Market Size of Italy Commercial HVAC Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

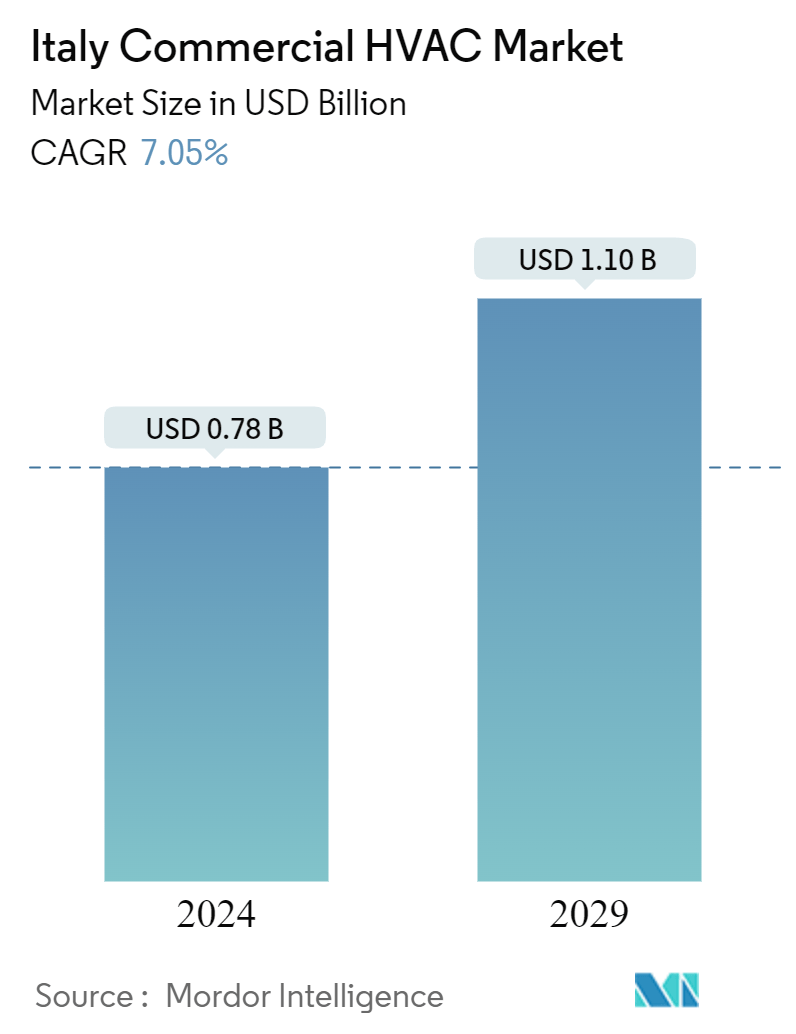

| Market Size (2024) | USD 0.78 Billion |

| Market Size (2029) | USD 1.10 Billion |

| CAGR (2024 - 2029) | 7.05 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Italy Commercial HVAC Market Analysis

The Italy Commercial HVAC Market size is estimated at USD 0.78 billion in 2024, and is expected to reach USD 1.10 billion by 2029, growing at a CAGR of 7.05% during the forecast period (2024-2029).

- The commercial sector in Italy is experiencing a notable rise in demand for HVAC equipment, driven largely by a growing preference for air conditioning systems and heat pumps. This trend results from several factors, including climate change, urbanization, changing lifestyles, and technological advancements. The market is benefiting from increased construction in commercial spaces, government backing for eco-friendly construction, and rapid urbanization. For instance, at the beginning of 2024, 72.1% of Italy's population resided in urban areas, with the remaining 27.9% in rural regions.

- Governments are looking forward to introducing stringent regulations, thus mandating the incorporation of heat pumps and a ban on boilers. Such initiatives are driving the market’s growth. For instance, the EU is gearing up to enforce a ban on gas boilers starting in 2029, aligned with the Green Homes Directive. This directive is part of the proposed amendments to the Ecodesign Regulation 813/2013/EU, which delineates the standards for designing and marketing space heating appliances.

- Across several regions in Italy, the demand for cooling surpasses that for heating. As a result, the prevalent choice for heating and cooling solutions is the reversible air-to-air heat pump. While primarily employed for cooling purposes, these systems also effectively meet heating requirements during the colder months, covering a significant portion of the nation.

- Key market players are focusing on new product launches to meet consumer demand. For instance, in March 2024, LG Electronics unveiled its latest residential air conditioner, the DUALCOOL, at MCE 2024 in Milan, Italy. MCE 2024 stands as one of Europe's premier HVAC exhibitions. Running from March 12-15, the event showcased LG's cutting-edge air conditioning innovations, notably highlighting the Soft Air™ feature, designed to elevate indoor comfort throughout the year.

- The construction industry is vital to the Italian economy, employing over three million people and contributing more than EUR 110 billion (USD 119.73 billion) to the country's GDP. The growing construction of commercial buildings and the presence of many commercial buildings in Italy drive demand for HVAC systems to reduce carbon footprint and CO2 emission.

- For instance, in 2023, the Southern region of Italy boasted the largest stock of commercial buildings, with approximately 2.6 million units. The North-West and Central regions followed closely, with around 2.5 million and 2 million commercial units, respectively. This commercial real estate encompasses a variety of non-residential structures, including retail spaces, labs, credit institutions, warehouses, hotels, public offices, and agricultural units.

- The competitive rivalry in the Italian commercial HVAC market studied is high due to its many established vendors. Global manufacturers are focusing on energy efficiency as one of their key concerns. Many players, such as Daikin, Carrier, Robert Bosch Gmbh, Danfoss AS, Mitsubishi Electric Europe BV, and Lennox International Inc., have already started launching energy-efficient HVAC products. Hence, they have become price setters in the market. Thus, comparatively smaller players lack the financial capacity to match the level of technological innovations incorporated in these products and must sell their products at a lower price point.

- The ongoing Russia and Ukraine War has led to political and economic turbulence, diminishing consumer purchasing power in the region. Russia's invasion of Ukraine has significantly impacted the energy sector in many EU countries, including Italy. According to the European Commission, the decline in energy prices in Italy is expected to reduce inflation to 1.6% in 2024, with a slight increase to 1.9% anticipated in 2025. Despite the recovery in real disposable incomes, households are expected to increase their savings, leveraging higher interest rates. These factors are projected to hamper the market’s growth for a short period of time in the country.

Italy Commercial HVAC Industry Segmentation

Heating, ventilation, and air conditioning (HVAC) regulate the temperature, humidity, and air purity of enclosed spaces. HVAC systems aim to ensure thermal comfort and acceptable indoor air quality.

The study tracks the revenue accrued through various players' sales of HVAC equipment to Italy's commercial end users. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates during the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report's scope encompasses market sizing and forecasts for the various market segments.

The Italian commercial HVAC market is segmented by type of component (HVAC equipment (heating equipment, air conditioning /ventilation equipment), HVAC services) and end-user industry (hospitality, commercial buildings, public buildings, and other end-user industries). The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| By Type of Component | ||||

| ||||

| HVAC Services |

| By End-user Industry | |

| Hospitality | |

| Commercial Buildings | |

| Public Buildings | |

| Other End-user Industries |

Italy Commercial HVAC Market Size Summary

The Italian commercial HVAC market is poised for significant growth, driven by increasing demand for energy-efficient heating, ventilation, and air conditioning systems. This demand is largely fueled by urbanization, climate change, and technological advancements, which have led to a preference for air conditioning systems and heat pumps. The market is further bolstered by government initiatives promoting eco-friendly construction and stringent regulations mandating the use of heat pumps while phasing out traditional boilers. The construction of commercial buildings, particularly in urban areas, is a key factor contributing to the market's expansion, as these structures require advanced HVAC systems to meet modern energy efficiency standards and reduce carbon emissions.

The competitive landscape of the Italian commercial HVAC market is characterized by the presence of several established global players, such as Daikin, Mitsubishi Electric, and Robert Bosch GmbH, who are focusing on innovation and energy efficiency to maintain their market positions. These companies are actively launching new products and technologies to cater to the growing demand for sustainable HVAC solutions. The market is also witnessing a rise in the popularity of ductless mini-split air conditioners, which offer flexible and efficient heating and cooling solutions for large buildings and small spaces alike. Despite challenges posed by geopolitical tensions and economic fluctuations, the market is expected to continue its upward trajectory, supported by ongoing investments in commercial real estate and the adoption of advanced HVAC technologies.

Italy Commercial HVAC Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Consumers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitute Products

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Industry Value Chain Analysis

-

1.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Type of Component

-

2.1.1 HVAC Equipment

-

2.1.1.1 Heating Equipment

-

2.1.1.2 Air Conditioning /Ventillation Equipment

-

-

2.1.2 HVAC Services

-

-

2.2 By End-user Industry

-

2.2.1 Hospitality

-

2.2.2 Commercial Buildings

-

2.2.3 Public Buildings

-

2.2.4 Other End-user Industries

-

-

Italy Commercial HVAC Market Size FAQs

How big is the Italy Commercial HVAC Market?

The Italy Commercial HVAC Market size is expected to reach USD 0.78 billion in 2024 and grow at a CAGR of 7.05% to reach USD 1.10 billion by 2029.

What is the current Italy Commercial HVAC Market size?

In 2024, the Italy Commercial HVAC Market size is expected to reach USD 0.78 billion.