of Jeddah zone is poised for the fastest 8.83% CAGR through 2030.

Jeddah Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 infrastructure spending & economic diversification | 2.8% | Global, with primary focus on Jeddah Central and waterfront districts | Long term (≥ 4 years) |

| Jeddah Islamic Port expansion boosting logistics space | 2.1% | Port-adjacent areas, logistics corridors, industrial zones | Medium term (2-4 years) |

| Tourism-driven hospitality demand surge | 1.8% | Jeddah waterfront, Al Balad historic district, corniche areas | Short term (≤ 2 years) |

| REIT-led capital-market deepening | 1.5% | National, with early gains in Riyadh, Jeddah, Eastern Province | Medium term (2-4 years) |

| Digitalisation & smart-building retrofits | 1.2% | Urban centers, concentrated in CBD and North Jeddah | Medium term (2-4 years) |

| Flexible workspace uptake by SMEs post-COVID | 0.9% | Central Business District, mixed-use developments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Infrastructure Spending & Economic Diversification

Unprecedented national outlays topping USD 850 billion in giga-projects anchor Jeddah’s transformation into a diversified commercial hub. The SAR 75 billion (USD 20 billion) Jeddah Central Project alone spans 5.7 million m², dedicating 45% to green space and introducing 17,000 residential units, 2,700 hotel keys, and an opera house that elevate downtown’s investment profile. With 45% completion targeted for 2027, the project is forecast to add SAR 47 billion (USD 12.5 billion) to GDP by 2030 and generate 25,000 jobs. Complementary schemes, such as the SAR 1.3 billion (USD 345 million) Maersk-led logistics zone at Jeddah Islamic Port, will compound demand for Grade-A warehouses, offices, and hospitality assets. These capital injections, coupled with eased foreign-investment rules, underpin the long-term uplift in the Jeddah commercial real estate market.

Jeddah Islamic Port Expansion Boosting Logistics Space

DP World’s SAR 900 million (USD 240 million) logistics park, integrated customs zones, and berth deepening collectively raise container capacity and drive a 9.43% CAGR in logistics floor space. Port-proximate warehouses with 15-meter clear heights and cold-chain fit-outs now command rental premiums of 12% over inland facilities, pushing developers to fast-track speculative builds. The logistics-led uplift radiates into industrial corridors, reinforcing the growth path of the Jeddah commercial real estate market.

Tourism-Driven Hospitality Demand Surge

Luxury supply is scaling rapidly as operators position ahead of the Kingdom’s 100 million-visitor goal. The Jeddah EDITION debuted in May 2024, and IHG has signed Holiday Inn Jeddah Al Naseem and Regent Jeddah for openings through 2026. Heritage conversions in Al Balad will deliver 34 boutique hotels by 2027, combining cultural preservation with diversified revenue streams. These assets capture rising leisure arrivals and spillover demand from MICE events, lifting hotel-linked retail and F&B footfall.

REIT-Led Capital-Market Deepening

Saudi Arabia’s REIT regime, refined since 2016, channels patient capital into stabilized assets and broadens investor accessibility. A pending USD 700 million King Abdullah Financial District REIT and Arabian Centres’ two funds totaling SAR 6.2 billion (USD 1.65 billion) exemplify heightened institutional appetite. Regulations mandating 75% asset deployment into developed properties enhance transparency, while the February 2025 Investment Law abolishes licensing barriers for foreign investors. Together, these frameworks compress funding costs, stimulate development pipelines, and fortify secondary-market liquidity—bolstering valuations across the Jeddah commercial real estate market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Materials & skilled-labour shortages | -1.8% | National, with acute impacts in mega-project zones | Short term (≤ 2 years) |

| Complex regulatory approvals & permitting delays | -1.2% | Municipal jurisdictions, concentrated in CBD and waterfront areas | Medium term (2-4 years) |

| Potential Grade-A office oversupply from mega-projects | -0.9% | Central Business District, North Jeddah business zones | Long term (≥ 4 years) |

| Rising flood-mitigation & climate-adaptation costs | -0.7% | Coastal developments, Red Sea waterfront properties | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Materials & Skilled-Labour Shortages

Saudi Arabia’s USD 850 billion construction pipeline strains supply chains, inflating steel and cement prices by up to 20% annually and extending project schedules by 6-12 months. A USD 1.5 trillion reservoir of unawarded MENA projects compounds procurement risks. Although Saudization lowered national unemployment to 7% in 2024, wage escalation persists, pressuring developer margins. Adoption of AI-enabled scheduling and robotics-assisted fabrication is estimated to lift productivity 20-30%, partly offsetting inflationary drag[1]Global Arbitration Review, “Saudi Construction Pipeline Faces Supply Chain Constraints,” globalarbitrationreview.com.

Complex Regulatory Approvals & Permitting Delays

Even with one-stop digital portals, environmental studies and municipal clearances can stretch timelines by up to six months, especially along the flood-prone waterfront. Introduction of a 5% Real Estate Transaction Tax in April 2025 adds documentation layers and cash-flow implications for disposals. Payment lags of 45-60 days on public projects further disrupt contractor liquidity, accentuating delivery uncertainty across the Jeddah commercial real estate market.

