Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

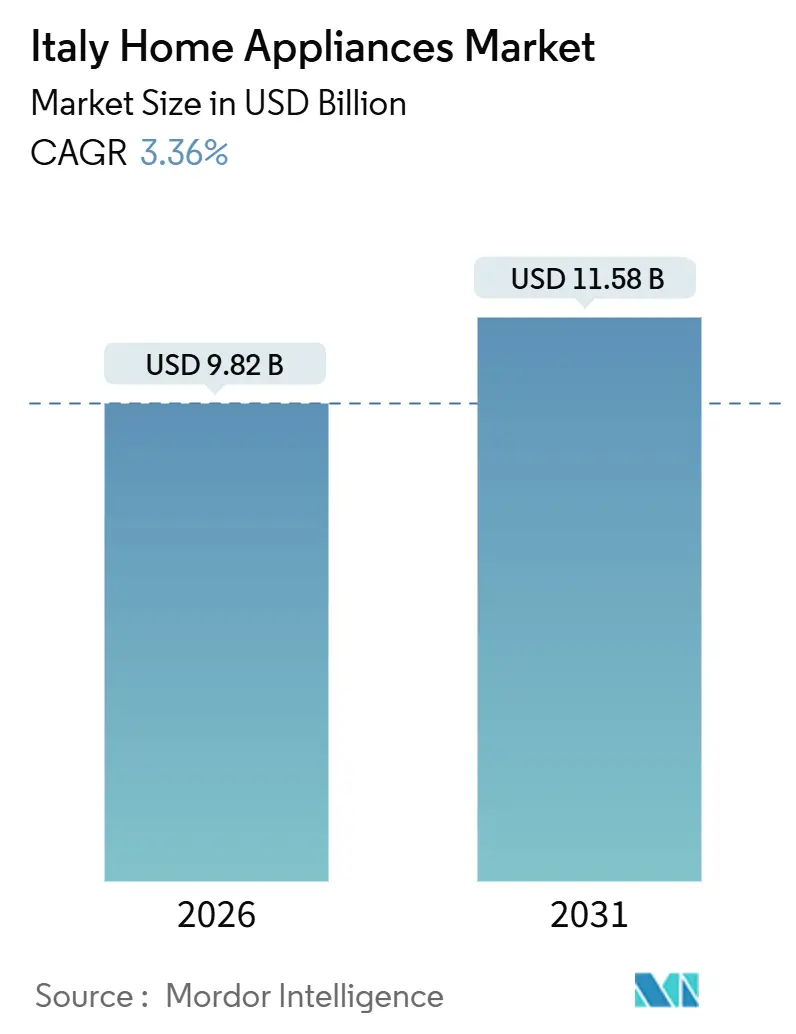

| Market Size (2026) | USD 9.82 Billion |

| Market Size (2031) | USD 11.58 Billion |

| Growth Rate (2026 - 2031) | 3.36% CAGR |

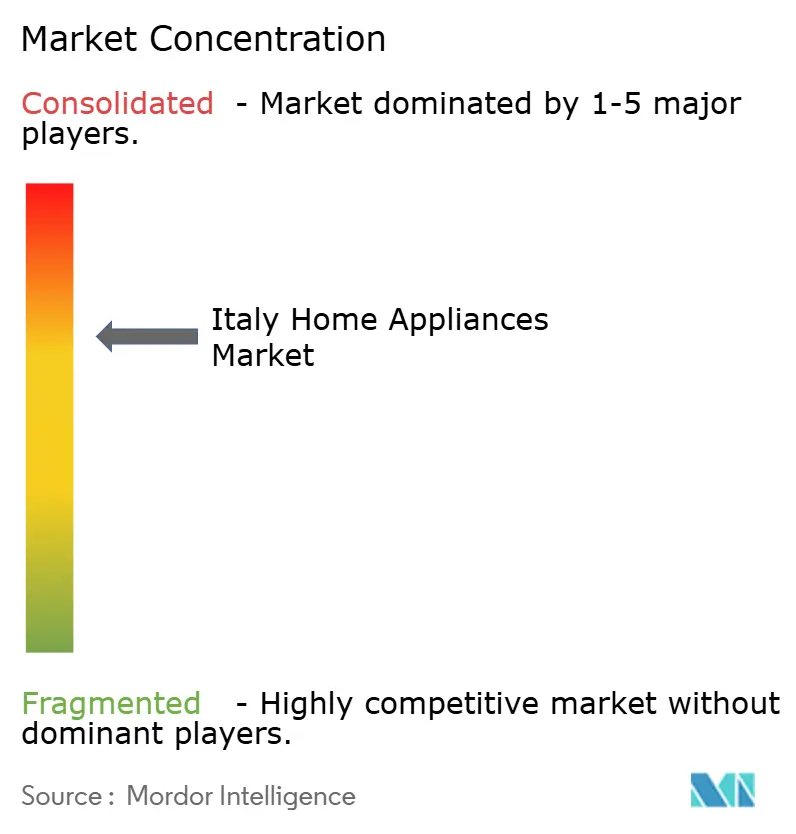

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Home Appliances Market Analysis by Mordor Intelligence

The Italy home appliances market size is valued at USD 9.82 billion in 2026 and is forecast to reach USD 11.58 billion by 2031, expanding at a CAGR of 3.36%. The trajectory builds on a historical CAGR of 3.15% from 2020 to 2025, underscoring steady replacement cycles across mature categories. Policy incentives, EU Ecodesign mandates, and consumer prioritization of lifetime running-cost savings are supporting demand for high-efficiency appliances in core product lines. Digital features that enhance energy optimization and user convenience are gaining relevance, as platforms such as Home and SmartThings link appliances to dynamic tariffs and remote diagnostics, reinforcing ecosystem lock-in in the Italy home appliances market.

