Market Overview

| Study Period | 2018 - 2031 |

|---|---|

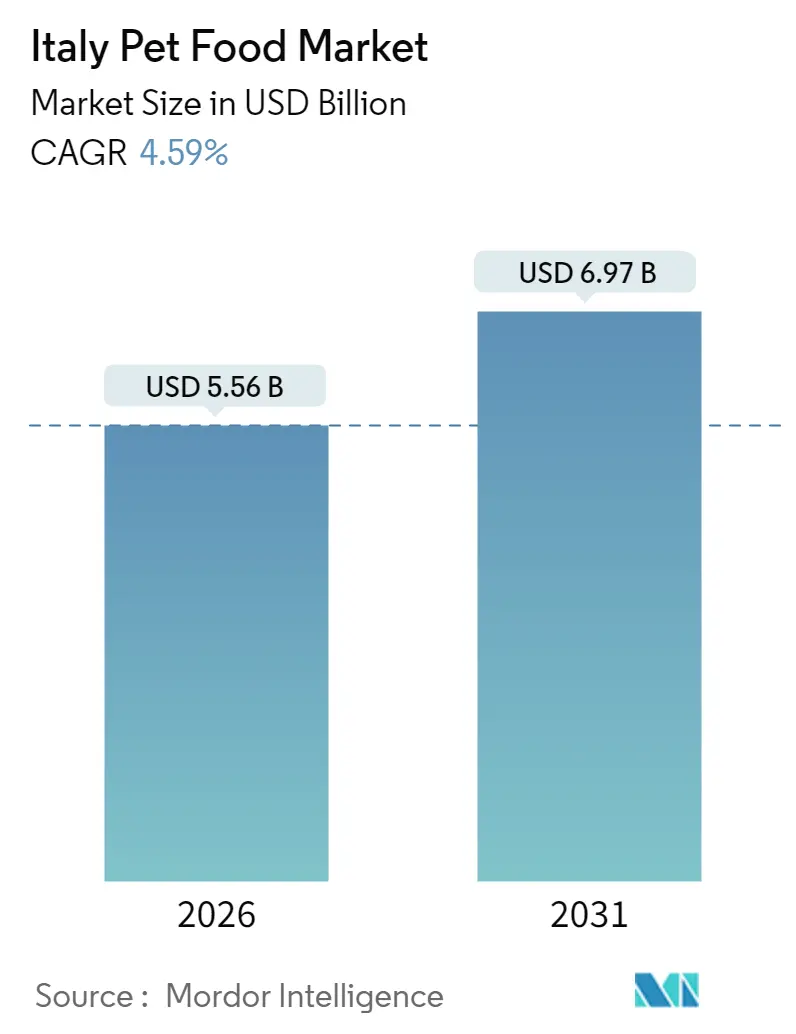

| Market Size (2026) | USD 5.56 Billion |

| Market Size (2031) | USD 6.97 Billion |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

| Fastest Growing Market | Dogs |

| Largest Market | Cats |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Pet Food Market Analysis by Mordor Intelligence

The Italy pet food market is expected to grow from USD 5.32 billion in 2025 to USD 5.56 billion in 2026 and is forecast to reach USD 6.97 billion by 2031 at 4.59% CAGR over 2026-2031. Robust premiumization, rapid digital adoption, and sustained pet humanization keep the Italy pet food market on a steady upward course despite macro-economic headwinds[1]Source: Assalco-Zoomark, “Italian Pet Industry Report 2024,” ASSALCO.IT. Discretionary purchasing power in Northern regions, regulatory approval for novel proteins, and a shift toward functional nutrition amplify value creation, while private-label rollouts widen access to quality offerings. Online subscription models, single-serve wet-food innovation, and domestic capacity investments strengthen supply resilience and product diversity. Competitive fragmentation allows regional specialists, veterinary-endorsed brands, and direct-to-consumer entrants to flourish alongside multinational leaders, intensifying innovation cycles and category differentiation across the Italy pet food market.

Key Report Takeaways

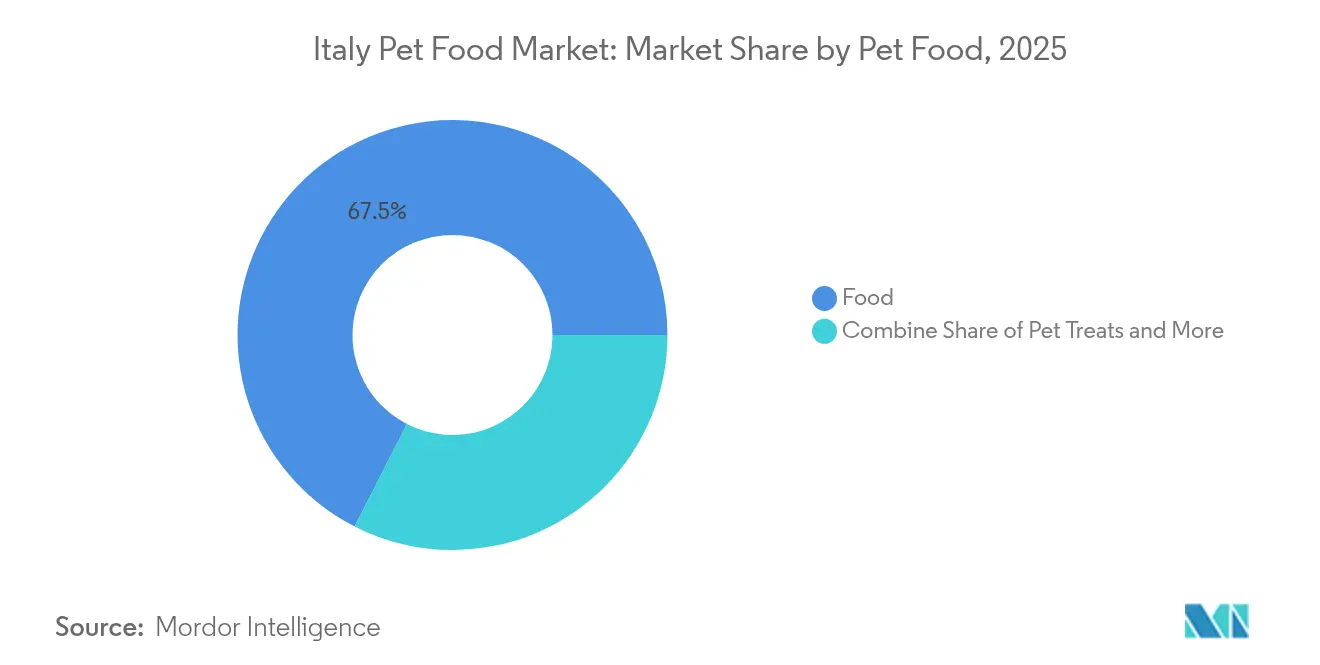

- By Pet Food product, Food led with 67.48% of the Italy pet food market share in 2025, while Pet Nutraceuticals and Supplements are projected to post an 10.81% CAGR through 2031.

- By Pets, Dogs accounted for 43.32% of the Italy pet food market size in 2025 and are projected to advance at a 5.41% CAGR between 2026 and 2031.

