Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

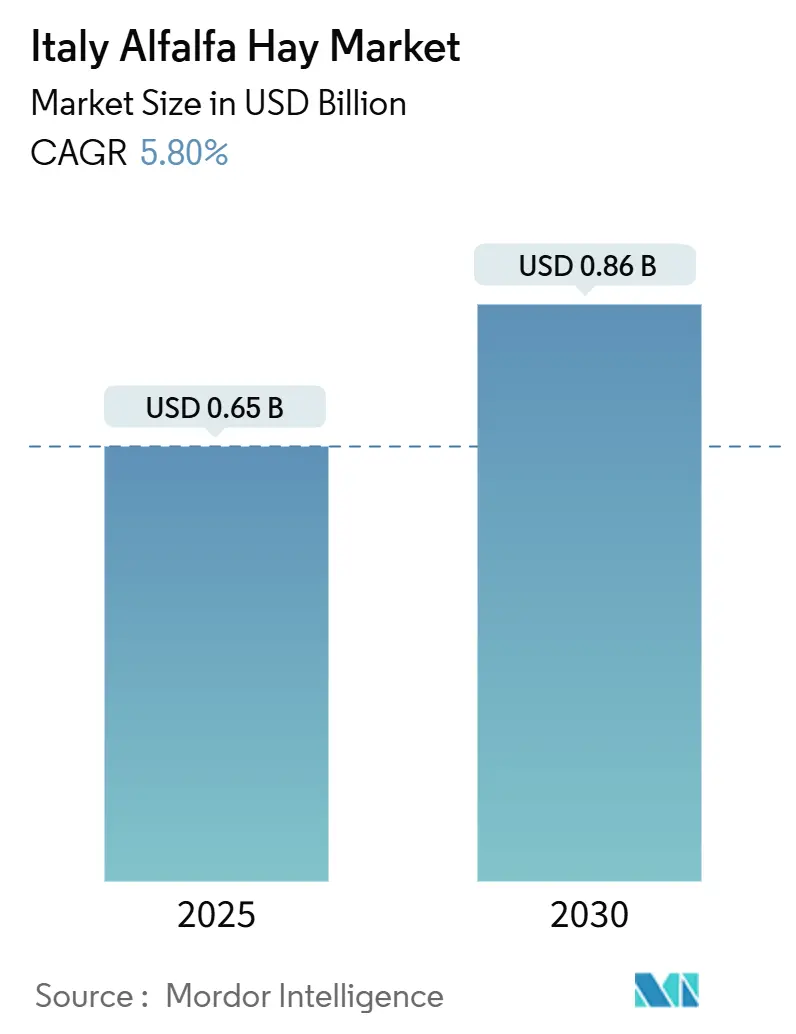

| Market Size (2025) | USD 0.65 Billion |

| Market Size (2030) | USD 0.86 Billion |

| Growth Rate (2025 - 2030) | 5.80% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Alfalfa Hay Market Analysis by Mordor Intelligence

The Italy alfalfa hay market size is estimated at USD 0.65 billion in 2025 and is projected to reach USD 0.86 billion by 2030, growing at a CAGR of 5.8% from 2025 to 2030. The rising demand for premium Protected Designation of Origin (PDO) dairy products, carbon-farming incentives within the Common Agricultural Policy, and stricter feed sourcing rules for organic certification are key drivers of this expansion. The Italy alfalfa hay market also benefits from dairy processors’ need to protect Protected Designation of Origin (PDO) status during volatile commodity cycles, while policy-backed nitrogen credits improve growers’ profit margins. Investments in pelleting capacity and precision irrigation lower the cost per unit protein, which keeps locally produced forage competitive against imported protein meals. Headline risks include drought-driven yield swings, logistics inflation, and nascent competition from hydroponic fodder. Yet, the Italy alfalfa hay market retains structural resilience because cheese-making rules lock in forage demand.

Key Report Takeaways

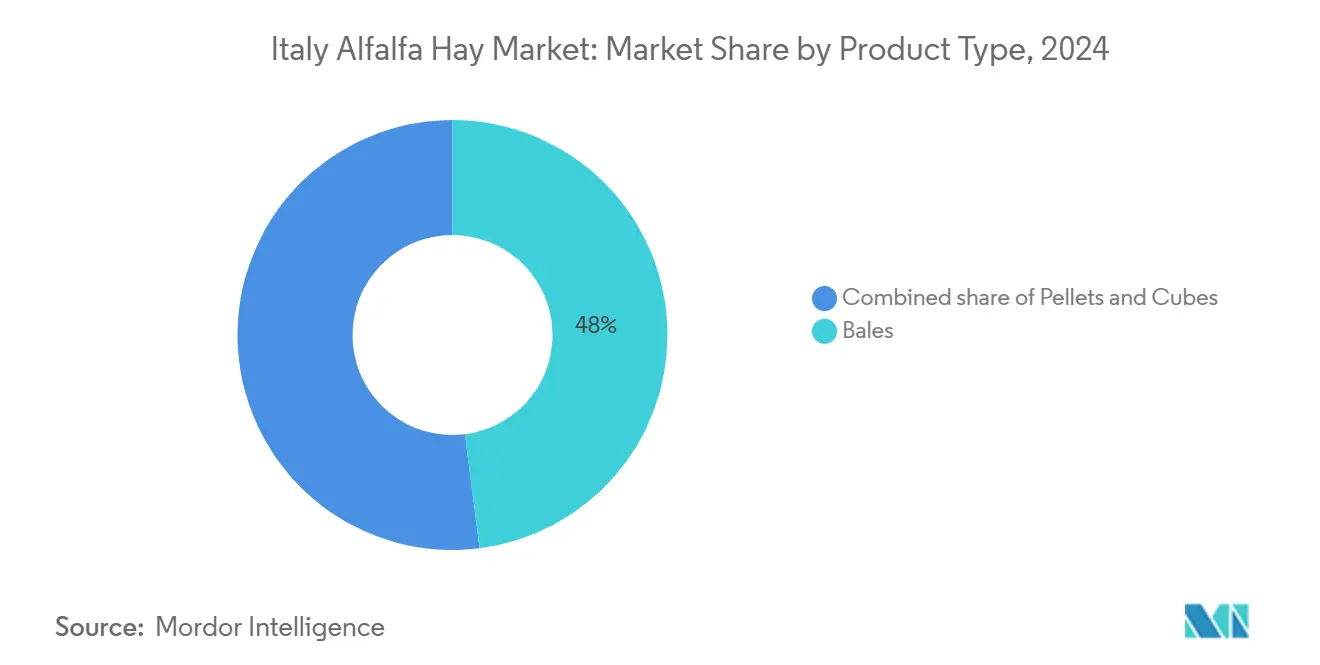

- By product type, bales led with 48% of the Italy alfalfa hay market share in 2024, while pellets are projected to expand at an 8.2% CAGR through 2030.

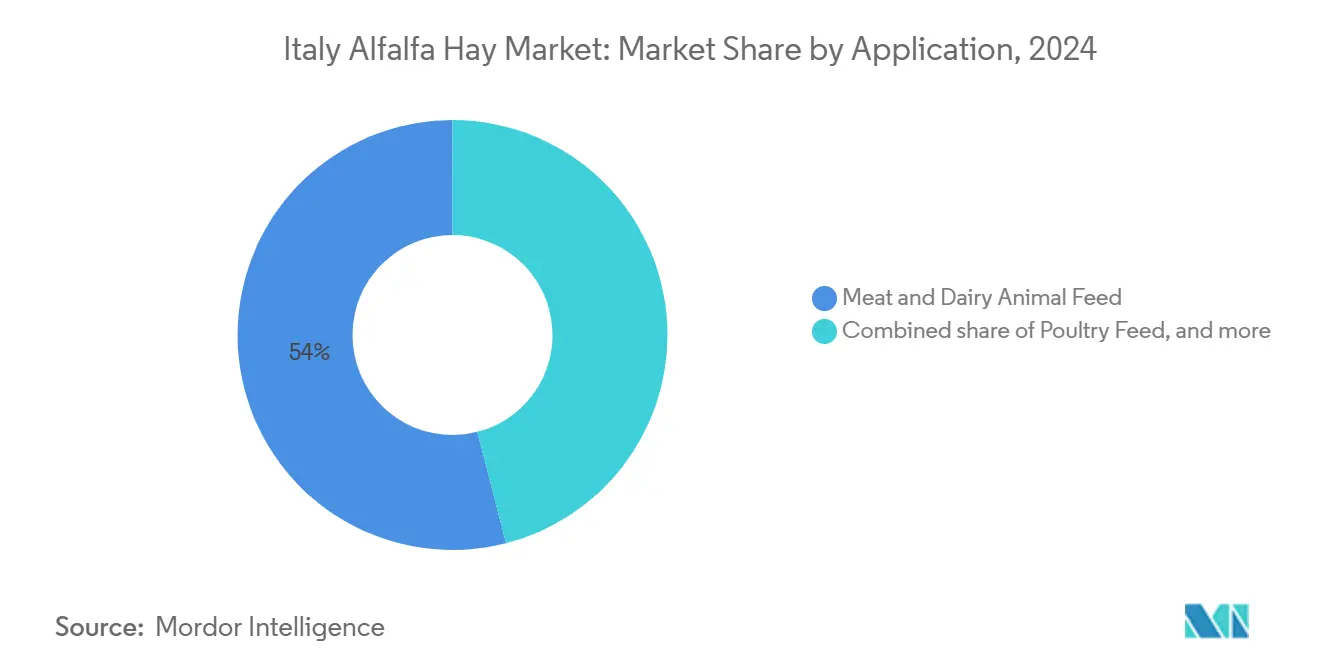

- By application, meat and dairy animal feed captured 54% revenue share of the Italy alfalfa hay market size in 2024, while poultry feed is projected to advance at a 9% CAGR through 2030.

Italy Alfalfa Hay Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for premium meat and dairy products | +1.2% | Lombardy, Emilia-Romagna, Veneto Protected Designation of Origin (PDO) zones | Medium term (2-4 years) |

| Growth in livestock and poultry herd size | +0.9% | National, the strongest recovery in the North | Short term (≤ 2 years) |

| Government subsidies for forage quality improvement programs | +0.7% | National, higher uptake across the Centre-North | Medium term (2-4 years) |

| Expansion of Italy’s organic dairy segment | +0.6% | National, long-term growth steered by premium retail demand | Long term (≥ 4 years) |

| Carbon-farming incentives encouraging legume rotations | +0.5% | National, aligned with Community-acquired pneumonia (CAP) 2023-2027 eco-scheme rollout. | Long term (≥ 4 years) |

| Rising exports of dehydrated alfalfa to North Africa | +0.4% | Emilia-Romagna and Veneto export corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for Premium Meat and Dairy Products

Cheese consortium rules mandate high forage inclusion that cannot be replaced by cheaper concentrates, which fixes baseline demand for top-grade alfalfa hay. Grana Padano and Parmigiano Reggiano, together, accounted for more than one-quarter of Italian cheese output in 2023, cementing a structural pull from the dairy belt. Farm-gate milk prices in Lombardy increased 18.9% year-over-year to EUR 59.67 per 100 liters (USD 63.10), providing dairies with the headroom to pay premiums for protein-rich forage. Higher protein targets in milk, now averaging 3.51%, place alfalfa’s 18-22% protein at the center of ration design that underpins Protected Designation of Origin (PDO) quality.

Growth in Livestock and Poultry Herd Size

Dairy cattle feed consumption increased in 2024, up by 3.1% on the year, while poultry feed hit roughly 6 million tons as broiler farms restocked after H5N1 losses. Integrators now blend 3-5% alfalfa pellets for gut fiber and natural pigments, widening demand beyond ruminants. Buffalo herds in Campania maintain niche yet steady volumes for mozzarella. Rising per-animal forage ratios in organic dairies amplify base tonnage and protect the Italy alfalfa hay market from substitution risk.

Government Subsidies for Forage Quality Improvements Programs

Italy’s Rural Development Programme reimburses up to 40% of investments in dehydration equipment, lowering the break-even point for mid-sized processors [1]Source: European Commission, “CAP Strategic Plans,” European Commission, agriculture.ec.europa.eu. Eco-schemes pay EUR 110 per hectare (USD 116) for legume cover crops and EUR 250 per hectare (USD 263) for permanent grasslands, trimming cultivation costs by about 12-15%. Subsidies accelerate the adoption of precision dryers that maintain moisture levels under 12%, which is crucial for producing export-grade pellets. Policy stability through 2027 gives growers confidence to scale acreage instead of rotating into cereals.

Rising Exports of Dehydrated Alfalfa to North Africa

Densified pellets ship from Adriatic ports to Morocco and Tunisia at 10-15% price premiums versus domestic bales, offering processors a margin hedge. Freight disruptions in 2024 increased bunker costs, but a decrease in pellet density reduced transport expenses per protein unit, making exports viable. Italian agribusiness is also securing forward supply through a USD 441-452 million Algerian farm project led by Bonifiche Ferraresi [2]Source: Government of Italy, “Italy and Algeria Sign Agreement on High-Tech Regenerative Agriculture,” Governo, governo.it. Strong North African demand cushions sales during domestic market saturation, making export growth a meaningful tailwind.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal dependency and climatic vulnerability | -0.8% | Po Valley and southern irrigated plains | Short term (≤ 2 years) |

| High production and road freight costs | -0.7% | National, acute on long-haul south-north corridors | Short term (≤ 2 years) |

| Competition from hydroponic high-protein fodder | -0.4% | Lombardy and Veneto dairy zones | Medium term (2-4 years) |

| European Union Nitrate Directive limits on nitrogen fertilization | -0.5% | 30% of the farmland in vulnerable zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seasonal Dependency and Climatic Vulnerability

The 2022 drought slashed yields by 15% and spotlighted the Po Valley’s fragile water balance. Summer evapotranspiration peaks at 8 millimeters per day, prompting stands to enter early dormancy. Floods in May 2023 destroyed 50,000 hectares, driving alfalfa meal prices up 44.1% to EUR 330.57 per ton. Climate models predict 10-20% less summer rainfall by 2050, so growers must invest in precision irrigation, which costs EUR 150-250 per hectare, to safeguard yields.

High Production and Road-Freight Costs

Diesel averaged EUR 1.60-1.80 per liter (USD 1.68-1.89) in 2024, while driver shortages lifted freight rates 3.9 percentage points quarter on quarter [3]Source: European Commission, “Road Freight Transport Statistics,” Eurostat, ec.europa.eu. Bales fill truck volume quickly, so a 500-kilometer haul costs EUR 40-50 per ton, which is 12-15% of the delivered price. Toll hikes in January 2025 added EUR 2-3 per ton. Rising labor and diesel costs squeeze margins for both growers and dairy buyers.

Segment Analysis

By Product Type: Pellets Gain Share on Poultry Demand

Bales controlled 48% of the Italy alfalfa hay market share in 2024, as traditional dairy barns favor easily stackable formats that allow for rapid visual quality checks. The Italy alfalfa hay market size for pellets is projected to expand at an 8.2% CAGR through 2030, driven by poultry integrators that cut feed storage space by up to 70% when switching from bales. Pelleting heat also deactivates anti-nutritional factors, which boosts digestibility for broilers. Cubes remain a niche for horses and small ruminants where uniform particle size limits waste. Precision moisture sensors and satellite-guided irrigation help pellet producers achieve the sub-12% moisture threshold that prevents mill blockage, while smaller bale-only farms often tolerate 14-18% moisture, keeping entry barriers high for densified formats.

Capital outlays of EUR 2 to 4 million (USD 2.1 to 4.2 million) for a 3 to 5 ton-per-hour pellet line leave the densified segment in the hands of vertically integrated processors. Growers who cannot justify the investment continue to supply regional dairy buyers who value physical inspection of bale color and leaf retention. Yet as poultry output grows, pellets will likely chip away at bale dominance. Pellets also carry export upside because the higher density cuts freight by up to 30%, which widens margins on Moroccan and Tunisian shipments. The Italy alfalfa hay market, therefore, shows a clear division between bale-centric traditional supply chains and pellet-led growth channels aligned with poultry and export customers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Poultry Feed Accelerates After Disease Recovery

Meat and dairy animal feed accounted for 54% of the Italy alfalfa hay market size in 2024. Ration guidelines for Grana Padano and Parmigiano Reggiano stipulate a minimum forage dry matter, so nutritional consultants regularly include 15-20% alfalfa to sustain milk-fat percentages. The Italy alfalfa hay market faces a low substitution risk in this segment because over-feeding concentrates can cause rumen acidosis, which quickly reduces cheese yields.

Poultry feed is anticipated to grow at a 9% CAGR through 2030. Following flock restocking after 2023 H5N1 losses, integrators use 3-5% alfalfa pellets for natural xanthophyll pigments that improve skin color and market value. With broiler production back on an upward slope, densified forage is now a standard part of least-cost formulation models. Horse feed and pet food consume smaller tonnage but command premium prices, offering margin hedges for processors that can segment supply. Value-added human food products, such as Agricole Forte’s alfalfa flour line, position the industry to diversify as consumer interest in green protein continues to grow.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Northern Italy dominates supply and consumption. Emilia-Romagna, Lombardy, and Veneto produce the majority of the national volume, thanks to fertile soils, widespread irrigation, and their proximity to the cheese belt. The Po Delta alone supports four to five alfalfa cuts per year and yields 10-12 metric ton of dry matter per hectare under precision practices. Lombardy accounts for 45% of the national milk output, and many dairy cooperatives maintain permanent meadows that secure regional forage demand.

Southern regions such as Campania supply buffalo mozzarella dairies that prefer local hay but still import from the north during shortages. Organic area in the South doubled from 2010 to 2023, but the share of national organic land slipped to about 55% as Centre-North investment accelerated. Regions like Tuscany and Umbria fall in the middle, serving local equestrian and specialty cheese buyers. Sardinia and Sicily remain net importers because water scarcity favors higher-value crops, such as citrus and olives, over forage.

Export flows add a Mediterranean dimension. Adriatic ports in Emilia-Romagna and Veneto ship densified alfalfa to Morocco and Tunisia at a 10–15% premium over domestic bale prices. Freight costs rose 8-12% in 2024, so exporters rely on pellet density to protect margins. Bonifiche Ferraresi’s USD 441-452 million Algerian farm deal signals strategic moves to secure North African forage chains, though field trials will likely add alfalfa only after cereal rotation years stabilize soil nitrogen. Whether the Italy alfalfa hay market can scale exports depends on maintaining processing capacity and competitive shipping while domestic dairy demand remains inelastic.

Competitive Landscape

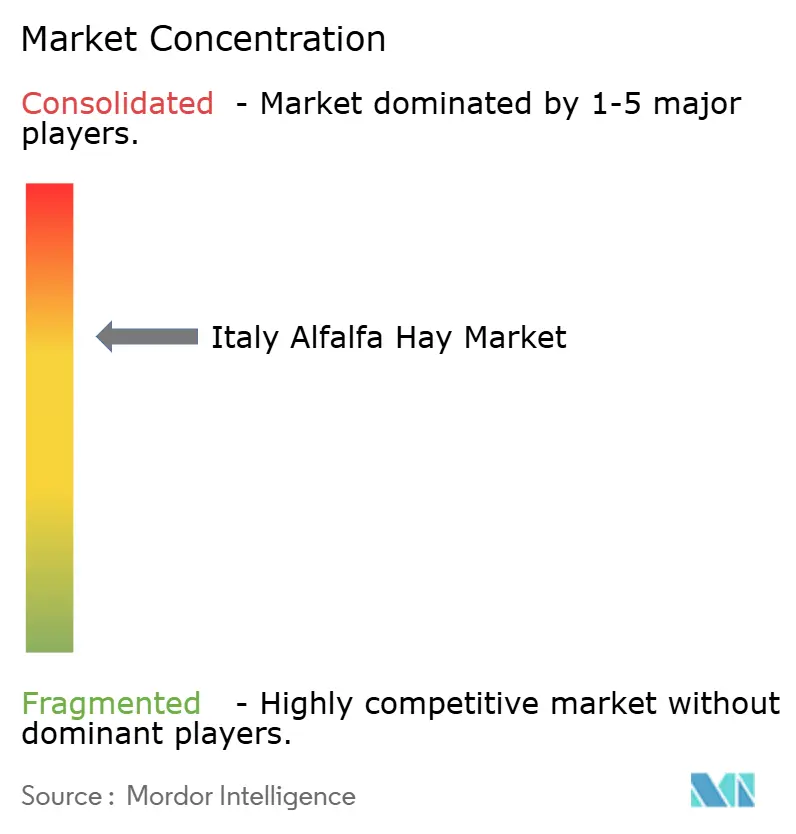

Italy’s alfalfa hay market is moderately concentrated. The top five companies account for the majority of the revenue. Gruppo Carli leads due to its end-to-end control, from cultivation to pellet packaging. Al Dahra Holding owns a significant share after acquiring Italian dehydrators, reflecting overseas appetite for European forage assets that can feed both domestic dairies and export channels. Biselli Foraggi Group, Agricole Forte, and Società Produzioni Erbe Disidratate collectively hold a prominent market share through regional specialization, organic certification, and niche innovations, such as alfalfa flour for biscuits.

The strategic focus is on backward integration into farmland and forward integration into branded feed lines. Top players lease 2,000 to 4,000 hectares each, which insulates them from price spikes on the open market. They also market hay-fed labels that carry premiums in Protected Designation of Origin (PDO) cheese chains. Foreign capital intensifies consolidation pressure on family-run growers, who often lack succession plans or the capital required for pellet upgrades.

Technology widens the gap. Leaders install Internet of Things (IoT) sensors in dryers to minimize moisture variation and operate pellet lines that comply with export hygiene regulations. Smaller bale suppliers rely on manual checks and outdated balers, which limit access to premium buyers who demand standardized nutrient profiles. The competitive field will depend on whether midsized cooperatives secure Community-acquired pneumonia (CAP) grants worth 40% of the capital cost for new equipment. Without that support, the Italy alfalfa hay market could tilt further toward the present top five.

Italy Alfalfa Hay Industry Leaders

-

Gruppo Carli

-

Al Dahra Holding

-

Biselli Foraggi Group SRL

-

Agricole Forte S.a.r.l

-

Società Produzioni Erbe Disidratate

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2024: The European Feed Manufacturers’ Federation and Assalzoo hosted 150 participants in Rome to debate sustainable livestock feed, reinforcing domestic focus on low-carbon protein sourcing. This initiative is anticipated to positively influence Italy's alfalfa hay market by encouraging sustainable practices and increasing demand for low-carbon feed options.

- June 2024: Bonifiche Ferraresi signed a EUR 420-430 million (USD 441-452 million) agreement with the Algerian government for a 36,000-hectare regenerative farming project in Timimoun. This initiative is anticipated to strengthen Italy's position in the global alfalfa hay market by enhancing production capabilities and fostering international collaboration.

Italy Alfalfa Hay Market Report Scope

Alfalfa hay, also called lucerne, is a perennial flowering plant in the legume family Fabaceae. Alfalfa hay is a grass, legume, or another herbaceous plant that has been cut and dried to be stored for use as animal fodder, either for large grazing animals raised as livestock, such as cattle, horses, goats, and sheep, or for smaller domesticated animals such as rabbits and guinea pigs. The Italy alfalfa hay market is segmented by Product type into Bales, Pellets, and Cubes, and Application into Meat/Dairy Animal Feed, Poultry Feed, Horse Feed, and Other Applications. The report offers the market size and forecasts for volume in (metric tons) and value in (USD) for all the above segments.

By Product Type

| Bales |

| Pellets |

| Cubes |

By Application

| Meat and Dairy Animal Feed |

| Poultry Feed |

| Horse Feed |

| Other Applications |

| By Product Type | Bales |

| Pellets | |

| Cubes | |

| By Application | Meat and Dairy Animal Feed |

| Poultry Feed | |

| Horse Feed | |

| Other Applications |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Italy alfalfa hay market?

The Italy alfalfa hay market is valued at USD 0.65 billion in 2025 and is projected to reach USD 0.86 billion by 2030.

Which product type holds the largest share in Italy’s alfalfa trade?

Bales lead with 48% of the market because most dairy farms have storage designed for rectangular stacks.

Why are pellets gaining popularity in Italy’s poultry sector?

Pellets reduce storage space by up to 70% and supply pigments and fiber that improve broiler performance, supporting a forecasted 8.2% CAGR for this format.

How does government policy support Italian alfalfa production?

Eco-schemes within the Community-acquired pneumonia (CAP) pay EUR 110-250 per hectare for legume crops and permanent grasslands, cutting production costs and encouraging crop rotations that include alfalfa.

What climate risks threaten Italian alfalfa growers?

Drought in the Po Valley and flood events, such as the 2023 Emilia-Romagna disaster, can swing yields by double digits, which prompts growers to adopt precision irrigation.

Page last updated on: