Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

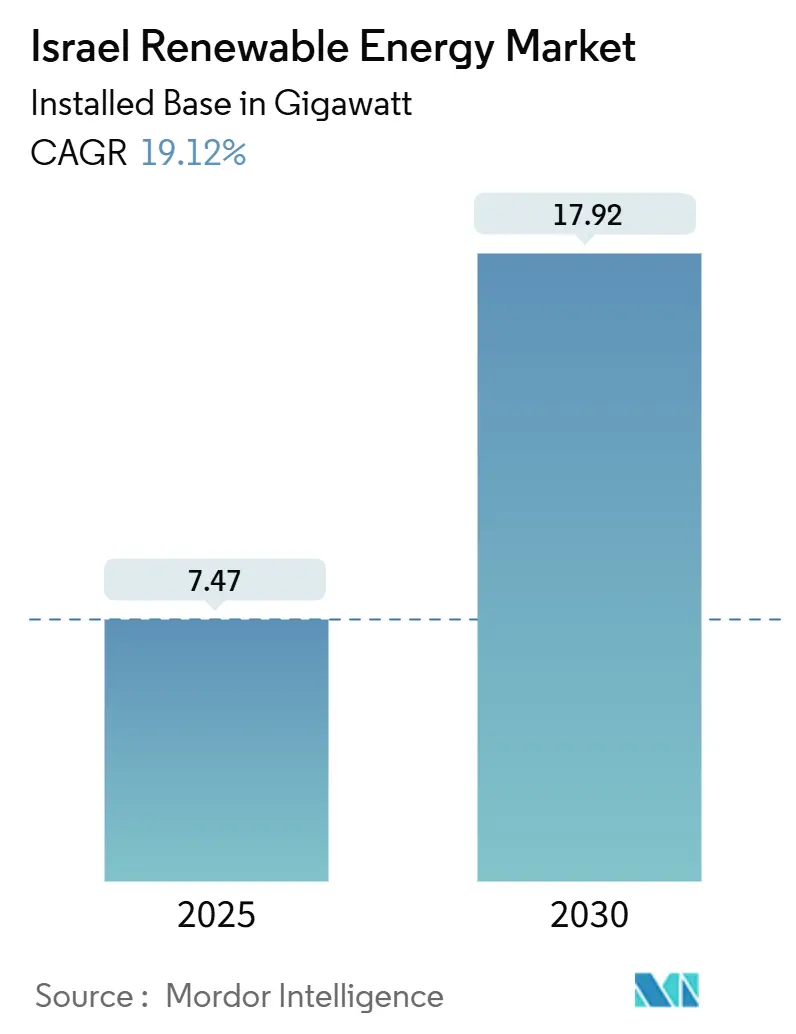

| Market Volume (2025) | 7.47 gigawatt |

| Market Volume (2030) | 17.92 gigawatt |

| Growth Rate (2025 - 2030) | 19.12% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Israel Renewable Energy Market Analysis by Mordor Intelligence

The Israel Renewable Energy Market size in terms of installed base is expected to grow from 7.47 gigawatt in 2025 to 17.92 gigawatt by 2030, at a CAGR of 19.12% during the forecast period (2025-2030).

This expansion reflects a strategic pivot toward energy autonomy as regional security disruptions heighten the urgency of diversifying away from fossil imports.[1]Nikkei Asia, “Conflicts Spur Mideast to Seek Energy Autonomy,” asia.nikkei.com Utility-scale solar projects dominate new builds, while distributed generation systems scale quickly under mandatory rooftop solar rules for new structures. Independent power producers (IPPs) now finance most capacity additions, signalling a permanent shift from state-controlled generation to private capital. Rapid cost declines in photovoltaic modules, rising corporate clean-power purchases from Israel’s tech and defence campuses, and the revival of long-term feed-in tariffs underpin the strong demand outlook.