Key Report Takeaways

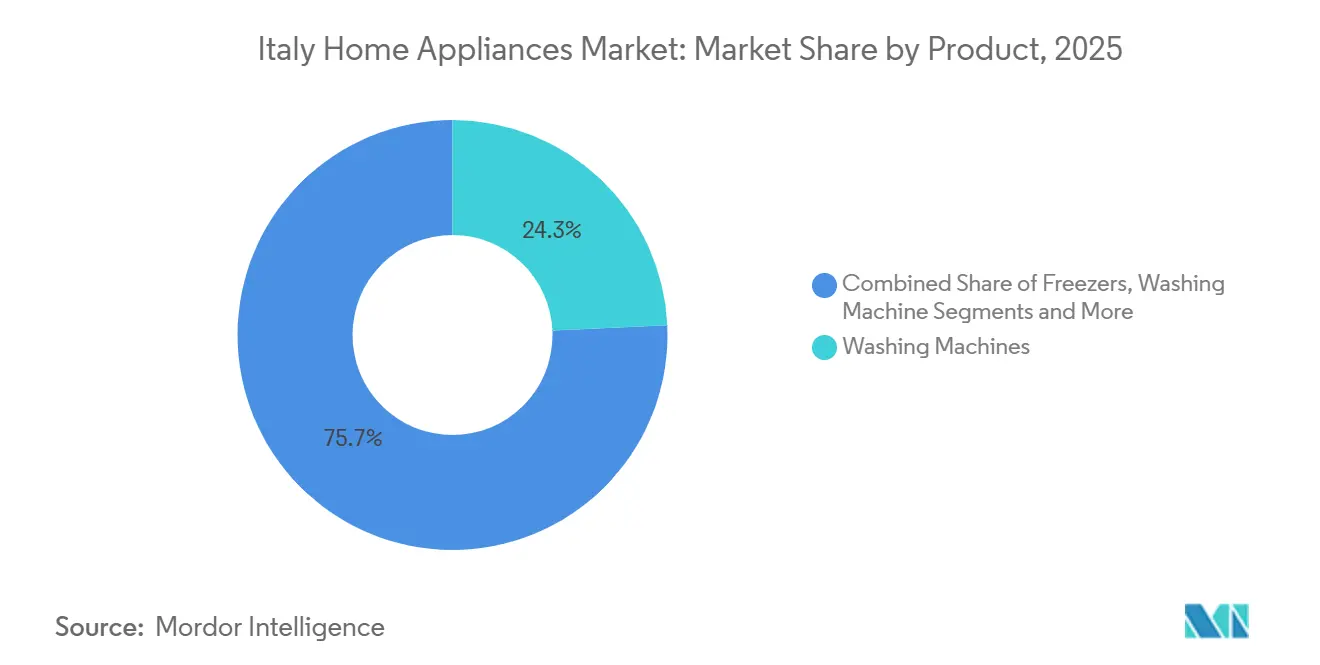

- By product type, washing machines led the Italy Home Appliances Market with a 23.63% revenue share in 2025, while coffee makers are forecast to expand at a 3.81% CAGR through 2031.

