Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

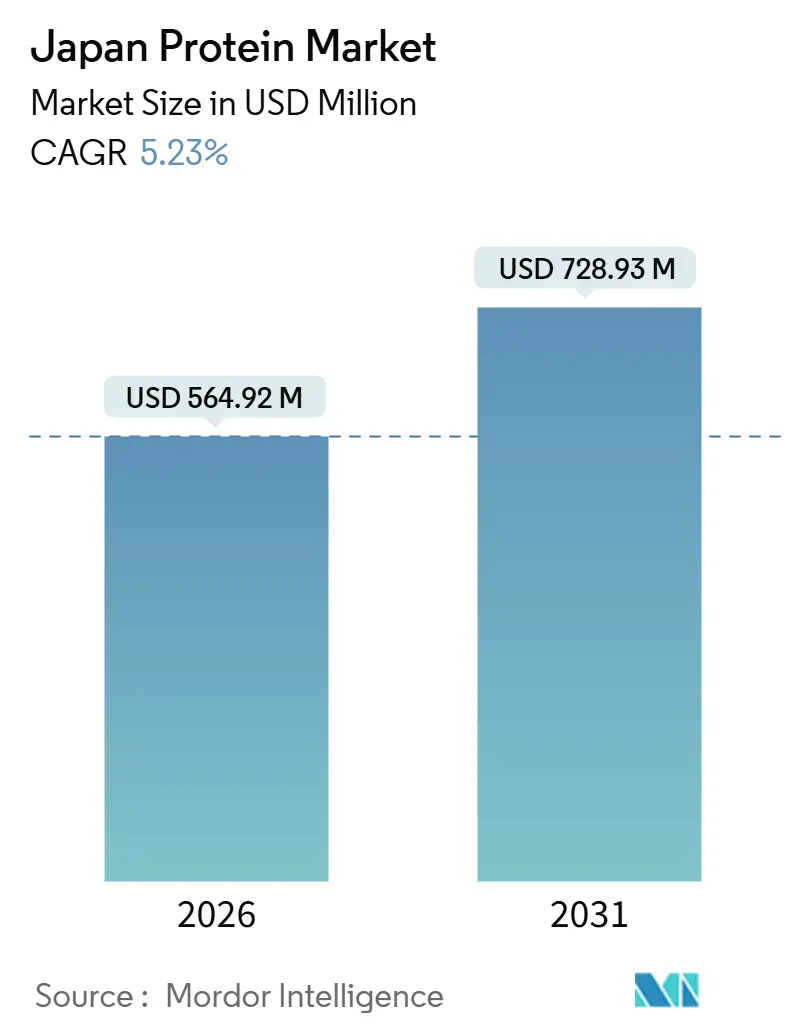

| Market Size (2026) | USD 564.92 Million |

| Market Size (2031) | USD 728.93 Million |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Protein Market Analysis by Mordor Intelligence

The Japan Protein Market size is estimated at USD 564.92 million in 2026, and is expected to reach USD 728.93 million by 2031, at a CAGR of 5.23% during the forecast period (2026-2031). This growth reflects a significant shift in how protein is consumed, positioned, and integrated into daily nutrition. The market's expansion is driven by protein's evolution from a niche, performance-focused ingredient to a fundamental component of preventive health and functional diets. Simultaneously, advancements in processing technologies, formulation science, and ingredient functionality are enhancing digestibility, taste, and versatility. These improvements allow protein to be seamlessly integrated into a wide range of consumption occasions. Additionally, the market is adapting to clean-label expectations, sustainability concerns, and the demand for scientifically validated nutrition. These factors are reshaping product development strategies and strengthening consumer trust.

Key Report Takeaways

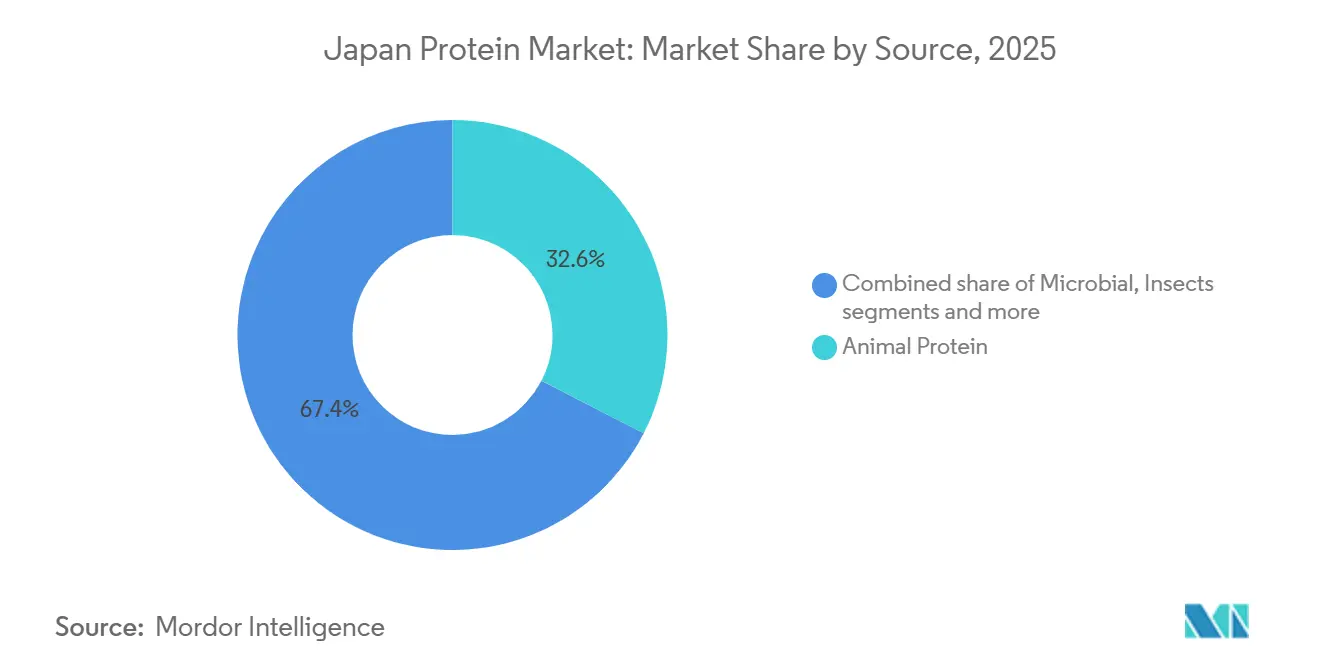

- By source type, animal protein held 32.56 of % Japan protein market share in 2025, while microbial protein is forecast to expand at a 5.64% CAGR through 2031.

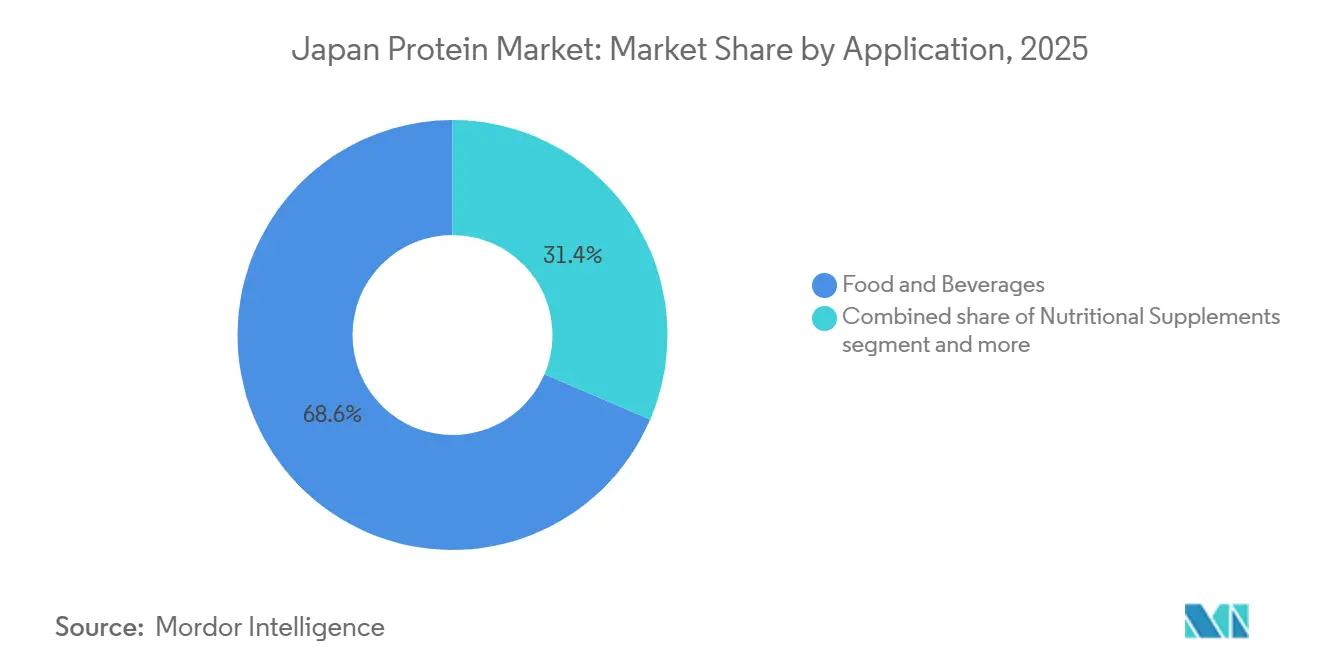

- By application, food and beverages accounted for 68.58% of the Japan protein market size in 2025, whereas cosmetics and personal care are projected to grow at a 6.45% CAGR to 2031.

Japan Protein Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly aging society and healthy longevity focus | +1.2% | National, with concentration in Tokyo, Osaka, and rural prefectures experiencing accelerated aging | Long term (≥ 4 years) |

| Expansion of sports, fitness, and active lifestyle culture | +0.9% | National, with early gains in urban centers (Tokyo, Yokohama, Nagoya) | Medium term (2-4 years) |

| Clean label and minimalist ingredient preferences | +0.7% | National, strongest in metropolitan areas among consumers aged 30-50 | Medium term (2-4 years) |

| Growing demand for plant-based and hybrid protein products | +0.8% | National, with higher adoption in Tokyo, Kyoto, and Fukuoka | Medium term (2-4 years) |

| Convenience-driven nutrition consumption patterns | +0.6% | National, particularly among working-age population (25-55 years) | Short term (≤ 2 years) |

| Shift toward high-quality, easily digestible proteins | +0.7% | National, with emphasis on elderly population (65+ years) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapidly aging society and healthy longevity focus

The rapidly aging population and the national emphasis on healthy longevity are key factors driving the Japan protein market. Dietary protein is increasingly recognized as vital for maintaining muscle mass, mobility, immune function, and overall quality of life among older adults. Japan's demographic structure, heavily skewed toward older age groups, heightens the demand for nutritional solutions targeting age-related conditions such as sarcopenia, frailty, and reduced metabolic efficiency. Protein-rich diets, delivered through fortified foods, functional beverages, supplements, and medical nutrition, are actively promoted to address these needs. This demand is further supported by the preference of elderly consumers for easy-to-consume, highly digestible, and clinically validated protein formats, such as whey, collagen peptides, and plant-based blends incorporated into everyday foods. The scale and urgency of this trend are highlighted by demographic data from the United Nations Population Fund (UNFPA), which indicates that individuals aged 65 years and older accounted for 29.56% of Japan's population in 2023, one of the highest proportions globally [1]Source: United Nations Population Fund (UNFPA), "Share of persons aged 65+ in the total population in Japan", unfpa.org. This demographic reality is driving food, beverage, and nutrition manufacturers to focus on protein fortification and age-specific formulations.

Expansion of sports, fitness, and active lifestyle culture

The growth of sports, fitness, and active lifestyle culture serves as a significant structural driver for the Japan protein market. Protein consumption is increasingly associated with physical performance, muscle recovery, and overall functional health across various age groups. Japan has experienced a consistent shift toward regular exercise, gym participation, recreational sports, and structured fitness routines. This lifestyle change is directly contributing to a rising demand for sports nutrition products, including whey and plant-based protein powders. Protein is now being positioned as a daily nutritional necessity rather than a specialized bodybuilding supplement, broadening its appeal among office workers, recreational athletes, and health-conscious individuals. Supporting this trend, data from the Ministry of Economy, Trade and Industry (METI) indicates that Japan had approximately 2.88 million fitness club members in 2024, underscoring the scale of organized fitness participation in the country [2]Source: Ministry of Economy, Trade and Industry (METI), "Number of fitness club members in Japan", meti.go.jp. This expanding fitness ecosystem is promoting consistent protein consumption as part of active lifestyle habits. Consequently, manufacturers are increasingly focusing on innovation in this space.

Clean label and minimalist ingredient preferences

Clean-label and minimalist ingredient preferences are becoming a significant driver in the Japan protein market, reflecting the country's strong consumer focus on transparency, safety, and simplicity in food and nutrition choices. Japanese consumers are increasingly examining ingredient lists and favoring protein products that exclude artificial additives, synthetic flavors, excessive sweeteners, and complex chemical components. This trend aligns with Japan's traditional food culture, which emphasizes purity, natural ingredients, and functional benefits over heavily processed formulations. Consequently, protein manufacturers are reformulating products to include shorter ingredient lists, easily recognizable raw materials, and clearly identified protein sources, such as whey, soy, marine collagen, and fermentation-derived proteins. Clean-label positioning is particularly impactful in categories such as functional foods, ready-to-drink protein beverages, elderly nutrition products, and beauty-from-within supplements, where trust and perceived safety play a critical role in purchase decisions.

Growing demand for plant-based and hybrid protein products

Growing demand for plant-based and hybrid protein products is a key factor influencing the development of the Japan protein market. Consumers are increasingly seeking nutrition solutions that offer health benefits, sustainability, and dietary flexibility. While animal protein remains a staple in traditional diets, there is a growing acceptance of plant-based proteins such as soy, pea, rice, and algae, especially when these are marketed as complementary rather than complete substitutes. This trend has driven the rise of hybrid protein formulations, which combine plant proteins with animal-derived proteins like whey or collagen. These formulations aim to improve amino acid profiles, digestibility, and taste while reducing dependence on single-source proteins. Additionally, increasing awareness of digestive health, cholesterol management, and environmental sustainability is encouraging consumers to diversify their protein sources. Food and beverage manufacturers are actively responding to these shifts in consumer preferences by innovating new product offerings, reformulating existing products, and investing in research to meet the evolving demands of the market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taste, texture, and sensory acceptance challenges | -0.8% | National, particularly affecting plant-based and insect protein segments | Medium term (2-4 years) |

| Digestive sensitivity among elderly consumers | -0.7% | National, concentrated in population aged 65+ years | Long term (≥ 4 years) |

| Regulatory complexity for functional and health claims | -0.6% | National, affecting all novel protein ingredients and functional claims | Medium term (2-4 years) |

| Limited protein intake awareness relative to dietary norms | -0.4% | National, most pronounced in rural areas and among elderly population | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Taste, texture, and sensory acceptance challenges

Taste, texture, and sensory acceptance challenges are significant restraints in the Japan protein market, as consumer purchase decisions are heavily influenced by flavor authenticity, mouthfeel, and overall eating experience. Japanese consumers are highly particular about sensory quality, often expecting protein-enriched products to meet the same standards as traditional foods in terms of taste, aroma, and texture. Many protein formulations, particularly plant-based, microbial, and hybrid proteins, face issues such as bitterness, beany or earthy off-notes, chalky mouthfeel, or excessive thickness, which can deter repeat purchases. These sensory challenges are especially pronounced in ready-to-drink beverages, bakery products, and functional snacks, where protein inclusion can disrupt texture and flavor balance. Furthermore, elderly consumers, a key demographic for protein-fortified foods, are especially sensitive to texture and palatability, favoring smooth, mild, and easy-to-swallow formats, which limits formulation flexibility.

Regulatory complexity for functional and health claims

Regulatory complexity surrounding functional and health claims poses a significant restraint on the Japan protein market. Japan enforces one of the most stringent and detailed regulatory frameworks for foods, supplements, and functional ingredients. Protein products marketed with health, functional, or preventive benefits must adhere to various regulatory pathways, including Foods for Specified Health Uses (FOSHU), Foods with Function Claims (FFC), and general food labeling standards. Each pathway requires extensive scientific substantiation and documentation, creating significant challenges for manufacturers. This complexity often leads to prolonged approval processes, high compliance costs, and reduced flexibility in marketing communication, particularly for emerging protein sources such as microbial, insect, or hybrid proteins. Additionally, the need to navigate overlapping regulations and ensure compliance with evolving standards further complicates market entry. Manufacturers must carefully align scientifically accurate claims with regulatory requirements, which can dilute consumer-facing messaging, hinder product differentiation, and slow innovation in the market.

Segment Analysis

By Source Type: Fermentation Drives Next-Generation Proteins

In 2025, animal protein accounted for a substantial 32.56% share of the Japan protein market, highlighting its continued preference among Japanese consumers. This dominance is largely attributed to the perception of animal proteins, such as whey, casein, collagen, and egg proteins, as high-quality, complete proteins that supply all essential amino acids required for muscle development, recovery, and overall health. The aging population in Japan further drives demand, as older adults increasingly adopt protein-rich diets to address sarcopenia and maintain bone and muscle health. Additionally, the growing fitness and sports nutrition trend has bolstered animal protein consumption, with gym-goers, athletes, and active individuals favoring whey and casein-based supplements for their benefits in muscle repair and sustained energy.

Microbial protein is emerging as the fastest-growing segment in the Japan protein market, with a projected CAGR of 5.64% through 2031. This growth is fueled by its alignment with Japan’s priorities in food security, sustainability, and technological innovation. Advancements in biotechnology and fermentation processes have enabled the efficient production of high-purity proteins from microorganisms such as yeast, fungi, bacteria, and algae. Unlike traditional animal protein, microbial protein offers consistent quality, controlled production conditions, and reduced susceptibility to agricultural variability, making it well-suited for industrial-scale applications. The segment’s expansion is further supported by Japan’s robust Researh and Development (R&D) ecosystem and government initiatives promoting alternative protein development as part of future food systems.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Cosmetics Outpaces Food in Growth

In 2025, the food and beverages segment accounted for a significant 68.58% market share, solidifying its position as the cornerstone of the Japan protein market. This dominance is attributed to the widespread integration of protein into daily dietary habits, as consumers increasingly prioritize nutritional enhancement through regular food consumption rather than standalone supplements. Protein-enriched foods and beverages are favored for their convenience, familiarity, and ease of incorporation into daily routines. The growing demand for functional and health-oriented foods has further propelled protein inclusion as a key ingredient, aligning with consumer preferences for preventive nutrition and balanced diets. Manufacturers are focusing on clean-label formulations, improved taste profiles, and multifunctional benefits, enabling protein to be seamlessly incorporated into mainstream food and beverage products.

