Market Trends of Investment Casting Industry

This section covers the major market trends shaping the Investment Casting Market according to our research experts:

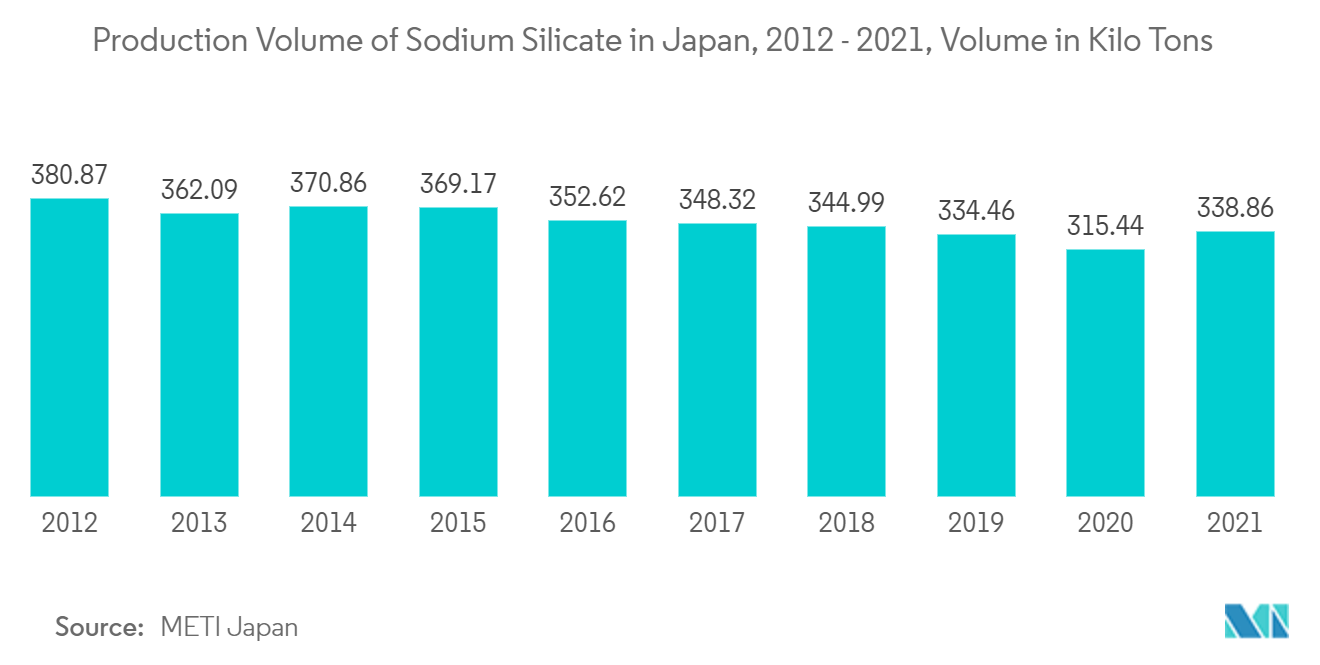

Sodium Silicate Process To Exhibit The Highest Growth Rate

Silica sol casting gives the investment castings better dimensional accuracy and surface finish with minimal defects. Hence, the cost of the process is higher than that of the water glass casting. Silica sol zircon sand is very expensive, and the preparation required is also higher, which is a prime reason for the higher costs.

Due to its higher costs, the silica sol process has comparatively less adoption in foundries. The silica sol investment casting used in automotive or industrial components costs around 6.5 USD/kg on average.

Several companies have now identifed the sodium silicate casting as the economical cause over the ceramic casting. However, this process is preferred if the highest casting quality and the low repair rate are the main focus of the end user. Compared to the water glass process, the silica sol process can produce extra-large parts weighing 50-100 kg. Hence, this process is used for producing larger and heavier parts, like water pumps, impellers, diversion shells, pump bodies, ball valve bodies, and valve plates. At the same time, this process is widely used to produce extra small parts (2-1000 g) that require high dimensional accuracy.

The sodium silicate process is slowly becoming more popular in regions like Asia-Pacific, where Japan has showcased itself to lead the production demand from forefront. As a result of the ongoing efforts to improve the quality and dimensional accuracy of the components produced.

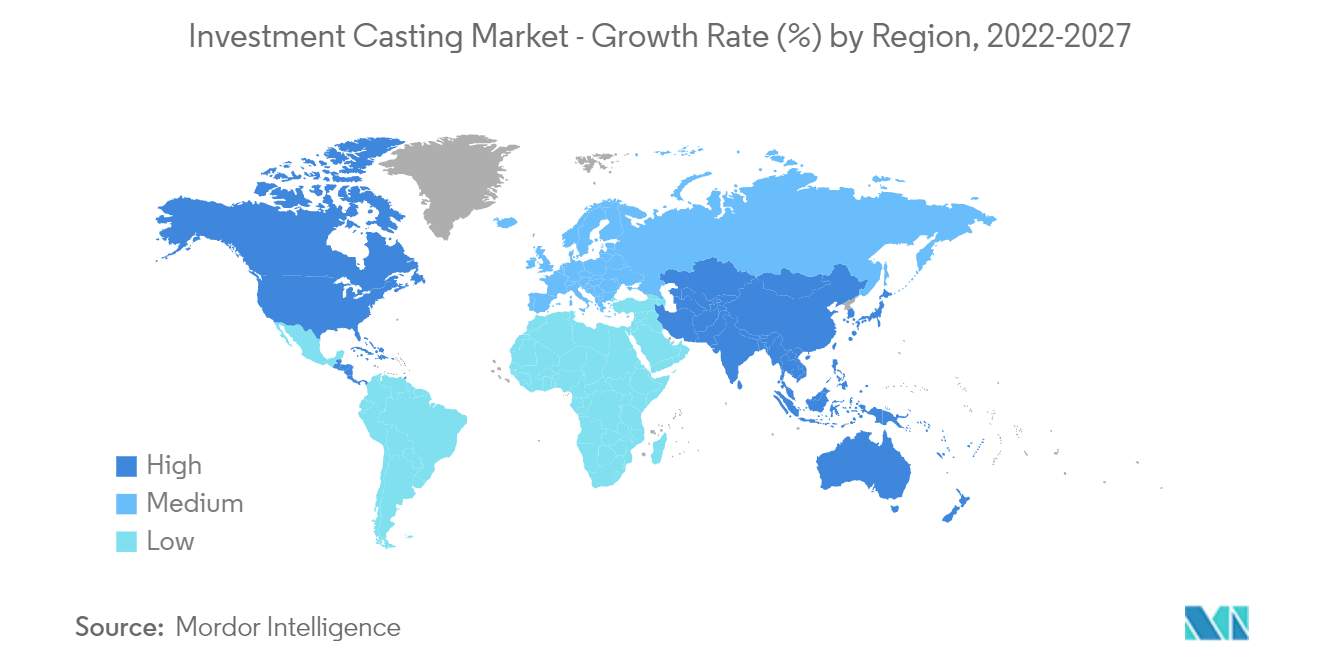

North America Leads the Investment Casting Market

North America is leading the investment casting market and is likely to hold the top position, followed by Asia-Pacific and Europe. The factors attributable to North America's growth are the expanding manufacturing industry, primarily industrial gas and aerospace and defense applications, and the presence of significant defense aircraft and component manufacturers in the region, including Lockheed Martin, Raytheon, and Northrop Grumman.

Aerospace manufacturing is one of the major sectors in the United States, with production plants for major aircraft programs, like Boeing 737, Boeing 777, Boeing 787, and Airbus A220 located in the region. The manufacturing of military aircraft programs, like the F-35, in the country is expected to generate demand for investment casting parts.

The United States is one of the major automotive industries in the world, which contributes at least 3% to the overall gross domestic product (GDP) of the country. In addition, the country is one of the largest manufacturers of the luxury car market with net revenue of USD 5 billion in 2021. Luxury car maker BMW in 2021, reported record-breaking sales of over 336,600 units vehicles.

However, the automotive industry in the United States witnessed a hit due to the COVID-19 pandemic, as the majority of the production sites were either closed or operating at reduced capacity. In April 2022, United States new vehicles sales were reported 1,256, 224 units with a 18% decline compared to April 2021 figures. In addition, during April, passenger car sales dropped down to 23.3% with reporting 278,827 units, while SUV and truck sales also decreased 16.3% with 977,397 units. Q1 2022, has been less favorable for United States automotive sector. These expanding auto sector evoke high utilization of investment casting application for automotive parts and compnents will would likely to elevate the demand for investment casting during long term period.

Further, according to the Aerospace Industries Association of Canada, Airbus, Boeing, De Havilland Canada, and Bombardier Inc. are some of the major aerospace manufacturers in the countrywith 95% of companies running at partial capacity. De Havilland Canada plans to gradually begin the production of aircraft in phases. Key aersopace companies are seen expansing their business potential in order to elevate the demand for investment casting in the region. For instance, In November 2022, Aircraft engine manufacturer Pratt & Whitney announced the opening of their new turbine airfoil facility in United States. The fcility would be equipped with advance casting foundry with combined investment of USD 650 million.

Morover, key casting companies are also seeking oppotunities to expans their investment casting potnetial in North America to resonate elevated sales bars amid rising demand. For instance,In September 2022, Signicast Corporation which is form technology company announced the celebration of its new opening of latest investment casting facility.

Cosidering these factors and development demand for investment casting is anticipated to hold high potential for growth in North America owing to widely spread application.