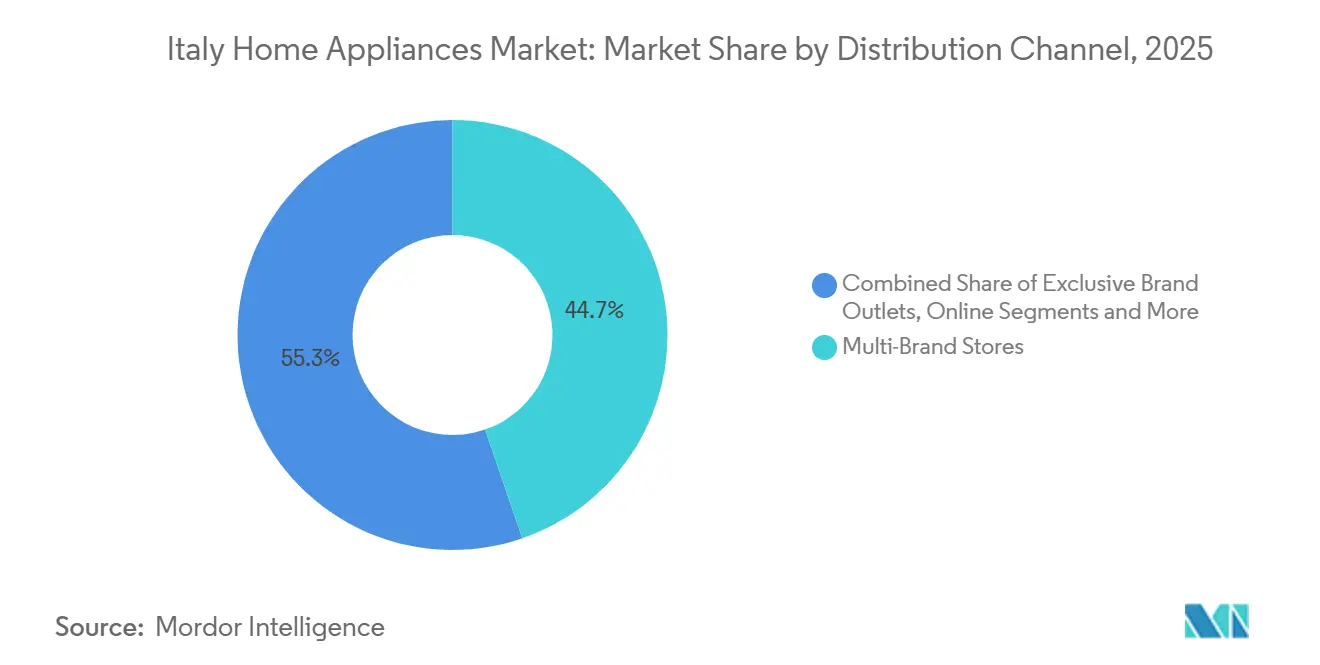

- By distribution channel, multi-brand stores held 44.72% share in 2025, while online recorded the highest projected growth at a 4.46% CAGR through 2030.

- By geography, North-West Italy accounted for a 24.81% share of the Italy Home Appliances Market in 2025, while Central Italy is forecast to grow the fastest at a 3.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Home Appliances Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency regulations are driving accelerated replacement cycles | +0.8% | National, EU-wide regulatory alignment | Short term (≤ 2 years) |

| Surge in smart/connected-appliance adoption supported by broadband | +0.6% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| E-commerce and omnichannel retail growth are expanding consumer reach | +0.5% | National, strongest in Lombardy, Lazio, Emilia-Romagna | Medium term (2-4 years) |

| 110% Superbonus renovation scheme boosting efficient white goods | +0.4% | National, early gains in Lombardy, Veneto, Tuscany | Short term (≤ 2 years) |

| Premium built-in formats favored by compact urban kitchens | +0.3% | Metropolitan areas and high-income urban households | Long term (≥ 4 years) |

| EU Right-to-Repair policy stimulating modular upgradable models | +0.2% | EU27 with phased compliance across Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Regulations Driving Accelerated Replacement Cycles

Italy’s 2025 Budget Law extends the Furniture and Appliances Bonus, allowing a 50% tax deduction on eligible appliance purchases up to EUR 5,000 for homes undergoing renovation, provided that products meet Class A energy thresholds[1]FiatLux, “Tax Bonuses in Italy: All the news for 2025,” FiatLux, fiatlux.legal . The updated policy stance away from fossil-fuel appliances is also channeling consumer adoption toward electric heat pumps and induction cooking, reinforcing a replacement wave for older, inefficient units. This mix of incentives and regulations is extending the upgrade cycle in the Italy home appliances market as manufacturers align assortments and pricing to energy labels and lifetime cost-of-ownership.

Surge in Smart/Connected-Appliance Adoption Supported by Broadband Penetration

Smart appliances have reached 40% of households by 2025 as fiber connectivity spreads across major cities and as consumers seek convenience, usage insights, and energy savings through app-linked control. Haier Europe’s hOn platform integrates with an Italian digital energy supplier so that users can schedule cycles at off-peak hours tied to real-time electricity prices, enabling measurable bill reductions alongside lower grid strain. Samsung’s SmartThings adds household safety and care features through connected devices, positioning white goods within a broader home ecosystem that can automate energy-aware behavior[2]Samsung Electronics, “Samsung Electronics Unveils ‘AI Home’ Vision at Welcome to Bespoke AI Event,” Samsung Newsroom, news.samsung.com. The adoption curve is strongest in urban regions where income and network coverage support premium features, and these factors amplify ecosystem stickiness in the Italy home appliances market. Despite momentum, interoperability remains a hurdle for mainstream users, although incremental support for cross-brand standards is improving the user experience over time.

E-Commerce & Omnichannel Retail Growth Expanding Consumer Reach

E-commerce is expanding its role in appliances, leading retailers have scaled hybrid store formats and marketplace integrations to widen assortments without proportionate inventory risk, which helps meet varied price and feature preferences. The market, valued at EUR 85.4 billion across all e-commerce categories, is growing at an 8.46% CAGR from 2025 to 2029, with consumer electronics and home appliances[3]Landmark Global, “Top 10 Essential Facts About Italian E-commerce (2025 Edition),” Landmark Global, landmarkglobal.com. Service and logistics upgrades are also material, with spare-parts consolidation hubs and automation cutting delivery times and enabling rapid after-sales response in dense urban centers. Greater online exposure is accelerating the diffusion of energy-efficient and connected models, increasing price transparency and speeding feature adoption in the Italy home appliances market. The channel’s growth reinforces demand-side flexibility as shoppers compare lifetime cost-of-ownership and evaluate total service propositions beyond headline prices.

110% "Superbonus" Renovation Scheme Boosting Demand for Efficient White Goods

The Superbonus tax credit triggered a renovation wave and has maintained a meaningful incentive for energy-efficient upgrades within eligible projects. The policy accelerated the replacement of older appliances during 2021 to 2023, lifting unit sales growth for core white goods above long-term trend lines. The step-down in the program altered volumes for single-family homes, yet condominium projects meeting timeline thresholds continued to support demand in 2025. Manufacturers are pivoting by repackaging incentives: the 2025 Appliance Bonus, capped at EUR 200 for households with ISEE below EUR 25,000, offers a direct 30% discount at the point of sale for high-efficiency units (Class A washing machines, Class B cooker hoods), with a total fund of EUR 48 million[4]Salone del Mobile.Milano, “2025 Appliance Bonus: how it works and what it includes,” Salone del Mobile.Milano, www.salonemilano.it. Yet this smaller-scale subsidy is unlikely to replicate the Superbonus's volume impact, recalibrating the market toward organic replacement demand rather than policy-induced surges.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-driven squeeze on discretionary spending | -0.6% | Southern and Central Italy, price-sensitive areas | Short term (≤ 2 years) |

| Supply-chain and raw-material price volatility | -0.5% | National, acute in manufacturing hubs | Short term (≤ 2 years) |

| Rising compliance costs for SMEs | -0.3% | National, disproportionate burden on SME suppliers | Medium term (2-4 years) |

| Category saturation lengthening replacement cycles | -0.4% | Mature markets in North-West and Central Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inflation-Driven Squeeze on Discretionary Spending

Households contended with real-income pressure in 2024 and early 2025, which tempered upgrades in non-essential categories and favored value-led offerings. The most pronounced impact emerged in regions with lower income levels, where price sensitivity was high, and promotions drove a disproportionate share of volume. Brands expanded accessible price points for efficient models to preserve category momentum, often pairing affordability with energy savings to support adoption. Promotions and financing options became more prominent, although sustained discounting risks eroding margins if input costs remain elevated in the Italy home appliances market. These dynamics reinforced the importance of after-sales networks and repairability, which help extend product life and protect household budgets.

Supply-Chain & Raw-Material Price Volatility

Global supply conditions increased cost complexity for manufacturers, especially for electronics-rich models that depend on semiconductors and sensors. Companies responded with design changes that optimize component count and with procurement strategies that diversify sources where feasible. Logistics volatility added to planning challenges, which elevated the value of local spare-parts hubs and automated fulfillment to maintain service levels. Persistent input-cost pressure increases the need for pricing discipline and differentiated features to sustain category mix in the Italy home appliances market. In this context, investment in energy-efficient R&D and platform modularity helps reduce cost volatility over product lifecycles.

Segment Analysis

By Product: Major Appliances Anchor Market, Small Appliances Accelerate

Within Major Appliances, washing machines led with 23.63% of Italy's home appliances market share in 2025 as replacements advanced due to energy labels and running-cost awareness. Refrigerators followed as a core category, with energy-efficient formats gaining ground and digital features helping users optimize food preservation and electricity usage. Premium models increasingly differentiate through AI-enabled programs and integration with home platforms that schedule cycles based on tariffs and occupancy. These patterns show how mature categories sustain renewal as performance, connectivity, and energy savings converge in the Italy home appliances market.

Small Appliances outpaced growth with shorter replacement cycles and strong demand for convenience, wellness, and at-home beverage experiences. Coffee makers are projected to grow at a 3.81% CAGR, benefiting from Italy’s espresso culture and from product innovation that brings customizable profiles to everyday use. Multifunctional designs like air fryers with dehydration features and compact food-prep devices resonate with smaller households and urban kitchens that prioritize space and utility. The Italy home appliances industry continues to blend design and performance in Small Appliances, capturing cross-category spending from consumers who value modular, counter-friendly systems. Combined with energy-use optimization, these trends reinforce steady upgrade cycles that support the Italy home appliances market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Multi-Brand Stores Retain Dominance, Online Surges

Multi-brand stores held 44.72% of value in 2025, reflecting the channel’s role in enabling hands-on evaluation, guided selling, and immediate pickup for large outlays within the Italy home appliances market. Store formats have evolved with digital tools that extend assortments beyond shelf space, while integrated inventory and expedited pickup compress the time from decision to use. Exclusive brand outlets serve premium positioning where service, warranty extensions, and ecosystem experiences reinforce loyalty and total cost-of-ownership confidence. These dynamics sustain the physical channel’s relevance as shoppers compare energy labels and consider repairability alongside price, anchoring the path-to-purchase in the Italy home appliances market. As store traffic patterns normalize, curated assortments and service propositions remain central to conversion in the Italy home appliances industry.

Online distribution is the fastest-growing channel at a projected 4.46% CAGR through 2030, driven by mobile commerce, transparent pricing, and marketplace breadth. Retailers and brands are scaling integrated models, pairing web discovery with in-store pickup and quick delivery, which improves customer experience in dense cities. Online share is high for Small Appliances, where rapid replenishment and accessory ecosystems encourage recurring purchases, while major appliances benefit from rich content and reviews. The Italy home appliances market is seeing logistics investments that cut spare-parts lead times and strengthen after-sales coverage, a differentiator for smart and efficient models. These omnichannel enhancements reinforce trust and speed, which are key to purchase decisions in higher-priced categories.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The North-West region, anchored by Lombardy and Milan, held 24.81% of value in 2025 as dense urbanization, higher incomes, and strong service networks supported premium adoption in the Italy home appliances market. The region is also a focal point for smart-appliance usage, which aligns with better broadband availability and greater exposure to connected ecosystems. As the largest regional base, the North-West is transitioning toward more stable growth as policy-driven spikes give way to standard replacement cycles. The Italy home appliances market benefits from supply-chain assets in Lombardy, including consolidated spare-parts hubs that help maintain service quality.

Central Italy is the fastest-growing region with a projected 3.75% CAGR, supported by Rome’s large urban base, ongoing renovations, and a tilt toward built-in formats in high-density housing. Higher adoption of energy labels and upgrade incentives is contributing to increased demand for efficient appliances across kitchens and laundry. The tourism sector also lifts upgrade cycles in properties that consider both guest expectations and running costs, especially for dishwashers and refrigerators aligned with energy thresholds. The Italy home appliances market has also seen expanding connected adoption in Rome and Florence as ecosystem integrations gain visibility through retailer marketing. These patterns sustain regional momentum and reinforce mid-term growth.

The Rest of Italy accounted for 18% of the value and grew at a 2.7% pace, reflecting tighter budgets and a higher share of price-led purchases within the Italy home appliances market. Online channels are important in this region for access to a wider range of models and for price transparency, which supports the adoption of efficient units even where retail assortments are limited. Right-to-repair obligations and spare-parts availability apply nationwide, and improved information flows will support lifetime value for households outside major cities. Uniform application of EU policies should continue to enhance product choice and service quality across all regions over time.

Competitive Landscape

The Italy home appliances market operates with moderate consolidation as the top five players collectively hold about half the share, though a long tail of brands and private labels maintains price competition across tiers. In April 2024, Whirlpool contributed its European MDA business to Beko Europe with Arçelik, establishing a platform of 24 million units of annual capacity, reshaping sourcing, branding, and service strategies in the region. This combination advances scale benefits in procurement and logistics that can translate into competitive pricing and broader coverage for Italian consumers. Competitors are emphasizing technology and service differentiation as a counterbalance, underpinned by energy efficiency and connectivity.

Digital ecosystems remain core to brand strategies as platforms deliver value through energy optimization, maintenance prompts, and household coordination features. Haier Europe’s Home platform exemplifies appliance-utility integration in Italy, aligning device operation with wholesale electricity pricing to lower running costs, which can reinforce appliance replacement intent. Logistics upgrades support these models, with spare-parts hubs designed to improve service times and support right-to-repair compliance in the Italy home appliances market. Investment in energy-efficiency R&D is ongoing across leading groups, aided by financing programs that target lower consumption, improved recyclability, and modular design.

Premium and built-in ranges benefit from urban design trends and smaller household sizes, while accessible price points remain critical in regions with tighter budgets. Brands pair aesthetic coherence with practical features such as app-linked operation and programmable modes that align with tariffs, which deepens ecosystem stickiness in the Italy home appliances market. Companies position after-sales networks and spare-parts availability as part of the value proposition amid new right-to-repair obligations, encouraging lifetime service relationships beyond initial sale. These strategies collectively balance short-term pricing pressures with long-term customer value anchored in energy efficiency and reliability.

Italy Home Appliances Industry Leaders

Whirlpool Corp (incl. Indesit)

Haier Europe / Candy Hoover

BSH Hausgeräte GmbH

Electrolux AB

Arçelik AŞ (Beko, Grundig)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Whirlpool Corporation revealed a planned USD 300 million investment to expand its laundry manufacturing operations in Clyde and Marion, Ohio, creating an estimated 400–600 new jobs and strengthening domestic production of washers and dryers.

- March 2025: Samsung unveiled its refreshed AI Home vision and 2025 Bespoke AI appliances at the global “Welcome to Bespoke AI” event in Seoul, showcasing AI Home screens on refrigerators, washers/dryers, and new laundry units. AI Vision Inside can recognise a broad range of food items (up to 37) to enhance food management, and energy-efficient laundry models offer substantial savings.

- December 2024: The European Investment Bank agreed a EUR 200 million loan to Electrolux Group to support R&D and innovation in energy-efficient household appliances across Italy, Sweden, Germany, Poland, and Romania, aligning with sustainability and digital goals.

- April 2024: Whirlpool Corporation completed its strategic transaction with Arçelik, contributing its European major domestic appliance business to form Beko Europe, now the largest home appliance maker in Europe with ~24 million annual unit capacity and over 20,000 employees. Whirlpool retains a 25% stake.

Italy Home Appliances Market Report Scope

This report provides a complete background analysis of the Italian home appliances market, including an assessment of the economy, emerging market trends by segments, significant changes in the market dynamics, and the market overview. The Italy Home Appliances Market is segmented by Major Appliances (Refrigerators, Freezers, Dishwashing Machines, Washing Machines, Air Conditioners, Ovens, Other Major Appliances), Small Appliances (Vacuum Cleaners, Food Processors, Toasters, Grills and Roasters, Coffee Machines, and Other Small Appliances), and Distribution Channel (Multi-Brand Stores, Exclusive Brand Outlets, Online, and Other Distribution Channels). The report offers market size and forecast values for the Italy Home Appliances Market in USD Billion for the above segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Counter-top Ovens | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography (Italy)

| North-West (Lombardy, Piedmont, Liguria, Aosta) |

| Central (Tuscany, Lazio, Umbria, Marche) |

| Rest of Italy |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Counter-top Ovens | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography (Italy) | North-West (Lombardy, Piedmont, Liguria, Aosta) | |

| Central (Tuscany, Lazio, Umbria, Marche) | ||

| Rest of Italy | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the size and growth outlook for the Italy home appliances market from 2026 to 2031?

The Italy home appliances market size is USD 9.82 billion in 2026 and is expected to reach USD 11.58 billion by 2031 at a 3.36% CAGR.

Which product categories lead demand in Italy and why?

Major Appliances anchor value while washing machines lead share due to energy-label driven replacements, and coffee makers are among the fastest-growing on the back of at-home espresso culture.

How are policy incentives shaping appliance upgrades in Italy?

The 2025 Budget Law extends appliance-related tax deductions linked to Class A thresholds, and EU Ecodesign rules reinforce a sustained replacement cycle for efficient models.

Which channels are gaining share in the Italian appliance space?

Multi-brand stores remain the largest, while online is the fastest-growing with a projected 4.46% CAGR through 2030 as omnichannel capabilities expand.

What regions are most significant for appliance sales in Italy?

The North-West leads with 24.81% share, while Central Italy is the fastest growing at a 3.75% CAGR due to urban density and renovation activity.

How are connectivity and right-to-repair shaping competition?

Ecosystems like SmartThings and hOn enable energy-aware use and remote features, while right-to-repair obligations emphasize service networks and spare-parts availability across the product lifecycle.