Key Report Takeaways

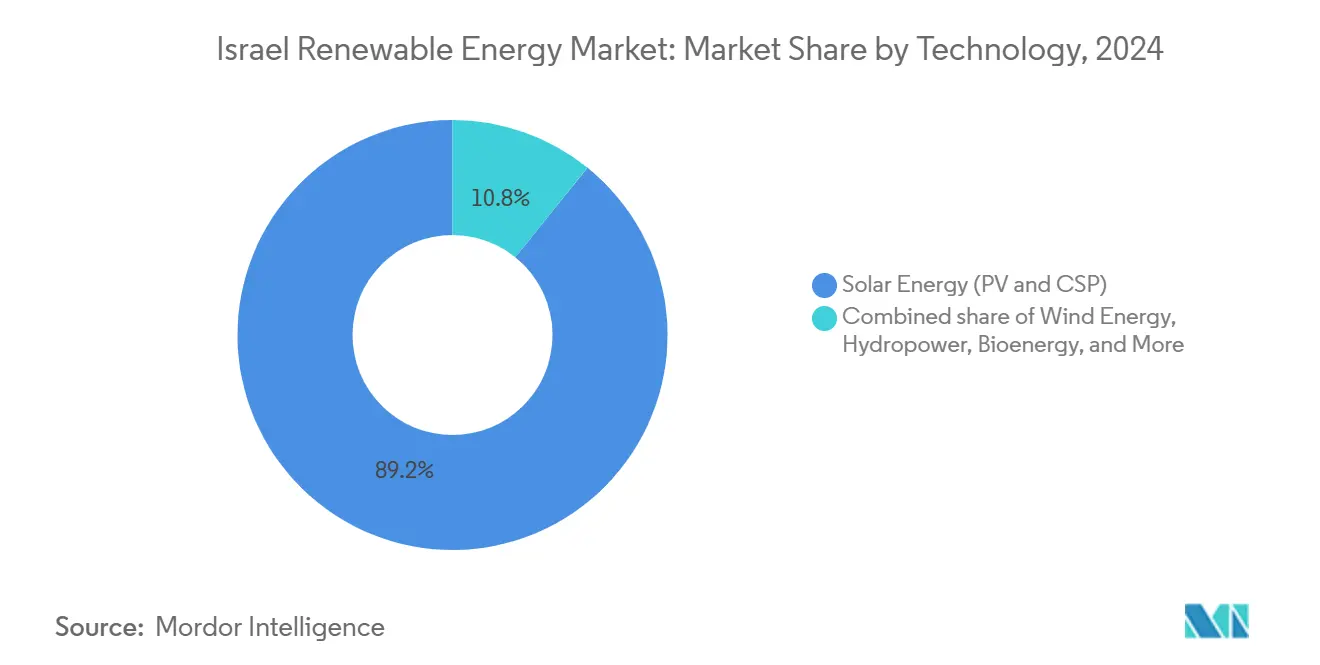

- By technology, solar energy commanded 89.2% of the Israel renewable energy market share in 2024; wind energy is projected to lead segment growth with a 42.0% CAGR through 2030.

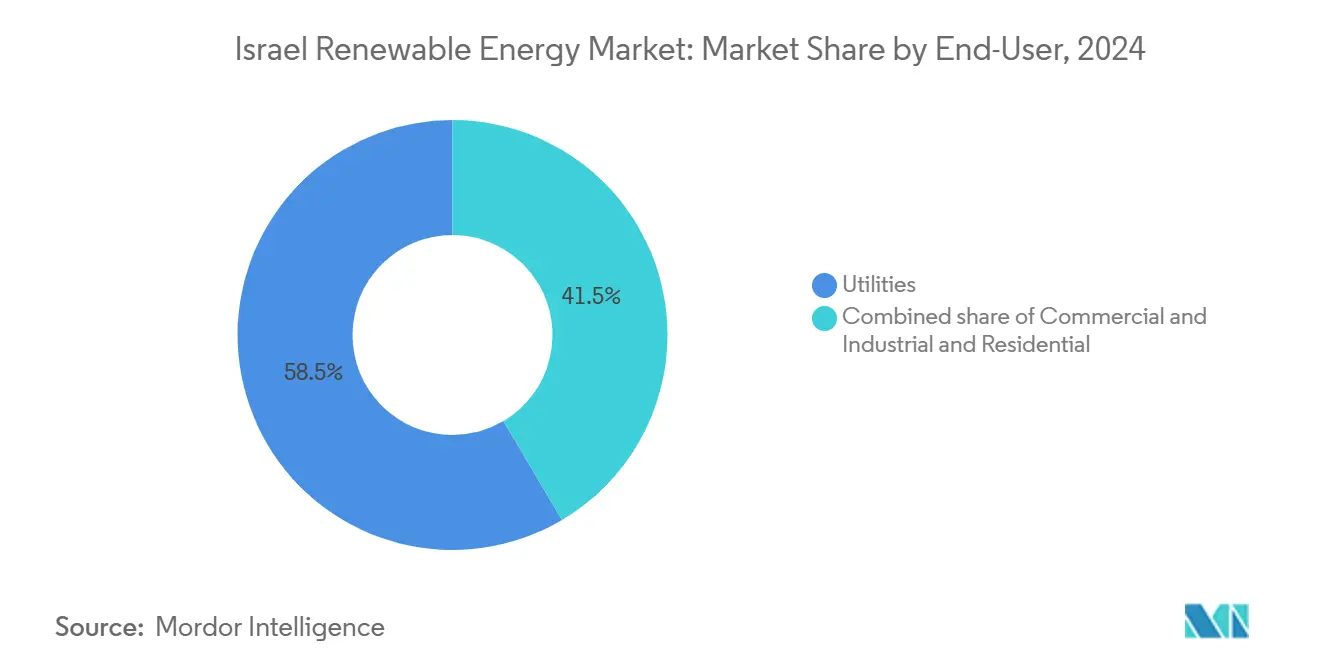

- By end-user, utilities accounted for 58.5% of the Israel renewable energy market size in 2024, while commercial and industrial users recorded the fastest growth at a 24.7% CAGR to 2030.

Israel Renewable Energy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed feed-in-tariffs revival | +2.5% | Northern Israel, Negev, Arava | Medium term (2-4 years) |

| Falling LCOE of utility-scale solar PV | +3.5% | Negev (Dimona, Ashalim), Western Negev (Takuma) | Short term (≤ 2 years) |

| 40% renewable-electricity target for 2030 | +4.0% | National | Long term (≥ 4 years) |

| Corporate PPAs from tech & defense campuses | +2.0% | Tel Aviv, Haifa tech corridors | Medium term (2-4 years) |

| Emerging offshore-wind resource in EEZ | +1.5% | Mediterranean Exclusive Economic Zone | Long term (≥ 4 years) |

| Agrivoltaics for arid-land optimization | +1.0% | Negev, Arava, Galilee | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-backed Feed-in-Tariffs Revival

Israel reinstated 20-year feed-in-tariff contracts that guarantee predictable cash flows for projects up to 250 MW.[2]International Energy Agency, “Israel Resurrects Solar Feed-in Tariffs,” iea.org The mechanism corrects the financing gap created after the 2013 shift to net-metering and now underpins at least 250 MW of annual solar additions mandated by Government Resolution 4450. Smaller IPPs benefit most because the tariff improves bankability without large corporate offtakers. Activity is concentrated in the Negev and Golan, where land is abundant yet grid access remains limited, prompting developers to co-site new substations with solar parks. The policy directly raises installation rates and broadens investor participation in the Israel renewable energy market.