Segment Analysis

By Property Type: Offices Dominate While Logistics Accelerates

Office assets retained a commanding 34.56% Jeddah commercial real estate market share in 2024, buoyed by Vision 2030’s regional headquarters requirement that compels multinationals to establish Saudi bases. Prime CBD rents climbed 9.5% in 2024 as occupancy breached 92%, reinforcing investor appetite for core projects and supporting steady escalation clauses. Two-tier dynamics persist, with Grade-B stock discounting 18% to lure start-ups and back-office tenants. Landlords differentiate via wellness certifications and touch-free access, which can secure rental premiums of 7%. Complementary retailtainment and F&B podiums elevate dwell times and diversify income streams, embedding mixed-use vitality into office precincts.

Conversely, logistics facilities are positioned for the fastest 9.43% CAGR through 2030, thanks to DP World’s SAR 900 million (USD 240 million) park, Maersk’s SAR 1.3 billion (USD 345 million) zone, and Ministry of Transport’s USD 106.6 billion national logistics strategy. Demand for 15-meter-clear warehouses, cold-chain units, and bonded storage surges as e-commerce penetration tops 25% of retail sales. Build-to-suit agreements with 10-year leases anchor financing, while yield compression attracts global pension funds into sale-and-lease-back deals. Together, these trends reinforce the long-term volume and value proposition of the Jeddah commercial real estate market.

Note: Segment shares of all individual segments available upon report purchase

By Business Model: Rental Strength With Sales Momentum

Rental operations controlled 68.98% share of the Jeddah commercial real estate market size in 2024, underpinned by stable cash flows and REIT eligibility. Prime offices delivered net yields of 6-7%, edging regional comparables and luring cross-border capital. Lease tenures average 3-5 years with 5% annual escalations, while hospitality management contracts stretch 15-20 years with revenue-sharing overlays. Institutional landlords deploy AI-based asset-management suites to optimize occupancy and reduce operating costs 12%. The combination of resilient occupancies and enhanced transparency keeps the rental model a preferred strategy for risk-averse investors.

The sales segment, though smaller, is expanding at 8.30% CAGR through 2030, catalyzed by the January 2026 foreign-ownership liberalization and improved mortgage-financing options. Off-plan purchases under the Wafi program surged 28% in 2024, while strata-law reforms unlock pooled ownership in high-rises. Developers incorporate fixed-price exit clauses, enabling retail investors to lock in capital gains upon project completion. As a result, the ownership path gains traction among high-net-worth individuals seeking exposure to the Jeddah commercial real estate market.

By End-User: Corporates Rule, Households Accelerate

Corporates and SMEs generated 88.67% of end-user activity in 2024, propelled by 31% year-over-year growth in SME lending to SAR 383.2 billion (USD 102 billion). Multinationals pre-lease contiguous floors, while SMEs prefer flex-space modules, sharpening space-planning flexibility. Government-backed incubators such as the Social Development Bank’s Jada30 support 245 enterprises and nurture demand for managed offices, labs, and showrooms. Coworking operators integrate plug-and-play meeting pods and cloud-based access to entice start-ups, ensuring robust occupancy pipelines in the Jeddah commercial real estate market.

The individual and household bracket is forecast to grow at a 9.03% CAGR through 2030, aligned with the Premium Residency scheme for properties over SAR 4 million (USD 1.06 million). Branded residences atop hotels and waterfront mixed-use towers appeal to expatriate executives seeking on-site amenities, diversifying buyer profiles. Crowdfunding platforms trial fractional ownership offerings, lowering entry thresholds and expanding retail investor participation.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The Central Business District held a 34.56% slice of the Jeddah commercial real estate market in 2024, supported by the UNESCO-listed Al Balad quarter and the SAR 75 billion (USD 20 billion) Jeddah Central project that elevates downtown’s skyline with cultural icons and 2,700 hotel rooms. Corporate clustering around Tahlia Street and King Road sustains above-market rents and catalyzes transit-oriented redevelopment along mass-transit corridors. Operator-managed parking hubs and pedestrian enhancements strengthen asset competitiveness, driving value appreciation[2]Jeddah Economic Company, “Jeddah Economic City Progress Update 2025,” jec.sa.

North Jeddah, encompassing Obhur and the North Corniche, benefits from proximity to King Abdulaziz International Airport and the 5.3 million-m² Jeddah Economic City, which integrates smart grids and district cooling. Hospitality pipelines, including the Regent Jeddah and branded residences, buttress mixed-use demand while logistics tenants favor the King Abdullah Economic Zone corridor for multimodal connectivity. Infrastructure synergies heighten land uptake, positioning the sub-market for mid-single-digit rental growth.

The Rest of Jeddah zone is poised for the fastest 8.83% CAGR through 2030 as peripheral districts absorb spillover demand from mega-projects. ROSHN’s ALAROUS community will deliver 2,200 homes and integrated commercial strips, enhancing livability outside heritage cores. Simultaneously, the 9.5-kilometer waterfront promenade integrates marinas, an opera house, and public beaches, aligning with Vision 2030’s leisure goals and amplifying tourism footfall. Special Economic Zones confer tax incentives and expedited permitting, attracting manufacturing, data-center, and logistics investors into formerly under-capitalized plots, further broadening the breadth of the Jeddah commercial real estate market.

Competitive Landscape

Market leadership remains moderately concentrated, with Emaar Economic City, Jeddah Economic Company, and Dar Al Arkan leveraging government partnerships and robust land banks to deliver giga-projects. These incumbents adopt phased financing structures and establish build-operate-transfer joint ventures with public entities to de-risk execution. ROSHN’s 2024 rebrand signaled a pivot from purely residential to multi-asset development, unlocking synergies in retailtainment and hospitality that diversify revenue and extend project life cycles.

Technology has become a decisive differentiator. King Abdullah Financial District’s deployment of IBM Maximo spans 100,000 digitalized assets and lifts tenant satisfaction to 95%. Taiba Investments’ collaboration with Horizontal Digital embeds AI-driven yield optimization across 7,700 guest rooms, illustrating the shift toward data-guided portfolio management. Logistics players integrate solar rooftops and hydrogen-ready systems, responding to institutional investors’ ESG screens.

New entrants—ranging from PropTech startups exploring tokenized ownership to regional private-equity firms—gain traction by targeting niche asset classes such as refrigerated warehouses and student housing. Venture-capital infusions projected at USD 2 trillion over the coming decade seed disruptive models that chip away at incumbent dominance. Nonetheless, high land costs and evolving regulatory templates temper fragmentation, keeping the Jeddah commercial real estate market in the mid-range on the concentration spectrum[3]BECO Capital, “MENA PropTech Investment Outlook 2030,” becocapital.com.

Jeddah Commercial Real Estate Industry Leaders

Emaar Economic City

Jeddah Economic Company

Dar Al Arkan Real Estate Development Company

Jabal Omar Development Company

Red Sea Global

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: IHG Hotels & Resorts and Ashaad Company announced three new hotel signings across Jeddah and Al Khobar during the Future Hospitality Summit Riyadh 2025, adding over 1,700 rooms to IHG's portfolio with openings scheduled between 2028-2030, supporting Saudi Vision 2030's tourism expansion goals.

- March 2025: Diriyah Company advanced discussions with Alshaya Group and Starbucks to establish a flagship store within the 14 square kilometer mixed-use development featuring 566,000 square meters of retail and F&B offerings, targeting over 100,000 residents and visitors.

- November 2024: ROSHN Group rebranded, broadening its mandate to retail, commercial, and hospitality across 4 million m² GLA

- July 2024: The Public Investment Fund launched Al Balad Development Company to overhaul Jeddah’s historic district across 2.5 million m²

Jeddah Commercial Real Estate Market Report Scope

Commercial real estate (CRE) refers to non-residential property that serves to generate income. This includes shopping malls, hotels, and office spaces.

A complete background analysis of Jeddah’s commercial real estate market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

Jeddah’s commercial real estate market is segmented by type (offices, retail, industrial, logistics, multi-family, and hospitality). The report offers market size and forecasts for Jeddah’s commercial real estate market in value (USD) for all the above segments.

| Offices |

| Retail |

| Logistics |

| Others (industrial real estate, hospitality real estate, etc.) |

| Sales |

| Rental |

| Individuals / Households |

| Corporates & SMEs |

| Others |

| North Jeddah (Obhur, North Corniche) |

| Central Business District (Al Balad, Tahlia) |

| Waterfront Developments (Jeddah Waterfront, Corniche) |

| Rest of Jeddah |

| By Property Type | Offices |

| Retail | |

| Logistics | |

| Others (industrial real estate, hospitality real estate, etc.) | |

| By Business Model | Sales |

| Rental | |

| By End-user | Individuals / Households |

| Corporates & SMEs | |

| Others | |

| By Geography | North Jeddah (Obhur, North Corniche) |

| Central Business District (Al Balad, Tahlia) | |

| Waterfront Developments (Jeddah Waterfront, Corniche) | |

| Rest of Jeddah |

Key Questions Answered in the Report

How large is the Jeddah commercial real estate market in 2025?

It is valued at USD 13.40 billion and is on track for a 7.85% CAGR to 2030.

Which property type holds the largest share in Jeddah?

Offices lead with 34.56% share, fueled by the regional headquarters initiative.

What is the fastest-growing segment?

Logistics real estate is expanding at a 9.43% CAGR, assisted by port-adjacent investments.

How will foreign-ownership reforms affect the market?

The January 2026 liberalization is expected to lift sales transactions, which are already forecast to grow at an 8.30% CAGR.

Which area of Jeddah offers the highest growth potential?

Peripheral zones labeled “Rest of Jeddah” are projected to grow at an 8.83% CAGR through 2030, driven by new infrastructure and tourism projects.

Are REITs influencing commercial property funding?

Yes, multiple large REIT offerings and supportive regulations are deepening capital-market liquidity for stabilized assets.

Page last updated on: