Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

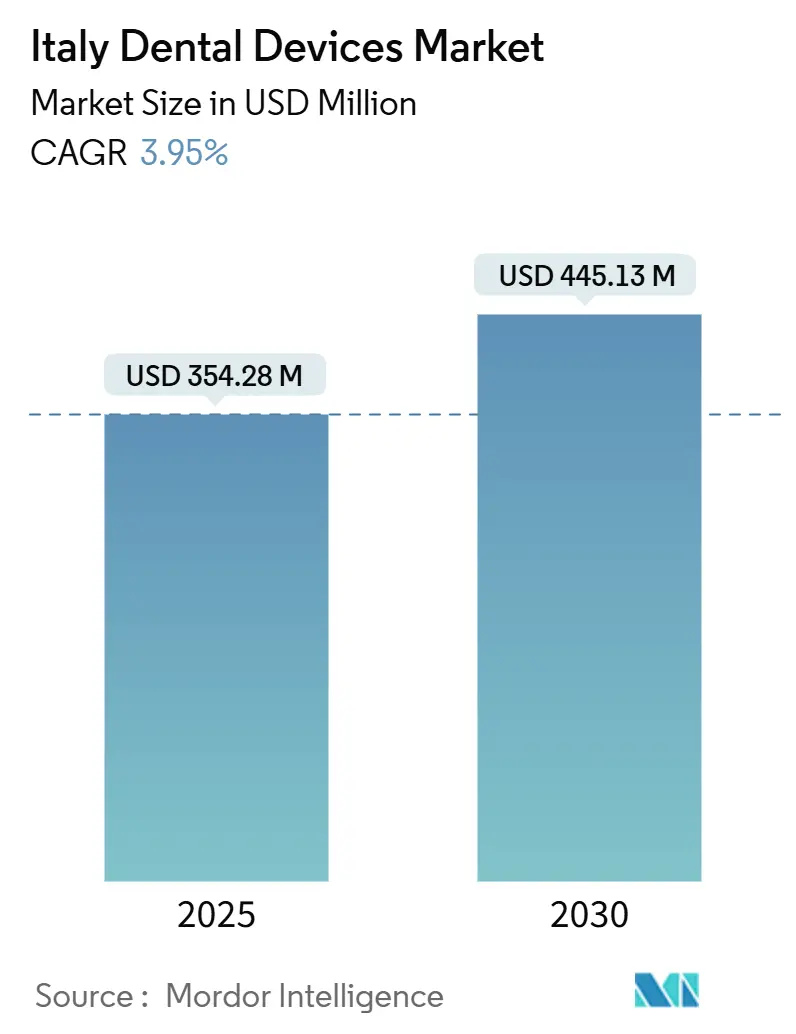

| Market Size (2025) | USD 354.28 Million |

| Market Size (2030) | USD 445.13 Million |

| Growth Rate (2025 - 2030) | 3.95% CAGR |

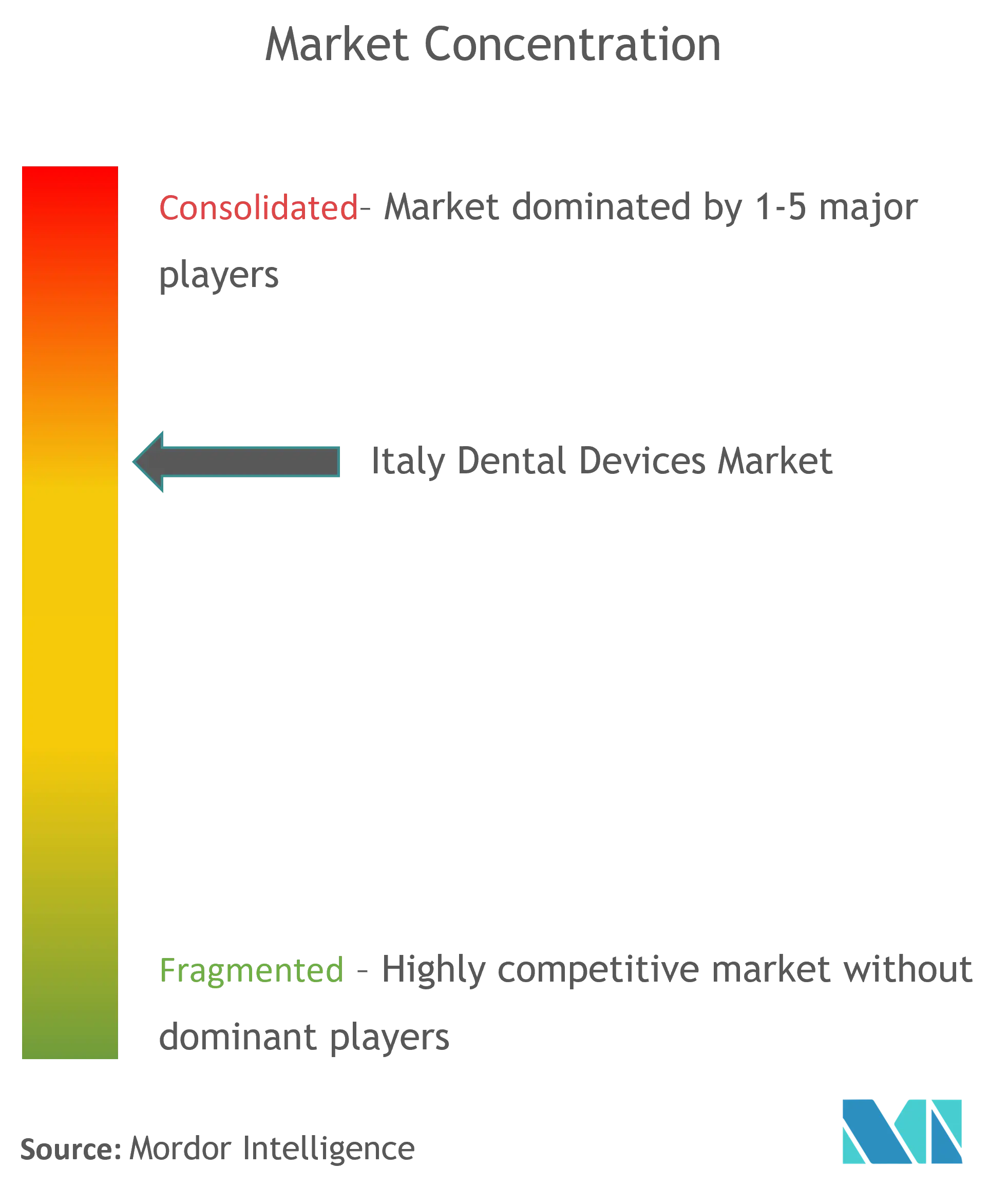

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Dental Devices Market Analysis by Mordor Intelligence

The Italian dental devices market size reached USD 354.28 million in 2024 and is forecast to climb to USD 445.13 million by 2030, expanding at a 3.95% CAGR between 2025-2030. Growth is underpinned by a rapidly ageing population, widening adoption of digital workflows and ongoing consolidation among distributors, yet moderated by persistent reimbursement gaps. Implant‐based restorative demand is surging as 24% of residents are already 65 years or older, while clear aligners, chair-side CAD/CAM and dental lasers are reshaping treatment protocols in clinics that can finance the necessary capital equipment. Competitive intensity is rising as global multinationals and niche Italian manufacturers race to embed AI, cloud connectivity and 3D printing into integrated ecosystems that lower per-procedure times and boost practitioner profitability. At the same time, the North–South income divide dictates starkly different purchasing power, compelling suppliers to tailor pricing models, training packages and financing options across regions.

Key Report Takeaways

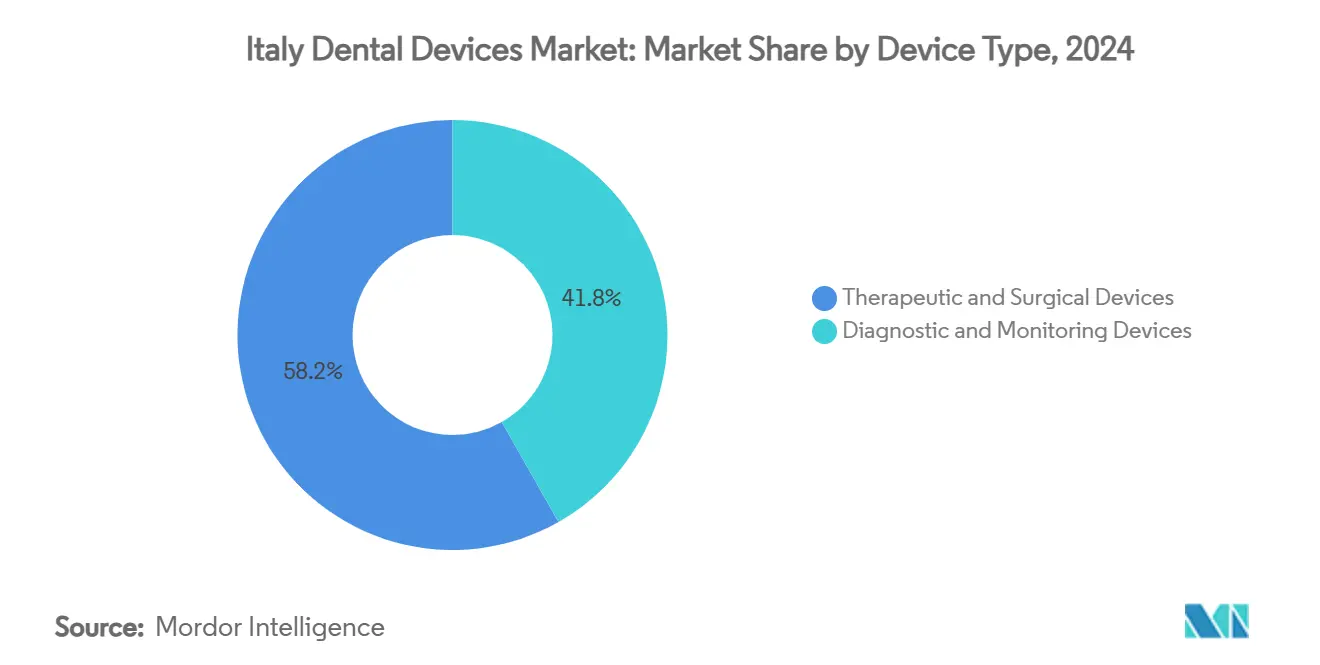

- By product, diagnostic devices commanded 39.50% of the Italian dental devices market share in 2024, while dental consumables are projected to expand at a 3.23% CAGR through 2030.

- By treatment, orthodontics led with 31.50% revenue share in 2024; periodontic procedures are expected to post the fastest 3.01% CAGR to 2030.

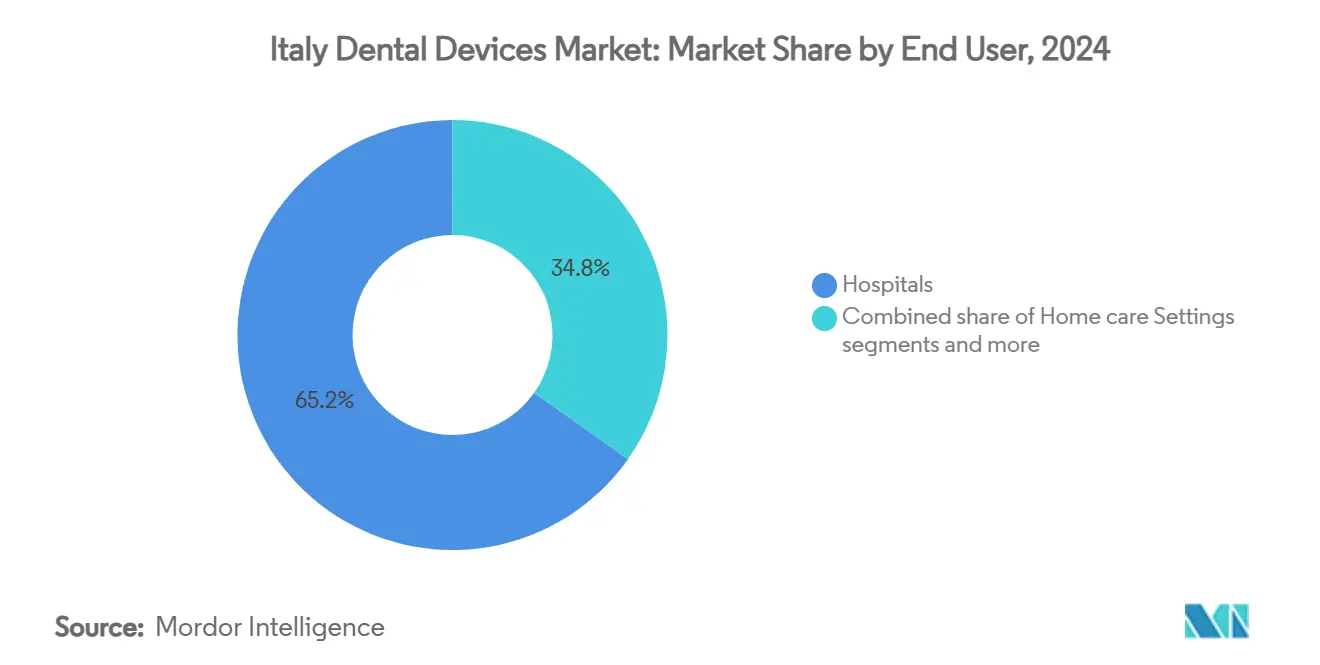

- By end user, clinics controlled 61.67% of the Italian dental devices market size in 2024, whereas academic & research institutes are forecast to grow at a 3.21% CAGR over 2025-2030.

Italy Dental Devices Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Implant Demand from Italy's ≥65-Year Cohort | +1.2% | National, with higher concentration in Northern regions | Medium term (2-4 years) |

| Chair-side CAD/CAM Uptake in Private Clinics | +0.8% | National, with early adoption in major urban centers | Medium term (2-4 years) |

| Dental Tourism Growth | +0.6% | Concentrated in major cities and tourist destinations | Long term (≥ 4 years) |

| Nationwide e-Health Record Integration of Dental Imaging | +0.4% | National, with initial implementation in Northern regions | Long term (≥ 4 years) |

| Italian Society–Led Adoption of Minimally-Invasive Lasers | +0.3% | National, with higher adoption in specialized clinics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid implant demand from Italy’s ≥65-year cohort

Italy’s age structure is reshaping the Italian dental devices market. With 24% of citizens now 65 years or older—and projections pointing to 37% by 2050—the volume of edentulous and partially edentulous patients is rising sharply[1]Source: Organisation for Economic Co-operation and Development, “Health at a Glance: Europe 2024,” oecd.org . Titanium implants still dominate owing to their 94.7% success rate in compromised bone, yet zirconia systems are the fastest-growing due to superior aesthetics and biocompatibility. Manufacturers are consequently engineering implant kits with shorter drilling sequences, antibacterial coatings and packaging that streamlines surgery in geriatric patients with systemic comorbidities. Affluent seniors show willingness to pay premium prices for fixed restorations that improve mastication and social interaction, encouraging clinics to invest in dedicated implantology suites and cone-beam CT scanners. The ripple effect extends to auxiliary consumables such as surgical guides produced on in-office 3D printers, further enlarging devices revenue pools.

Chair-side CAD/CAM uptake in private clinics

Digital impression systems have crossed the 60% adoption threshold in well-capitalised northern practices, cutting clinical chair-time by up to four hours and laboratory work by seven hours per case. The Italian dental devices market benefits as workflow efficiency lifts per-procedure profitability 15-20%, offsetting system prices that can exceed EUR 100,000. Cosmetic dentistry is the beachhead segment: same-day crowns and veneers reduce patient visits and amplify word-of-mouth referrals. Vendors differentiate through mill accuracy, AI-driven margin detection and cloud collaboration features that enable remote design by lab technicians. Bundled financing, subscription-based updates and certified training help dentists overcome the steep learning curve while guaranteeing manufacturers recurring revenue.

Dental tourism growth

Italy has cultivated a reputation for high clinical quality at prices lower than those in Northern Europe, creating a niche premium dental tourism segment. Exports of Italian dental solutions surpassed EUR 45 million and continue to climb, supported by devices showcases in the Italian pavilion at global trade fairs. Practices in Rome, Florence and coastal cities now integrate multilingual staff, digital scanners and chair-side milling to deliver complex rehabilitations within travellers’ tight itineraries. This trend fuels demand for portable X-ray units, rapid sintering furnaces and CBCT imaging suites that streamline diagnostics, surgical planning and same-day delivery. Regional authorities also view dental tourism as an economic booster, incentivising clinics to upgrade facilities in heritage cities where visitors combine treatment with culture.

Nationwide e-health record integration of dental imaging

Italy’s alignment with European e-Health strategies is pushing dental images into the central electronic health record. Compatible intraoral scanners, DICOM-native CBCT units and AI triage software are gaining traction, with early pilots demonstrating 27% higher caries detection accuracy and reduced diagnostic variability. Interoperability has shifted from a differentiator to a requirement in tenders issued by health regions. Digital-ready practices attract more referrals because general physicians and specialists can instantly review periodontal charts and implant plans. Manufacturers emphasise secure cloud platforms, HL7 interfaces and automated encryption to address GDPR obligations, thereby positioning their systems as future proof assets in the Italian dental devices market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement Issues for Oral Care | -0.9% | National, with greater impact in Southern regions | Long term (≥ 4 years) |

| Shortage of Digital-Dentistry Skilled Staff in South | -0.7% | Concentrated in Southern regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reimbursement issues for oral care

Only emergency and paediatric dental treatments enjoy meaningful SSN reimbursement, leaving 85% of adult expenditure funded out-of-pocket. This financing gap curbs equipment investment, particularly in communities where average income trails the EU mean. Patients defer non-urgent prosthodontic work, dampening demand for high-ticket lasers and CAD/CAM mills. Clinics in the South report 50% higher abandonment of treatment plans relative to their Northern peers, underscoring the direct link between reimbursement policy and technology uptake. Suppliers counter with leasing schemes and pay-per-use models, yet their success hinges on economic and political reforms that might only materialise over the long term.

Shortage of digital-dentistry skilled staff in South

Italy graduates merely 1.43 dentists per 100,000 inhabitants annually, insufficient to replace retiring practitioners[2]Source: Unione Nazionale Industrie Dentarie Italiane, “Italian Dental Export Statistics 2024,” unidi.it . Digital workflow expertise is concentrated in Lombardy, Veneto and Emilia-Romagna, while many southern clinics lack staff trained to operate CBCT systems or design CAD restorations. Even when southern practices purchase equipment through vendor promotions, utilisation rates can fall below 40%, impeding return on investment. Manufacturers increasingly bundle multi-day on-site coaching and remote support subscriptions, while academic centres fast-track continuing education programmes. Bridging this skills gap remains pivotal for unlocking unified growth across the Italian dental devices market.

Segment Analysis

By Product: Digital Technologies Reshape Equipment Landscape

Diagnostic devices captured 39.50% of 2024 revenue, yet dental consumables represent the fastest-expanding component at a 3.23% CAGR to 2030 as implant cylinders, biomaterials and clear-aligner foils gain prominence. Diagnostic imaging and laser devices are advancing in tandem, driven by practitioner demand for minimally invasive techniques that accelerate healing and improve aesthetics. The integration of 3D printers for surgical guides is blurring the boundary between equipment and consumables, creating hybrid revenue streams that reinforce vendor lock-in. Over the forecast period, AI-assisted cameras and augmented-reality microscopes are expected to widen the premium tier, sustaining steady replacement cycles.

In parallel, the Italian dental devices market size for CAD/CAM solutions is set to expand as chair-side units allow single-session restorations. Therapeutic lasers are positioned for mid-single-digit growth as periodontists adopt erbium and Nd:YAG wavelengths for non-surgical pocket decontamination. Vendors that pair hardware with cloud design services maximise recurring income and simplify workflow adoption for smaller clinics. Consumables will continue to outpace devices in percentage terms, yet hardware sales remain the primary engine for value creation as diagnostic accuracy and surgical precision assume centre stage in an ageing society.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Treatment: Aesthetic Demands Drive Procedural Evolution

Orthodontics held 31.50% of revenue in 2024, reflecting Italian consumer preference for subtle aesthetics and correct occlusion. Transparent thermoplastic aligners dominate incremental demand, enabling adult cases that conventional brackets deterred. Periodontic care is projected to record the briskest 3.01% CAGR, energised by laser adjunctive therapy and increasing scientific awareness of oral-systemic links. Consequently, the Italian dental devices market size for periodontal lasers and ultrasonic scalers will grow alongside guided-tissue regeneration membranes.

Implant-supported prosthodontics also drives devices and equioment upgrades, prompting acquisitions of torque-controlled physiodispensers and optical scanners capable of capturing edentulous arches. Endodontic treatments benefit from heat-treated NiTi files and adaptive motion motors that shorten chair time. Across segments, AI-backed treatment planning becomes pervasive, reinforcing diagnostic consistency and limiting retreatments. Clinics able to integrate imaging, design and manufacturing into seamless digital chains are positioned to capture higher case volumes at reduced per-procedure costs.

By End User: Clinics Dominate While Academic Centers Innovate

Dental clinics generated 61.67% of 2024 turnover, underlining their centrality in Italy’s private care model. Multi-operator studios and group practices proliferate, pooling resources for premium CBCT and milling units that single-owner offices find onerous. Academic and research institutes, while accounting for a smaller slice, will expand at a 3.21% CAGR as universities embed digital curricula and conduct clinical trials that validate next-gen workflows. These institutions often acquire flagship systems earlier, providing proof-points that propel broader market adoption.

Dental hospitals in major metropolitan areas prioritise high-throughput, network-enabled devices with built-in cybersecurity features. Mobile outreach units and tele-dentistry platforms also surface as supplementary channels, addressing rural access gaps. Together, these dynamics underscore that the Italian dental devices market share held by clinics will remain dominant even as academic centres and telehealth solutions accelerate their contributions to overall growth.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Northern regions—Lombardy, Veneto, Emilia-Romagna—command the highest device penetration, buoyed by elevated GDP per capita and dense networks of private practices. Clinics here routinely adopt intraoral scanners within 18 months of launch, whereas Southern counterparts can lag four years. Central Italy shows mixed metrics: Rome and Florence mirror northern adoption curves, but rural areas resemble the South. Dental tourism amplifies devices sales in heritage cities, where clinics configure chair-side milling and whitening lasers to serve international patients on tight schedules.

The Italian dental devices market size for implantology is greatest in the North, aligned with older demographics and greater disposable income. Conversely, the South presents untapped potential if financing and training hurdles are mitigated. E-health record integration pilots progressed fastest in Lombardy and Veneto, providing early revenue for AI-ready CBCT vendors. Regional funding schemes in Emilia-Romagna subsidise digital diagnostic devices for clinics meeting quality-of-care metrics. These incentives are absent in Sicily and Calabria, exacerbating the digital divide.

Workforce disparities compound devices adoption gaps. Dentists trained in Milan or Bologna frequently relocate northward, intensifying shortages in Apulia and Campania. Suppliers therefore tailor go-to-market models: turnkey solutions with embedded training and remote monitoring are emphasised in the South, while cutting-edge upgrades dominate northern campaigns. The interplay of income, demographics, infrastructure and policy will continue dictating region-specific growth trajectories within the broader Italian dental devices market.

Competitive Landscape

The market players are committed to developing innovative solutions for customers and patients, generating proven clinical outcomes. The competitive landscape includes an analysis of a few international as well as local companies that hold the market shares and are well known, including 3M, A-Dec Inc., Biolase Inc., Carestream Health Inc., Dentsply Sirona, and Envista Holdings Corporation, among others.

Italy Dental Devices Industry Leaders

-

3M Company

-

Carestream Health Inc.

-

GC Corporation

-

Dentsply Sirona

-

Envista Holdings (Nobel Biocare Services AG)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Ziacom Group expanded its European presence by acquiring two Italian dental companies, strengthening its implant and digital dentistry positions

- April 2024: DD Group acquired a leading Italian dental distributor, enhancing nationwide logistics

Italy Dental Devices Market Report Scope

As per the scope of the report, dental devices are tools used by dental professionals to provide dental treatment. It includes tools to examine, manipulate, treat, restore, and remove teeth and surrounding oral structures. Italy's dental devices market is segmented by Product (General and Diagnostics Equipment, Dental Consumables, and Other Dental Devices), By Treatment (Orthodontics, Endodontics, Periodontics, and Prosthodontics), and By End User (Hospitals, Clinics, and Other End Users). The report offers the value (in USD million) for the above segments.

By Product

| Diagnostics Devices | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | ||

| Radiology Equipment | Extra Oral Radiology Equipment | |

| Intra-oral Radiology Equipment | ||

| Dental Chair and Equipment | ||

| Therapeutic Devices | Dental Hand Pieces | |

| Electrosurgical Systems | ||

| CAD/CAM Systems | ||

| Milling Equipment | ||

| Casting Machine | ||

| Other Therapeutic Devices | ||

| Dental Consumables | Dental Biomaterial | |

| Dental Implants | ||

| Crowns and Bridges | ||

| Other Dental Consumables | ||

| Other Dental Devices | ||

By Treatment

| Orthodontic |

| Endodontic |

| Peridontic |

| Prosthodontic |

By End User

| Dental Hospitals |

| Dental Clinics |

| Academic & Research Institutes |

| By Product | Diagnostics Devices | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | |||

| Radiology Equipment | Extra Oral Radiology Equipment | ||

| Intra-oral Radiology Equipment | |||

| Dental Chair and Equipment | |||

| Therapeutic Devices | Dental Hand Pieces | ||

| Electrosurgical Systems | |||

| CAD/CAM Systems | |||

| Milling Equipment | |||

| Casting Machine | |||

| Other Therapeutic Devices | |||

| Dental Consumables | Dental Biomaterial | ||

| Dental Implants | |||

| Crowns and Bridges | |||

| Other Dental Consumables | |||

| Other Dental Devices | |||

| By Treatment | Orthodontic | ||

| Endodontic | |||

| Peridontic | |||

| Prosthodontic | |||

| By End User | Dental Hospitals | ||

| Dental Clinics | |||

| Academic & Research Institutes | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Italian dental devices market in 2025?

The Italian dental devices market size stands at about USD 367 million in 2025 and is set to grow steadily toward USD 445 million by 2030.

What is the main growth driver for Italian dental devices sales?

Surging implant demand from Italy’s rapidly ageing population adds roughly 1.2 percentage points to the forecast CAGR as seniors seek fixed restorative solutions.

Which product category is growing fastest?

Dental consumables—especially implant components, biomaterials and clear-aligner foils—are rising at a 3.23% CAGR, outpacing equipment but depending on digital systems for fabrication.

Why is equipment adoption higher in Northern Italy?

Higher disposable incomes, denser clinician networks and earlier digital-dentistry training push Northern regions ahead on CAD/CAM, laser and imaging penetration rates.

Page last updated on: