Market Trends of Japan Aerospace And Defense Industry

The Manufacturing Segment Accounted for a Major Share in 2023

The manufacturing service type segment stands out as the dominant force, holding the largest market share. Renowned companies such as Mitsubishi Heavy Industries, Ltd. and Kawasaki Heavy Industries, Ltd. play pivotal roles in shaping this sector. These industry giants leverage their expertise in precision engineering and cutting-edge technology to manufacture a wide array of aerospace and defense products, ranging from fighter jets and helicopters to sophisticated missile systems.

The significance of the manufacturing service type is underscored by the intricate collaboration between these companies and the Japanese government, fostering a strategic partnership for national security. Additionally, emerging players like Subaru Corporation contribute to the sector's growth by diversifying their portfolios to include aerospace components. The emphasis on innovation, quality, and reliability positions Japan's manufacturing service type segment as a linchpin in the nation's aerospace and defense capabilities, reflecting a synergy between technological prowess and strategic foresight.

Moreover, increasing orders from the Japanese government for indigenous manufactured products is also contributing to the growth of manufacturing sector. For instance, in November 2023, Mitsubishi Heavy Industries forecast its defense sales to double to 1 trillion yen (USD 6.7 billion) by 2026 and stay strong as geopolitical tensions boost business for MHI. The Japanese government's latest five-year strategy suggests a 56% increase in defense spending, through 2027, from the previous term as it strives to build up the Japan’s defense capabilities. Major key focus of MHI is to develop a domestic capability to produce long-range missiles that can achieve distances of over 1,000 kilometers.

The government is also offering manufacturers profit margins of up to 10% to encourage indigenous innovation and manufacturing and is prepared to offset up to 5% in cost increases to help with high inflation rates. Developments in such domains are expected to be a part of Japan's new multidimensional integrated defense force. Thus, such ongoing developments are expected to drive the Japanese defense market during the forecast period.

Aerospace Sector to Witness Significant Growth During the Forecast Period

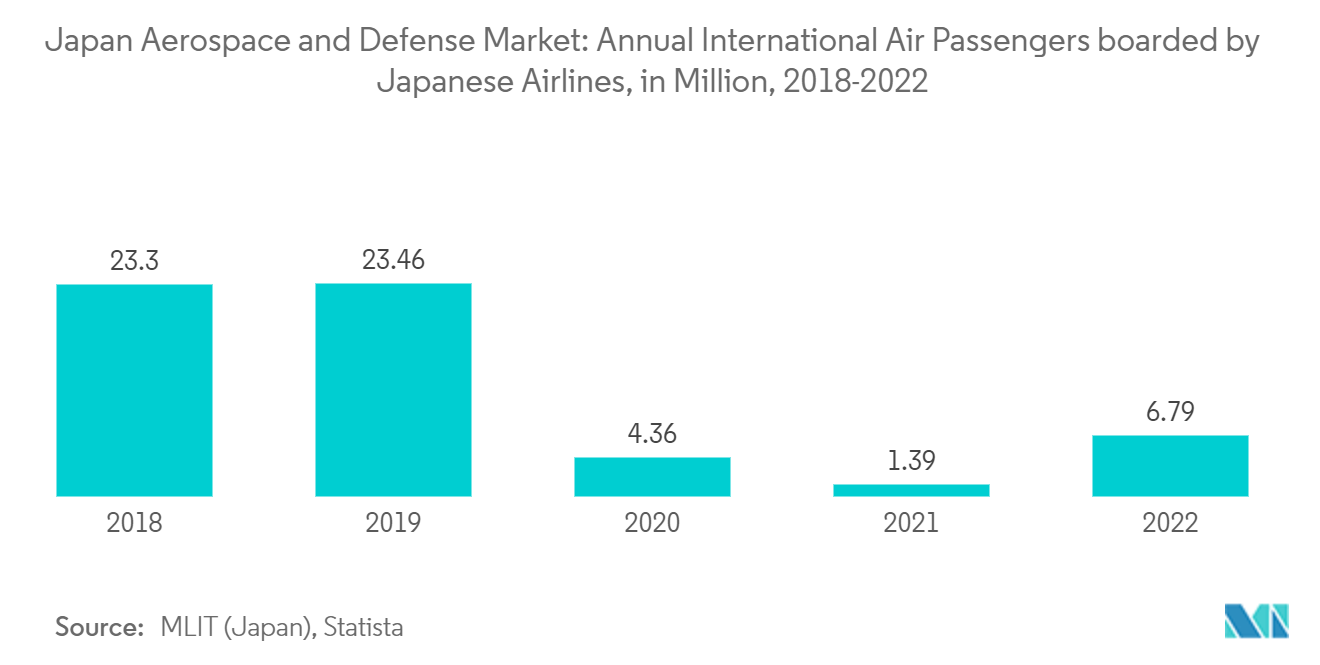

The aerospace sector is poised to showcase remarkable growth during the forecast period. Japan continues to offer a lucrative market for imported aircraft, aircraft parts, and engines. Currently, Japan is playing a pivotal role in the development of several aircraft families, including the B777, B777X, and B787. In March 2023, Japan Airlines (JAL), Japan's national flag carrier, announced an order of 21 Boeing B737 MAX aircraft. The airline aims to bring advanced and fuel-efficient aircraft into its fleet starting in 2026. The value of the contract was approximately USD 2.5 billion. Haneda International Airport (HND), Narita International Airport (NRT), Kansai International Airport (KIX), and Fukoma International Airport (FUK) are the four major airports in Japan that together handle over 200 million passengers annually.

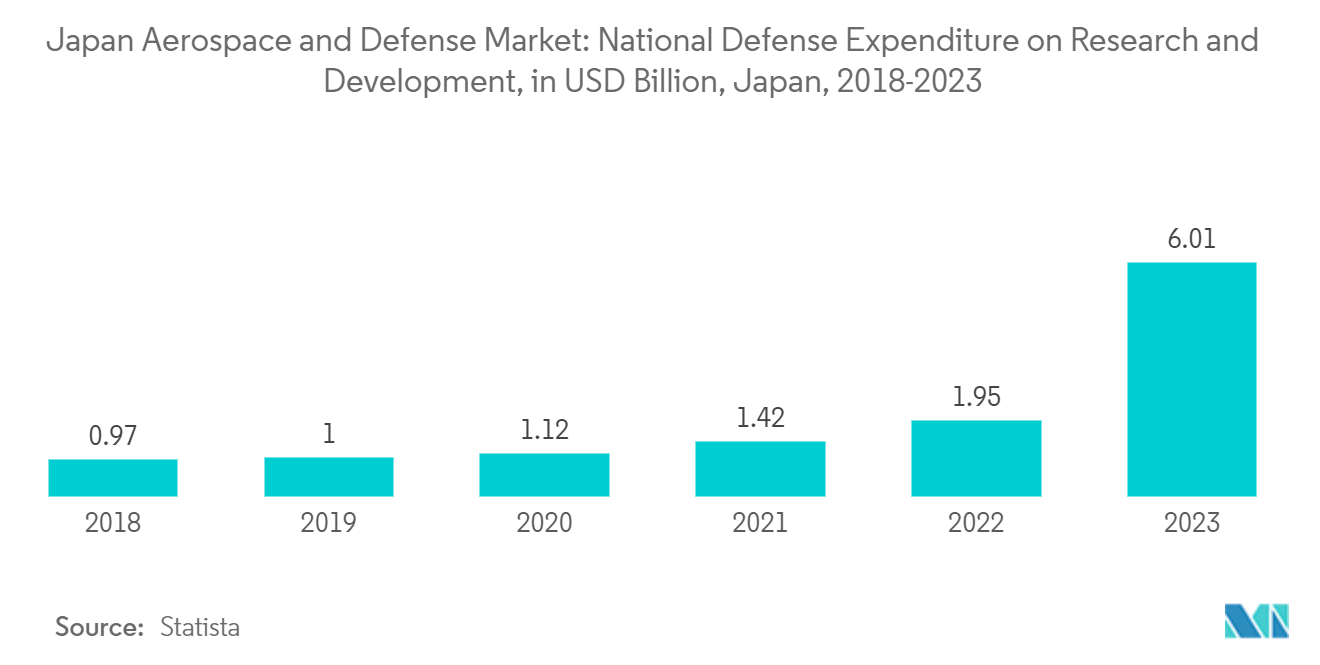

Furthermore, Japanese companies are also actively engaged in providing engineering services towards the development and MRO of aircraft engines, such as the V2500, Trent1000, GEnx, GE9X, PW1100G-JM, etc. Similarly, in January 2022, the US Department of Defense (DoD) announced a contract worth USD 471 million to The Boeing Company for the development of new systems for Japan Air Self-Defense Force's (JASDF) F-15 Eagle Super Interceptors fleet. The Japanese firms have also contributed to the development of various engineering test satellites, marine and terrestrial observation satellites, communications, broadcasting, global navigation satellites, etc., including weather satellites such as the HIMAWARI 8 and 9. In 2021, the Japanese government spent USD 4.14 billion on space activities. The Japanese space firms developed Launch vehicles such as the M-V, H-IIA/B, and Epsilon rockets. The Japanese satellite manufacturers are also using their advanced technical capabilities, high quality, and competitive costs to open the overseas market. Thus, growing expenditure on research and development and rising spending on enhancing aviation infrastructure drive market growth across the country.