Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

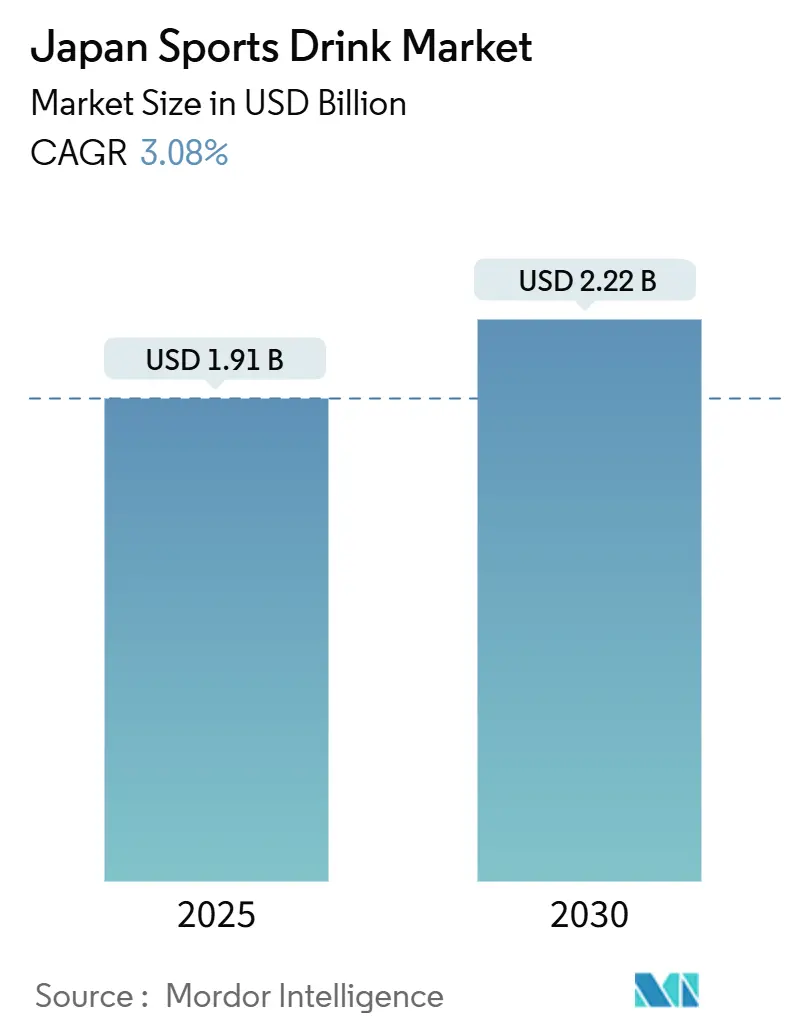

| Market Size (2025) | USD 1.91 Billion |

| Market Size (2030) | USD 2.22 Billion |

| Growth Rate (2025 - 2030) | 3.08% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Sports Drink Market Analysis by Mordor Intelligence

Japan's sports drink market is projected to reach USD 1.91 billion by 2025 and grow further to USD 2.22 billion by 2030, with a CAGR of 3.08% during 2025-2030. The growth is primarily driven by premium product innovations, functional benefits, and expanding sales channels rather than higher consumption volumes. With an aging population, there is increasing demand for protein-fortified and low-sugar electrolyte drinks that support joint health and sarcopenia. While isotonic drinks like Pocari Sweat and Aquarius still dominate over half of the market value, protein-based ready-to-drink products are growing rapidly. Packaging has become a key focus for branding, with plant-based PET, ultra-light recycled PET, and premium glass bottles emphasizing sustainability and quality. Online sales are also rising, as subscription services and direct-to-consumer brands avoid the crowded convenience store market and partner with fitness apps to reach consumers.

Key Report Takeaways

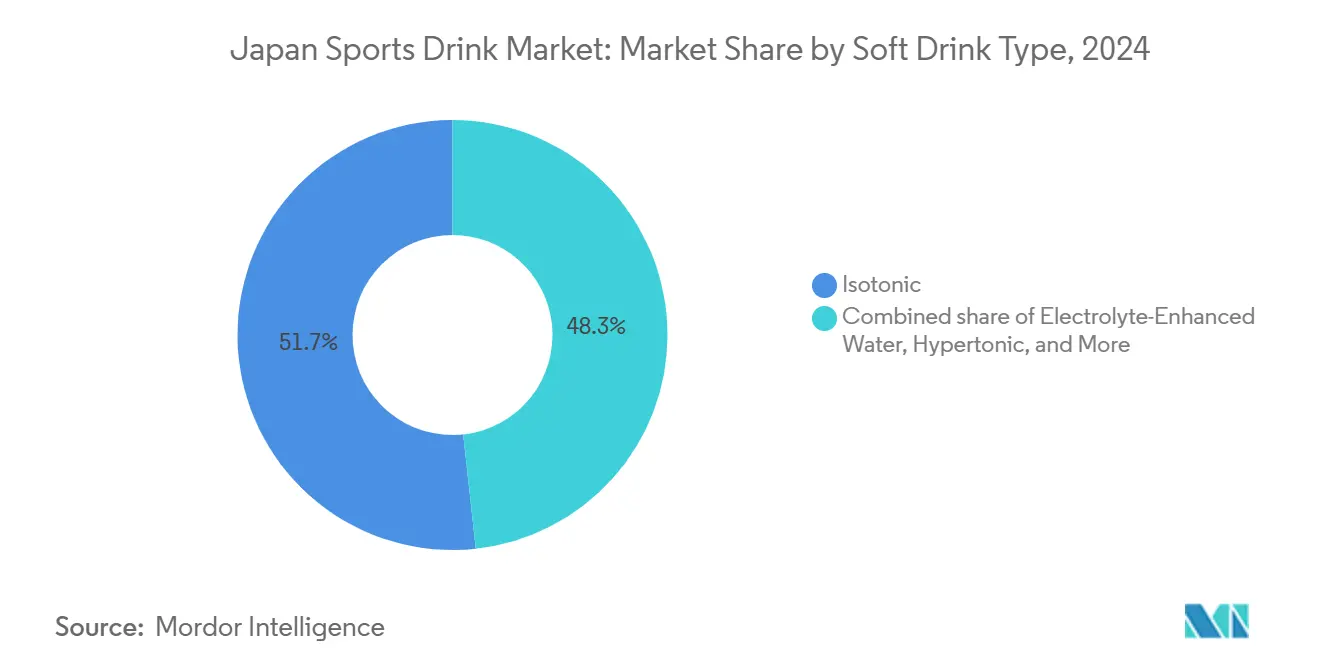

- By soft drink type, isotonic drinks led with 51.72% of the Japan sports drink market share in 2024, while protein-based variants are projected to expand at a 4.89% CAGR through 2030.

- By packaging type, PET bottles captured 54.28% share of the Japan sports drink market size in 2024; glass bottles exhibit the fastest 5.27% CAGR between 2025 and 2030.

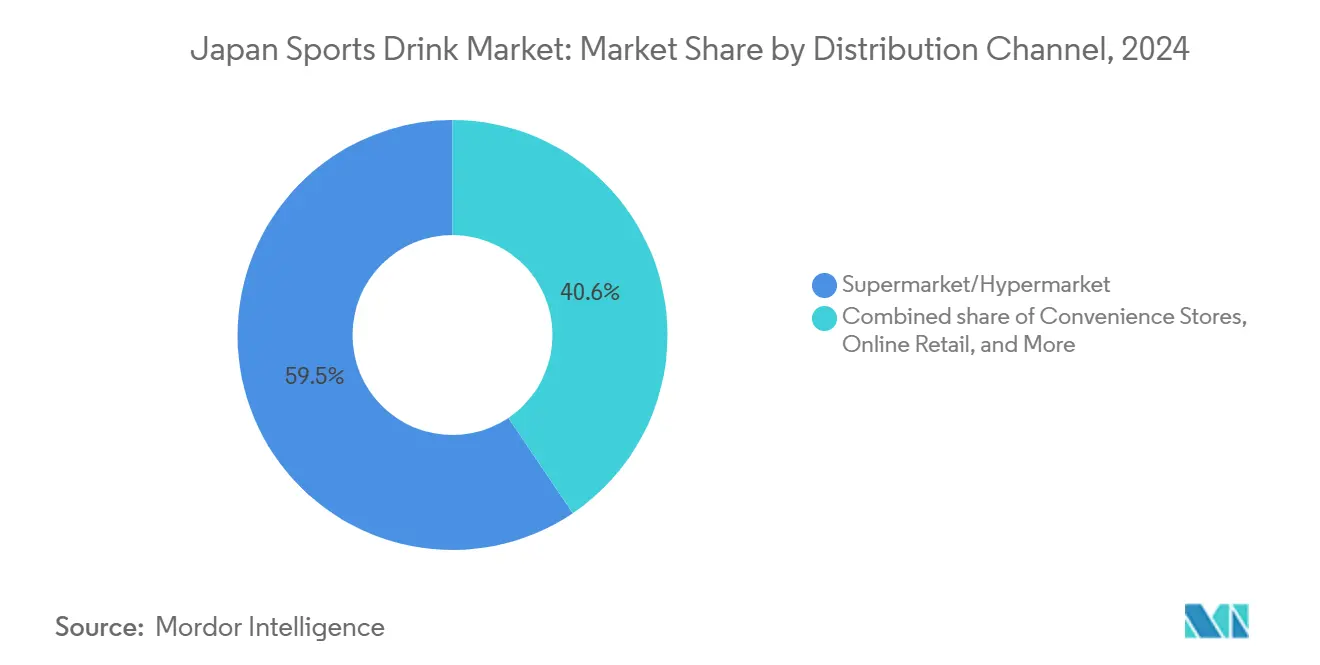

- By distribution channel, supermarkets / hypermarkets accounted for 59.45% value in 2024, whereas online retail is advancing at a 4.36% CAGR during the forecast period.

Japan Sports Drink Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness among consumers | +0.7% | National, with concentration in Tokyo, Osaka, and Nagoya metropolitan areas | Medium term (2-4 years) |

| Increased participation in organized sports, marathons, fitness clubs | +0.6% | National, with early gains in urban prefectures hosting major events (Tokyo, Osaka, Hokkaido) | Short term (≤ 2 years) |

| The broader culture of sports and major events | +0.4% | National, event-driven spikes in Tokyo (World Athletics Championships, Deaflympics 2025) | Short term (≤ 2 years) |

| Product innovation with natural ingredients | +0.5% | National, premium adoption in metropolitan areas | Medium term (2-4 years) |

| Government sports promotion initiatives | +0.3% | National, with targeted programs in rural prefectures to counter aging trends | Long term (≥ 4 years) |

| Demand for clean-label and functional benefits | +0.4% | National, led by health-conscious urban consumers and fitness enthusiasts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness Among Consumers

Japan is moving from reactive to preventive health management, which is changing how sports drinks are made and marketed. The Sasakawa Sports Foundation's White Paper on Sport shows that weekly exercise participation in Japan increased from 23.7% in 1992 to 58.5% in 2022. Meiji's SAVAS protein drinks are addressing this trend[1]Sasakawa Sports Foundation, "White Paper on Sport." ssf.or.jp. In March 2024, they launched a chocolate flavor, followed by a 30-gram protein option in September 2024. These ready-to-drink products are promoted as meal replacements, especially for busy office workers and seniors dealing with sarcopenia. The Ministry of Health, Labour and Welfare's Health Japan 21 third edition (2024-2035) supports this shift by setting 51 specific goals related to nutrition, exercise, and chronic disease prevention. This provides indirect regulatory support for drinks that combine hydration with protein or amino acids. Reflecting this trend, Otsuka's Amino Value and Ajinomoto's AminoVital, both enriched with amino acids, gained more shelf space in drugstores and fitness-club vending machines in 2024. At the same time, the Consumer Affairs Agency's updated Foods with Function Claims system creates challenges for new players. It requires health-hazard reporting from September 2024 and Good Manufacturing Practice compliance by April 2025, but it also validates functional claims for established brands.

Increased Participation in Organized Sports, Marathons, Fitness Clubs

In 2024, marathon registrations in Japan's major cities increased by 15% compared to the previous year. This growth was driven by Tokyo's upcoming hosting of the World Athletics Championships and the Deaflympics in late 2025, according to the Japan Association of Athletics Federations[2]JAAF, "Japan Association of Athletics Federations." jaaf.or.jp. The rise in marathon participation has led to higher demand for isotonic and hypotonic drinks, particularly at race expos and convenience stores near event venues. The fitness-club market is evolving, with premium chains like Konami Sports Club and Anytime Fitness focusing on affluent urban customers. Meanwhile, chocoZAP, a budget micro-gym chain by RIZAPgroup, expanded to 1.31 million members and 1,755 locations by mid-2024, making fitness more accessible and creating new opportunities to sell single-serve protein drinks. In January 2025, Mizuno partnered with Minami Shinshu Beer to launch "PUHAAH," a non-alcoholic beer designed for post-exercise refreshment. This move highlights how sports-equipment brands are using their reputation to enter the beverage market. Kirin strengthened its position in the health-science sector by acquiring Fancl in August 2024 and obtaining a functional beverage brand from Kao in February 2024. These steps enable Kirin to introduce sports drinks containing LC-Plasma, a lactic acid strain that supports immunity. LC-Plasma generated 24 billion yen in revenue in 2024 and has about 780,000 regular users.

Product Innovation with Natural Ingredients

Consumer skepticism towards synthetic additives, coupled with the rising popularity of botanical-forward beverages, has propelled clean-label formulations from niche health-food outlets to mainstream konbini shelves. Launched in August 2024, Umami Cola harnesses koji fermentation to infuse natural sweetness, replacing refined sugar, and adds botanical extracts. In November 2024, Meiji's SAVAS line received the Informed Protein certification, a third-party endorsement ensuring freedom from banned substances. This move directly addresses a significant concern for competitive athletes, who risk career-ending sanctions from unintentional contamination, thus broadening the market appeal beyond just recreational users. Suntory made headlines in October 2024 with its debut of bio-paraxylene PET bottles, a groundbreaking technology sourced from plant sugars instead of petroleum. This innovation, touted as the world's first commercial-scale application, boasts a 25% reduction in lifecycle carbon emissions compared to traditional PET. In a forward-looking move, the Ministry of Economy, Trade and Industry, in March 2025, mandated that by 2030, beverage bottles must comprise at least 15% recycled or bio-based materials. This regulation favors early adopters like Suntory and Otsuka Foods. Notably, Otsuka Foods achieved a milestone in February 2025, rolling out its JAVA TEA line with 100% recycled PET, leading to a commendable 63% reduction in CO2 emissions.

Government Sports Promotion Initiatives

The Japan Sports Agency introduced its Vision 2025 framework alongside Tokyo hosting the World Athletics Championships and Deaflympics. This plan provides funding for municipal sports facilities and supports corporate wellness programs, increasing the demand for hydration products in public gyms and workplace fitness centers. In September 2024, Otsuka Pharmaceutical was named the official sports drink sponsor of the World Athletics Championships Tokyo 25. The company installed 500 branded hydration stations at the Olympic Stadium and training venues, creating around 2 million consumer interactions during the event. The Tokyo Metropolitan Government's "Tokyo Vision 2025" aims to raise the percentage of residents engaging in weekly physical activity from 58.5% in 2022 to 70% by the end of 2025[3]Tokyo Metropolitan Government, "Tokyo Metropolitan Government - Vision 2025." metro.tokyo.lg.jp. This goal has led to partnerships between beverage companies and local governments to co-brand sports drinks for events like community marathons and school sports festivals. During fiscal 2024, Kirin's Health Science division plans to use government wellness subsidies to promote its LC-Plasma-infused beverages as preventive health products. These beverages are eligible for corporate reimbursement under Japan's Specific Health Checkup system.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over high sugar content | -0.3% | National, with heightened scrutiny in urban areas following MHLW guidelines | Short term (≤ 2 years) |

| Regulatory restrictions on ingredients | -0.2% | National, with stricter enforcement in functional claims under revised FFC system | Medium term (2-4 years) |

| Competition from traditional beverages | -0.4% | National, strongest in rural prefectures with entrenched tea consumption | Long term (≥ 4 years) |

| Supply chain and distribution challenges | -0.2% | National, acute in remote prefectures with limited cold-chain infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over High Sugar Content

In April 2025, Coca-Cola made its first major change to Aquarius in 20 years. The reformulation reduced calories from 95 to 90 per bottle and increased potassium from 8 to 9 mg per 100 ml. This change was a response to consumer concerns about sugary sports drinks, which typically contain 19 grams of sugar per 500 ml, equal to nearly five teaspoons. Japan's Ministry of Health, Labour and Welfare, through its Health Japan initiative, has set a national goal to reduce daily sugar intake. While there are no specific limits for beverages, this goal has driven the launch of more zero-sugar options in the market. For example, Kirin's sugar-free Hyoketsu series grew by about 30% year-on-year in 2023, showing that consumers are willing to choose healthier options when products highlight functional ingredients like electrolytes and amino acids. In November 2024, Monster Energy increased its price from 205 yen to 230 yen, a 5% rise. This was due to the higher costs of alternative sweeteners like acesulfame K and stevia, which are 2-3 times more expensive than high-fructose corn syrup but are necessary to meet clean-label standards. Additionally, in August 2024, the Consumer Affairs Agency updated the Foods with Function Claims system. The new rules require companies to report any health hazards within 15 days of discovery, increasing the risk for brands that overstate hydration benefits or understate sugar content.

Competition from Traditional Beverages

In 2024, green tea led cold-drink purchases at convenience stores, accounting for nearly twice the combined 14% share of carbonated and sports drinks, according to the Japan Soft Drink Association. This reflects Japan's strong cultural preference for tea as a common hydration choice. Brands like Suntory and Ito En have capitalized on this trend by promoting their unsweetened tea lines as zero-calorie options. These teas benefit from their antioxidant properties without needing to make functional claims, which are subject to stricter regulations under Japan's revised Foods with Function Claims system. Additionally, traditional tea can be consumed at room temperature, removing the need for cold storage. This reduces costs and allows retail prices to be 10-15% lower than refrigerated sports drinks, which is important for price-sensitive rural consumers. In October 2024, a study by Asahi Soft Drinks found that cold carbonated water can temporarily raise blood pressure and improve mood after exercise. This positions sparkling water as a zero-calorie hydration option, further diversifying the sports drink market.

Segment Analysis

By Soft Drink Type: Protein Surge Challenges Isotonic Dominance

In 2024, isotonic drinks commanded a 51.72% share of Japan's sports drink market, a dominance rooted in Otsuka's Pocari Sweat and Coca-Cola's Aquarius. These brands set osmolality benchmarks—aligning with blood plasma at approximately 280-300 mOsm/kg—to enhance absorption during moderate exercise. In April 2025, Coca-Cola's Aquarius underwent a reformulation, trimming calories from 95 to 90 per bottle, boosting potassium content from 8 to 9 mg per 100 ml, and adding more acesulfame K sweetener for a refined taste. This move underscores Coca-Cola's strategy to safeguard its market share against emerging zero-sugar competitors, all while retaining its loyal isotonic sweetness fans. Otsuka, reinforcing its isotonic dominance, announced in September 2024 its sponsorship of the World Athletics Championships Tokyo 25, featuring 500 branded Pocari Sweat hydration stations. Yet, while the isotonic segment's value has surged, largely due to premiumization with functional additives like amino acids and vitamins, its volume growth has plateaued, signaling a maturation phase.

Protein-based sports drinks are on track to grow at a 4.89% CAGR through 2030, outpacing all other soft drink categories. This surge is largely fueled by Meiji's SAVAS and Morinaga's Weider brands, both of which clinched the Informed Protein certification in November 2024, a crucial third-party endorsement for elite athletes. In September 2024, Meiji introduced a 30-gram protein variant of SAVAS, targeting sarcopenia prevention for Japan's aging demographic. Notably, 29% of Japan's population was aged 65 or older in 2023, with projections indicating a rise to 33.9% by 2038. This strategic positioning frames the drink more as a meal replacement than a mere post-exercise recovery aid. Hypotonic drinks, with osmolality levels below 280 mOsm/kg, cater to endurance runners desiring swift gastric emptying. However, their market presence remains limited due to insufficient brand investment. On the other hand, hypertonic drinks, surpassing the 300 mOsm/kg mark, are primarily reserved for post-workout recovery. Yet, they grapple with challenges stemming from a growing consumer preference for lower-calorie alternatives.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Packaging Type: Glass Premiumization Outpaces PET Ubiquity

In 2024, PET bottles accounted for 54.28% of Japan's sports drink market. This dominance is supported by Japan's widespread network of around 2.64 million beverage vending machines, roughly one for every 30 people. PET bottles are preferred due to their lightweight design and resistance to shattering. In October 2024, Toyo Seikan introduced a 500 ml Coca-Cola bottle made entirely from recycled PET, weighing just 21 grams, the lightest in Japan. This innovation highlights how companies are focusing on sustainability to appeal to environmentally conscious urban consumers. Similarly, in November 2024, Suntory launched 45 million bio-paraxylene PET bottles, the first commercial-scale bottles made from plant sugars instead of petroleum. These bottles reduce lifecycle carbon emissions by 25% and position Suntory ahead of the Ministry of Economy, Trade and Industry's proposed March 2025 regulation, which requires at least 15% recycled or bio-based materials in beverage bottles by 2030.

Glass bottles are expected to grow at a 5.27% CAGR through 2030, the fastest among all packaging types. Premium sports drinks are increasingly using glass to convey purity and justify a 20-30% price premium over PET bottles. Kirin's Ice brand, which uses glass packaging to promote fruit-waste reduction, aims to cut 150 tons of waste annually by 2027. This shows how sustainability claims linked to packaging can help differentiate hydration products in a competitive market. Metal cans, commonly used for energy drinks by brands like Red Bull and Monster, have limited use in the sports drink market. Consumers often associate aluminum cans with carbonated beverages rather than isotonic drinks. Aseptic packages, such as Tetra Pak cartons, remain a niche option for sports drinks because consumers still view cartons as suitable for juice or milk, not functional beverages.

By Distribution Channel: Online Gains as Konbini Saturates

In 2024, supermarkets and hypermarkets held a 59.45% share of the Japan Sports Drink Market. These retailers benefited from bulk-purchase discounts and prominent end-cap displays, especially during summer when hydration needs increased. Major chains like Aeon and Ito-Yokado offered exclusive pack sizes, such as 12-bottle multipacks, which were not available in convenience stores. This approach appealed to households and sports teams preparing for the season. In June 2024, Seven-Eleven launched a private-label version of Aquarius, priced 10-15% lower than Coca-Cola's branded product. This move highlighted retailers' growing presence in the sports drink market and put pressure on manufacturers' margins, as they rely heavily on supermarket sales.

Online retail is growing at a 4.36% CAGR through 2030, making it the fastest-growing distribution channel. This growth is driven by subscription services that deliver protein drinks and electrolyte powders directly to consumers, avoiding the need to carry heavy bottles from stores. LIFEDRINK COMPANY's ZAO SODA, which ranked first in Rakuten's beverage category for three consecutive years up to 2024, shows how direct-to-consumer brands can gain market share. These brands offer custom options, like caffeine-free or extra-electrolyte variants, which are not cost-effective for mass retailers to stock. Convenience stores, with about 58,000 locations nationwide and contributing 18% of food-and-beverage sales, remain important for impulse purchases. However, visit frequency has leveled off, with 40% of consumers visiting 2-3 times a week and 27% visiting 4-5 times a week, leaving little room for further growth in this category.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In Japan, urban centers like Tokyo, Osaka, and Nagoya dominate the consumption of premium protein drinks and functional isotonic variants. In contrast, rural prefectures favor value-priced PET bottles, typically sold through agricultural cooperatives and regional supermarkets. The Tokyo Metropolitan Government's Vision 2025 initiative aims to boost weekly physical activity among residents from 58.5% in 2022 to 70% by 2025. This push has led to collaborations between beverage firms and local governments, co-branding sports drinks for community marathons and school sports festivals. Otsuka's strategy is evident with its April 2025 opening of a production facility in Vietnam, primarily targeting Southeast Asian exports. However, the move also aims to de-risk supply chains for the domestic Japanese market, diversifying manufacturing beyond its Tokushima headquarters.

Consumption patterns in Japan showcase stark contrasts. In Hokkaido, the colder climate fuels a year-round demand for hot vending-machine beverages. This limits sports drink sales to the summer months and indoor fitness venues. Conversely, Okinawa's subtropical climate ensures isotonic sales year-round. Notably, convenience stores near beaches and hiking trails in Okinawa report sports drink revenues 30-40% above the national average. The Japan Sports Agency's "Sport in Life" initiative, targeting a 65% weekly exercise participation by 2030, allocates funds to rural prefectures. This aims to combat aging trends and depopulation, presenting brands an opportunity to market sports drinks as preventive health tools, potentially qualifying for municipal wellness subsidies. Kirin's strategic August 2024 acquisition of Fancl, coupled with its AI-driven inventory-optimized vending machine network (the Vendy system), positions the company to cater to regional preferences. This includes promoting higher-protein variants in aging rural areas and zero-sugar options in urban centers prioritizing health.

While the Ministry of Health, Labour and Welfare's Health Japan 21 third edition (2024-2035) sets a national standard for nutrition and exercise goals, prefectural governments have the autonomy to implement these guidelines. This has resulted in inconsistent enforcement of front-of-pack labeling and sugar-content disclosures across regions. The Consumer Affairs Agency, in August 2024, updated the Foods with Function Claims system. Starting September 2024, health-hazard reporting becomes mandatory, followed by Good Manufacturing Practice compliance in April 2025. While these regulations are nationwide, they pose a significant challenge for smaller regional brands lacking the compliance infrastructure of industry giants like Otsuka and Suntory. Highlighting the synergy between major events and regional initiatives, Coca-Cola Japan and Suntory are spearheading a bottle-to-bottle recycling initiative at EXPO 2025 Osaka. This initiative, set to run from April to October 2025, showcases how localized sustainability efforts can gain national traction.

Competitive Landscape

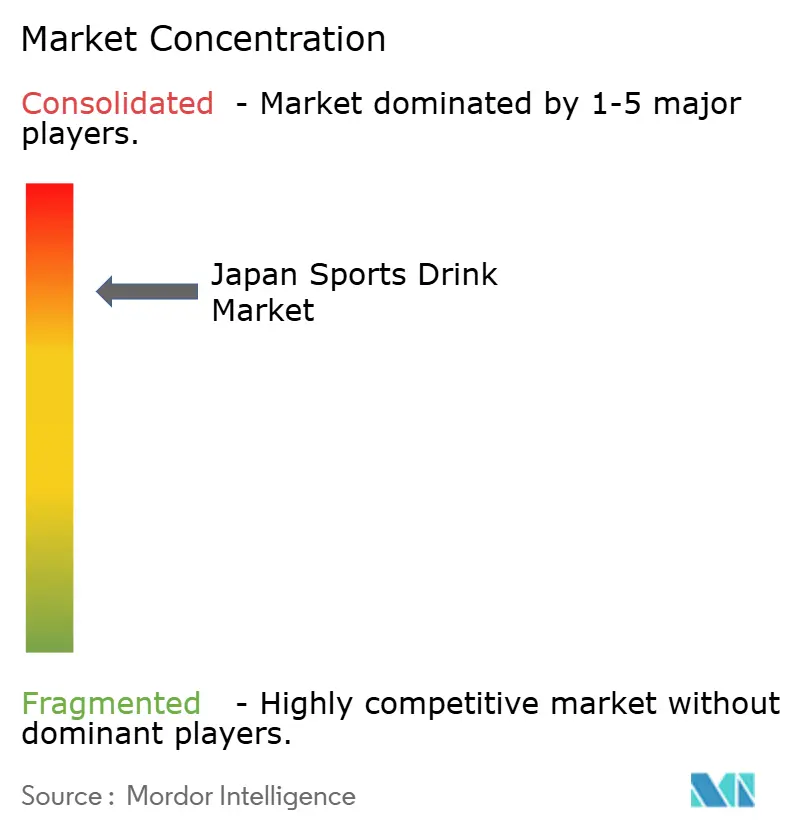

The Japan sports drink market is moderately concentrated, with a few well-established beverage manufacturers leading the category. These companies rely on strong brand recognition, nationwide distribution, and ongoing product innovation to maintain their position. They focus on creating electrolyte-balanced, low-sugar, and functional drinks designed for both daily hydration and athletic performance. Their partnerships with retail chains, sports associations, and vending machine networks enhance their visibility and accessibility, strengthening their market influence.

To stay competitive, key players in the market focus on strategies like expanding their operations, launching new products, and introducing innovations. They are developing unique products by using naturally derived ingredients and additives. Major companies in the Japan sports drink market include Otsuka Pharmaceutical Co., Ltd., The Coca-Cola Company, Suntory Holdings Limited, The Asahi Group Holdings, Ltd., and Otemon Co., Ltd.

In terms of technology, Kirin has implemented the Vendy AI system across 180,000 vending machines. This system predicts demand based on factors like weather, foot traffic, and local events, reducing stock shortages by 15-20%. Suntory, in October 2024, introduced bio-paraxylene PET bottles made from plant sugars using a proprietary fermentation process. This innovation is the first of its kind on a commercial scale and positions the company ahead of the Ministry of Economy, Trade and Industry's March 2025 requirement for beverage bottles to contain at least 15% recycled or bio-based materials by 2030.

Japan Sports Drink Industry Leaders

-

Otsuka Pharmaceutical Co., Ltd.

-

The Coca-Cola Company

-

Suntory Holdings Limited

-

The Asahi Group Holdings, Ltd.

-

Otemon Co., Ltd (Taisho)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Kaneka Corporation has launched a new product called “MITASU Plain,” a protein drink developed in collaboration with LAVA, a hot yoga studio group operated by LAVA International, Inc. The brand promotes itself as a natural product, made with simple ingredients such as soybeans, beet sugar, and inulin.

- September 2024: Otsuka Pharmaceutical Factory, Inc. has expanded its Oral Rehydration Solution OS-1® series, with the launch of OS-1 Jelly Apple Flavor 200g. According to the brand, OS-1 Jelly Apple Flavor is a product with the same concentrations of ingredients involved in the water and electrolyte replenishment effect as the oral rehydration solution OS-1.

- April 2023: Kirin has launched its first Food with Function Claims (FFC) sports nutrition drink, which offers immune health benefits to meet the demands of active consumers seeking multifunctional products.

Japan Sports Drink Market Report Scope

Japan Sports Drinks Market is segmented by packaging and distribution channel. On the basis of packaging, the market is segmented into PET Bottles, Cans, and others. On the basis of distribution channel, the market is segmented by Supermarkets/Hypermarkets, Convenience Stores, Online Retail Stores, and Other Channels.

Soft Drink Type

| Electrolyte-Enhanced Water |

| Hypertonic |

| Hypotonic |

| Isotonic |

| Protein-based Sport Drinks |

Packaging Type

| Aseptic packages |

| Glass Bottles |

| Metal Can |

| PET Bottles |

| Others |

Distribution Channel

| Convenience Stores |

| Online Retail |

| Specialty Stores |

| Supermarket/Hypermarket |

| Others |

| Soft Drink Type | Electrolyte-Enhanced Water |

| Hypertonic | |

| Hypotonic | |

| Isotonic | |

| Protein-based Sport Drinks | |

| Packaging Type | Aseptic packages |

| Glass Bottles | |

| Metal Can | |

| PET Bottles | |

| Others | |

| Distribution Channel | Convenience Stores |

| Online Retail | |

| Specialty Stores | |

| Supermarket/Hypermarket | |

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Japan sports drink market in 2025?

The market stands at USD 1.91 billion in 2025 and is forecast to hit USD 2.22 billion by 2030.

Which drink type is growing fastest in Japan’s sports segment?

Protein-based ready-to-drink products are expanding at a 4.89% CAGR, outpacing isotonic staples.

Which channel shows the highest growth for sports drink sales?

Online retail leads with a 4.36% CAGR thanks to subscriptions that bypass konbini saturation.

How are Japanese regulators influencing sports drink formulations?

Health Japan 21 sugar-reduction goals and stricter Foods with Function Claims rules push brands toward lower-sugar and fully documented functional ingredients.