Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

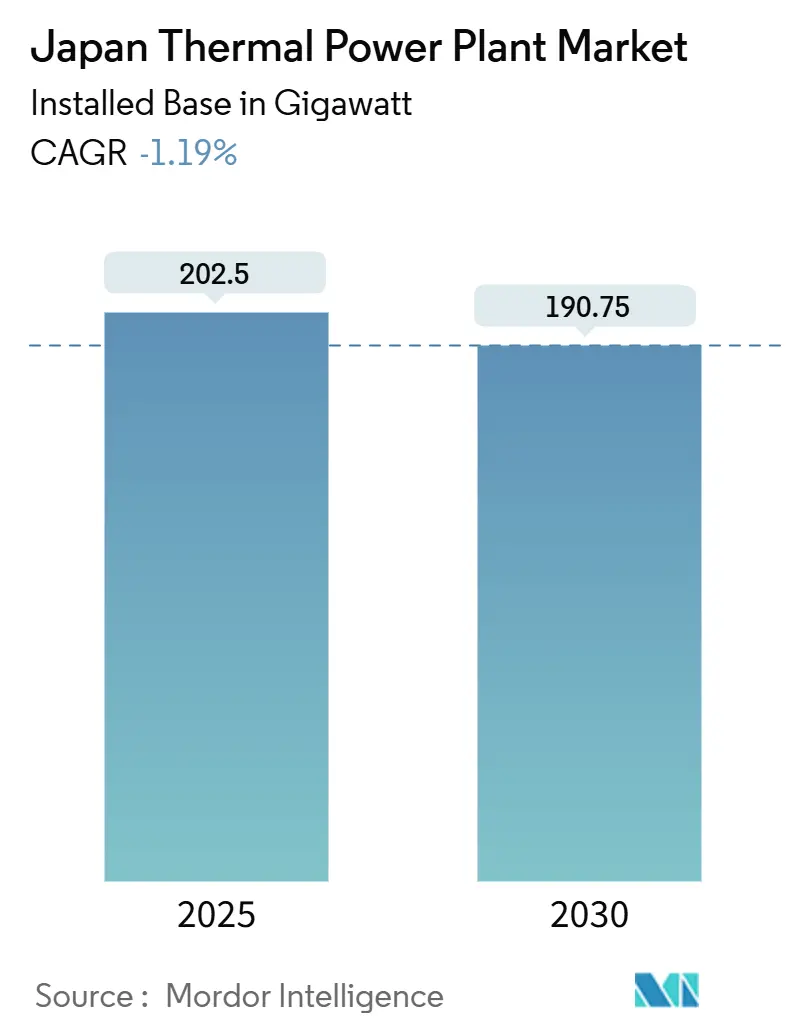

| Market Volume (2025) | 202.5 gigawatt |

| Market Volume (2030) | 190.75 gigawatt |

| Growth Rate (2025 - 2030) | -1.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Thermal Power Plant Market Analysis by Mordor Intelligence

The Japan Thermal Power Plant Market size in terms of installed base is expected to decline from 202.5 gigawatt in 2025 to 190.75 gigawatt by 2030.

The contraction co-exists with replacement demand because nuclear restarts, coal retirements, and policy-driven decarbonization reorder the generation mix. LNG remains the bridge fuel; gas-fired plants held 49.6% capacity share in 2024 and continue to expand as coal exits the fleet. Utilities are installing ultra-efficient combined-cycle turbines, accelerating ammonia co-firing pilots, and testing carbon capture to comply with the emissions-trading system that becomes mandatory in 2026. Competitive pressure stays intense because capacity-market payments favor dispatchable assets, while data-center build-outs in Tokyo and Osaka create a new source of round-the-clock demand that rewards flexible peaker plants.

Key Report Takeaways

- By fuel type, natural gas held 49.6% of the Japan thermal power market share in 2024 and is the only segment projected to grow, advancing at a 1.2% CAGR through 2030.

- By technology, combined heat and power accounted for 3.8% of incremental capacity additions in 2024 and is forecast to record the fastest 3.8% CAGR through 2030.

- By application, peaker plants contributed 4.9% of new capacity in 2024 and are projected to register a 4.9% CAGR to 2030.

- By combustion method, turbine-based systems represented 50.9% of incremental builds in 2024 and are set to grow at a 2.5% CAGR through 2030.

- JERA, Kansai Electric, and Chubu Electric together generated 57% of national thermal output in 2024.

Japan Thermal Power Plant Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decommissioning of aging coal fleet | +0.3% | Hokkaido, Tohoku, Chugoku | Medium term (2-4 years) |

| LNG-to-power capacity additions | +0.5% | Chiba, Aichi, Hyogo | Short term (≤ 2 years) |

| Industrial cogeneration demand | +0.2% | Aichi, Osaka, Kanagawa | Long term (≥ 4 years) |

| Hydrogen and ammonia co-firing retrofits | +0.4% | Nationwide, early JERA and Hokkaido Electric sites | Medium term (2-4 years) |

| Data-center-led baseload growth | +0.3% | Tokyo and Osaka metros | Short term (≤ 2 years) |

| Carbon-capture pilot incentives | +0.2% | Kansai, Kanto, Chubu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Decommissioning of Aging Coal Fleet Accelerates Market Restructuring

Japan's thermal power plant market sees 22% of sub-critical coal units slated for closure by 2030, catalyzing demand for efficient replacements that meet tightening emission norms. Plant retirements converge with fossil-fuel levies, making shutdowns more economical than retrofits. Utilities in Kansai and Kyushu are fast-tracking CCGT and ultra-supercritical projects to secure reliable capacity and grid stability. As coal exits, investment shifts toward gas turbines that pair with battery storage and demand-response frameworks. The cycle creates construction opportunities for OEMs while lowering average fleet emissions intensity.

LNG-to-Power Capacity Additions Strengthen Energy Security Architecture

Three replacement projects delivered 6.66 GW between February 2024 and March 2025, reinforcing LNG’s central role in the Japan thermal power plant market. JERA’s annual procurement of 30 million t, 40% of the national supply, anchors price negotiations and hedging strategies. Coastal siting near existing terminals shortens lead times, and high-efficiency CCGTs lift fleet average thermal efficiency. Yet, domestic LNG demand dropped 25% since 2014, prompting utilities to re-export oversupply via regional trading hubs. This dual track balances domestic security with commercial flexibility.

Industrial Cogeneration Demand Driven by Manufacturing Resilience Requirements

Manufacturers operate 6,213 cogeneration units totaling 11,085 MW, achieving 44-50% overall efficiency that trims energy bills and emissions. Captive power shelters factories from grid price swings and blackout risk, a priority after recent supply chain disruptions. The revised Energy Conservation Act mandates tighter efficiency metrics, spurring upgrades in Aichi, Osaka, and Kanagawa. Developers bundle waste-heat applications with carbon-capture pilots to future-proof assets. As a result, industrial cogeneration becomes a niche growth pocket within the broader, slow-growing Japan thermal power plant market.

Carbon-Capture Pilot Incentives Create Pathways for Thermal Power Longevity

Nine CCS projects selected in July 2024 receive state backing, signalling that policymakers consider abated thermal generation a viable long-term asset class.(1)ICAP, “Japan Emissions Trading System,” capcarbonaction.com Kansai Electric’s Himeji plant captures 5 t CO₂ per day, validating technology integration without extensive downtime. Smaller skid units supplied by Toshiba to Tokyo Gas open distributed applications. Japan’s experience at Tomakomai, 0.3 Mt stored over 2016-2019, builds public confidence in offshore sequestration. If economics improve, CCS could offset a share of carbon-pricing liabilities, keeping legacy capacity dispatchable.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aggressive renewable capacity targets | –0.8% | Nationwide | Long term (≥ 4 years) |

| Rising carbon pricing and ETS costs | –0.6% | Nationwide | Medium term (2-4 years) |

| Coastal LNG terminal opposition | –0.3% | Domestic & Southeast Asia projects | Medium term (2-4 years) |

| Global LNG price volatility | –0.4% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aggressive Renewable Capacity Targets Compress Thermal Utilization

Japan aims for renewables to exceed 36-38% of the mix by 2030, a goal led by Kyushu’s solar and Tohoku’s wind build-out.(2)Ministry of Economy, Trade and Industry, “Sixth Strategic Energy Plan,” meti.go.jpHigh penetration forces curtailment of mid-merit thermal units, shrinking run-hours, and squeezing spark-spreads. Utilities respond by mothballing older oil and sub-critical coal assets. Grid-enhancement projects, including HVDC links, aim to smooth regional imbalances yet further curtail thermal dispatch in high-renewables zones.

Rising Carbon Pricing & ETS Costs Tilt Economics Away from Fossil Assets

The Fossil-Fuel Levy scheduled for FY 2028 levies incremental costs that escalate through 2030. Early ETS pilots price carbon near USD 15/t, and analysts expect a doubling by 2030 as free allocations taper. Higher compliance costs disproportionately hit coal and oil units, accelerating decommissioning schedules and constraining any upside in the Japan thermal power plant market.

Segment Analysis

By Fuel Type: Natural Gas Expands as Coal Contracts

Natural gas accounts for 49.6 GW of the Japan thermal power market size and is projected to rise at a 1.2% CAGR to 2030. Coal retirements accelerate, illustrated by Hokkaido Electric’s 600 MW closure plan, while oil units serve only emergency roles. JERA’s 2.34 GW Goi plant and 1.32 GW Chita expansion anchor the shift. LNG over-contracting pressures margins, yet policy incentives and lower carbon intensity keep gas in a growth trajectory.(3)Turbomachinery Magazine, “Futtsu Group 4 Commercial Operation,” turbomachinerymag.com

Despite 76% of the coal fleet being high-efficiency units, rising carbon costs and ammonia-supply uncertainty curb reinvestment appetite. If CCS pilots achieve sub-USD 100 per-tonne costs and capacity-market revenues remain stable, selected ultra-supercritical plants may survive beyond 2030.

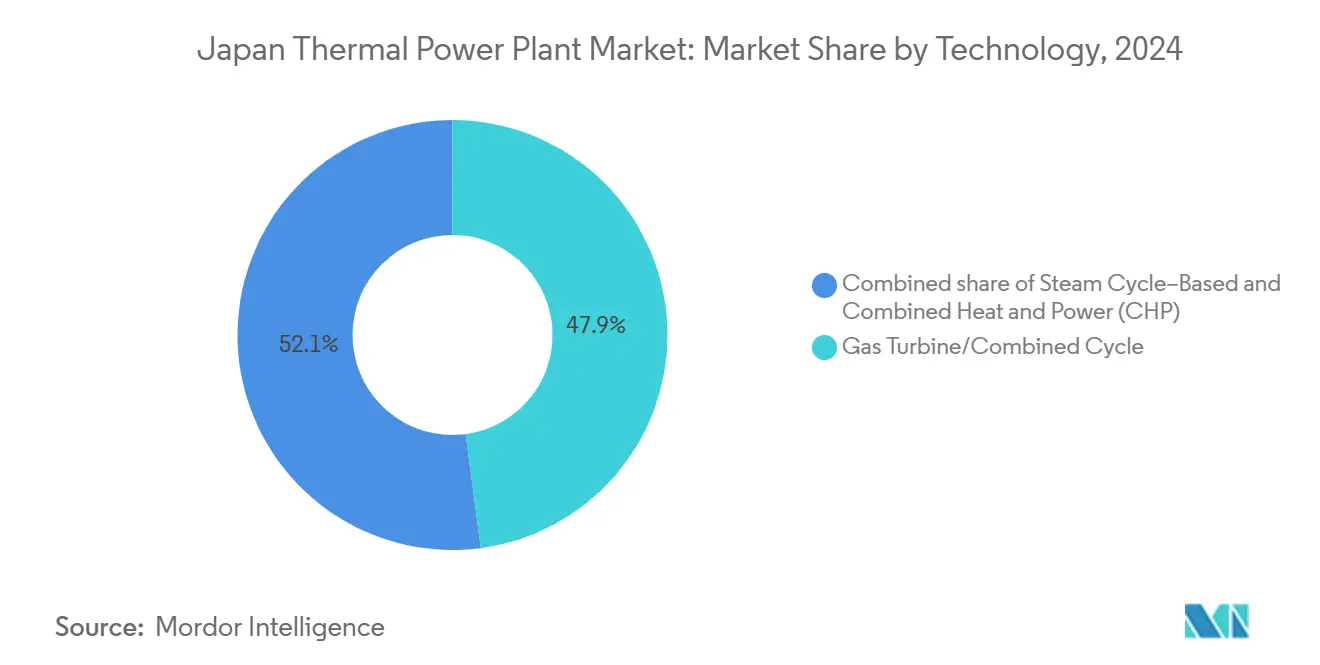

By Technology: CHP Captures Industrial Efficiency Gains

Gas turbine/combined-cycle technology held a 47.9% share in 2024, led by HA-class turbines that reach 64% thermal efficiency. However, combined heat and power is the fastest-growing category, expanding at a 3.8% CAGR as manufacturers hedge against high tariffs. Projects by Hiroshima Gas and the Hyuga Biomass plant show 60-80% efficiency gains.

Small-to-medium CHP units from YANMAR and Aisin proliferate in chemical and steel clusters, while hydrogen household engines advance under METI’s roadmap. Steam-cycle capacity declines in lockstep with coal shutdowns, and IGCC remains niche due to high levelized costs.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Combustion Method: Turbine-Based Systems Gain Flexibility Premium

Pulverized fuel still comprised 49.1% of capacity in 2024, yet turbine-based combustion is growing at a 2.5% CAGR. GE Vernova HA turbines at Goi and Futtsu ramp from cold start to full load in under 30 minutes, a critical attribute as solar output swings 40 GW within a day.

Fluidized-bed and gasification projects, such as Hirono IGCC, stay demonstration-scale because costs top USD 120 per MWh. Internal-combustion engines remain confined to remote microgrids.

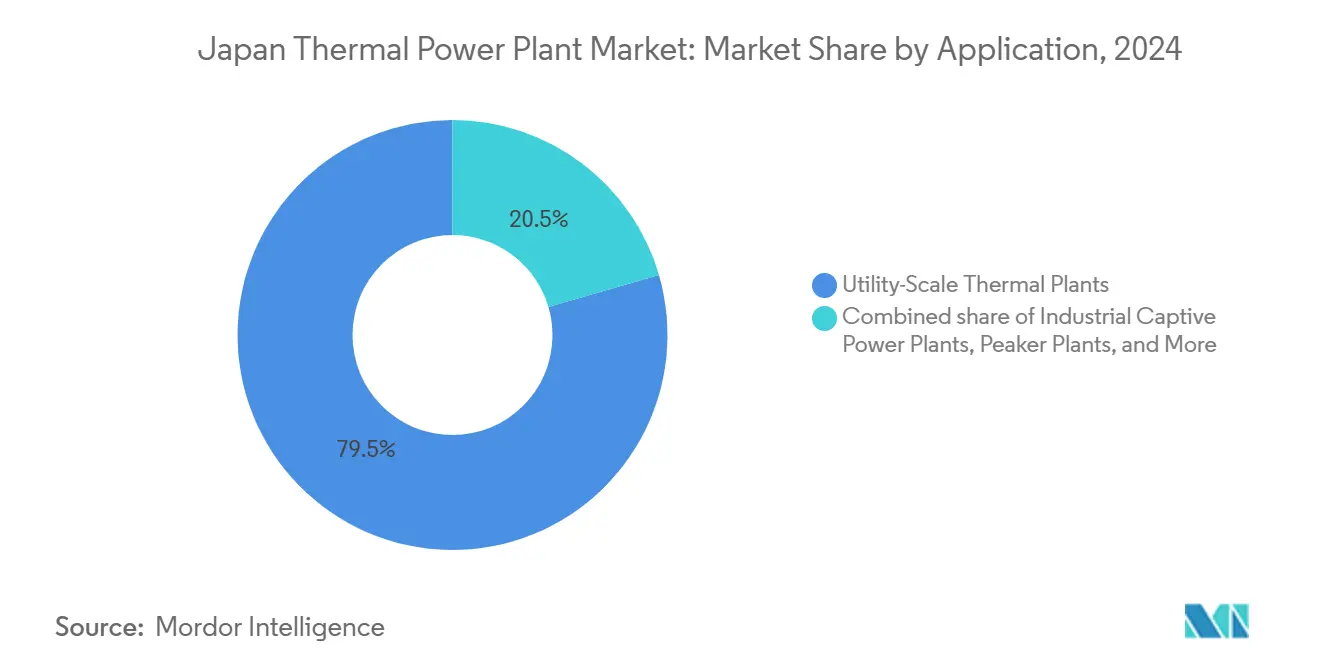

By Application: Peaker Plants Balance Intermittency

Utility-scale plants still hold a 79.5% share, but peaker plants post a 4.9% CAGR as the grid absorbs more renewables. Capacity-market design pays premiums for rapid-start units, and data-center operators favor dispatchable contracts bundled with certificates. Industrial captive power sees steady uptake of CHP, especially in Aichi, Osaka, and Kanagawa.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Tokyo-centric Kanto hosts the largest LNG fleet, including the 2.34 GW Goi plant, and faces a 1.3 GW data-center build-out by 2027. Osaka-based Kansai leads carbon capture, with MHI’s pilot at Himeji No. 2 capturing 5 t/d from 2025. Chubu’s 1.32 GW Chita upgrade underpins LNG demand and feeds into the Tokyo Bay Area CCS export plan to Malaysia.

Hokkaido combines accelerated coal retirements, a 569.4 MW LNG plant brought forward to 2031, and a 20% ammonia co-firing target at Tomato-Atsuma by 2031. Tohoku and Kyushu leverage offshore wind and geothermal, respectively, retiring thermal capacity earlier than the national average. Chugoku remains the testbed for IGCC and gasifier-linked CCS, but cost hurdles limit rollout.

Nuclear restarts shape regional load. Kansai’s Takahama restart in 2023 lifted nuclear to 8.5% of national generation, displacing LNG and worsening the 12 million tpa oversupply. As more reactors return, LNG terminals in regions with slower nuclear progress guard against supply gaps, maintaining geographic imbalances in the Japan thermal power market.(4)“Hokuriku Electric LNG Expansion,” nhk.or.jp

Competitive Landscape

JERA holds 30% generation share and 59 GW capacity, giving it scale to pilot ammonia and CCS while retiring coal. Kansai Electric partners with MHI on carbon-capture pilots; Chubu Electric co-develops Chita’s gas expansion; and Tohoku and Hokkaido Electric juggle quake-related reliability constraints with decarbonization goals. Independent power producers and trading houses exploit niches in industrial CHP, peakers, and fuel logistics.

Technology vendors shape competition. GE Vernova’s HA turbines anchor high-efficiency builds, MHI pushes hydrogen-ready turbines, and Toshiba supplies steam cycles in Chita’s upgrade. The JPY 1.6 trillion capacity market distributed 72% of payments to fossil plants in 2024, sparking debate that the mechanism delays retirements yet also secures reserve margins demanded by data-center operators.

Marubeni’s 250,000 tpa low-carbon ammonia deal with ExxonMobil and the Tokyo Bay Area CCS consortium indicates that fuel-supply and carbon-transport chains will become profit pools. The Japan thermal power market retains moderate concentration; the top five utilities control about 70% of capacity, enabling coordinated compliance with 2040 decarbonization milestones.(5)Federation of Electric Power Companies, “Press Conference January 2025,” fepc.or.jp

Japan Thermal Power Plant Industry Leaders

Tokyo Electric Power Company Holdings, Inc.,

Toshiba Corp

Mitsubishi Heavy Industries, LTD.

Hitachi, Ltd.

Japan Atomic Power Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Sakura Internet signed a memorandum of understanding with JERA to explore data center co-location opportunities at JERA's LNG power plants in the Tokyo Bay area, addressing growing AI-driven electricity demand while leveraging existing thermal infrastructure for enhanced operational efficiency, Japan Energy Hub.

- May 2025: Kansai Electric Power launched a CO2 capture pilot plant at Himeji Second Power Plant with 5-ton daily capacity, marking a commercial-scale demonstration of carbon capture integration with existing thermal power infrastructure in partnership with Mitsubishi Heavy Industries.

- April 2025: Tohoku Electric Power, JR East and partners signed renewable energy power purchase agreement to supply Tohoku Shinkansen operations, utilizing 59,800 kW from wind and solar sources while maintaining thermal backup capabilities for grid stability Tohoku Electric Power Co..

- March 2025: JERA initiated the world's first large-scale demonstration of 20% ammonia co-firing at Hekinan Thermal Power Station, targeting a 50% substitution rate by FY 2028 as part of its zero-emissions thermal power development strategy.

- February 2025: Sumitomo Corporation signed a loan agreement for the Muara Laboh geothermal expansion project in Indonesia, doubling capacity to 170 MW by 2027 with 70 billion yen financing from an international banking syndicate Sumitomo Corporation.

Japan Thermal Power Plant Market Report Scope

The Japan thermal power plant market report include:

By Fuel Type

| Coal-Fired Power Plants |

| Natural Gas–Fired Power Plants |

| Oil-Fired Power Plants |

By Technology

| Steam Cycle–Based |

| Gas Turbine/Combined Cycle |

| Combined Heat and Power (CHP) |

By Combustion Method

| Pulverized Fuel (PF) Combustion |

| Fluidized Bed Combustion |

| Gasification |

| Internal Combustion Engines |

| Turbine-Based Combustion |

By Application

| Utility-Scale Thermal Plants |

| Industrial Captive Power Plants |

| Distributed Thermal Plants |

| Peaker Plants |

| By Fuel Type | Coal-Fired Power Plants |

| Natural Gas–Fired Power Plants | |

| Oil-Fired Power Plants | |

| By Technology | Steam Cycle–Based |

| Gas Turbine/Combined Cycle | |

| Combined Heat and Power (CHP) | |

| By Combustion Method | Pulverized Fuel (PF) Combustion |

| Fluidized Bed Combustion | |

| Gasification | |

| Internal Combustion Engines | |

| Turbine-Based Combustion | |

| By Application | Utility-Scale Thermal Plants |

| Industrial Captive Power Plants | |

| Distributed Thermal Plants | |

| Peaker Plants |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is Japan's thermal power capacity in 2025?

Installed capacity totals 202.50 GW in 2025.

What CAGR is projected for gas-fired plants through 2030?

Gas-fired capacity is expected to grow at 1.2% CAGR.

Which technology segment is growing the fastest?

Combined heat and power is advancing at 3.8% CAGR as manufacturers seek efficiency gains.

What policy sets Japan's 2040 thermal-generation cap?

The 7th Strategic Energy Plan limits thermal power to 30-40% of generation by 2040.

How does ammonia co-firing help decarbonize coal plants?

Demonstrations such as JERA's 20% test at Hekinan cut CO? while preserving existing assets for grid stability.

When does emissions trading become mandatory?

Japan's ETS shifts from voluntary to mandatory participation in 2026.