Falling LCOE of Utility-scale Solar PV

EDF Renewables won a 300 MW tender at USD 0.019/kWh in 2024, a record low that establishes solar as Israel’s least-cost new-build technology.[3]PV Magazine, “EDF Wins 300 MW Tender at USD 0.019/kWh,” pv-magazine.com High isolation above 2,000 kWh/m², superior tracker designs, and volume procurement have pushed PV costs 45% below 2022 levels. Industrials now lock in 20-year corporate PPAs to hedge fuel volatility, while developers such as Solaer report 1.78 GW in construction, helped by cheap modules. The price advantage catalyses utility-scale projects and accelerates distributed rooftop rollouts, cementing solar PV as the backbone of the Israel renewable energy market.

2030 30%-RE Target & Net-Zero 2050 Pledge

The revised policy requires 17.1 GW of solar and 3 GW of storage by 2030. Achieving this requires grid digitalization, flexible generation, and aggressive battery build-out, with the Ministry of Energy allocating USD 710 million for storage tenders over the period 2025-2027. The roadmap lifts investor confidence, aligns multiple ministries on permitting reforms, and integrates dual-use agrivoltaics into land-scarce regions. Long-term clarity reinforces corporate decarbonisation plans and makes the Israel renewable energy market a high-priority target for global capital inflows.

Corporate PPAs from Tech & Defence Campuses

Multinationals located in greater Tel Aviv now sign 10- to 20-year renewable PPAs that bundle battery capacity for 24/7 delivery. Defence OEMs similarly commit to clean-power sourcing to secure NATO procurement eligibility. These bankable offtake contracts lower financing costs by up to 120 basis points, accelerating greenfield pipelines for IPPs. The clustering of high-load campuses enables dedicated feeder lines that ease urban grid congestion, further integrating distributed PV into the Israeli renewable energy industry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion & limited sub-station capacity | -2.5% | Northern Israel, Takuma, Arabah | Short term (≤ 2 years) |

| Scarcity of suitable land parcels | -2.0% | National, acute in coastal plains and central districts | Medium term (2-4 years) |

| Geopolitical/security curtailment risks | -1.5% | Border regions | Medium term (2-4 years) |

| Water stress for CSP cooling | -1.0% | Negev (Ashalim CSP complex) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion & Limited Sub-Station Capacity

Three high-renewable zones already exceed local switching-station ratings at midday, forcing 5-8% curtailment in 2024. The Israel Electric Corporation plans to invest NIS 20 billion by 2027 to add 738 km of 400 kV lines; however, the build-out lags behind solar additions, potentially delaying project commissioning by up to a year. Developers now pre-screen sites for grid headroom rather than solar irradiance, concentrating new capacity in zones with immediate access to interconnection.

Scarcity of Suitable Land Parcels

Competing claims from agriculture, defense, nature reserves, and urban growth leave fewer than 500 km² genuinely available for utility solar. Multi-stakeholder permitting can stretch to 18-24 months, and developers pay risk premiums for contested sites, such as the Golan Heights, where Doral plans a 300 MW solar-plus-1.2 GWh storage plant valued at ILS 900 million (approximately USD 253 million). Higher-density configurations, bifacial modules, elevated trackers, and agrivoltaics boost yield per hectare by 20-30%, effectively stretching scarce land.

Segment Analysis

By Technology: Solar Dominance Meets Wind Acceleration

Solar energy led the Israel renewable energy market share at 89.2% of installed capacity in 2024, reflecting an isolation of 2,200-2,800 kWh/m²/year in the Negev and LCOE below USD 0.02/kWh in recent tenders. Wind capacity is small today but is set to outpace all other technologies with a 42.0% CAGR through 2030, supported by the first 207 MW utility plant and by the Great Sea Interconnector that will channel wind-heavy imports. The Israel renewable energy market size for solar is projected to exceed 15 GW by 2030, while wind may surpass 1.8 GW over the same horizon.

Hybrid assets at the Ashalim complex combine CSP with 4.5-hour thermal storage to firm evening peaks, illustrating a transition toward dispatchable renewables. Hydropower, bioenergy, geothermal, and ocean energy collectively account for less than 2% of total capacity. Eco Wave Power’s 100 kW pilot at Jaffa Port highlights ongoing innovation, yet its LCOE above USD 0.20/kWh limits near-term scaling.[4]Eco Wave Power, “Jaffa Port Pilot Results,” ecowavepower.com Israeli developers increasingly focus on export-oriented hydrogen and wind projects abroad, while domestic growth centers on solar-plus-storage and agrivoltaics.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: Utilities Lead, C&I Surges

Utilities accounted for 58.5% of the Israel renewable energy market size in 2024, backed by centralized tenders that awarded 1.5 GW of battery capacity in February 2025. Commercial and industrial customers, however, are projected to grow at a rate of 24.7% annually through 2030. Corporate PPAs enable on-site solar at prices below grid tariffs, and the rooftop solar mandate targets 3.5 GW of new installations by 2040. The Israel renewable energy market share of C&I segments will rise as projects co-locate generation with load centers to hedge price volatility.

Residential adoption lags due to Israel’s high rate of apartment dwelling, which complicates rooftop ownership. A rooftop-mapping tool launched in 2025 may reduce permitting time, but fewer than 50 MW of capacity were added by households in 2024. Aggregators like Nofar Energy and Shikun & Binui are bundling multi-tenant rooftops to achieve bankable scale, yet structural hurdles keep the residential deployment niche for now.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Northern Israel benefits from reliable ridge-top winds across the Golan Heights, enabling 207 MW of onshore turbines that supply 70,000 households and reduce CO₂ emissions by 180,000 t annually. Developers queue an additional 420 MW, yet they still struggle with grid capacity limits on the Katzrin-Haifa corridor. In contrast, the Negev Desert offers abundant sunlight and inexpensive terrain, hosting 55% of Israel's installed PV base in the renewable energy market, including the flagship 300 MW EDF project.

Central coastal districts face land scarcity and high property values, but commercial roofs, carports, and floating systems on Mekorot reservoirs fill the gap. Ten reservoir-top arrays now contribute 47 GWh yearly, illustrating how dual-use sites sidestep land bottlenecks. The Tel Aviv tech corridor also anchors a burgeoning corporate PPA ecosystem that underwrites utility-scale solar in outlying zones, while blending battery-backed rooftop PV for data center resiliency.

Israel's Mediterranean Exclusive Economic Zone is likely to host the nation's first offshore wind pilot after 2028, extending geographic diversity and improving winter evening supply when solar energy fades. Finally, agricultural valleys deploy agrivoltaic rows that shade crops, conserve water, and generate revenue. The REGACE consortium trials CO₂-enriched greenhouses under thin-film panels, demonstrating how rural economies can benefit from Israel's renewable energy market without compromising food output.

Competitive Landscape

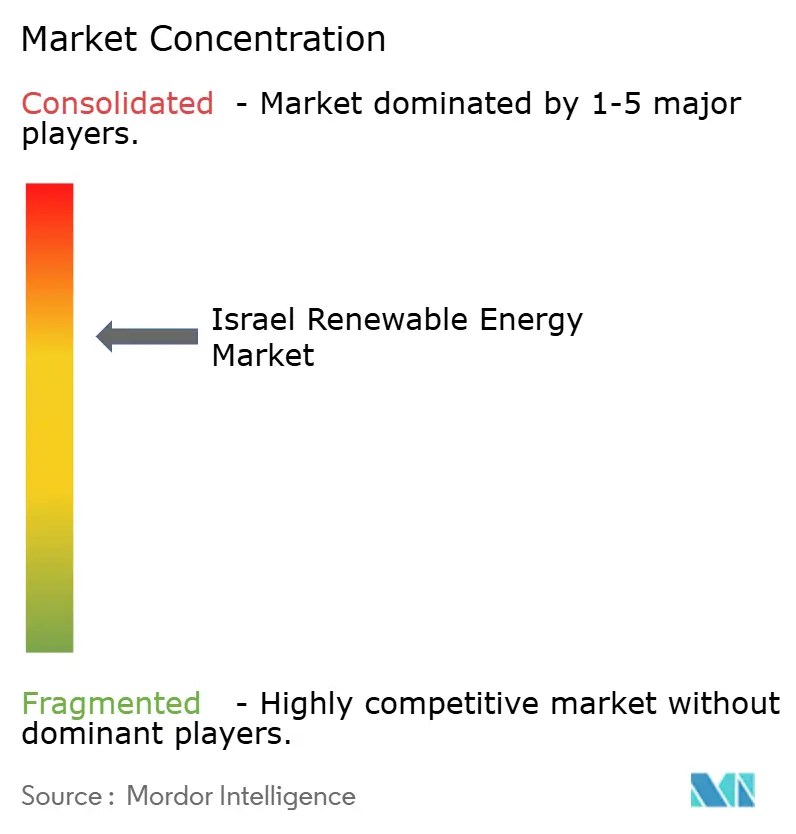

Competition is moderate yet tilting toward consolidation, as giga-scale projects demand deep balance sheets and integrated storage expertise. Domestic champions Energix, Enlight, and Econergy draw on in-house EPC capabilities, land-bank pipelines, and agile community engagement. They collaborate with global suppliers such as First Solar for bifacial modules and SMA for central inverters, compressing delivery timelines to under 14 months. International majors EDF Renewables and Ormat Technologies import project-finance acumen, pushing bid prices to record lows that challenge smaller entrants.

Ormat’s 300 MW/1.2 GWh storage win in February 2025 marks a strategic play into grid-scale batteries, signalling a future where solar-plus-storage packages become the default tender requirement. Meanwhile, TriSolar pilots agrivoltaic systems, Brenmiller commissions thermal storage for industrial steam, and Eco Wave Power exports its breakwater technology to Portugal, underscoring Israel’s depth in cleantech innovation.

Market share remains dispersed: the top five developers controlled roughly 43% of operating renewable capacity in 2024, down from 48% in 2023 as new IPPs enter through rooftop and C&I niches. Strategic joint ventures with pension funds and sovereign investors are common, reflecting confidence in the Israel renewable energy market despite geopolitical volatility. Looking ahead, the ability to pair PV with four-hour batteries and to secure long-tenor PPAs will separate enduring leaders from one-off project builders.

Israel Renewable Energy Industry Leaders

-

Enlight Renewable Energy Ltd.

-

EDF Renewables

-

Doral Group

-

Energix Renewable Energies Ltd.

-

Ormat Technologies Inc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Ormat Technologies secured tolling agreements for 300 MW / 1.2 GWh battery systems valued at USD 200 million.

- August 2024: Israel has mandated solar installations on new non-residential buildings, aiming for an additional 3.5 GW of rooftop capacity by 2040.

- August 2024: EDF Renewables began building Israel’s largest 300 MW PV plant in the Negev at record-low tariffs.

- January 2024: Technion announced a breakthrough in green hydrogen powered by renewables for industrial use.

Israel Renewable Energy Market Report Scope

The Israel renewable energy market report includes:

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecasted capacity for Israel's renewable sector by 2030?

Installed renewable capacity is projected to reach 17.92 GW by 2030, growing at a 19.12% CAGR from 2025.

How dominant is solar within Israel's generation mix?

Solar technologies held 89.2% of installed renewable capacity in 2024 and remain the core pillar of growth.

Why are corporate PPAs significant in Israel?

Deregulation in 2024 allowed direct PPAs, letting corporates lock in discounted power prices and meet carbon goals while driving new project finance.

What role does storage play in upcoming projects?

The 2025 tender awarded 1.5 GW of batteries, positioning storage as a grid-relief valve and a profit center for co-located solar.

How is land scarcity being addressed?

Developers deploy agrivoltaics, floating solar, and higher-density panel layouts to boost yield per hectare and navigate land constraints.

Which international companies are active in Israel's market?

EDF Renewables, Ormat Technologies, and several Chinese equipment suppliers have secured tenders or supplied hardware alongside domestic champions.

Page last updated on: