Market Trends of Japan Property & Casualty Insurance Industry

This section covers the major market trends shaping the Japan Property & Casualty Insurance Market according to our research experts:

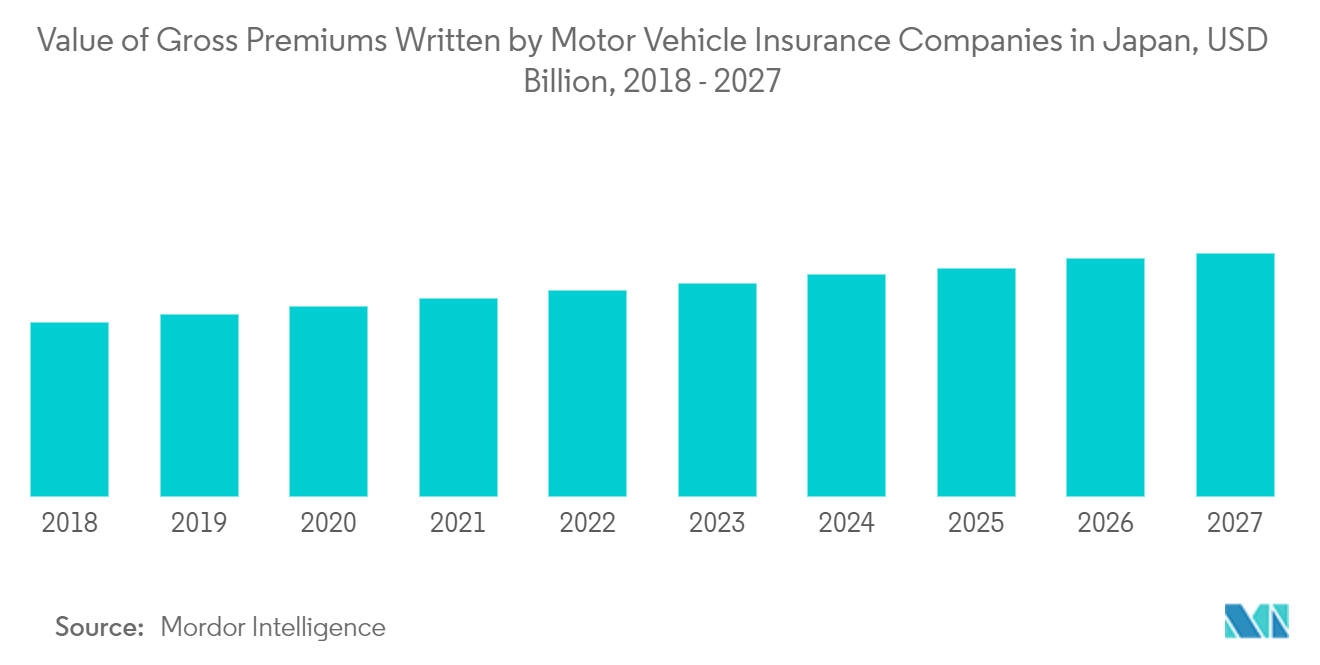

Status of Automobile Insurance in Japan

In Japan, automotive insurance (including mandatory automobile liability insurance) accounts for 60% of net premiums. Premiums are calculated using a "grading system" based on the accident histories of policyholders. Agencies dominate auto insurance sales. Direct sales are expanding at a rate of roughly 4%.

Motor insurance demand is expected to decline in the long run due to Japan's shrinking population and well-developed public transportation system. The development of autonomous driving technologies will likely expand the demand for product liability insurance, telematics automobile products, and cyber protection.

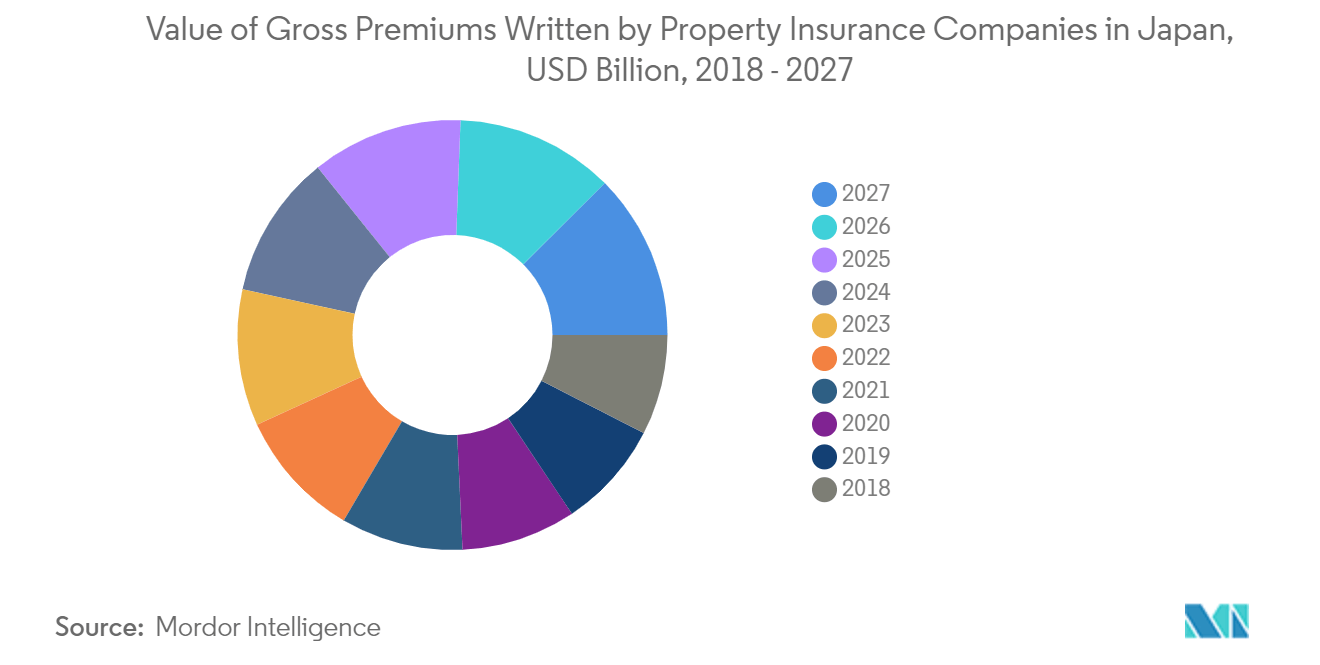

Status of Property Insurance in Japan

Wind and flooding damage is also covered by fire insurance in Japan. In the fiscal year ending 31 March 2017, fire insurance accounted for 15% of total premium income, making it the second most profitable business line behind auto insurance. However, it is the least profitable of the primary lines of business and has been losing money on underwriting for many years. Japanese non-life insurers raised their fire insurance premiums for homes by a national average of 6 to 8% in January 2021. The premium hikes were made in response to a string of natural disasters, such as torrential rains in western Japan and Typhoon Jebi, which caused heavy damage to Kansai International Airport in 2018. Insurance premiums are expected to rise mainly in the disaster-hit western areas of the country. Some expect an increase of over 10%, depending on the location and building. Insurance payouts exceeded JPY 1 trillion in 2019 because many houses were damaged in disasters, including Typhoon Faxai.

Earthquake insurance is a type of insurance that covers only earthquake disasters. It covers damage caused by fire, destruction, burying, or washing away because of an earthquake or volcanic eruption, as well as a tsunami resulting from either of these events. Earthquake Insurance covers buildings for residential use as well as household valuables. It is attached to fire insurance. Namely, it is a prerequisite to carry fire insurance to carry Earthquake Insurance. Fire insurance policyholders without Earthquake Insurance can attach it midway through the policy period. The Earthquake Insurance, whose objective is to stabilize the livelihoods of those affected by earthquakes, is established with the government reinsuring massive earthquake damage, which exceeds a certain amount of liability that private insurance companies underwrite. The limit is JPY 11.7751 trillion. Combined with the liability sharing for private insurance companies, the limit on total payouts for a single earthquake, etc., sums to JPY 12 trillion.