The cosmetics and personal care segment is the fastest-growing application in the Japan protein market, projected to expand at a CAGR of 6.45% through 2031. This growth is primarily driven by the increasing use of marine collagen peptides in anti-aging skincare, hair care formulations, and ingestible beauty supplements. Japan’s strong "beauty-from-within" culture has fostered the convergence of nutrition and cosmetics, positioning protein-based ingredients as essential components. These proteins are increasingly utilized in premium anti-aging serums due to their high bioavailability, clean sensory profile, and strong consumer trust in marine-derived ingredients. The segment’s growth is further supported by Japan’s premiumization trend in personal care, where consumers actively seek scientifically validated, functional, and age-defying formulations over conventional cosmetic solutions. This trend is reflected in trade data, as Japan Customs reported that the import value of cosmetics into Japan reached approximately JPY 446.1 billion in 2024, underscoring the robust demand for advanced, high-value cosmetic products that increasingly incorporate protein-based actives [3]Source: Japan Customs, "Import value of cosmetics to Japan", customs.go.jp.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Japan's protein market demonstrates significant regional differences, influenced by variations in demographic profiles, industrial concentration, retail infrastructure, and lifestyle preferences. Urban areas benefit from dense populations, advanced distribution systems, and greater exposure to functional foods, sports nutrition, and premium wellness products. In contrast, rural regions exhibit demand patterns focused on aging-related nutrition and essential dietary supplementation. These regional disparities affect consumption volumes, preferred product formats, protein sources, and the adoption of innovations, resulting in a geographically diverse market structure.

The Greater Tokyo Area, along with Osaka and the Kansai region, serves as the primary demand hub for the protein market. High urbanization, frequent purchasing behavior, and rapid adoption of nutrition trends characterize these metropolitan areas. Fitness centers, specialty retailers, convenience food outlets, and innovation-driven foodservice channels are concentrated in these regions, driving strong demand for protein-enriched foods, ready-to-drink beverages, and lifestyle-focused nutrition products. Consumers in urban Japan show a preference for hybrid proteins, clean-label formulations, and functional claims related to performance, beauty, and preventive health. These factors position urban areas as key testing grounds for new protein concepts and premium offerings.

In contrast, regions such as Hokkaido and rural prefectures, including aging-intensive areas like Akita and Shimane, exhibit demand patterns centered on nutritional needs rather than lifestyle preferences. These areas face accelerated population aging and limited retail diversification, leading to a stronger reliance on protein-fortified staple foods, clinical nutrition products, and easily digestible formats designed for muscle maintenance and general health. Although innovation adoption is slower in these regions, they remain critical demand centers for functional and medical nutrition, highlighting protein's role in addressing Japan's long-term demographic challenges.

Competitive Landscape

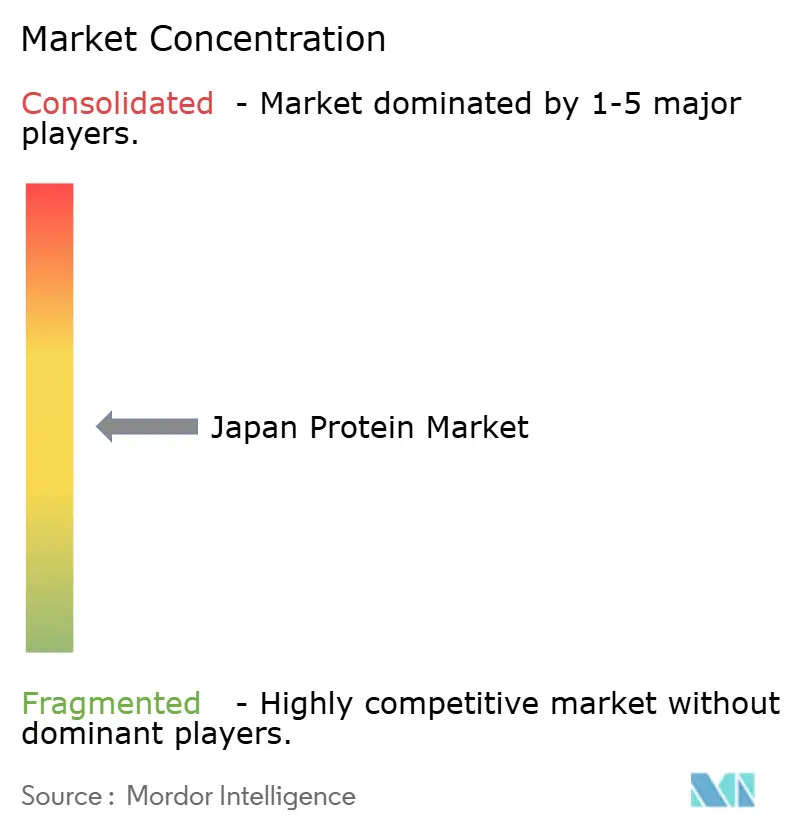

The Japan protein market is moderately concentrated, with a limited number of multinational ingredient suppliers operating alongside strong domestic specialists. Key players in the market include Archer Daniels Midland Company, Arla Foods amba, Bunge Limited, Fuji Oil Holdings Inc., and Darling Ingredients Inc. These companies leverage vertically integrated supply chains, diversified protein portfolios, and technical expertise to cater to various end-use applications, including food and beverages, nutrition, cosmetics, and pharmaceutical formulations.

Within the market, opportunities are emerging in hybrid protein formats that combine plant- and animal-derived proteins. These formats deliver complete amino acid profiles while maintaining taste, texture, and digestibility. This approach appeals to flexitarian consumers who prioritize nutritional balance and sustainability but are not ready to fully adopt plant-based diets. Hybrid proteins help suppliers address sensory challenges associated with single-source formulations while maintaining consumer trust and familiarity.

Technological advancements are reshaping competitive dynamics, emphasizing advanced processing and functional innovation. Enzymatic hydrolysis and fermentation technologies enable suppliers to fractionate proteins into bioactive peptides with targeted health benefits, such as muscle maintenance, skin health, digestive support, and metabolic function. These innovations allow protein ingredients to transition from basic nutritional products to high-value, science-backed applications, enhancing supplier relevance in functional foods, beauty-from-within products, and clinical nutrition.

Japan Protein Industry Leaders

-

Archer Daniels Midland Company

-

Arla Foods amba

-

Bunge Limited

-

Fuji Oil Holdings Inc.

-

Darling Ingredients Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Leaft Foods has collaborated with Lacto Japan, a distributor and producer of specialty food ingredients, to advance the commercialization of its innovative Rubisco Protein Isolate for use in Japanese food manufacturing.

- February 2025: Kinish, a company specializing in plant molecular farming to produce milk proteins, has raised JPY 120 million in a seed funding round. The funds will be utilized to advance research and development efforts in casein production and plant factory operations.

Japan Protein Market Report Scope

Protein ingredients are derived from various animal, plant, and microbial sources that are often used to enhance the functional properties of foods, beverages, personal care products, and animal feed.

The Japan protein market is segmented based on the source and application. Based on the source, the market is segmented into animal, microbial, insects, and plant. Based on the application, the market is segmented into food and beverages, nutritional supplements, animal feed, cosmetics and personal care, pharmaceuticals, and others.

The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

By Source Type

| Animal |

| Microbial |

| Insects |

| Plant |

By Application

| Food and Beverages |

| Nutritional Supplements |

| Animal Feed |

| Cosmetics and Personal Care |

| Pharmaceutical |

| Others |

| By Source Type | Animal |

| Microbial | |

| Insects | |

| Plant | |

| By Application | Food and Beverages |

| Nutritional Supplements | |

| Animal Feed | |

| Cosmetics and Personal Care | |

| Pharmaceutical | |

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Japan protein market in 2026?

The Japan protein market size reached USD 564.92 million in 2026 and is projected to continue growing at a 5.23% CAGR.

Which source type is expanding fastest?

Microbial protein is the fastest-growing source, forecast to rise at a 5.64% CAGR through 2031 as fermentation capacity scales.

Why is collagen popular in Japan?

Marine collagen from salmon and tuna skins offers high bioavailability and aligns with beauty-from-within trends, driving strong demand in cosmetics and supplements.

What is the main barrier to plant protein adoption?

Sensory challenges such as beany flavor and grittiness limit inclusion rates, although masking technologies are improving acceptance.

Page last updated on: