Market Size of Japan Third-Party Logistics (3PL) Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

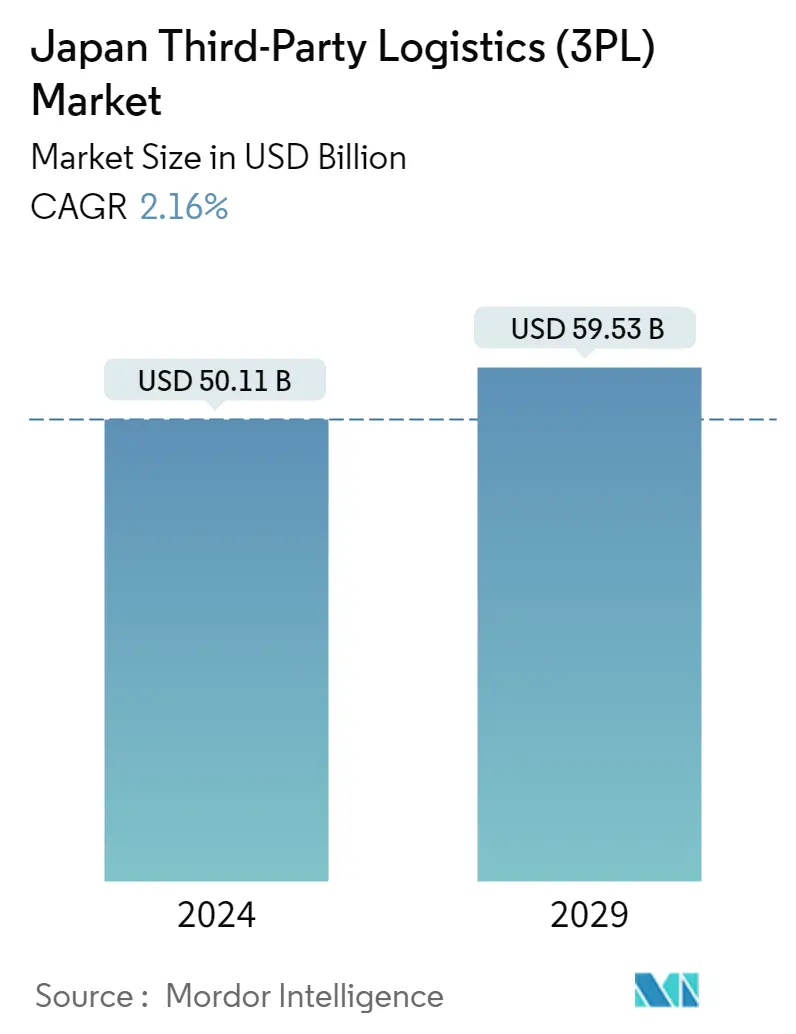

| Market Size (2024) | USD 50.11 Billion |

| Market Size (2029) | USD 59.53 Billion |

| CAGR (2024 - 2029) | 2.16 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Japan Third-Party Logistics (3PL) Market Analysis

The Japan Third-Party Logistics Market size is estimated at USD 50.11 billion in 2024, and is expected to reach USD 59.53 billion by 2029, growing at a CAGR of 2.16% during the forecast period (2024-2029).

- The COVID-19 epidemic had a direct effect on logistics companies, which move, store, and move goods.Logistics companies help businesses do business and get their products to customers. They became an important part of value chains both inside and outside of national borders. Hence, supply chain interruptions brought on by the pandemic could affect the sector's competitiveness, economic expansion, and job creation.

- Japan has made a lot of progress in the supply chain space over time. For example, it has embraced digital technologies to change a traditional industry. In the last few years, the social and economic factors that affect logistics have changed a lot. These factors include a shrinking or aging population, new ideas in some areas, more frequent deliveries of smaller goods, and different customer needs. In Japan, there is more demand for 3PL as large companies look at how their logistics networks work and outsource more tasks to 3PL providers to cut costs and improve efficiency.

- 3PL logistics firms are the ones who run supply chains and get materials and goods to all industries and consumers. Japan, one of the biggest economies in East Asia, relies on 3PL logistics a lot because of its manufacturing industry. As a result, organizations like Yamato Holdings are among the top logistics providers globally. 120 million people in the archipelago handled 4.71 billion tons of domestic freight, and foreign trade added 900 million tons more.

- Since 2000, there has been a big rise in the need for large, modern logistics leasing facilities in Japan. Outsourcing logistics operations, imbalances in corporate real estate, and moving out of multiple old warehouses all contributed to the rise. The freight and logistics industry in Japan is a big part of the economy, making up more than 5% of the GDP.

- The logistics business is known for its fierce cost competitiveness. To outbid rivals, sophisticated coordination and economies of scale are required. Through the use of "third-party logistics," sometimes known as "3PL," logistics firms have begun to streamline their operations. Automation and artificial intelligence (AI) are further tools for cost control.

It's likely that the logistics systems industry will grow to include more of these technical solutions. Although automated warehouses are now in use, it will be some time before fully autonomous trucks are allowed on the roads. Automation advancements cannot arrive soon enough for Japan. Its logistics sector is experiencing a manpower deficit, and on top of that, drivers are aging quickly, endangering the availability of services at fair prices. Two goals of this effort are to increase productivity in the trucking sector and to foster work environments that attract and retain older and female drivers. It has to be seen whether this tactic stabilizes the market effectively enough until automation advances further.

Japan Third-Party Logistics (3PL) Industry Segmentation

Third-party logistics companies provide services that have to do with the logistics of the supply chain. This includes shipping, storing, picking and packing, figuring out how much inventory there will be, filling orders, packaging, and freight forwarding.

A 3PL (third-party logistics) provider offers logistics services that are outsourced. These services include the management of one or more aspects of purchasing and shipping. In business, 3PL has a broad meaning that applies to any service contract that involves storing or shipping items. A 3PL service can be a single provider, like shipping or storing goods in a warehouse, or it can be a system-wide bundle of services that can manage the supply chain.

A comprehensive background analysis of the Japan third-party logistics (3PL) market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry. The impact of COVID-19 has also been incorporated and considered during the study.

The Japan third-party logistics (3PL) market is segmented by service (domestic transportation management, international transportation management, and value-added warehousing and distribution) and by end-users (manufacturing and automotive, oil and gas, and chemicals), distributive trade (wholesale and retail trade, including e-commerce), pharma and healthcare, construction, and other end-users. The report offers the market size and forecast in value (USD billion) for all the above segments.

| By Service | |

| Domestic Transportation Management | |

| International Transportation Management | |

| Value-added Warehousing and Distribution |

| By End-User | |

| Manufacturing & Automotive | |

| Oil & Gas and Chemicals | |

| Distributive Trade (Wholesale and Retail trade including e-commerce) | |

| Pharma & Healthcare | |

| Construction | |

| Other End-Users |

Japan Third-Party Logistics (3PL) Market Size Summary

The third-party logistics (3PL) market in Japan is poised for steady growth, driven by the country's robust manufacturing sector and the increasing demand for efficient supply chain solutions. As a significant player in East Asia's economy, Japan's logistics industry has evolved by integrating digital technologies and automation to enhance operational efficiency. The COVID-19 pandemic underscored the critical role of logistics in maintaining supply chain continuity, prompting businesses to outsource more logistics functions to 3PL providers. This trend is further fueled by demographic shifts, such as an aging population and changing consumer preferences, which necessitate more frequent and smaller deliveries. Major logistics companies like Yamato Holdings and Vantec are at the forefront, leveraging advanced technologies to streamline operations and meet the complex demands of industries such as automotive and pharmaceuticals.

The logistics sector in Japan is a vital component of the national economy, contributing significantly to GDP and supporting the country's status as a leading exporter. The market is characterized by intense competition, requiring firms to adopt cost-effective strategies and innovative solutions like automation and artificial intelligence. The rise of e-commerce has also spurred demand for value-added services, prompting logistics providers to enhance their offerings in packaging, labeling, and sorting. Environmental sustainability is becoming increasingly important, with efforts to reduce the carbon footprint through eco-friendly logistics practices. Key players in the market, including Yusen Logistics, Nippon Express, and Hitachi Transport System, are actively investing in technology and infrastructure to maintain their competitive edge and cater to the evolving needs of the Japanese market.

Japan Third-Party Logistics (3PL) Market Size - Table of Contents

-

1. MARKET DYNAMICS AND INSIGHTS

-

1.1 Current Market Scenario

-

1.2 Market Dynamics

-

1.2.1 Drivers

-

1.2.2 Restraints

-

1.2.3 Opportunities

-

-

1.3 Value Chain / Supply Chain Analysis

-

1.4 Industry Policies and Regulations

-

1.5 General Trends in Warehousing Market

-

1.6 Demand From Other Segments, such as CEP, Last Mile Delivery, Cold Chain Logistics Etc.

-

1.7 Insights on Ecommerce Business

-

1.8 Technological Trends and Automation

-

1.9 Industry Attractiveness - Porter's Five Forces Analysis

-

1.9.1 Threat of New Entrants

-

1.9.2 Bargaining Power of Buyers/Consumers

-

1.9.3 Bargaining Power of Suppliers

-

1.9.4 Threat of Substitute Products

-

1.9.5 Intensity of Competitive Rivalry

-

-

1.10 Impact of COVID--19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Service

-

2.1.1 Domestic Transportation Management

-

2.1.2 International Transportation Management

-

2.1.3 Value-added Warehousing and Distribution

-

-

2.2 By End-User

-

2.2.1 Manufacturing & Automotive

-

2.2.2 Oil & Gas and Chemicals

-

2.2.3 Distributive Trade (Wholesale and Retail trade including e-commerce)

-

2.2.4 Pharma & Healthcare

-

2.2.5 Construction

-

2.2.6 Other End-Users

-

-

Japan Third-Party Logistics (3PL) Market Size FAQs

How big is the Japan Third-Party Logistics (3PL) Market?

The Japan Third-Party Logistics (3PL) Market size is expected to reach USD 50.11 billion in 2024 and grow at a CAGR of 2.16% to reach USD 59.53 billion by 2029.

What is the current Japan Third-Party Logistics (3PL) Market size?

In 2024, the Japan Third-Party Logistics (3PL) Market size is expected to reach USD 50.11 billion.