Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 17.10 Billion |

| Market Size (2026) | USD 17.96 Billion |

| Market Size (2031) | USD 22.98 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

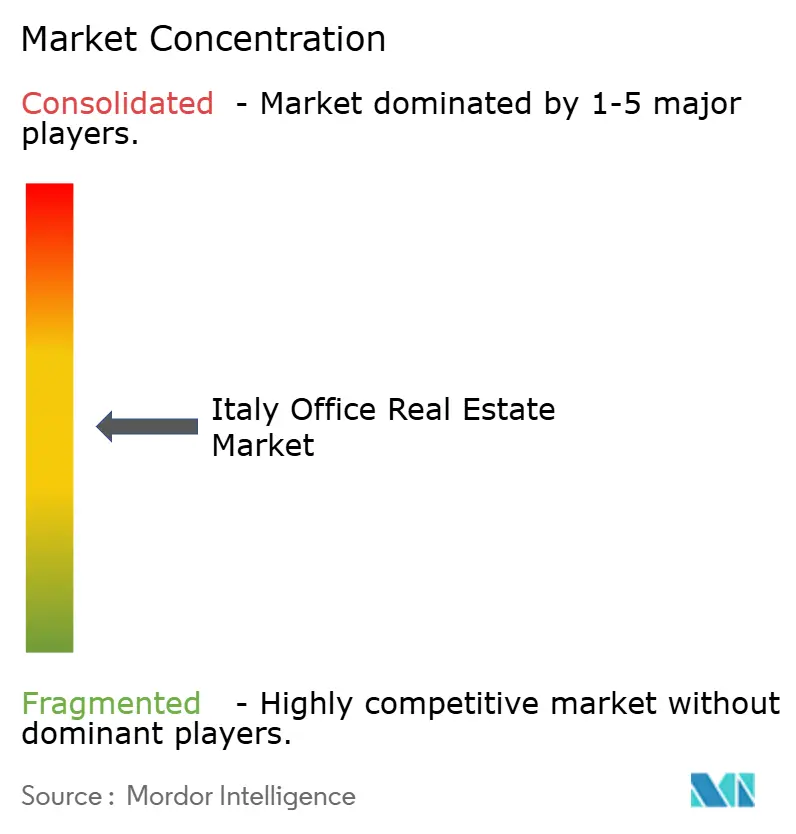

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Office Real Estate Market Analysis by Mordor Intelligence

The Italy office real estate market size is expected to grow from USD 17.10 billion in 2025 to USD 17.96 billion in 2026 and is forecast to reach USD 22.98 billion by 2031 at 5.05% CAGR over 2026-2031. Urban migration, a steady stream of foreign capital and rising demand for ESG-qualified space all underpin this expansion. Segment data show a clear flight to quality: Grade A assets hold the largest share at 45% and are also the fastest mover, advancing at a 5.81% CAGR. Rentals still dominate at 74%, yet investment sales are accelerating with a 6.10% CAGR. On the occupier side, BFSI tenants account for 35% of demand, while IT & ITES is growing quickest at 6.43%. Milan remains the country’s commercial anchor with a 43% share, but Rome is set to outpace it, logging a projected 6.21% CAGR. Rome’s edge lies in lower occupational costs and the connectivity upgrades that form part of the National Recovery and Resilience Plan (NRRP). The European Central Bank (ECB) notes that Italian lenders hold sizeable office exposure; enhanced regulatory oversight is keeping loan-loss provisions on a tight leash. The Bank of Italy adds that construction activity tied to the NRRP is offsetting softness in residential building and is helping sustain the office pipeline.

Key Report Takeaways

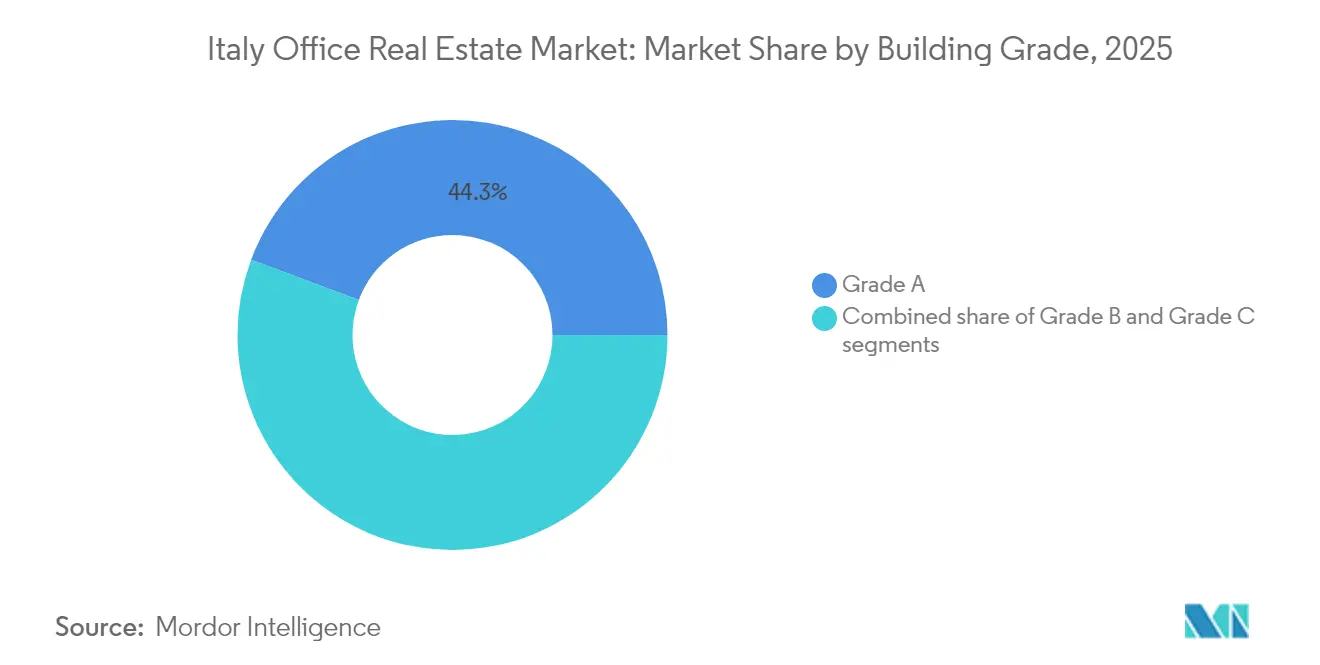

- By building grade, Grade A captured 44.30% of Italy office real estate market share in 2025; the same segment is projected to expand at a 5.62% CAGR through 2031.

- By transaction type, rentals led with 73.45% of revenue in 2025, while sales are forecast to post the fastest 5.93% CAGR between 2026-2031.

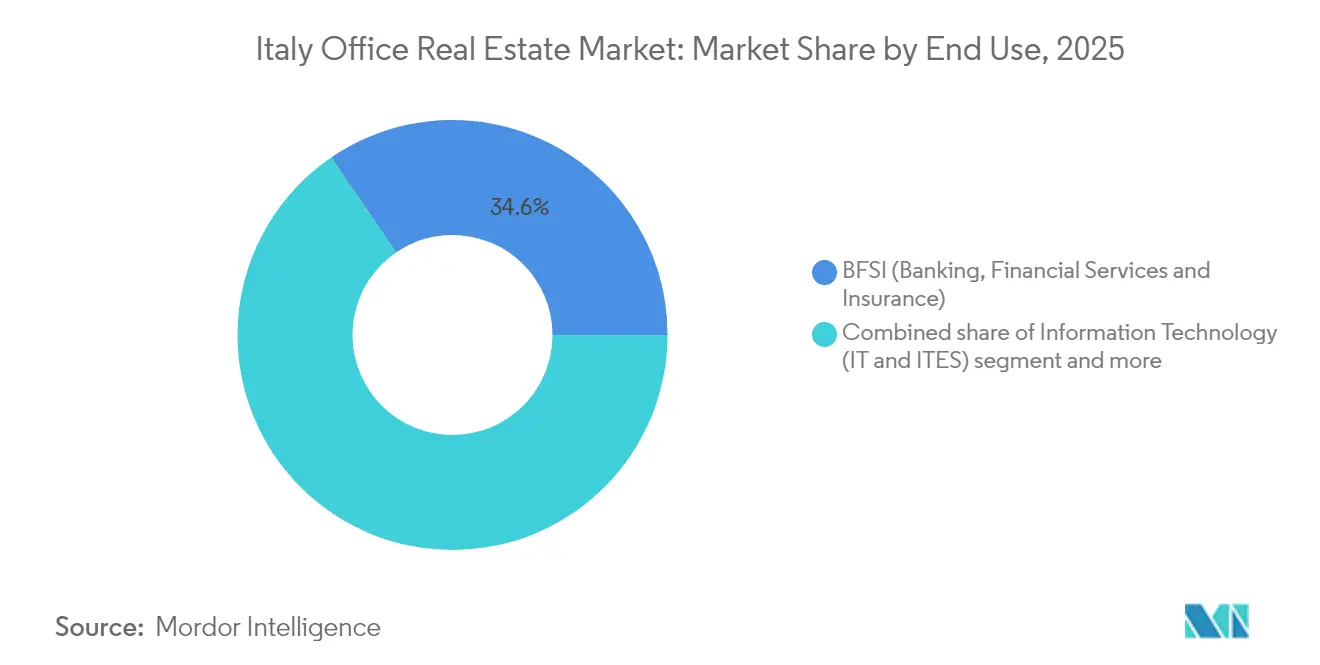

- By end use, BFSI accounted for 34.55% of the Italy office real estate market size in 2025, whereas IT & ITES is expected to grow at a 6.22% CAGR through 2031.

- By city, Milan held 42.60% of national revenue in 2025, but Rome is on track for the strongest 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanisation & Transit-Oriented Development | +1.2% | Milan, Rome, Turin metropolitan areas | Medium term (2-4 years) |

| ESG & Green Building Compliance | +1.1% | Nationwide, early uptake in Milan & Rome | Long term (≥ 4 years) |

| Foreign Institutional Capital Inflow | +0.9% | Milan CBD, Rome EUR district | Short term (≤ 2 years) |

| Coworking & Flex Office Expansion | +0.7% | Milan, Rome city centres | Medium term (2-4 years) |

| Shift to Hybrid Work Models | +0.6% | Milan, Rome, Turin | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urbanisation & Transit-Oriented Development

Government spending is tilting decisively toward transport. Of the USD 15.0 billion raised by 2023 BTP Green bonds, 41.5% went to rail and metro projects[1]Maria Teresa Cannata, “BTP Green Allocation Report 2023,” Ministero dell’Economia e delle Finanze, mef.gov.it. Politecnico di Torino finds that mixed-use nodes such as Naples’ Municipio outperform single-use clusters on transit uptake. NRRP upgrades are also smoothing city-to-city links; the Bank of Italy reports that these works are shoring up construction even as the wider economy cools

Foreign Institutional Capital Inflow

The euro area posted a USD 464.3 billion current-account surplus in 2024, providing deep capital pools for real-asset allocations. ECB research shows rapid growth in pan-European real-estate funds, many targeting Italian offices. In Piemonte alone, 27 FDI projects announced in 2024 carry a USD 4.36 billion price tag, 18% of which is real estate. Borrowing costs are also supportive: the average rate on new corporate loans slipped to 3.79% in April 2025

Coworking & Flex Office Expansion

ECB outreach to non-financial firms highlights a sharper focus on variable costs, prompting wider adoption of subscription-based space. Although the Bank of Italy notes subdued capex on plant and equipment, service-sector resilience is pushing demand for turnkey offices. Across EMEA, flex inventory grew by 161,303 m² in 2023, and Milan operators report strong pre-leasing from names such as Microsoft and HSBC.

ESG & Green Building Compliance

The Energy Performance of Buildings Directive requires a 16% energy-use cut by 2030 and zero-emission standards for new private buildings from January 2030. ECB modelling suggests the EU must invest USD 677.8 billion a year through 2030 to stay on track. Italy is leaning on BTP Green proceeds and tax credits (now a 5% deduction, rising to 7.5% in 2025) to help owners fund upgrades. Early adopters already see the benefit: Generali’s green offices command 5%-7% rent premiums, and Stoneweg has 85% of its Italian assets pre-labelled “green” with an 83 GRESB score.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Office Stock and Retrofit Costs | −0.8% | Milan periphery, Rome secondary districts | Long term (≥ 4 years) |

| Rising Construction and Fit-Out Costs | −0.6% | National, with acute pressure in Milan & Rome | Medium term (2-4 years) |

| Low Availability of Suitable Redevelopment Land | −0.4% | Core CBD plots in Milan, Rome and other tier-1 submarkets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Office Stock and Retrofit Costs

Italy’s office landscape is grappling with the legacy of outdated infrastructure. Over 65% of the country’s commercial buildings were constructed before 1980, yet the annual renovation rate remains just 0.81%, falling far short of EU climate targets.[2]Roberto Cingolani, “National Climate & Energy Plan Update,” Ministry for Ecological Transition, mase.gov.it Although refurbishments can lift asset value by approximately 13.5%, many owners—especially in fringe submarkets—struggle to fund deep retrofits, as prevailing rents often fail to justify the return on cost. This mismatch fuels rising vacancy risk for obsolete stock, pushing tenants to prioritise Grade A space. As a result, Italy’s office market continues to experience a structural split, where the flight-to-quality trend accelerates, but net absorption in older districts remains constrained.

Rising Construction and Fit-Out Costs

Cost pressures are reshaping Italy’s office development pipeline. In 2022, total construction spending hit USD 177.56 billion, but inflation in materials and labour sharply compressed developer margins, extending into the realm of premium office fit-outs[3]Emily Sanchez, “Italy – Construction Market Overview 2024,” U.S. Department of Commerce, trade.gov. The Superbonus 110% tax incentive, though aimed at stimulating renovations, tightened contractor availability and exacerbated price escalations, causing project delays and downsizing across multiple office pipelines. In this environment, developers have become cautious with speculative starts, leading to prolonged supply gaps in high-demand urban zones. Until costs stabilise, this situation is likely to restrict future take-up and delay much-needed inventory in core office corridors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Premium Quality Commands Market Leadership

Grade A stock commands 44.30% of the market in 2025 and is projected to grow at a 5.62% CAGR through 2031. ECB valuation guidance underlines lenders’ preference for energy-efficient assets. Semi-annual data from Agenzia delle Entrate confirm that top locations fetch a 20% premium over suburban equivalents. With only 515,000 m² of Grade A space due by 2027, rents appear set for further upside.

Flight-to-quality also manifests beyond Milan. In Rome, prime EUR district schemes obtain USD 654 per m² rents and capture greater international occupier interest on the back of new metro extensions. Meanwhile, Grade B stock remains the cost-efficient alternative, particularly for companies pivoting to suburban hubs amid hybrid work. Yet retrofitting costs and looming EU efficiency rules weigh on Grade C assets, accelerating disposals, conversions, or demolitions. Overall, the Grade A segment is set to post the fastest 5.62% CAGR through 2031, ensuring it continues to anchor future demand and pricing trends across the Italy office real estate market.

By Transaction Type: Rental Dominance with Sales Acceleration

Rental agreements accounted for 73.45% of total activity in 2025, reflecting Italy’s custom of long-term leasing and flexible renewal clauses, but sales are catching up, forecasting a 5.93% CAGR. The ECB’s lending survey shows only a small tightening in corporate credit, while looser housing standards free up bank balance sheets for commercial deals. Corporate sale-and-leasebacks are gaining traction as firms unlock capital without surrendering operational control.

Domestic investors dominated 77% of Q1 2025 sales volume, underscoring local conviction in core assets, but cross-border parties remain active at the upper end of the market. Corporates are turning to sale-and-leaseback structures to free cash for core operations, especially in capital-intensive sectors such as manufacturing and utilities. For landlords, these hybrid models lock in long leases from credit-strong tenants, improving financing terms and portfolio valuations. Such dynamics support a gradual convergence between leasing and owning behaviour in the Italy office real estate market, even as rentals remain the principal mode.

By End Use: BFSI (Banking, Financial Services and Insurance) Leadership with Technology Sector Momentum

BFSI (Banking, Financial Services and Insurance) occupiers commanded 34.55% of Italy office real estate market size in 2025, anchored by Milan’s Porta Nuova and Rome’s banking quarters. Although branch optimisation is trimming space needs, headquarters demand stays resilient, often requiring advanced security and ESG features. The IT & ITES cohort is accelerating fastest at a 6.22% CAGR, fed by digital-transformation budgets and the draw of Italy’s large domestic consumer base. These firms frequently adopt agile workplace layouts and shorter lease horizons, fuelling the rise of managed-flex platforms.

Professional services firms, notably auditors and legal advisors, maintain steady absorption, driven by rising regulatory complexity around sustainability and data privacy. Life sciences, energy, and creative industries round out demand but increasingly stipulate net-zero pathways when negotiating new tenancies. Collectively, this end-user mosaic fosters nuanced demand profiles that landlords must accommodate to maximise occupancy and yield within the Italy office real estate market.

Geography Analysis

Italy’s office landscape pivots on two hubs: Milan retains a 42.60% grip thanks to its deep financial ecosystem, premier universities, and four-line metro grid that underpins commuter flows. Scarce Grade A supply and consistent cross-border capital inflows keep yields firm and rents at historic peaks, though development land in prime zones is nearly exhausted. Rome trails in share yet outpaces in growth, fuelled by a 6.05% CAGR outlook as metro extensions and rail upgrades lift the appeal of once-peripheral EUR and Tiburtina districts to multinationals seeking cost savings without compromising connectivity.

Regional diversification is gaining momentum. The Piemonte region’s 2024 haul of 27 foreign direct investment projects, worth USD 4.36 billion, underscores the draw of cost-advantaged northern cities such as Turin and Novara where office conversions can ride on established manufacturing clusters. Further south, Bologna and Florence benefit from large university populations that feed tenant pipelines in research, IT, and life science spin-offs; government grants for digitalisation are particularly appealing to these knowledge hubs. Naples and Bari illustrate a different narrative, leveraging expanded high-speed rail and port capacities to attract back-office shared-service centres seeking affordable labour but international reach. Transit-oriented investment via the NRRP is knitting these nodes into a more integrated network, letting occupiers deploy hub-and-spoke strategies that reduce occupancy cost per employee while preserving access to Italy’s flagship cities. As the Italy office real estate market matures, such multi-city location strategies help mitigate risk, ease recruitment, and meet employee preference for shorter commutes and affordable housing.

Competitive Landscape

The Italy office real estate market displays moderate concentration. International advisory firms CBRE, Jones Lang LaSalle IP, and Cushman & Wakefield continue to intermediate the lion’s share of large-ticket leasing and investment deals thanks to pan-European client relationships and end-to-end data platforms. Their service breadth—ranging from capital markets to ESG consultancy—creates stickiness with multinationals that prefer one-stop solutions. Domestic stalwarts such as Gabetti Property Solutions wield strong local knowledge, municipal contacts, and asset-management capabilities that help them compete effectively for mid-sized disposals and occupier mandates.

REITs and long-hold institutional investors remain essential demand drivers: Covivio lifted occupancy to 95.5% on its USD 16.79 billion Italy-focused portfolio by concentrating on city-centre properties with high sustainability ratings. COIMA RES and Generali Real Estate are likewise doubling down on value-add refurbishments that align with EU climate rules, a strategy rewarded by rental outperformance and lower obsolescence risk. Foreign capital—ranging from Korean pension funds to Canadian REITs—targets stand-alone trophy assets or joint ventures that accelerate ESG upgrades, injecting fresh competition for limited core product.

PropTech adoption is where the next wave of differentiation is forming. Leading managers deploy occupancy analytics, touchless access, and carbon-tracking dashboards that boost tenant satisfaction and command premium rents. Local specialists with deep micro-market intelligence often partner with these technology providers to integrate smart-building solutions quickly. The result is a multilayered playing field in which scale, sustainability credentials, and digital capability jointly determine competitive edge within the Italy office real estate market.

Italy Office Real Estate Industry Leaders

CBRE

Jones Lang LaSalle IP

Cushman & Wakefield

Savills

Colliers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ECB data show new corporate loan rates down to 3.79%, easing financing for office deals.

- February 2025: Bank of Italy Governor Fabio Panetta underscores NRRP infrastructure as a productivity lever.

- January 2025: Bank of Italy sees construction buoyed by NRRP projects despite a softer housing market.

- December 2024: MEF reports USD 2.72 trillion in outstanding government securities at an average 3.60% yield.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italy office real estate market as all revenue generated from developing, acquiring, leasing, and selling dedicated office buildings across the country's key urban clusters, measured in constant 2024 US dollars. Assets are classified by building grade (A, B, C) and by transaction route (rental or sale), and then mapped to end-user sectors such as IT-ITES, financial services, business consulting, and other services. According to Mordor Intelligence, the addressable pool therefore captures standing stock, new completions, and refurbishments that return to the office inventory.

Scope Exclusions: Pure coworking membership fees, mixed-use properties where office space is below fifty percent of lettable area, and land-bank trading are left outside the definition.

Segmentation Overview

- By Building Grade

- Grade A

- Grade B

- Grade C

- By Transaction Type

- Rental

- Sales

- By End Use

- Information Technology (IT and ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Services

- Other Services (Retail, Lifesciences, Energy, Legal Services)

- By City

- Milan

- Rome

- Turin

- Rest of Italy

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interview asset managers, brokerage heads, corporate real estate occupiers, and local valuers spread across Milan, Rome, Turin, and secondary cities. Conversations test demand assumptions around hybrid working, verify achievable rents by grade, and gauge cap rate expectations, which helps us close data gaps and recalibrate early desk findings.

Desk Research

We begin with publicly available macro and sector statistics from ISTAT, the Bank of Italy real estate dashboard, and the Ministry of Infrastructure building permit files, which anchor total stock and construction pipelines. Additional insights flow from the European Public Real Estate Association, the Italian Revenue Agency's quarterly deed data, and reputable trade journals that monitor prime rents and yields in Milan and Rome. Company filings, investor presentations, and news archives accessed through D & B Hoovers and Dow Jones Factiva complement the picture by revealing developer balance sheets and major leasing deals. These sources are illustrative; many other publications inform the evidence base used for validation and clarification.

Market-Sizing & Forecasting

We apply a top-down model that reconstructs national revenue from stock inventories and city-level rent trajectories, followed by selective bottom-up checks built from sampled average selling price times volume on key transactions. Variables such as vacancy rate shifts, Grade A delivery pipeline, prime yield movement, foreign direct investment, corporate employment growth, and ESG-led retrofit costs feed the model. Multivariate regression, chosen for its transparency, projects each driver and generates the 2025-2030 outlook, with scenario overlays for interest rate and remote work adoption shocks. Where bottom-up estimates diverge, variance is prorated to the most reliable city evidence set.

Data Validation & Update Cycle

Outputs undergo variance checks against third-party indices, analyst peer review, and a senior sign-off. We refresh every twelve months, re-contacting sources sooner if material events, policy shifts, or major portfolio trades occur, and a final sweep is completed just before report release.

Why Mordor's Italy Office Real Estate Baseline Stands Up to Scrutiny

Published figures often differ because firms pick contrasting asset mixes, rental benchmarks, and refresh cadences.

The main divergence usually stems from whether Grade C buildings or small provincial stock are included and from how aggressive rent growth assumptions are embedded.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.10 Bn (2025) | Mordor Intelligence | |

| USD 21.40 Bn (2024) | Global Consultancy A | Focuses only on Milan and Rome and inflates totals by applying a single rent multiplier across grades |

| EUR 10.00 Bn (2025) | Industry Association B | Blends office with flexible workspace service revenue and omits Grade B renovations |

The comparison shows that, by selecting a balanced scope, triangulating variables, and maintaining an annual refresh, Mordor Intelligence delivers a dependable baseline that decision makers can replicate and audit with limited effort.

Key Questions Answered in the Report

What is the current value of the Italy office real estate market?

It stands at USD 17.96 billion in 2026 and is projected to reach USD 22.98 billion by 2031.

Which city holds the largest share of Italy’s office market?

Milan leads with 42.60% market share in 2025, underpinned by its financial sector concentration and limited Grade A supply.

Why is Rome expected to grow faster than Milan?

Ongoing NRRP infrastructure upgrades and lower occupancy costs are forecast to drive a 6.05% CAGR for Rome through 2031.

What segment is expanding the quickest by end-user category?

The IT & ITES segment is predicted to grow at a 6.22% CAGR, fuelled by digital-transformation investments.

How important is ESG compliance for Italian office assets?

Highly important: 32% of older stock risks obsolescence by 2030, and certified green buildings command rent premiums of 5%-7%.

Are flexible offices gaining ground in Italy?

Yes, EMEA flex inventory grew by over 161,000 m² in 2023, and corporate tenants increasingly secure flexible space in Milan and Rome.

Page last updated on: