| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 23.25 Billion |

| Market Size (2030) | USD 26.33 Billion |

| CAGR (2025 - 2030) | 2.52 % |

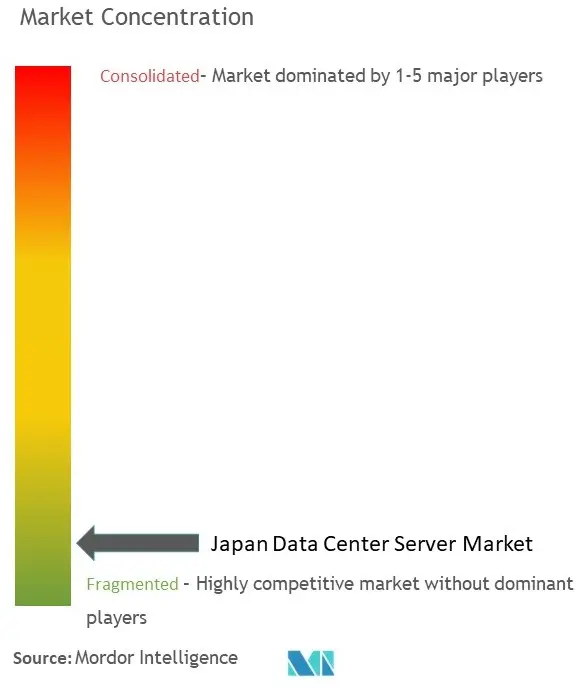

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Japan Data Center Server Market Analysis

The Japan Data Center Server Market size is estimated at USD 23.25 billion in 2025, and is expected to reach USD 26.33 billion by 2030, at a CAGR of 2.52% during the forecast period (2025-2030).

Japan's data center servers landscape is undergoing significant transformation, driven by the country's advanced digital infrastructure and technological maturity. As of 2023, Japan maintains one of the world's most sophisticated internet penetration rates at 82.9%, supported by a robust network of 43.8 million broadband subscribers, including 36.6 million FTTH subscribers and 6.5 million CATV Internet subscribers. The country's mobile broadband infrastructure is equally impressive, serving 184 million 4G and 5G subscribers, demonstrating the nation's commitment to maintaining cutting-edge connectivity. This extensive digital infrastructure has positioned Japan as a prime location for data center infrastructure investments, particularly in key economic hubs like Osaka Prefecture, which boasts a GDP of USD 360 billion, comparable to Norway's economy.

The market is witnessing a strategic shift in data center infrastructure locations, with companies exploring opportunities beyond traditional hubs. Currently, more than 80% of Japan's server space is concentrated in the Greater Tokyo or Osaka/Kansai area, prompting the government to implement decentralization initiatives. This geographical diversification is exemplified by recent major investments, including Asia Pacific Land's USD 854 million commitment to construct a new data center in Kitakyushu, positioning the city as an "alternative nerve center" to Tokyo. The facility's planned 120-megawatt power consumption capacity makes it one of Kyushu's largest power users, highlighting the scale of new developments outside traditional zones.

The emergence of artificial intelligence and advanced computing requirements is reshaping server infrastructure deployment strategies across Japan. A recent NHK survey conducted between December 2023 and January 2024 revealed that more than 80% of Japan-based companies are actively utilizing generative artificial intelligence in their operations, indicating a robust demand for high-performance computing infrastructure. This trend is further supported by significant investments from technology giants, with companies like NEC, Fujitsu, and SoftBank committing substantial resources to develop Japanese-language AI systems based on large language models (LLMs).

The financial services sector is driving substantial changes in data center servers requirements, with digital transformation initiatives gaining momentum. According to a 2023 survey by Z.com Engagement Lab, over 50% of Japanese internet users have embraced mobile payments and internet banking, reflecting a broader shift toward digital financial services. This transition is supported by major financial institutions' technological initiatives, exemplified by MUFG Bank's partnership with AWS in November 2023 to accelerate its digital transformation through AI and machine learning implementations. The banking sector's evolution is further evidenced by the increasing adoption of Banking as a Service (BaaS) platforms by institutions such as Mizuho Financial Group, Shinsei Bank Group, and SBI Sumishin Net Bank.

Japan Data Center Server Market Trends

Increase in Construction of New Data Centers, Development of Internet Infrastructure

The Japanese data center landscape is experiencing significant expansion, driven by both government initiatives and private sector investments. According to Cloudscene, Japan hosted 218 data centers as of September 2023, with approximately 40 facilities identified as extensive data center installations. The Japanese government has implemented strategic initiatives to decentralize data center locations, particularly focusing on diversifying submarine cable landing points beyond traditional hubs like Tokyo and Shima. This decentralization strategy is evidenced by recent developments such as the February 2024 joint venture between Marubeni Corporation and Yondr Group to develop data center facilities in Japan, starting with the West Tokyo area.

Japan's internet infrastructure continues to demonstrate remarkable robustness, with an internet usage rate of 82.9% and an impressive optical fiber development rate of 99.3%. The country's telecommunications backbone is further strengthened by the presence of four major commercial Internet Exchange Points (IXPs) in Tokyo and Osaka, each connecting 200-300 ASNs in Tokyo and around 100 in Osaka, with a total peak traffic exchange of 13.5 Tbps. The government's commitment to infrastructure development is further illustrated by its plan to extend wireless networks to 99% of the population by 2030, while ensuring nationwide seabed cable completion by 2025. These infrastructure improvements are essential to support the growing demand for high-performance computing and data processing capabilities across various sectors, including the deployment of data center equipment and server hardware.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Adoption of Cloud and IoT Services

The Japanese market is witnessing a substantial surge in cloud computing infrastructure adoption, particularly in enterprise environments. According to the Ministry of Internal Affairs and Communications' 'Communications Usage Trends Survey 2023', over 70% of 2,400 surveyed companies reported utilizing cloud server technologies either partially or across their entire organization. This adoption is driven by the growing implementation of Internet of Things (IoT) devices across diverse sectors, including consumer electronics, military applications, agriculture, and construction, supported by prominent domestic technology leaders such as Sony, Panasonic, Fujitsu, NEC, and Toshiba.

The integration of advanced technologies is further exemplified by Japan's ambitious Smart City initiatives under the 6th Strategic Technology Infrastructure (STI) plan, which aims to implement 100 initiatives by 2025 with participation from over 1,000 organizations spanning local government, regional entities, and private enterprises. The IoT landscape is particularly dynamic in the manufacturing sector, where it demonstrates the highest penetration rate at 25% among companies implementing the technology, followed by raw material manufacturing at 21.4% and the construction industry at 20.2%. This widespread adoption is complemented by the rapid development of 5G infrastructure, with approximately 69.8 million 5G subscriptions recorded as of March 2023, creating a robust foundation for advanced IoT applications and cloud computing infrastructure services. The ecosystem is further strengthened by strategic partnerships, such as the collaboration between NEC, Fujitsu, and Nokia to develop and test new mobile communication technologies for the commercial launch of 6G services by 2030, which will likely involve the use of edge server and data center hardware.

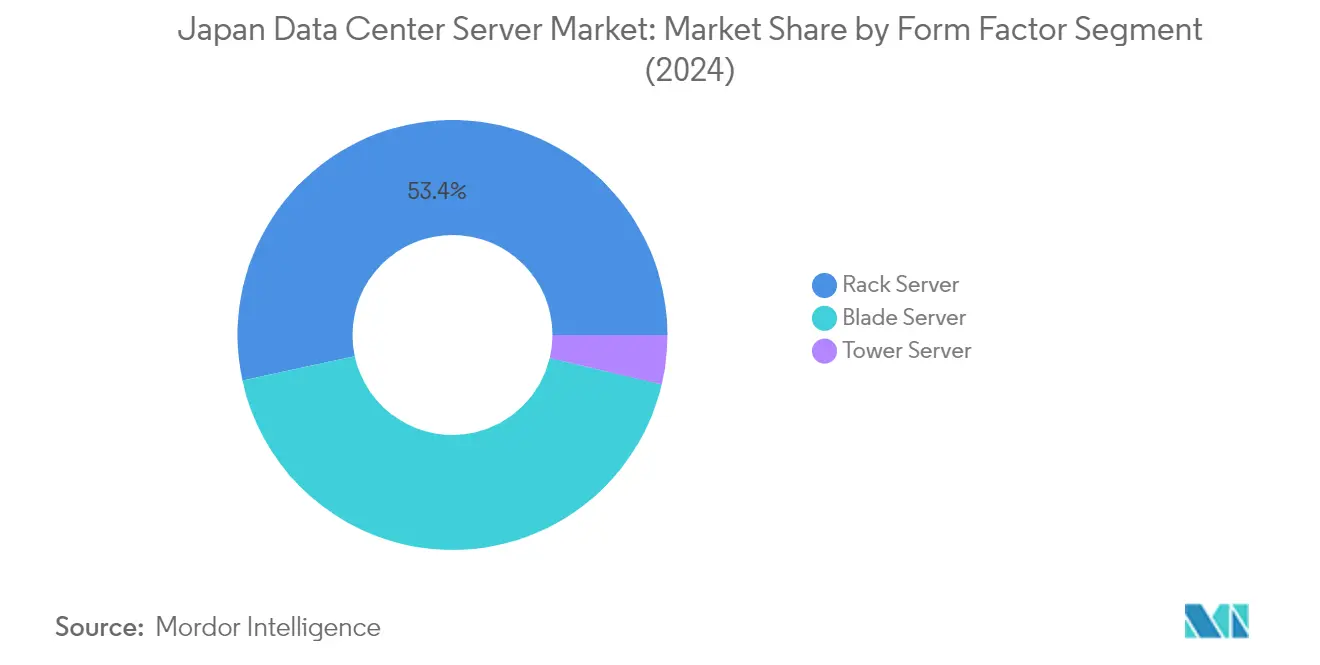

Segment Analysis: By Form Factor

Rack Server Segment in Japan Data Center Server Market

The rack server segment dominates the Japan data center server market, commanding approximately 53% of the market share in 2024. Rack servers have emerged as the preferred choice for medium-sized data centers in Japan due to their cost-effectiveness and scalability advantages. These servers are particularly valued for their ability to accommodate up to 42 servers in a single rack, making them ideal for organizations seeking to optimize space utilization. The segment's prominence is further reinforced by the ongoing construction of medium data center facilities by companies like NEC Corporation and ESR Group Limited. Rack servers offer enhanced flexibility through multi-processor, multi-memory, and multi-storage support capabilities, allowing organizations to easily scale their operations based on changing requirements. The segment's growth is also driven by the increasing technological sophistication of mid-sized centers and the servers' ability to provide improved system airflow, reducing power consumption while maximizing performance.

Blade Server Segment in Japan Data Center Server Market

The blade server segment is experiencing the fastest growth in the Japan data center server market, with a projected growth rate of approximately 4% from 2024 to 2029. This robust growth is driven by the increasing demand for high-density computing solutions in larger data centers. Blade servers are particularly gaining traction in regions like Hokkaido, where cooler temperatures provide optimal conditions for their operation. The segment's growth is further supported by their hot-swapping capabilities, allowing for server replacement without powering down entire clusters, thereby significantly reducing downtime. The Japanese government's plans to build several new data centers across the country by decentralizing landing bases for submarine cables are expected to create additional opportunities for blade server deployments. Their compact design and high-performance processing capabilities make them especially suitable for organizations requiring intensive computing power in space-constrained environments.

Remaining Segments in Form Factor

The tower server segment, while smaller in market share, continues to play a crucial role in the Japanese data center server market, particularly for small-scale operations and office environments. Tower servers are valued for their independence and simplicity in deployment, making them ideal for companies and organizations seeking straightforward server solutions without extensive infrastructure requirements. Despite their limited scalability compared to rack and blade servers, tower servers maintain their relevance in specific use cases where individual server deployment and easy maintenance access are prioritized over high-density computing needs. Their design is particularly well-suited for small data centers that are not planning significant expansion, offering a balance of performance and manageability for specific business requirements.

Segment Analysis: By End User

IT & Telecommunication Segment in Japan Data Center Server Market

The IT & Telecommunication segment dominates the Japan data center server market, commanding approximately 27% market share in 2024, driven by extensive digital transformation initiatives and 5G infrastructure development. The segment's prominence is reinforced by major telecommunications providers like NTT Docomo, KDDI, SoftBank, and Rakuten Mobile, who are actively expanding their digital infrastructure. The Japanese government's commitment to achieving 95% population coverage for 5G networks by March 2024 has significantly boosted server demand in this sector. Additionally, the increasing adoption of cloud computing, with over 70% of Japanese companies implementing cloud technologies either partially or company-wide, has further strengthened this segment's position. The segment's growth is also supported by substantial investments in data center infrastructure, exemplified by Equinix's recent launch of its hyperscale data center TY13x with 36MW of IT load capacity.

Government Segment in Japan Data Center Server Market

The Government segment represents the second-fastest growing segment in the market, with an expected growth rate of approximately 3% from 2024 to 2029. This growth is primarily driven by Japan's comprehensive digital transformation strategy and significant investments in technological infrastructure. The Japanese government's commitment to developing domestic semiconductor capabilities, evidenced by the recent USD 13.3 billion investment allocation, demonstrates its focus on strengthening digital infrastructure. The government's initiatives extend to promoting data center decentralization through incentive programs targeting regions like Hokkaido and Kyushu, while also emphasizing cybersecurity and digital service delivery through the newly established National Digital Agency. The segment's growth is further supported by various digital initiatives, including the implementation of the "Government Cloud" services and the development of smart cities under Society 5.0 objectives.

Remaining Segments in Japan Data Center Server Market

The remaining segments, including BFSI and Media & Entertainment, continue to play vital roles in shaping the Japan data center server market. The BFSI sector is experiencing significant digital transformation with the increasing adoption of digital banking services, mobile payments, and cloud-based financial solutions. The Media & Entertainment segment is driven by the growing demand for streaming services, social media platforms, and digital content delivery networks. Both sectors are benefiting from Japan's robust internet infrastructure and increasing cloud adoption rates. The market also sees significant contributions from other end-users such as healthcare, manufacturing, and education sectors, which are increasingly adopting digital technologies and cloud-based solutions to enhance their operational efficiency and service delivery capabilities.

Japan Data Center Server Industry Overview

Top Companies in Japan Data Center Server Market

The market features prominent global technology leaders, including Dell Technologies, HPE, Cisco Systems, Lenovo, Quanta Computer, Super Micro Computer, Huawei, Fujitsu, NEC Corporation, and IBM Corporation. These companies are driving innovation through advanced server computing solutions optimized for AI, data analytics, cloud computing, and enterprise applications. Product development focuses on enhanced processing capabilities, improved energy efficiency, and specialized solutions for emerging technologies like edge computing and IoT. Companies are strengthening their positions through strategic partnerships, particularly in areas like chip development and cloud infrastructure. The competitive landscape is characterized by continuous investment in R&D, expansion of product portfolios with next-generation server hardware, and efforts to establish a stronger local presence through distribution networks and support services across Japan.

Global Leaders Dominate Consolidated Server Market

The Japanese enterprise data center server market exhibits a high degree of consolidation, with global technology conglomerates holding dominant positions through their established brand presence and comprehensive product portfolios. These multinational players leverage their extensive R&D capabilities, manufacturing scale, and global supply chain networks to maintain competitive advantages over local specialists. The market structure favors large integrated solution providers who can offer end-to-end server infrastructure, including servers, storage, networking equipment, and associated services. While domestic players like Fujitsu and NEC maintain strong positions through their deep understanding of local requirements and long-standing customer relationships, the market remains primarily controlled by international technology giants.

The competitive dynamics are shaped by increasing merger and acquisition activities aimed at expanding technological capabilities and market reach. Companies are pursuing strategic acquisitions to strengthen their positions in emerging areas like AI-optimized servers and edge computing solutions. The market has witnessed consolidation through vertical integration, with major players acquiring smaller specialized firms to enhance their product offerings and technical expertise. This trend of strategic consolidation is expected to continue as companies seek to build comprehensive capabilities across the data center servers technology stack while maintaining the scale needed to serve Japan's growing digital infrastructure needs.

Innovation and Localization Drive Market Success

Success in the Japanese enterprise server market increasingly depends on companies' ability to combine technological innovation with a deep local market understanding. Incumbent players must focus on developing specialized solutions for Japan's unique requirements while maintaining global technology leadership. Market leaders are strengthening their positions through enhanced local support infrastructure, customized product development, and strategic partnerships with Japanese technology firms and system integrators. The ability to provide energy-efficient solutions aligned with Japan's sustainability goals, while meeting strict reliability and performance standards, has become crucial for maintaining market share.

For emerging players and contenders, market entry and growth opportunities lie in identifying and serving specific market niches or technological segments underserved by dominant players. Success factors include developing strong relationships with local channel partners, demonstrating clear technological differentiation, and maintaining agility in responding to evolving customer needs. The market's high concentration of enterprise customers in sectors like finance, telecommunications, and manufacturing necessitates robust security features and compliance capabilities. While substitution risk remains low due to high switching costs and established vendor relationships, regulatory requirements around data sovereignty and security continue to influence market dynamics and competitive strategies.

Japan Data Center Server Market Leaders

-

Dell Technologies Inc.

-

Hewlett Packard Enterprise

-

Cisco Systems Inc.

-

Lenovo Group Limited

-

Quanta Computer Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Japan Data Center Server Market News

- February 2024 - Marubeni Corporation and Yondr Group entered a joint venture to develop data center facilities in Japan. Initially, Marubeni will construct a data center facility in the West Tokyo area, with further projects planned in the future. The project will initiate Marubeni's expansion into the emerging hyper-scale data center development market and its ambition to contribute to the decarbonization of society by supplying renewable energy to data centers.

- October 2023 - Air Trunk announced a significant expansion in Japan by launching a new data center in Osaka. The facility, OSK1, marks AirTrunk's third data center in Japan and its first venture outside the Tokyo region. OSK1 is set to offer more than 20 megawatts (MW) capacity, contributing to the regional diversity in a new major availability zone.

Japan Data Center Server Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increase in Construction of New Data Centers, Development of Internet Infrastructure

- 5.1.2 Increasing Adoption of Cloud and IoT Services

-

5.2 Market Challenge

- 5.2.1 High Initial Investments

- 5.3 Assessment of COVID-19 Impact

6. MARKET SEGMENTATION

-

6.1 By Form Factor

- 6.1.1 Blade Server

- 6.1.2 Rack Server

- 6.1.3 Tower Server

-

6.2 By End User

- 6.2.1 IT and Telecommunication

- 6.2.2 BFSI

- 6.2.3 Government

- 6.2.4 Media and Entertainment

- 6.2.5 Other End Users

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Dell Technologies Inc.

- 7.1.2 Hewlett Packard Enterprise

- 7.1.3 Cisco Systems Inc.

- 7.1.4 Lenovo Group Limited

- 7.1.5 Quanta Computer Inc.

- 7.1.6 Super Micro Computer Inc.

- 7.1.7 Huawei Technologies Co. Ltd

- 7.1.8 Fujitsu Limited

- 7.1.9 NEC Corporation

- 7.1.10 IBM Corporation

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Japan Data Center Server Industry Segmentation

The Japan data center server market is defined by the revenue accrued from various solutions used across end-user industries.

The Japan data center server market is segmented by form factor (blade server, rack server, and tower server) by end user (IT and telecommunication, BFSI, government, media and entertainment, and other end users). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Form Factor | Blade Server |

| Rack Server | |

| Tower Server | |

| By End User | IT and Telecommunication |

| BFSI | |

| Government | |

| Media and Entertainment | |

| Other End Users |

Need A Different Region or Segment?

Customize Now

Japan Data Center Server Market Research FAQs

How big is the Japan Data Center Server Market?

The Japan Data Center Server Market size is expected to reach USD 23.25 billion in 2025 and grow at a CAGR of 2.52% to reach USD 26.33 billion by 2030.

What is the current Japan Data Center Server Market size?

In 2025, the Japan Data Center Server Market size is expected to reach USD 23.25 billion.

Who are the key players in Japan Data Center Server Market?

Dell Technologies Inc., Hewlett Packard Enterprise, Cisco Systems Inc., Lenovo Group Limited and Quanta Computer Inc. are the major companies operating in the Japan Data Center Server Market.

What years does this Japan Data Center Server Market cover, and what was the market size in 2024?

In 2024, the Japan Data Center Server Market size was estimated at USD 22.66 billion. The report covers the Japan Data Center Server Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Japan Data Center Server Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Japan Data Center Server Market Research

Mordor Intelligence offers a comprehensive analysis of the data center server industry. We leverage extensive expertise in server computing and enterprise computing research. Our detailed examination covers the full spectrum of server infrastructure. This includes rack servers, blade servers, cloud servers, and tower servers. The report provides in-depth insights into data center infrastructure and cloud computing infrastructure. It also highlights emerging trends in data center technology, focusing on server hardware developments and data center equipment innovations.

Stakeholders gain valuable insights from our analysis of enterprise server deployments, dedicated server solutions, and managed server services. The report, available as an easy-to-download PDF, examines the evolution of ARM servers, edge servers, and hyperscale server implementations across enterprise data center environments. Our comprehensive coverage extends to colocation server facilities and x86 server architectures. We also explore advanced data center computing solutions, providing stakeholders with actionable intelligence for strategic decision-making in data center hardware investments and technological advancement initiatives.