- By Distribution Channel, Supermarkets and Hypermarkets held 44.17% of the Italy pet food market share in 2025, whereas the Online Channel is forecast to register a 6.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Pet Food Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization driven by pet humanization | +1.20% | Italy, with spillover to Southern Europe | Medium term (2-4 years) |

| Supermarket private-label rollouts expanding volume | +0.80% | Italy, concentrated in Northern regions | Short term (≤ 2 years) |

| Veterinary endorsement of functional diets | +0.90% | Italy, with veterinary clinic networks | Medium term (2-4 years) |

| Rapid growth of e-commerce channels | +0.70% | Italy, accelerated in urban centers | Short term (≤ 2 years) |

| Scale-up of domestic single-serve wet-food capacity | +0.60% | Italy, focused on Emilia-Romagna region | Medium term (2-4 years) |

| EU approval of insect protein for companion animals | +0.40% | EU-wide, early adoption in Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Premiumization Driven by Pet Humanization

Italian households increasingly treat companion animals as family members, reinforcing willingness to pay for human-grade ingredients, transparent labeling, and clinically substantiated functional benefits. Remote work patterns cemented during the pandemic deepened emotional bonds, with 73% of owners confirming higher nutrition spending in 2024. Premium claims now focus on organic certification, grain-free or limited-ingredient formulations, and targeted health outcomes such as joint mobility, cognitive support, or gut wellness. Regulatory guidance under FEDIAF compels evidence-based messaging, preventing cosmetic price mark-ups and fostering credible product development. Brands that marry scientific validation with storytelling resonate strongly, particularly among millennials and empty-nesters who channel discretionary income toward pet well-being. Single-serve wet-food lines, fresh-frozen subscriptions, and insect-protein recipes exemplify how the Italy pet food market converts human culinary trends into pet formats. As premiumization climbs the value ladder, volume growth slows yet average selling prices advance, sustaining revenue momentum even during inflationary cycles. This dynamic elevates margins for manufacturers capable of sourcing novel ingredients, executing small-batch production, and articulating verifiable functional claims.

Supermarket Private-Label Rollouts Expanding Volume

Leading grocery chains have deepened private-label penetration, widening affordable access and protecting margin during economic uncertainty. Coop Italia’s 2024 range extension priced 20%–30% below national brands without sacrificing nutrient adequacy, leveraging contract manufacturing economies[2]Source: Coop Italia, “Annual Report 2024,” COOP.IT. Esselunga and Carrefour mirrored the strategy, pairing exclusive recipes with loyalty-card promotions that amplified household penetration in Northern catchment areas. Private-label ascendance disciplines incumbent brands to accelerate differentiation via science-backed claims, sustainable sourcing, or bespoke breed-specific diets. Retailers use real-time scanner data to refine assortments, prune slow-moving SKUs, and calibrate price architecture in line with disposable-income shifts. For Italian suppliers, supermarket affiliation secures scale, lowers logistics costs, and shortens innovation cycles thanks to collaborative product-development sprints. Consumer confidence in supermarket quality seals the proposition, expanding overall category volume and cushioning the Italy pet food market against down-trading to home-prepared meals.

Veterinary Endorsement of Functional Diets

Clinical nutrition takes center stage as veterinarians promote proactive dietary interventions addressing obesity, osteoarthritis, dermatological sensitivities, and cognitive decline. Hill’s Pet Nutrition recorded a 23% jump in clinic-dispensed products during 2024, underscoring professional influence on purchase decisions. Italian pet parents lean heavily on trusted medical guidance where science and empathy intersect, validating premium price points for prescription and life-stage-specific formulas. Continuing-education modules sponsored by the Italian Veterinary Association equip practitioners with evidence-based protocols that translate into precise diet recommendations. Practices benefit from incremental revenue and tighter client loyalty, while brands secure channel exclusivity, insulated from direct grocery competition. The effect ripples beyond therapeutic SKUs: mainstream premium brands now tout vet-formulated claims and publish digestibility or palatability metrics to emulate professional credibility. As the preventive care culture spreads, functional diets transition from niche to core demand driver within the Italy pet food market.

Rapid Growth of E-commerce Channels

Digital commerce reshapes Italian purchasing behavior, offering assortment breadth, subscription convenience, and next-day fulfillment. Amazon Italy’s pet specialty portfolio, augmented by Zooplus’s localized warehouses, is projected to drive online channels during the forecast period. Urban consumers appreciate frictionless reordering, auto-ship discounts, and data-driven product suggestions, while rural owners gain access to premium formats absent from local shelves. Direct-to-consumer startups exploit lower overhead and targeted social-media outreach to test novel recipes and customize meal plans based on pet profiles. Retailers integrate click-and-collect and last-mile partnerships to bridge physical-digital divides, ensuring omnichannel continuity. E-commerce analytics reveal flavor, texture, and format preferences in granular detail, sharpening R&D agility. As digital adoption expands, incumbent supermarket leadership faces incremental erosion, but overall category penetration increases because frictionless access raises usage frequency and basket size in the Italy pet food market.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-linked down-trading to economy brands | -0.90% | Italy, particularly Southern regions | Short term (≤ 2 years) |

| Declining birth rate limiting new pet adoption | -0.60% | Italy, concentrated in Northern urban areas | Long term (≥ 4 years) |

| Compounding pharmacies cannibalizing veterinary diet demand | -0.30% | Italy, focused on major metropolitan areas | Medium term (2-4 years) |

| Omega-3 supply gaps from Adriatic fishing quotas | -0.40% | Italy and broader Mediterranean region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inflation-Linked Down-Trading to Economy Brands

Escalating feedstock and energy costs raise shelf prices, nudging budget-constrained households toward larger pack sizes, simplified ingredient decks, or economy labels. ISTAT recorded 34% of owners switching brands in 2024 to preserve feeding routines within tightened budgets [3]Source: European Commission, “Regulation 2022/1104,” EUR-LEX.EUROPA.EU. Although emotional attachment limits wholesale abandonment of quality standards, premium and super-premium tiers witness slowed volume, compelling manufacturers to optimize formulations and packaging weights. Retail data show accelerated rotation of mid-tier SKUs as shoppers stretch paychecks yet refuse nutritionally inferior options, placing private-label lines in a sweet spot between affordability and adequacy. Margin compression at the top end may temper R&D spending if inflationary pressure persists, though category innovation remains necessary to defend value. Over time, easing cost inflation or wage growth could restore premium momentum, but the immediate drag trims the Italy pet food market growth curve.

Declining Birth Rate Limiting New Pet Adoption

Italy’s fertility rate dropped to 1.24 births per woman by 2024, cooling the influx of young families that historically fueled first-time pet ownership [4]Source: ISTAT, “Demographic Statistics 2024,” ISTAT.IT. Urban housing constraints, rising living costs, and flexible job migration temper commitments to long-lived companions, especially larger dog breeds. Although aging households invest heavily in existing pets, replacement rate gaps emerge once older animals pass away, softening long-term volume tailwinds. Demographic stagnation particularly affects dog adoption, which correlates with suburban family life, yard space, and multigenerational dwellings. Immigration influx and single-adult households partially offset the deficit, and senior-pet nutrition opens specialized revenue streams. Nevertheless, slower pipeline growth imposes strategic emphasis on value expansion per pet rather than pure volume, shaping innovation priorities across the Italy pet food market.

Segment Analysis

By Pet Food Product: Functional Nutrition Drives Growth

Food products commanded 67.48% of the Italy pet food market in 2025, underscoring their non-discretionary role in daily feeding routines and stable loyalty dynamics. Within this domain, dry kibble offers calorie-dense convenience and price efficiency, while wet formats intensify palatability and hydration, lifting average revenue per kilogram. The Italy pet food market size for Food is projected to rise steadily as premium fortification and protein diversification boost unit value. Pet Nutraceuticals and Supplements, though smaller in absolute terms, outpace all other categories with an 10.81% CAGR, propelled by preventive health awareness, senior pet population growth, and veterinary endorsement. Functional chews, probiotic powders, and omega-3 capsules widen the spectrum of use-cases, from joint support to gastrointestinal health, enriching the Italy pet food industry product mix.

The Italy pet food market also benefits from treat innovation that merges indulgence with measurable wellness benefits. Training treats fortified with collagen or dental chews featuring enzymatic coatings bridge emotional reward and clinical functionality, expanding share-of-wallet beyond core meals. Veterinary diets remain a high-margin enclave governed by strict clinical evidence, with demand supported by rising chronic-disease prevalence in aging pets. Regulatory alignment under EU feed law assures cross-category safety, while domestic capacity investments in flexible pouching lines accommodate shorter runs and rapid flavor rotation. Collectively, product-mix evolution favors premium-value layers that offset volume maturation, ensuring resilient growth for the Italy pet food market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Pets: Canine Preference Shapes Market Dynamics

Dogs generated 43.32% of the Italy pet food market size in 2025 and are forecast to log a 5.41% CAGR through 2031, outperforming all other species segments. Higher caloric intake per animal and pronounced owner propensity to experiment with functional diets position dogs as revenue engines. Breed-specific sensitivities, such as large-breed hip dysplasia risk or small-breed dental issues, justify granular formulation cues that command premium pricing. The Italy pet food market for canine products capitalizes on this diversity through targeted kibble density, omega-3 levels, and kibble shape customization.

Cats constitute a sizable yet mature subsegment characterized by habitual feeding patterns and entrenched brand loyalty. Palatability reigns supreme, with wet pouches and mousse textures delivering hydration and umami richness that encourage repeat purchase. Other Pets, including birds, rabbits, and exotics, remain niche but profitable arenas for specialty brands adept at tailoring micro-batch nutrition and harnessing online micro-community marketing. Species-specific regulatory standards ensure nutrient balance, and veterinary guidance in exotic animal clinics offers ancillary demand drivers. As demographic shifts influence species preference, manufacturers monitor urban living constraints and household size trends to calibrate product pipeline for the Italy pet food market.

By Distribution Channel: Digital Transformation Accelerates

Supermarkets and Hypermarkets retained 44.17% share of the Italy pet food market in 2025, leveraging national coverage, price competitiveness, and multi-category one-stop convenience. Shelf sets continue to expand premium facings, and loyalty programs deepen stickiness; however, constrained physical space caps SKU proliferation. The Online Channel, building on superior assortment and subscription incentives, is set to deliver a 6.52% CAGR, the fastest among all channels. Lower search costs, targeted promotions, and last-mile logistics efficiencies tilt market share incrementally digital, yet bricks-and-mortar remains foundational for bulk replenishment and impulse treat purchases.

Specialty Stores differentiate through educated staff, in-store sampling, and curated premium offerings, sustaining a loyal base of high-spend customers seeking expert advice. Convenience Stores dominate urgent, small-basket tranches, benefiting from high footfall and proximity. Omnichannel strategies blur boundaries: supermarket banners deploy click-and-collect, while pet specialty chains stream live consultations and run subscription portals. The Italy pet food market therefore evolves into a fluid ecosystem where channel strategy synchronizes digital reach with experiential touchpoints, enhancing customer lifetime value across demographic segments.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Northern Italy dominates the country's pet food market in terms of both volume and premiumisation. Recent growth has been driven by wet food and cat products, which are outperforming the dog segments in value terms. This trend aligns with the broader "humanisation" phenomenon, where pet owners treat their pets as family members and opt for higher-margin wet, functional, and specialty formulas.

The affluent and highly urbanised northern regions, including Lombardy, Veneto, Emilia-Romagna, and nearby provinces, exhibit the strongest adoption of premium, organic, and functional pet foods. These areas also show the fastest shift toward e-commerce and specialist retail channels. Academic surveys and consumer studies indicate that pet owners in the north are more engaged with quality attributes and demonstrate a higher willingness to pay for health-oriented products. Additionally, major industry investments and manufacturing capacities are concentrated in this region. For instance, a recent significant investment by Nestlé Purina in Mantua highlights northern Italy's role as a key production and distribution hub for the pet food industry.

In central regions such as Lazio and Tuscany, consumer behavior varies. Urban pet owners often mirror northern buying patterns, favoring premium and convenient products. However, in smaller towns, price sensitivity remains higher, with a focus on staple dry kibbles. In southern regions like Campania, Puglia, Calabria, and Sicily, the adoption of higher-end pet food lines is slower on a per-household basis. This reflects persistent income and spending disparities between the North and South. As a result, value-oriented products, multi-pack formats, private-label dry food, and informal purchase channels remain significant in these areas. Nevertheless, national trends, including e-commerce growth and targeted local marketing efforts, are gradually increasing premium product penetration beyond the traditional northern strongholds.

Competitive Landscape

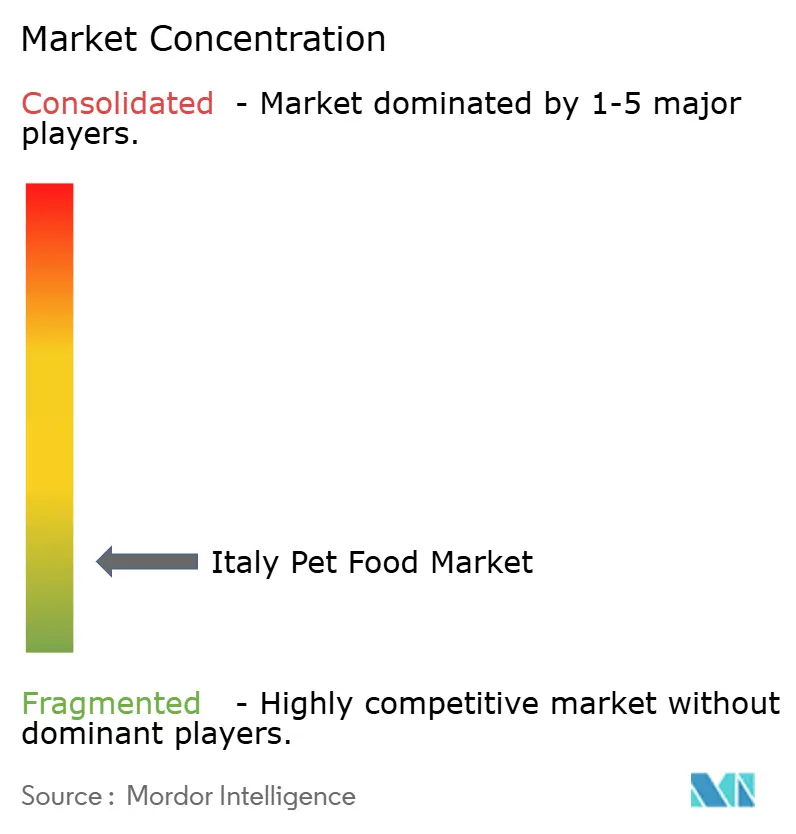

The Italy pet food market remains highly fragmented, leaving abundant space for regional specialists and private-label manufacturers. Nestlé Purina leads, leveraging portfolio depth, national advertising, and a newly expanded Portogruaro facility capable of flexible pouch production. Mars follows, integrating sustainability initiatives such as recyclable packaging across Royal Canin and Whiskas lines to protect its share. Hill’s Pet Nutrition strengthens its veterinary channel moat through direct e-commerce ordering, reinforcing clinician loyalty.

Regional midsize players like Affinity Petcare and VAFO Praha exploit agile manufacturing and supermarket partnerships to offer grain-free or single-protein recipes at accessible price points. Ingredient innovators DSM-Firmenich, Alltech, Kemin, and Evonik embed themselves as strategic allies, co-developing probiotic, omega-3, or amino acid solutions that bolster functional claims. Direct-to-consumer disruptors deploy predictive algorithms to tailor subscription meal plans, further fragmenting share.

Strategic imperatives pivot around formulation science, supply-chain resilience, and digital engagement. Companies integrate Life Cycle Impact assessments to validate sustainability credentials, while data analytics refine flavor development and targeted promotions. M&A potential remains elevated as multinationals scout niche brands exhibiting authentic origin stories or veterinarian trust. Policy shifts such as EU insect-protein approval open additional lanes for ingredient differentiation, intensifying competitive innovation across the Italy pet food market.

Italy Pet Food Industry Leaders

Affinity Petcare SA

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

Mars Incorporated

Nestle (Purina)

Vafo Praha, s.r.o.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2024: Nestlé Purina is investing €472 million (≈ USD 508 million) in a new pet food facility in Mantua, Italy. This development aligns with rising demand for locally manufactured, premium pet nutrition and may intensify competition in Italy’s pet food sector, pushing other players to scale or differentiate via ingredients, sustainability, or supply chain localization.

- July 2023: Hill's Pet Nutrition introduced its new MSC (Marine Stewardship Council) certified pollock and insect protein products for pets with sensitive stomachs and skin lines. They contain vitamins, omega-3 fatty acids, and antioxidants.

- May 2023: Nestle Purina launched new cat treats under the Friskies "Friskies Playfuls - treats" brand. These treats are round in shape and are available in chicken and liver and salmon and shrimp flavors for adult cats.

- May 2023: Vafo Praha, s.r.o. launched its new range of Brit RAW Freeze-dried treats and toppers for dogs. These products are made up of high-quality proteins and minimally processed ingredients for potential health benefits.

Italy Pet Food Market Report Scope

The Italy Pet Food Market Report is Segmented Into Pet Food Product (Food, Pet Nutraceuticals/Supplements, Pet Treats, and Pet Veterinary Diets), Pets (Cats, Dogs, and Other Pets), and Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, and Other Channels). Get Five Years of Historical Data and Market Forecasts in Value (USD) and Volume (Tons)

By Pet Food Product

| Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||||

| Wet Pet Food | ||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | ||

| Omega-3 Fatty Acids | ||||

| Probiotics | ||||

| Proteins and Peptides | ||||

| Vitamins and Minerals | ||||

| Other Nutraceuticals | ||||

| Pet Treats | By Sub Product | Crunchy Treats | ||

| Dental Treats | ||||

| Freeze-dried and Jerky Treats | ||||

| Soft and Chewy Treats | ||||

| Other Treats | ||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | ||

| Diabetes | ||||

| Digestive Sensitivity | ||||

| Obesity Diets | ||||

| Oral Care Diets | ||||

| Renal | ||||

| Urinary Tract Disease | ||||

| Other Veterinary Diets |

By Pets

| Cats |

| Dogs |

| Other Pets |

By Distribution Channel

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Pet Food Product | Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||||

| Wet Pet Food | |||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | |||

| Omega-3 Fatty Acids | |||||

| Probiotics | |||||

| Proteins and Peptides | |||||

| Vitamins and Minerals | |||||

| Other Nutraceuticals | |||||

| Pet Treats | By Sub Product | Crunchy Treats | |||

| Dental Treats | |||||

| Freeze-dried and Jerky Treats | |||||

| Soft and Chewy Treats | |||||

| Other Treats | |||||

| Pet Veterinary Diets | By Sub Product | Derma Diets | |||

| Diabetes | |||||

| Digestive Sensitivity | |||||

| Obesity Diets | |||||

| Oral Care Diets | |||||

| Renal | |||||

| Urinary Tract Disease | |||||

| Other Veterinary Diets | |||||

| By Pets | Cats | ||||

| Dogs | |||||

| Other Pets | |||||

| By Distribution Channel | Convenience Stores | ||||

| Online Channel | |||||

| Specialty Stores | |||||

| Supermarkets/Hypermarkets | |||||

| Other Channels | |||||

Need A Different Region or Segment?

Customize Now

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF