Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

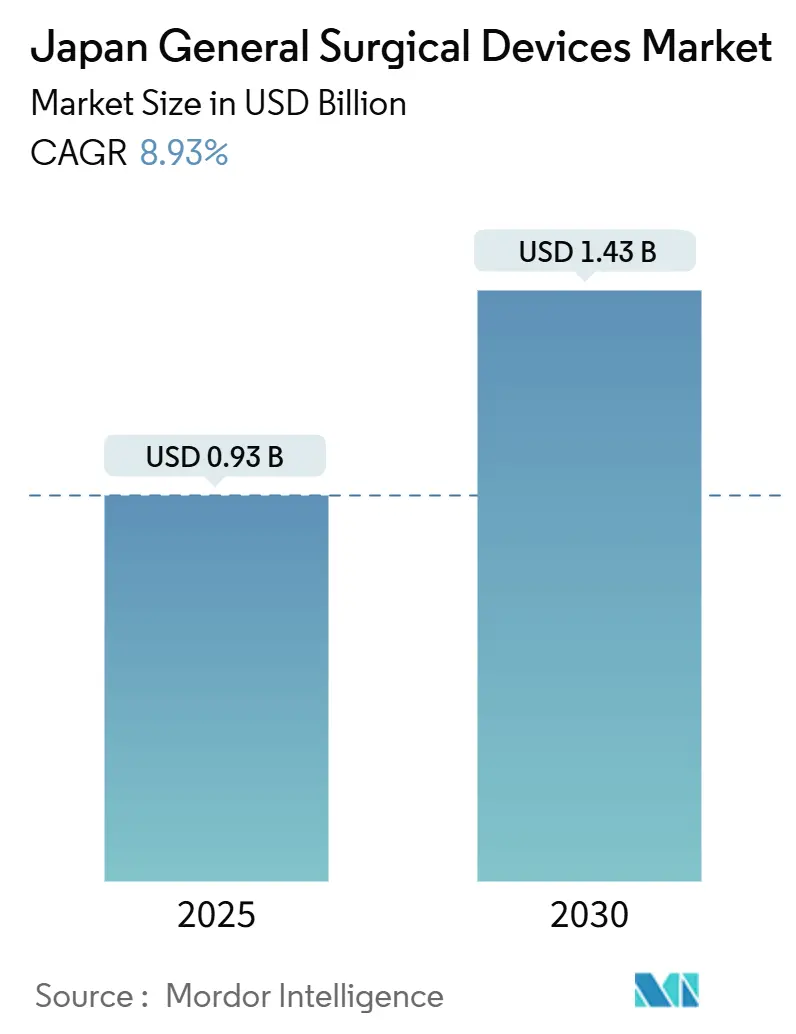

| Market Size (2025) | USD 0.93 Billion |

| Market Size (2030) | USD 1.43 Billion |

| Growth Rate (2025 - 2030) | 8.93% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan General Surgical Devices Market Analysis by Mordor Intelligence

The Japan General Surgical Devices Market size is estimated at USD 0.93 billion in 2025, and is expected to reach USD 1.43 billion by 2030, at a CAGR of 8.93% during the forecast period (2025-2030). Growing surgical demand from an aging society where 29.1% of citizens are 65 years or older, an aggressive shift toward minimally invasive techniques, and the country’s deep bench strength in robotics and artificial intelligence are the foundational forces that keep the market on a steep upward path. Hospitals are scaling integrated digital operating rooms, private investors are funding ambulatory surgical centers, and government policies that reimburse remote proctoring are accelerating technology diffusion. Laparoscopic systems remain the revenue anchor, yet electrosurgical platforms paired with robotic consoles are setting the growth pace. Domestic manufacturers such as Olympus and Terumo secure share through local service networks, while global leaders work through strategic partnerships and Japan’s demanding approval pathway to keep competitive parity. Supply-chain re-shoring incentives, telepresence-enabled training models, and fast prototype–to-pilot cycles in university hospitals collectively create fertile ground for next-generation devices that embed imaging, analytics, and automation at the point of care.

Key Report Takeaways

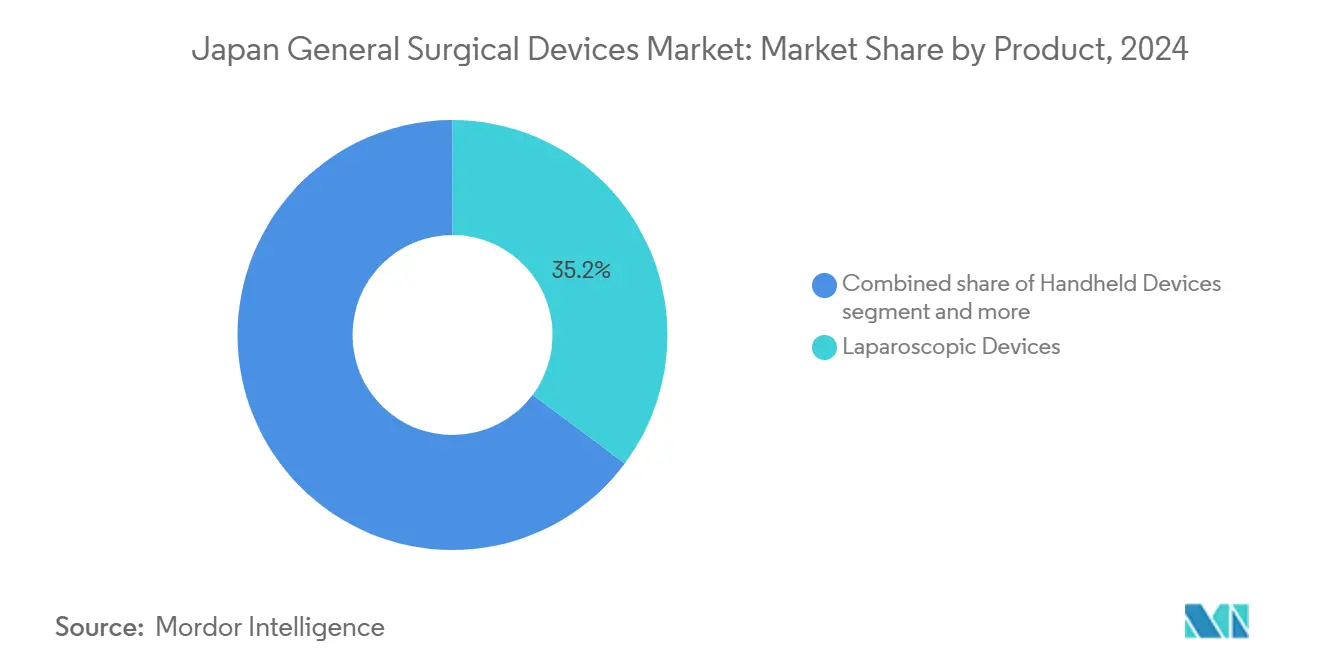

- By product, laparoscopic devices led with 35.16% revenue share in 2024; electrosurgical devices are projected to advance at a 9.82% CAGR through 2030.

- By procedure approach, minimally invasive surgery accounted for 72.74% of the Japan general surgical devices market share in 2024, while the same category posts the highest projected 9.52% CAGR to 2030.

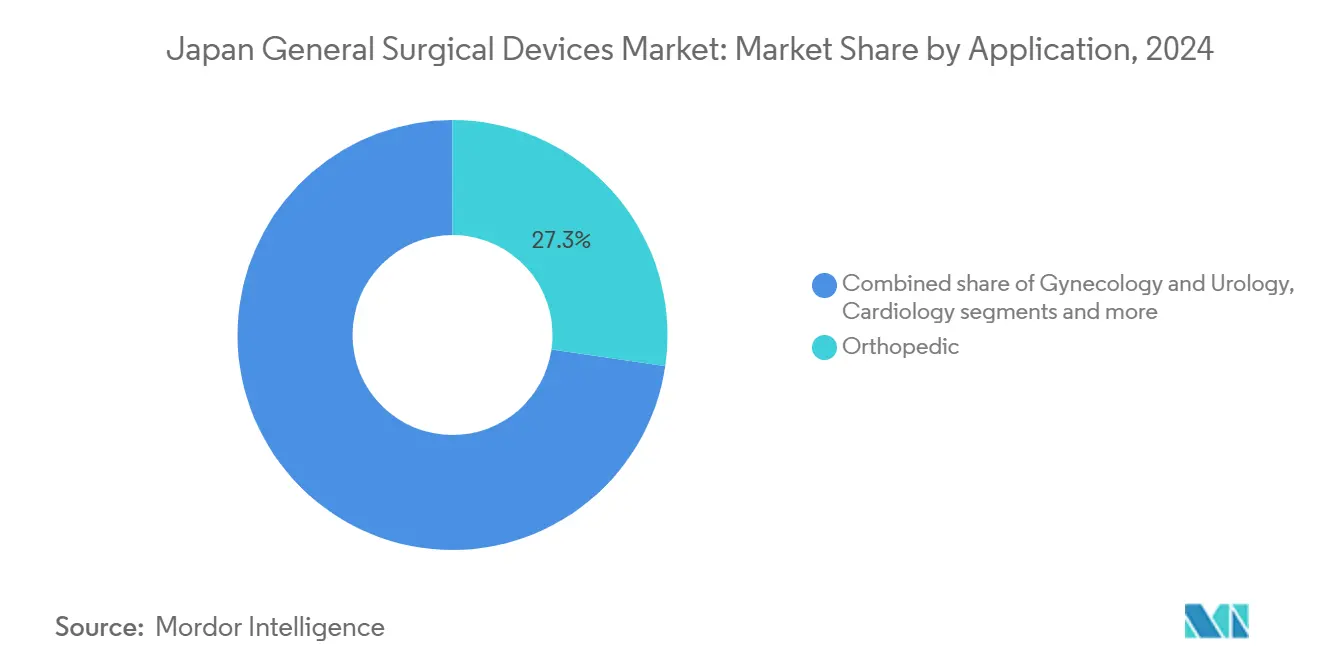

- By application, orthopedic procedures held 27.32% of the Japan general surgical devices market size in 2024 and gynecology and urology is growing at a 10.17% CAGR to 2030.

- By end-user, hospitals controlled 70.37% revenue share in 2024; ambulatory surgical centers are forecast to expand at a 10.01% CAGR through 2030.

Japan General Surgical Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-driven escalation in surgical volumes | +2.1% | National, with concentration in Tokyo, Osaka, Nagoya metropolitan areas | Long term (≥ 4 years) |

| Surge in minimally invasive procedures | +1.8% | National, with early adoption in university hospitals and private facilities | Medium term (2-4 years) |

| Rapid device innovation (robotics, AI, 4K/8K imaging) | +1.5% | National, with pilot programs in major medical centers | Medium term (2-4 years) |

| Remote-proctoring reimbursement accelerating adoption | +1.2% | National, with rural hospital priority implementation | Short term (≤ 2 years) |

| Domestic manufacturing-reshoring incentives | +0.9% | National, with focus on industrial clusters in Kyushu and Tohoku | Long term (≥ 4 years) |

| Expansion of private hospitals and ambulatory surgical centers | +0.7% | Urban areas, particularly Tokyo, Osaka, and regional capitals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging-driven escalation in surgical volumes

Japan’s demographic curve now places 20% of citizens in the 75-plus segment, pushing hospital case mix toward complex, multi-morbidity surgeries that rely on precise, low-trauma instrumentation.[1]Source: Statistics Bureau of Japan, “Statistical Handbook of Japan 2024,” stat.go.jp Older patients present higher perioperative risk, raising the premium on devices that shorten procedure times and reduce blood loss. Multicenter evidence shows that laparoscopic gastric cancer resections deliver 99.8% five-year disease-free survival, reinforcing confidence in minimally invasive approaches for senior cohorts. Workforce gaps intensify the imperative for robotic assistance that lets a leaner clinical team maintain throughput. Device makers that bundle analytics for pre-operative planning with ergonomic instruments positioned for arthritic hands are meeting an urgent and escalating need.

Surge in minimally invasive procedures

Minimally invasive surgery already dominates operating rooms and keeps growing as AI-driven visualization, 3-D mapping, and robotics tilt the risk-to-benefit ratio further in its favor. A comparative study of elderly liver resection patients showed no difference in complications versus younger cohorts, validating broader use in the oldest demographic. Tokyo startups now supply algorithms that illuminate loose connective tissue planes with 91.8% accuracy, reducing inadvertent injury and shortening learning curves. Office-based vitreoretinal surgery reached a single-session success rate of 97.3%, demonstrating how refined instruments migrate complex care from hospitals to outpatient suites. As clinical guidelines update, procurement cycles increasingly favor consoles and handpieces with plug-and-play AI modules that can be upgraded through software rather than hardware swaps.

Rapid device innovation (robotics, AI, 4K/8K imaging)

Japan’s intertwined electronics and medical technology clusters accelerate cross-domain breakthroughs. The hinotori Surgical Robot obtained domestic clearance with eight-axis arms and native 3-D vision. Sony’s microsurgery robot uses automatic instrument exchange to cut setup time and adds real-world haptics to featherweight movements. Thoracic surgery trials with the Saroa robot introduced force feedback that protects fragile tissue, an advance especially relevant for novice surgeons. Parallel progress in 4K and 8K endoscopes gives surgeons ultra-high-definition fields that improve margin assessment. These converging technologies reset procurement criteria toward platforms that integrate optics, navigation, and automation in a single ecosystem.

Remote-proctoring reimbursement accelerating adoption

A 2024 policy gave hospitals a clear reimbursement code for remote surgical guidance, letting one expert mentor multiple theaters simultaneously. Early 5G-enabled simulations completed without latency that might compromise patient safety. Rural centers now access skills previously concentrated in metropolitan teaching hospitals. Device developers respond by embedding cameras, dual-control modes, and encrypted data streams in consoles at the design stage. This policy lifts near-term demand because hospitals can justify capital spend with immediate utilization uplift.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy PMDA approval & re-approval timelines | -1.4% | National, affecting all device categories and manufacturers | Medium term (2-4 years) |

| High cost of stem cell therapies and manufacturing | -0.8% | National, with particular impact on advanced therapy segments | Long term (≥ 4 years) |

| OR nursing/technician shortages | -1.1% | National, with acute impact in rural and mid-tier hospitals | Short term (≤ 2 years) |

| Limited standardization and scalability | -0.6% | National, affecting device interoperability and training programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthy PMDA approval & re-approval timelines

Despite recent Sakigake and fast-track schemes, the median 12-month technical review for Class II–III devices plus quality-system audits slows commercial launches. Inventors must budget for local clinical data, bilingual dossiers, and five-year quality re-certifications that divert capital from innovation. Smaller firms face disproportionate burden, narrowing the competitive field and occasionally delaying novel tools that could raise procedural safety.

OR nursing & technician shortages

Work style reform caps physician overtime, and the national nurse vacancy rate keeps climbing, particularly in surgery-intensive rural prefectures. During the 2024 Noto earthquake response, Kanazawa Medical University Hospital treated 421 trauma patients yet reported operating room staffing strain that limited elective cases for weeks.[2]Source: Uramoto H. et al., “Initial Response to the 2024 Noto Earthquake,” Scientific Reports, nature.com Hospitals therefore prioritize devices that cut cycle time, automate camera control, and simplify instrument exchange, yet absolute capacity caps still temper procedure volume growth.

Segment Analysis

By Product: Laparoscopic Dominance Faces Electrosurgical Innovation

Laparoscopic systems held 35.16% revenue leadership in 2024, underscoring their entrenched role across gastrointestinal, bariatric, and hepatobiliary specialties. Over 700 hospitals now staff fellowship-trained laparoscopic surgeons, and five-year survival data reinforce the modality’s oncologic adequacy. The segment attracts upgrades to 4K cameras and articulating instruments, driving replacement cycles rather than first-time adoption. Handheld graspers and staplers maintain steady base demand, while wound-closure kits grow along with overall surgical volume. Trocars, insufflators, and access devices post mid-single-digit growth as procedural mix extends to colorectal, urologic, and gynecologic indications.

Electrosurgical platforms, although smaller today, expand at 9.82% and anchor the pivot toward fully digital suites. Integrated generators sync with robotic arms, detect tissue impedance, and auto-adjust energy delivery to minimize thermal spread. As these systems pair with AI algorithms that predict optimal coagulation settings, procedure times drop and consistency rises. Robotic and computer-assisted microscopes further blur traditional product lines, making energy systems a core module in smart OR ecosystems. Other niche tools, from fluorescence-guided clips to vessel sealing pens, capitalize on Japan’s appetite for specialized upgrades that boost precision without large workflow disruption. The transition signals that market value migrates from single-function devices to platform compatibility and software-driven enhancements.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Procedure Approach: Minimally Invasive Surgery Reshapes Standards

Minimally invasive surgery encompassed 72.74% of all operations in 2024 and sustains a 9.52% CAGR as evidence keeps mounting for shorter stays, lower infection rates, and faster return to work. AI-modified visualization now identifies dissection planes, and standardized two-surgeon robot techniques in liver resection cut median operative time to 156 minutes with negligible complications.

Open surgery, while shrinking in relative terms, remains imperative for emergencies and late-stage malignancies. Hospitals therefore still procure high-throughput suction devices, lights, and retractors tailored for open fields, yet budgets shift incrementally toward laparoscopic stacks and robotic carts. Cross-training programs let surgeons alternate between open and laparoscopic techniques, sustaining a baseline for instrument demand across both categories. The outlook suggests that the binary open-versus-laparoscopic framing will fade, replaced by an integrated workflow where digital adjuncts optimize every incision size.

By Application: Orthopedic Leadership Meets Gynecology Growth

Orthopedic cases generated 27.32% of 2024 revenue as hip, knee, and spine surgeries rise with demographic joint degeneration. Japan general surgical devices market share for orthopedic applications remains high because advanced navigation and cementless implants lengthen prosthesis life. Robotic arms calibrate bone cuts within sub-millimeter tolerance, while patient-specific guides trim OR minutes and inventory. Cardiology interventions follow, supported by surgical patches and vessel sealing innovations. Neurology procedures adopt AI for trajectory planning in tumor resection, although the sub-segment stays smaller in revenue terms.

Gynecology and urology register the fastest 10.17% CAGR as robotic pelvic surgery gains insurer acceptance. Comparative studies show robotic lymph node dissection retrieves more nodes than conventional laparoscopy without added morbidity. Thulium-fiber laser adoption in kidney stone management halves basketing time and cuts thermal injury risk. Cross-fertilization of tools, such as flexible scopes originally designed for colorectal work now repurposed for hysterectomy, stimulates accessory sales. Other smaller applications, including thoracic and bariatric surgery, benefit from high-definition scopes and advanced staplers that shorten staple lines and lower leak rates.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: Hospital Dominance Challenged by ASC Innovation

Hospitals controlled 70.37% of 2024 revenue as tertiary centers bundle surgery with critical care, imaging, and oncology follow-up. This segment is anticipated to grow substantially as bed tower expansions are completed in Tokyo and Osaka. University hospitals pioneer smart OR deployments with ceiling-mounted 3-D cameras and integrated dashboards that pull lab and radiology data into real-time displays.

Ambulatory surgical centers grow at 10.01% because same-day reimbursement models align with minimally invasive techniques that require shorter observation. Devices purchased by ASCs emphasize portability, touchscreen interfaces, and rapid sterilization turnaround. Specialty clinics, often physician-owned, extend emergency capabilities with hospital-grade anesthesia machines, showing how advanced gear migrates into community settings. Procurement managers in these centers prioritize vendor service responsiveness and modular warranties that match tighter cash-flow models. The shifting end-user mix motivates manufacturers to design scalable platforms that deliver identical performance in 20-square-meter ORs and in 100-square-meter hybrid suites.

Geography Analysis

Japan’s surgical device demand clusters around the Tokyo, Osaka, and Nagoya metropolitan corridors where population density, teaching hospitals, and venture funding converge. Metropolitan hubs pilot novel robotics under joint studies between device start-ups and academic surgeons, shortening bench-to-bedside cycles. Rural prefectures, by contrast, grapple with surgeon shortages and rely on 5G telepresence consoles linked to urban experts. The Ministry of Economy, Trade and Industry underwrites regional factory upgrades so that Kyushu optics makers and Tohoku precision-machining firms can supply domestic surgical robots, reinforcing strategic autonomy.

Cross-regional policy such as remote-proctoring reimbursement reduces outcome disparities because a senior surgeon in Tokyo can mentor three rural rooms in real time. Post-earthquake response in Ishikawa Prefecture showed that hospitals equipped with mobile laparoscopic towers resumed elective operations sooner than open-only facilities, reinforcing the link between device flexibility and system resilience.

Foreign entrants often base market access teams in Osaka’s International Business District, leveraging the upcoming Japan Health 2025 showcase to display prototypes before formal PMDA filing. Domestic champions such as Olympus post 11% of global revenue inside Japan and use proximity to customers for iterative design feedback. Terumo leverages its Tokyo R&D hub to co-create catheter-based platforms that can be bundled with vascular closure tools in unified tenders. The geographic landscape therefore merges concentrated innovation islands with broad national demand, requiring supply chains that can quickly replenish consumables and field-service engineers nationwide.

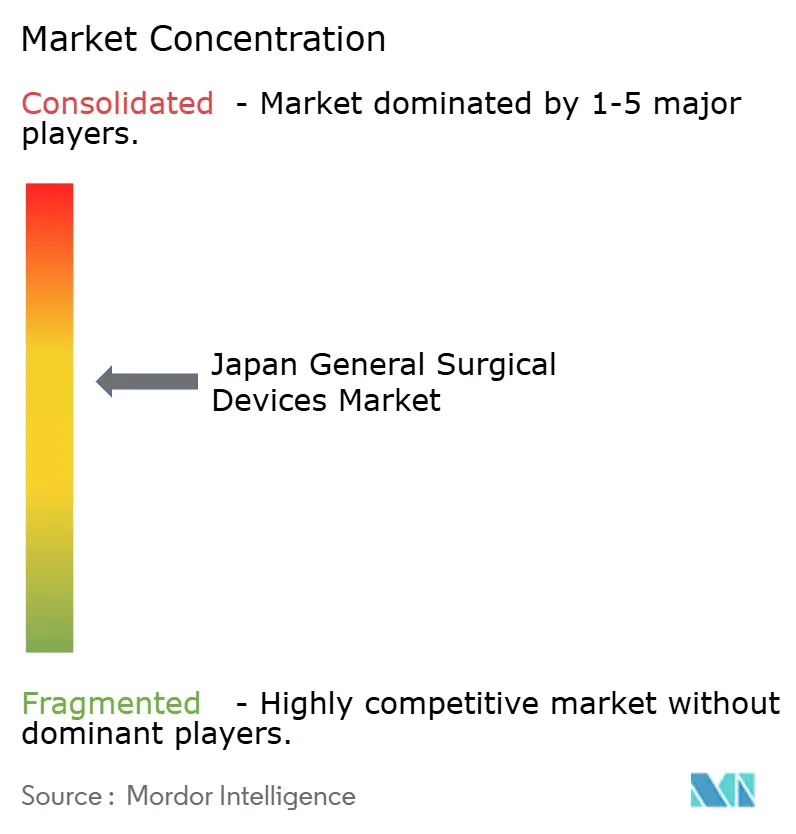

Competitive Landscape

The Japan general surgical devices market displays a moderate concentration where start-ups and technology entrants increase churn through niche breakthroughs. Olympus leverages endoscopic imaging dominance and 4K product cycles to defend installed base contracts, capturing 11% of global revenue domestically. Terumo aligns catheter innovations with automated vascular closure systems and partners with contract research firm NAMSA to shorten trial timelines for combination products.

Intuitive Surgical keeps da Vinci console placements steady by rolling out dual-console training packages, yet faces competition from Medicaroid’s hinotori and Sony’s microsurgery robots built for Japanese ergonomics. Johnson & Johnson MedTech integrates DePuy implants with Ethicon energy systems through the Polyphonic digital ecosystem that shares analytics in real time across device families, raising switching costs for hospitals. Stryker’s next-generation Mako platform with multi-joint capabilities strengthens orthopedic footprints and ties implant sales to capital equipment.

Domestic electronics giants entering robotics alter the power balance because they bring advanced sensor, actuator, and camera know-how plus consumer-grade manufacturing scale. Start-ups such as Riverfield and F.MED target thoracic and micro-surgery niches with force feedback and mini-scale arms that fit smaller ORs, catching interest from venture funds aligned with national industrial policy. Foreign mid-caps seeking entry often collaborate with local distributors to navigate PMDA filings and hospital group purchasing organizations. Competitive advantage therefore shifts toward ecosystem depth: companies able to fuse instruments, software, and services into a single subscription-compatible offer are set to widen their edge as reimbursement models favor outcome-based payments.

Japan General Surgical Devices Industry Leaders

-

Boston Scientific Corporation

-

Medtronic plc

-

B. Braun SE

-

Johnson & Johnson (Ethicon & DePuy Synthes)

-

Stryker Corp.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Juntendo University Hospital and Intuitive Surgical agreed to open Japan’s first da Vinci Total Program Observation Site to train multi-department teams and expand robotic surgery capacity.

- May 2024: OrthAlign launched its Lantern navigation system in Japan through its longstanding distribution partner, adding to the orthopedic digital toolkit.

- April 2024: Asensus Surgical signed a lease deal with Sendai Tokushukai Hospital for a Senhance Surgical System, marking continued placement of digital-laparoscopy consoles.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study classifies the Japan general surgical devices market as every reusable or single-use instrument or powered platform whose primary intent is to cut, dissect, seal, or provide access during open or minimally invasive procedures performed in Japanese hospitals, ambulatory surgical centers, and specialty clinics. This definition bundles handheld instruments, laparoscopic sets, electrosurgical generators, wound-closure consumables, trocars, and robotic or computer-assisted systems.

Scope Exclusions: equipment dedicated to ophthalmic, dental, or veterinary surgery and stand-alone imaging towers are not counted.

Segmentation Overview

- By Product

- Handheld Devices

- Laparoscopic Devices

- Electrosurgical Devices

- Wound-Closure Devices

- Trocars and Access Systems

- Robotic and Computer-Assisted Systems

- Other Devices

- By Procedure Approach

- Open Surgery

- Minimally Invasive Surgery

- By Application

- Gynecology and Urology

- Cardiology

- Orthopedic

- Neurology

- Other Applications

- By End-User

- Hospitals

- Ambulatory Surgical Centres

- Specialty Clinics

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed colorectal and orthopedic surgeons, supply-chain heads of large hospital groups, leading distributors, and regulatory consultants across Kanto, Kansai, and Kyushu. These conversations verified robotic adoption rates, replacement cycles for laparoscopic kits, and price gaps between imported and domestic devices, helping us close information gaps flagged in secondary work.

Desk Research

We extracted foundational inputs from tier-1 public sources such as the Ministry of Health, Labor and Welfare inpatient procedure tables, OECD Health Accounts, UN Comtrade import codes 9018/901890, PMDA approval logs, and Japan Surgical Society journals, which together map unit flows, price corridors, and regulatory cadence. Company 10-Ks, hospital procurement tenders, and news feeds accessed through D&B Hoovers and Dow Jones Factiva sharpened revenue splits and pricing trends. The sources cited are illustrative; numerous additional materials informed data gathering, validation, and clarification.

Market-Sizing & Forecasting

A top-down build converts national surgical case volumes into device demand pools; selective bottom-up supplier roll-ups plus sampled ASP x volume checks reconcile totals. Key variables include annual general surgery caseloads, >=65-year population share, device replacement intervals, import tariff shifts, and PMDA clearance lead times. Forecasts employ multivariate regression tied to procedure growth and demographic expansion, with scenario analysis layering reimbursement or regulatory shocks. Data voids in supplier granularity are bridged through channel checks and documented triangulation.

Data Validation & Update Cycle

Outputs undergo variance scans versus five-year historical trends, currency translation audits, and peer estimates before senior review. Models refresh annually, with interim patches when material events, large recalls or tariff changes, trigger re-contacts so clients receive the latest baseline.

Why Mordor's Japan General Surgical Devices Baseline Is Dependable

Published estimates often diverge because analysts bundle wider device families, apply differing exchange rates, or lock in older base years.

Key Gap Drivers: some studies mix implants and consumables, others omit high-ticket robotics, and a few rely on headline import spend without unit calibration, which inflates or suppresses totals. Mordor's disciplined scope, annual refresh, and dual-path modeling keep our figure balanced and traceable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.93 B (2025) | Mordor Intelligence | - |

| USD 7.89 B (2024) | Global Consultancy A | Bundles broader medical device classes and hospital capex pools |

| USD 0.66 B (2023) | Regional Consultancy B | Excludes robotic systems and uses older base year |

| USD 1.50 B (2024) | Trade Journal C | Conservative caseload growth assumptions and static ASPs |

In sum, our calibrated middle path offers decision-makers a transparent, reproducible baseline that sits between inflated spend figures and overly narrow component counts.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Japan general surgical devices market?

The Japan general surgical devices market size is USD 0.93 billion in 2025 and is forecast to reach USD 1.43 billion by 2030.

Which product segment leads revenue in Japan’s surgical device space?

Laparoscopic devices held 35.16% share in 2024, the highest among all product categories.

Why are ambulatory surgical centers growing faster than hospitals?

Same-day reimbursement models combined with minimally invasive techniques drive a 10.01% CAGR for ambulatory centers, compared with slower growth for hospital operating suites.

What regulatory hurdle most affects new device launches in Japan?

Lengthy Pharmaceutical and Medical Devices Agency approval and re-approval cycles, often taking 12 months or more, remain the biggest barrier for innovative entrants.

How does Japan’s aging population influence surgical device demand?

With 20% of residents already 75 years or older, procedure complexity and volume rise sharply, pushing hospitals to adopt robotic and AI-enhanced systems that maintain quality while easing workforce strain.

Which application area is expanding fastest?

Gynecology and urology surgeries, powered by robotic assistance and better imaging, are growing at 10.17% per year through 2030.

Page last updated on: