Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

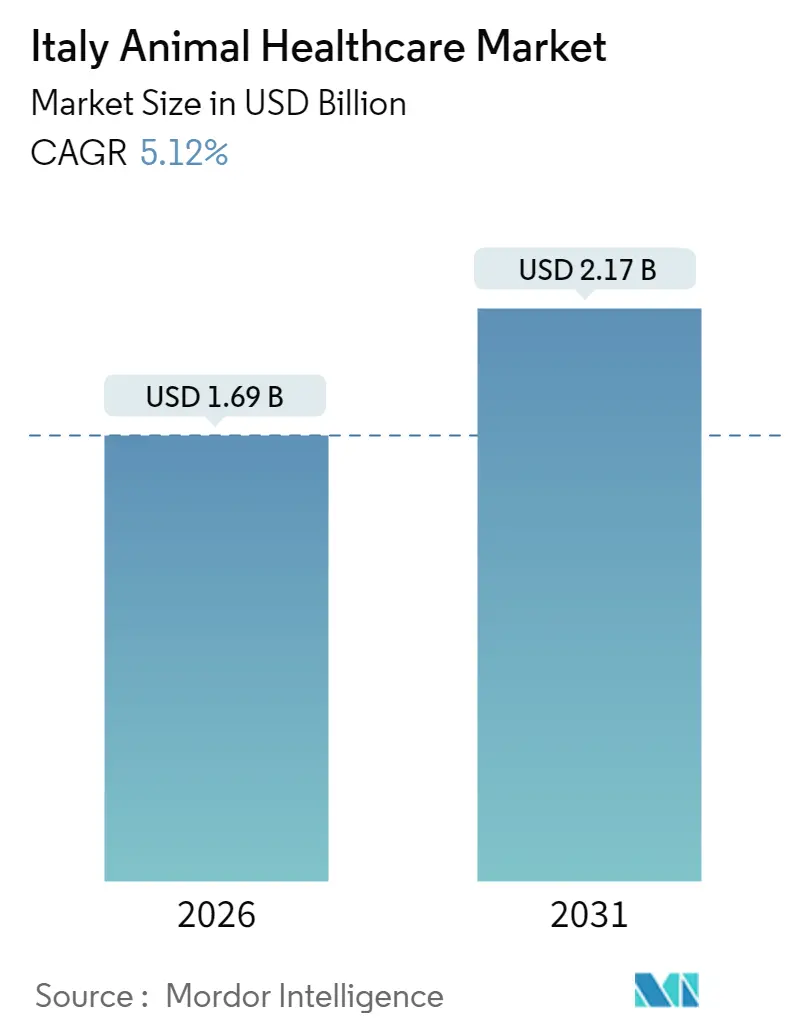

| Market Size (2026) | USD 1.69 Billion |

| Market Size (2031) | USD 2.17 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

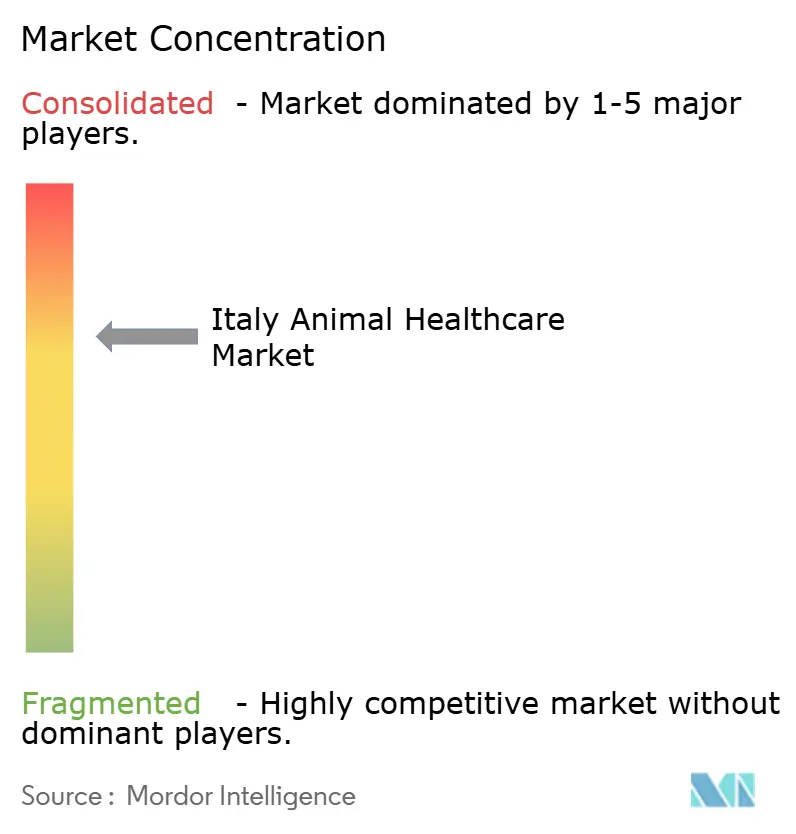

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Animal Healthcare Market Analysis by Mordor Intelligence

Italy animal healthcare market size in 2026 is estimated at USD 1.69 billion, growing from 2025 value of USD 1.61 billion with 2031 projections showing USD 2.17 billion, growing at 5.12% CAGR over 2026-2031. Growth is fuelled by rising ownership of companion animals. Italian households host 60.2 million pets, accompanied by a steady increase in preventive-care spending and a policy environment that explicitly links animal health to public health outcomes. Therapeutics remain the most significant revenue contributor, but diagnostics are scaling faster, driven by molecular assays and point-of-care innovations. Corporate networks are expanding their footprint, and the influx of capital is driving technology upgrades that help practices comply with the Ministry of Health’s antimicrobial stewardship mandate. The Italy animal healthcare market also benefits from European Union traceability rules that mandate more frequent livestock testing, thereby broadening the revenue base for laboratories. Counterbalancing these tailwinds are the profession’s manpower gaps and the high cost of advanced therapies, both of which could temper near-term access gains. Nevertheless, strong demand elasticity, combined with incentives embedded in the One Health framework, underpins a resilient outlook for the Italy animal healthcare market through 2030.

Key Report Takeaways

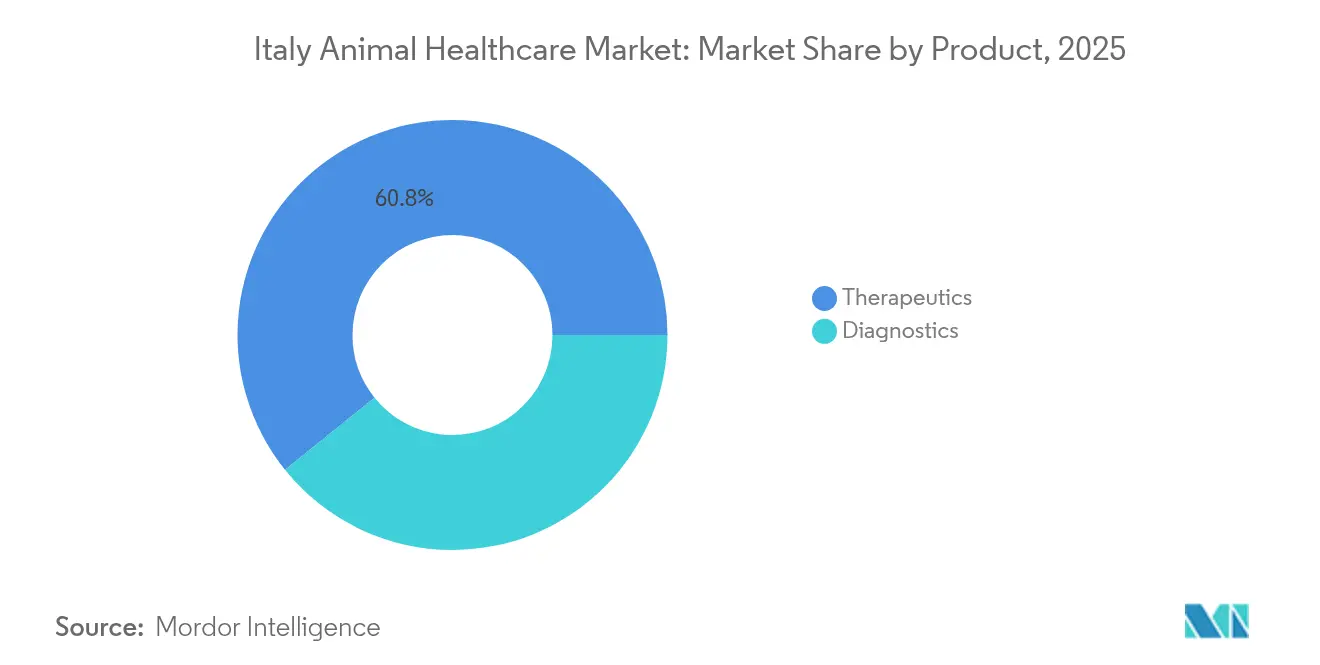

- By product type, therapeutics led with 60.78% revenue share in 2025, while diagnostics are projected to grow at a 7.29% CAGR to 2031.

- By animal type, dogs & cats accounted for 47.88% of the Italy animal healthcare market size in 2025, whereas the poultry segment is forecast to expand at a 6.17% CAGR between 2026 and 2031.

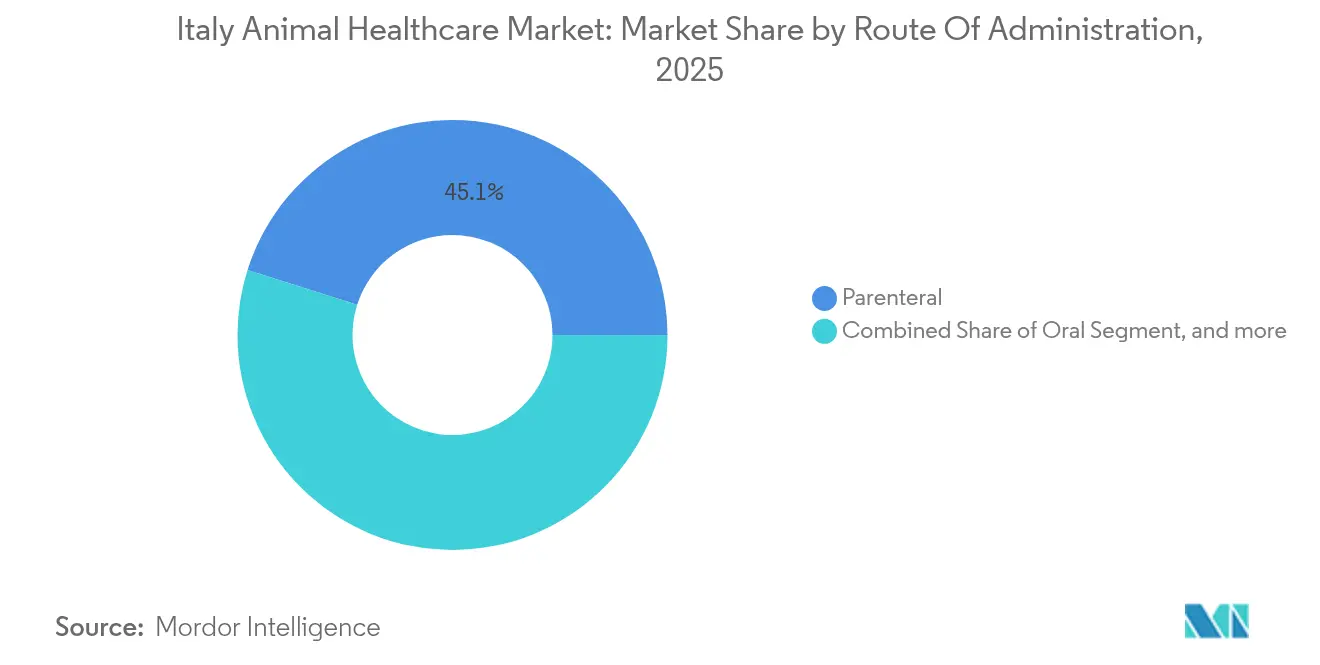

- By route of administration, parenteral products held 45.12% of the Italy animal healthcare market share in 2025; however, oral formulations are advancing at a 7.44% CAGR through 2031.

- By end user, veterinary hospitals & clinics captured 55.21% revenue share in 2025, while point-of-care settings are set to log a 6.31% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Animal Healthcare Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prescription volume and medication throughput | +1.5% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Expanding geriatric population and chronic-disease burden | +1.2% | Global; high-income, rapidly aging regions | Long term (≥4 years) |

| Heightened patient-safety and error-reduction mandates | +1.0% | Global, led by OECD members | Short term (≤2 years) |

| Shift toward centralized fill and hub pharmacies | +0.8% | North America and Western Europe | Medium term (2-4 years) |

| Integration of artificial intelligence for inventory optimization | +0.7% | Global; early adoption in tech-advanced health systems | Long term (≥4 years) |

| Surge in specialty-drug dispensing complexity | +0.6% | Global; oncology and rare-disease markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Expansion of Companion-Animal Population and Humanization Trends

Italy’s pet-care economy is expanding alongside a cultural shift that treats animals as family members. Sixty-three percent of owners consider pet health equal to human health and allocate around EUR 1,000 annually to pet upkeep, of which veterinary visits form a growing slice[1]RAI News, “Gli italiani e gli animali da compagnia,” rai.it. The constitutional amendment recognizing animals as sentient beings further legitimizes premium services such as oncology and advanced imaging. Pet-food expenditure rose to EUR 2.53 billion in 2024, reinforcing a willingness to pay for broader wellness packages. Demographically, northern regions possess higher disposable incomes, which translates into more frequent clinic visits and earlier adoption of telehealth. Urban millennials also favor subscription-based wellness plans that bundle vaccinations, diagnostics, and nutritional counseling. Collectively, these factors increase the average revenue per visit and underpin volume growth across both therapeutics and diagnostics in the Italy animal healthcare market.

Rising Expenditure on Preventive Veterinary Care and Insurance Uptake

Preventive care now commands a larger share of wallet as owners appreciate the cost-avoidance value of early intervention. About 32% of households purchase supplements and wellness products, and routine screening packages are becoming standard at corporate clinics. Although pet-insurance penetration lags northern Europe, policy count grew in double digits during 2024–2025, signaling latent demand. Insurers have begun partnering with multi-clinic networks to bundle coverage with annual check-ups, thereby embedding diagnostics and vaccinations into recurring revenue streams. Livestock operators are likewise investing in herd-health plans that emphasize biosecurity and vaccination compliance in response to EU disease-surveillance rules[2]European Commission, “National Control Plan 2023–2027,” europa.eu. These structural moves collectively push the Italy animal healthcare market toward a more preventative model, reducing seasonality and stabilizing cash flows for service providers.

Government Incentives and Favorable Animal-Welfare Regulations

The Ministry of Health’s 2025 directive calls for nationwide antimicrobial-resistance monitoring and reinforces the One Health principle that ties animal and human well-being[3]Ministero della Salute, “Piano Nazionale Antimicrobico 2025,” salute.gov.it. Complementary policies include a dedicated fund that offsets veterinary expenses for low-income families and VAT-relief proposals on critical animal-health products, both of which aim to widen access. The National Control Plan 2023–2027 mandates 15,007 full-time-equivalent staff for food-safety and veterinary inspections, increasing demand for laboratory diagnostics. University reforms that scrap entrance exams for veterinary medicine, effective in the 2025/2026 academic year, seek to ease the professional shortfall and improve rural service coverage. Collectively, these interventions reinforce structural demand and enhance the regulatory predictability crucial for investment in the Italy animal healthcare market.

Technological Advancements in Veterinary Pharmaceuticals and Diagnostics

Electronic prescription systems reduced antimicrobial scripts at the Naples University Veterinary Teaching Hospital from 41.6% to 36%, demonstrating technology’s regulatory utility. Liquid-biopsy protocols now achieve 85.7% diagnostic accuracy in canine oncology, expanding the addressable market for molecular tests. Business-intelligence platforms at Istituto Zooprofilattico Sperimentale delle Venezie standardize lab protocols and offer real-time disease-trend dashboards, enhancing biosecurity. Precision-livestock tools—wearables, GPS, and virtual fencing—help shepherds in hilly Sardinia monitor herd health, albeit adoption is slowed by cost and connectivity gaps. IDEXX Laboratories supports capability building by providing 90,000 continuing-education credits annually and rolling out the Cystatin-B renal test in 2024. Technology therefore boosts diagnostic throughput, operational efficiency, and clinical accuracy across the Italy animal healthcare market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital investment and maintenance costs | –1.0% | Global; most acute in emerging markets | Short term (≤2 years) |

| Workflow disruption and staff-training barriers | –0.7% | Global; facilities with limited change-management resources | Medium term (2-4 years) |

| Data security and privacy concerns in connected systems | –0.6% | Global; strictest in EU and North America | Long term (≥4 years) |

| Regulatory ambiguity for robotic sterile compounding | –0.4% | North America and select EU states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortfall of Veterinary Professionals and Rural Service Gaps

Veterinary headcount has not kept pace with demand; 78.5% of European countries report shortages, and Italy is no exception. Income disparity versus human-medical peers discourages graduates from livestock practice, while 76% of new veterinarians are women who often prefer urban clinics offering better work-life balance. Rural posts struggle with limited infrastructure and lower earnings, hindering disease surveillance in regions crucial to meat and dairy supply chains. The manpower gap compromises outbreak readiness, evidenced in slower response to the 2025 lumpy-skin-disease episode. The university-reform initiative may widen the talent pipeline, yet longer-term retention in underserved areas will require fiscal incentives and telemedicine support to narrow geographic disparities within the Italy animal healthcare market.

Escalating Costs of Veterinary Treatments and Pharmaceuticals

Average pet-care spending reached EUR 1,000 per animal in 2024, straining budgets of middle-income households. Veterinary antibiotic consumption rose 6.3%, compounding costs tied to antimicrobial resistance and making Italy Europe’s costliest jurisdiction for resistance-linked treatments. Specialized biologics and oncology drugs command premium prices, and mandatory investments in e-prescription platforms, imaging suites, and biosafety upgrades heighten overhead for clinics. Livestock producers face similar headwinds as feed additives and vaccines become pricier under tighter EU compliance standards. While corporate chains can leverage scale to negotiate better procurement terms, independent clinics may pass through costs, potentially suppressing volume growth in price-sensitive pockets of the Italy animal healthcare market.

Segment Analysis

By Product: Therapeutics Leadership Amid Diagnostic Innovation

Therapeutics generated 60.78% of the Italy animal healthcare market size in 2025, reflecting entrenched treatment protocols and reliable reimbursement from livestock operators. Vaccines form the blockbuster subcategory, buoyed by mandatory poultry and bovine immunization programs that mitigate epidemic-scale losses during avian-influenza and lumpy-skin-disease events. Parasiticides enjoy year-round demand given Italy’s Mediterranean climate that favors vector proliferation. Anti-infectives remain sizable but face regulatory scrutiny; veterinary antibiotic sales fell 12.7% to 585.4 tonnes in 2022 as stewardship programs intensified. Market attention is shifting to medical-feed additives, nutraceuticals, and targeted biologics that align with zero-antibiotic-residue labels favored by retailers.

Diagnostics, although a smaller base, are posting a 7.29% CAGR through 2031. Immunodiagnostic assays dominate routine screenings, while molecular platforms accelerate in oncology and genetic-disease panels. Diagnostic imaging sales benefit from corporate-clinic refurbishments in affluent northern cities, where computed tomography and digital radiography are becoming standard. Liquid-biopsy services, with 85.7% sensitivity in canine cancer, are opening adjacent demand for confirmatory molecular tests. Collectively, rapid diagnostic expansion adds a recurring-testing dimension that enhances stickiness of the Italy animal healthcare market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Animal Type: Companion Animals Drive Growth Despite Livestock Challenges

Dogs & cats represented 47.88% of 2025 revenue, supported by 19 million pets and high per-capita spend on wellness plans. Younger owners tend to gravitate toward minimally invasive therapies, driving the uptake of monoclonal antibodies for osteoarthritis and oral JAK inhibitors for dermatitis. Preventive dental care and weight-management programs add ancillary service revenue, deepening clinic-client engagement.

The poultry segment, advancing at a 6.17% CAGR, reflects Italy’s 1.3 million-tonne broiler output in 2024, a 10% increase that triggers expanded vaccine schedules. Stringent EU trade rules require disease-free certification, boosting lab testing volumes. The disease shock of 602,200 birds culled in the January 2025 avian influenza wave accelerates biosecurity investments. Swine, ruminants, and horses remain important, but their growth rates are steadier, influenced by commodity prices and targeted sports-medicine demand. Niche pockets such as aquaculture and exotic pets are nascent yet underscore the widening scope of the Italy animal healthcare market.

By Route of Administration: Oral Delivery Innovation Challenges Parenteral Dominance

Parenteral formulations accounted for 45.12% of the Italy animal healthcare market share in 2025 due to the clinical preference for injectables in acute care and mass-vaccination campaigns. Yet oral products are scaling at a 7.44% CAGR as companies improve palatability and controlled-release profiles. Elanco’s Zenrelia, approved in August 2025 for canine allergic dermatitis, epitomizes this pivot toward once-daily oral convenience.

Oral delivery also benefits from the e-prescription system that simplifies refill logistics and aligns with antimicrobial-stewardship dashboards. Topicals hold steady for dermatological and ectoparasite indications, supported by Italy’s warm climate. Other routes—transdermal patches, implants, and inhalables—are niche but growing in oncology and chronic-pain management. As owner adherence increasingly determines therapeutic success, administration-route innovation remains a differentiator in the Italy animal healthcare market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Hospital Consolidation Accelerates Amid Point-of-Care Innovation

Veterinary hospitals & clinics captured 55.21% of 2025 revenue, buoyed by chain formation and private-equity backing. Charme Capital Partners’ investment in Animalia, which operates 75 clinics across 13 regions, typifies consolidation that yields procurement scale and standardized protocols. Corporate players leverage data analytics to fine-tune service mix, integrate pharmacies, and cross-sell preventive plans, further solidifying their lead.

Point-of-care (POC) settings are advancing at a 6.31% CAGR as handheld analyzers, portable ultrasound, and cloud-based image archives shrink the turnaround time from diagnosis to treatment. Reference laboratories play a vital role in complex molecular tests and regulatory monitoring, with regional institutes ramping up their capacity to meet National Control Plan staffing targets. Academic & research centers diversify revenue through contract research and continuing-education programs, partly subsidized by diagnostics firms. Together, these end-user dynamics shape a multi-tier service ecosystem that broadens access and elevates clinical depth within the Italian animal healthcare market.

Competitive Landscape

The Italy animal healthcare market exhibits moderate concentration but growing consolidation. Multinationals such as Zoetis reported 4% Italian revenue growth to USD 29 million in Q1 2025, buoyed by demand for monoclonal antibodies and poultry vaccines. Domestic champions like Animalia leverage private-equity capital to expand regional footprints, standardize electronic health records, and negotiate favorable drug procurement contracts. IVC Evidensia, operating more than 2,500 European sites, channels cross-border know-how into Italian clinics, deepening competitive intensity.

Technology leadership has become a decisive factor. Chains rolling out electronic-prescription modules gain regulatory-compliance advantages and capture prescribing data that informs formulary choices. Laboratories that integrate liquid-biopsy and next-generation sequencing differentiate themselves in the oncology niche. Start-ups exploit white spaces in rural telemedicine and AI-enabled imaging triage, although reimbursement models remain nascent.

Strategic alliances across the value chain are rising. Elanco teamed with Medgene in February 2025 to commercialize an H5N1 cattle vaccine, potentially positioning firms for future livestock biosecurity mandates. On the CDMO front, the merger of Doppel Farmaceutici and Mipharm created DMX Pharma, enhancing local manufacturing capacity pivotal for supply-chain resilience. These moves collectively elevate entry barriers and reshape competitive contours in the Italy animal healthcare market.

Italy Animal Healthcare Industry Leaders

Elanco Animal Health

MSD Animal Health (Merck & Co.)

Virbac

Zoetis Inc.

Boehringer Ingelheim Animal Health

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Elanco Animal Health received European Commission approval for Zenrelia (ilunocitinib), a once-daily oral JAK inhibitor for canine allergic dermatitis, with an EU launch slated for Q3 2025.

- July 2025: Charme Capital Partners finalized an investment in Animalia, Italy’s largest veterinary-clinic group, to fund national roll-out and digital-platform upgrades.

- June 2025: Italy’s Ministry of University and Research enacted an “open semester” model that removes entrance exams for veterinary programs to mitigate workforce shortages.

- February 2025: Trilantic Europe and Alto Partners merged Doppel Farmaceutici with Mipharm, forming DMX Pharma, a CDMO projected to hit EUR 180 million turnover.

Italy Animal Healthcare Market Report Scope

Animal healthcare can be specified as the science associated with the diagnosis, treatment, and prevention of diseases in animals. Companion animals are animals that can be tamed or adopted for companionship or as house/office guards and farm animals are animals raised for meat- and milk-related products.

The Italy animal healthcare market is segmented by product and animal type. By product, the market is segmented into therapeutics and diagnostics. By animal type, the market is segmented into dogs and cats, horses, ruminants, swine, poultry, and other animals. The report offers value (in USD) for the above segments.

By Product

| Therapeutics | Vaccines |

| Parasiticides | |

| Anti-Infectives | |

| Medical Feed Additives | |

| Other Therapeutics | |

| Diagnostics | Immunodiagnostic Tests |

| Molecular Diagnostics | |

| Diagnostic Imaging | |

| Clinical Chemistry | |

| Other Diagnostics |

By Animal Type

| Dogs & Cats |

| Horses |

| Ruminants |

| Swine |

| Poultry |

| Other Animal Types |

By Route Of Administration

| Oral |

| Parenteral |

| Topical |

| Other Route of Administrations |

By End User

| Veterinary Hospitals & Clinics |

| Reference Laboratories |

| Point-Of-Care / In-House Testing Settings |

| Academic & Research Institutes |

| By Product | Therapeutics | Vaccines |

| Parasiticides | ||

| Anti-Infectives | ||

| Medical Feed Additives | ||

| Other Therapeutics | ||

| Diagnostics | Immunodiagnostic Tests | |

| Molecular Diagnostics | ||

| Diagnostic Imaging | ||

| Clinical Chemistry | ||

| Other Diagnostics | ||

| By Animal Type | Dogs & Cats | |

| Horses | ||

| Ruminants | ||

| Swine | ||

| Poultry | ||

| Other Animal Types | ||

| By Route Of Administration | Oral | |

| Parenteral | ||

| Topical | ||

| Other Route of Administrations | ||

| By End User | Veterinary Hospitals & Clinics | |

| Reference Laboratories | ||

| Point-Of-Care / In-House Testing Settings | ||

| Academic & Research Institutes | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the Italy animal healthcare market in 2031?

The market is forecast to reach USD 2.17 billion by 2031, supported by a 5.12% CAGR.

Which product category currently dominates spending?

Therapeutics lead with 60.78% revenue share, driven by vaccines and parasiticides.

Why are diagnostics expanding faster than therapeutics?

Molecular assays, liquid-biopsy techniques, and point-of-care devices are shortening turnaround times and improving clinical outcomes, fueling a 7.29% CAGR for diagnostics.

Which animal segment is growing the quickest?

Poultry is advancing at a 6.17% CAGR as producers scale biosecurity and vaccination programs.

How is government policy influencing market demand?

The Ministry of HealthÕs One Health directive and antimicrobial-stewardship rules mandate greater surveillance and incentivize preventive care, expanding diagnostic and treatment volumes.

What challenges could restrict future growth?

Veterinary-workforce shortages, especially in rural areas, and rising therapy costs could limit access and slow adoption of advanced services.