Interventional Radiology Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 30.15 Billion |

| Market Size (2031) | USD 39.65 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

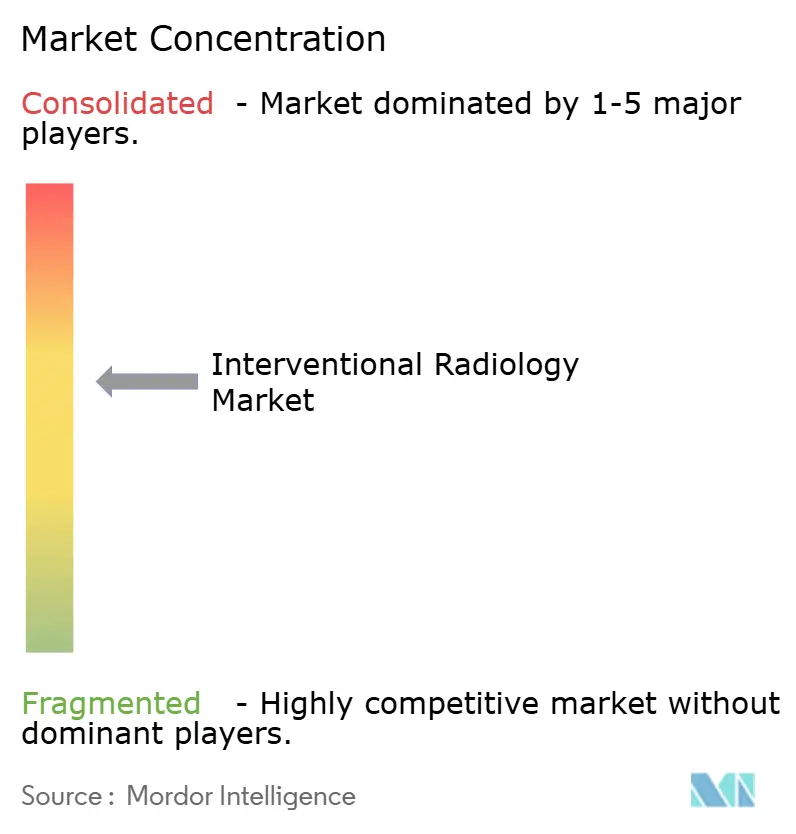

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Interventional Radiology Market Analysis by Mordor Intelligence

The interventional radiology market size is expected to grow from USD 28.55 billion in 2025 to USD 30.15 billion in 2026 and is forecast to reach USD 39.65 billion by 2031 at 5.62% CAGR over 2026-2031. Rapid migration from open surgery to minimally invasive, image-guided therapies underpins this expansion, reducing recovery times and lowering total expenditure for payers and providers. Artificial intelligence embedded in advanced imaging suites improves real-time guidance, elevates care quality, and stimulates procedure volumes in complex cardiovascular, oncologic, and neurovascular cases. Demand also benefits from a worldwide rise in chronic diseases that require repeat interventions and long-term disease management. At the same time, outpatient centers capture shifting procedure flows as pay-for-value reimbursement models reward cost-efficient care settings. Intensifying R&D investment from leading manufacturers sustains a strong pipeline of devices, software, and robotics that widen the addressable patient pool and open high-margin consumable revenue streams.

Key Report Takeaways

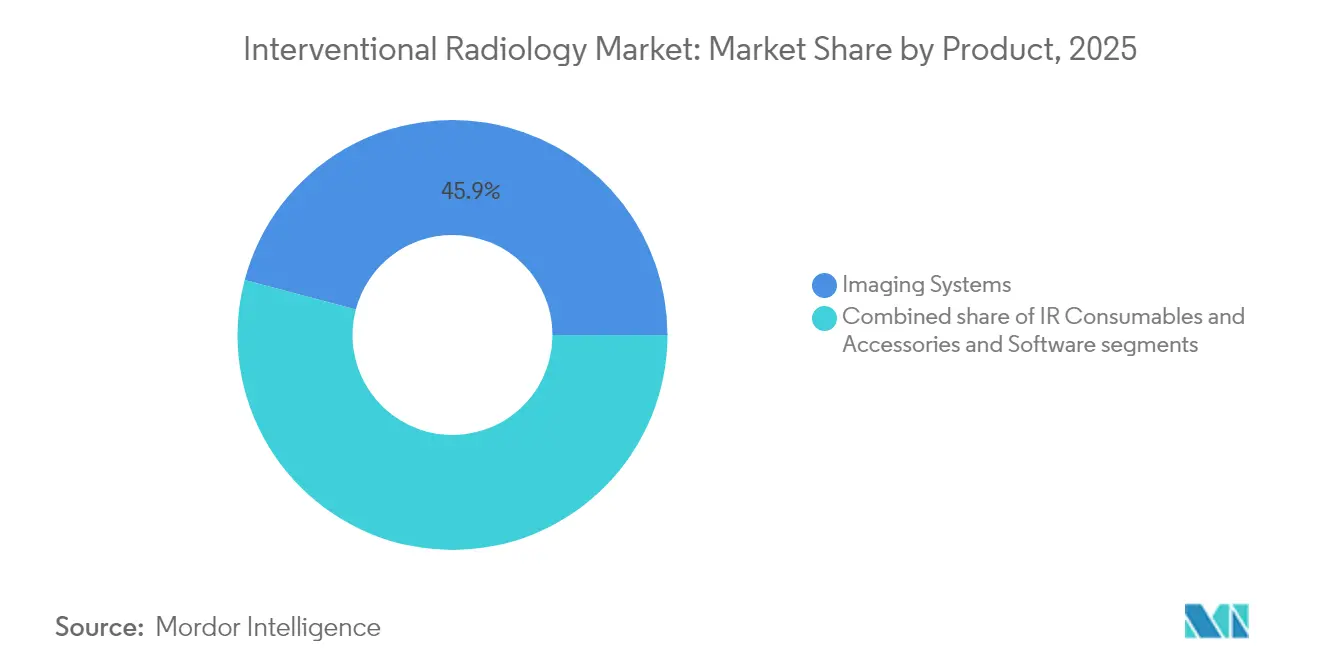

- By product, Imaging Systems led with 45.88% revenue share in 2025, while IR Consumables are projected to expand at a 7.1% CAGR through 2031.

- By procedure type, Diagnostic procedures accounted for 37.65% of the interventional radiology market share in 2025; Therapeutic procedures are advancing at a 7.32% CAGR to 2031.

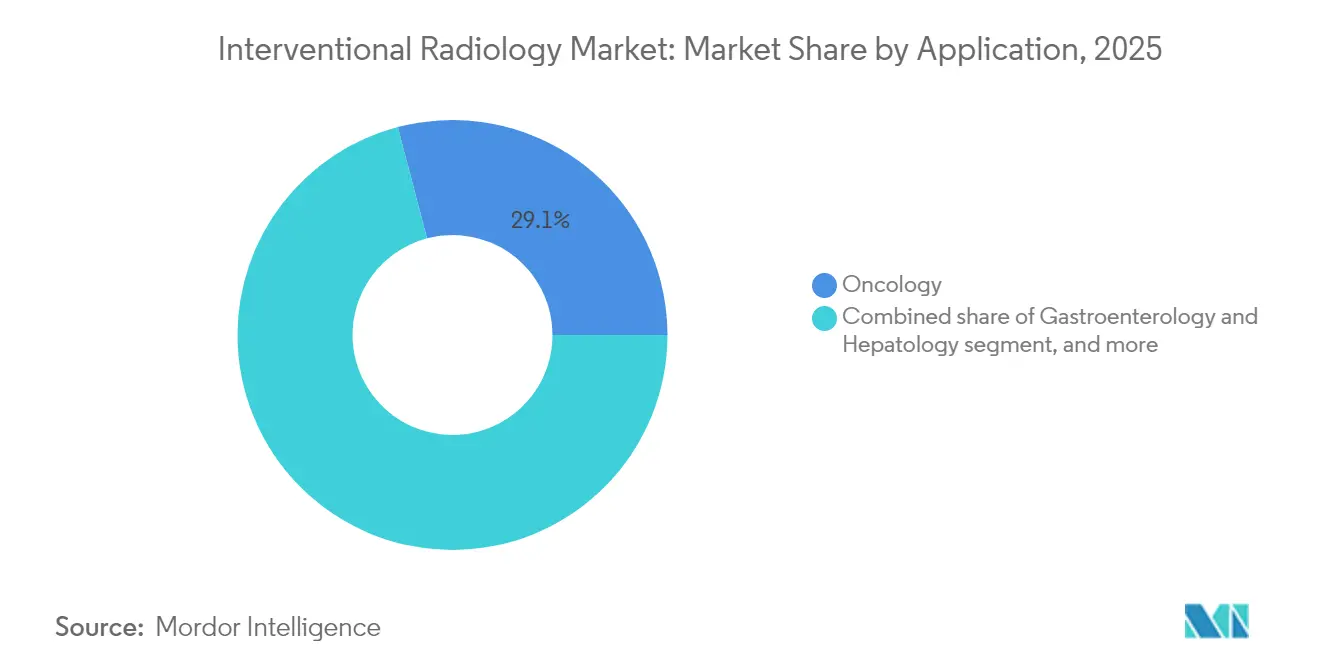

- By application, Oncology captured 29.10% of revenue in 2025, whereas Urology & Nephrology is forecast to grow at an 7.85% CAGR through 2031.

- By end-user, Hospitals retained 57.10% of revenue in 2025, yet Office-Based Labs and Imaging Centers are expanding at an 8.12% CAGR to 2031.

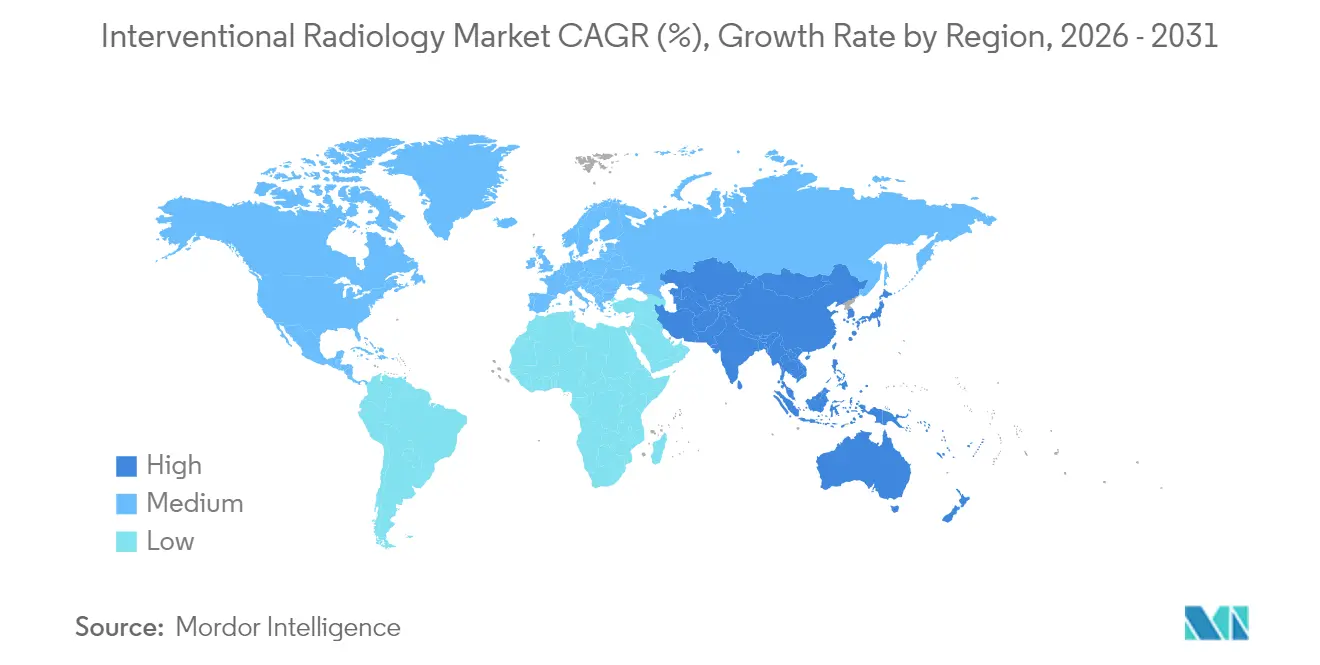

- By geography, North America held 42.60% revenue share in 2025, while Asia-Pacific is set to grow the fastest at a 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Interventional Radiology Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic and lifestyle diseases | +1.2% | North America & Europe | Long term (≥ 4 years) |

| Continuous advancements in minimally invasive imaging technologies | +1.8% | North America & Asia-Pacific | Medium term (2-4 years) |

| Expansion of interventional radiology applications across therapeutic areas | +1.1% | Developed markets worldwide | Medium term (2-4 years) |

| Shift toward outpatient and day-case treatment settings | +0.9% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Increasing capital investments in high-end imaging infrastructure | +0.7% | Asia-Pacific, Middle East & Africa | Long term (≥ 4 years) |

| Growing reimbursement support for image-guided procedures | +0.4% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic and Lifestyle Diseases

Cardiovascular and oncologic burdens elevate demand for catheter-based interventions that offer durable clinical benefits. Transcatheter aortic valve replacement alone generated nearly USD 7 billion in 2024, signaling sustained procedure uptake. Neurovascular advances such as Terumo’s WEB system achieved an 86.5% occlusion rate for ruptured aneurysms, broadening indications previously treated via open craniotomy. Peripheral artery disease therapies progress with Abbott’s FDA-cleared Esprit BTK dissolving stent, designed for more than 20 million affected Americans. As life expectancy rises, chronic comorbidities generate steady procedural pipelines, anchoring long-term growth for the interventional radiology market.

Continuous Advancements in Minimally Invasive Imaging Technologies

Artificial intelligence reduces fluoroscopy times and radiation dose, exemplified by Siemens Healthineers’ Ciartic Move, which accelerates spine and pelvic procedures by up to 50%. Robotics integrated with AI enable leadless left bundle branch pacing, first performed with Abbott’s investigational conduction system pacing platform. RapidAI’s Lumina 3D reconstructs high-quality neuro images within minutes, addressing technologist shortages and supporting time-sensitive stroke workflows. Philips deepens innovation capacity through a multi-year collaboration with NVIDIA to develop MRI foundational models that deliver zero-click scan planning. Together, these developments raise procedural accuracy and create defensible differentiation for premium imaging suites.

Expansion of Interventional Radiology Applications Across Therapeutic Areas

Radiofrequency and microwave ablation reduce the need for thyroid surgery, providing image-guided alternatives with low complication rates. Clinical trials such as GENESIS II validate genicular artery embolization for knee osteoarthritis, opening new pain-management pathways. Liver ablation boundaries widen through IntelliBlate microwave systems that display real-time ablation zones, lowering collateral tissue. The U.S. FDA’s new radiological acquisition guidance lowers regulatory friction, accelerating market entry for novel devices. This diversification enables physicians to address a wider spectrum of diseases, lifting utilization rates across the interventional radiology market.

Shift Toward Outpatient and Day-Case Treatment Settings

Cerebral angiography performed in outpatient endovascular centers validates a shift pioneered by interventional cardiology. Private-equity-backed imaging chains expand geographically, increasing patient access and optimizing cost structures through high-throughput facilities. Consumer preferences favor convenient sites, boosting outpatient imaging’s share from 40% in 2024 to 46% within three years. Integrated health campuses that co-locate imaging with primary care streamline referrals and shorten care cycles. These changes redistribute revenue across care settings and amplify demand for mobile, compact imaging platforms suited to office-based labs.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating costs of hybrid imaging suites | -0.8% | Emerging markets worldwide | Long term (≥ 4 years) |

| Stringent radiation safety regulations and compliance burdens | -0.6% | North America & Europe | Medium term (2-4 years) |

| Shortage of skilled interventional radiologists and staff | -0.5% | Global, most acute in rural and emerging regions | Medium term (2-4 years) |

| Competitive pressure from alternative endovascular specialties | -0.3% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Operating Costs of Hybrid Imaging Suites

Hybrid suites blending angiography, CT, and MRI can exceed several million USD and require specialized shielding, HVAC upgrades, and multi-modal software integration. Ongoing service contracts and staff training raise the total cost of ownership and deter adoption in budget-constrained hospitals. Siemens Healthineers mitigates these barriers through decade-long Value Partnerships that amortize modernization costs and standardize equipment fleets. Nonetheless, small facilities often pursue mergers to access financing and pooled procurement, slowing diffusion in less-developed health systems.

Stringent Radiation Safety Regulations and Compliance Burdens

The FDA’s amended Quality System Regulation harmonizes with ISO 13485, requiring device makers to align documentation, traceability, and risk management by February 2026[1]U.S. Food and Drug Administration, “Quality System Regulation Amendments,” fda.gov. Healthcare providers must also invest in dosimetry programs and periodic equipment audits, raising operational costs and prolonging facility upgrades. Although these rules enhance patient safety, they lengthen commercialization timelines and favor incumbents with established compliance infrastructures, restraining new-entrant momentum within the interventional radiology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Drive Revenue Despite Imaging Dominance

In 2025, Imaging Systems retained a 45.88% share, underscoring their foundational role in procedure planning and guidance. Continuous feature upgrades—such as AI-trained bone-removal algorithms on Siemens’ syngo DynaCT—support recurrent capital replacement cycles even as budgets tighten. IR Consumables, however, exhibit a 7.1% CAGR through 2031, reflecting their recurring revenue advantage as case volumes climb. Single-use catheters and embolization coils reduce cross-contamination risks and streamline inventory control, making them attractive for outpatient labs where turnover is high. The interventional radiology market size for consumables is projected to broaden swiftly as therapeutic complexity rises.

Accessories and workflow software outpace hardware growth because cloud analytics lower modality downtime and optimize scheduling. Philips’ helium-free BlueSeal MRI saves nearly 40 MWh annually per unit, illustrating how eco-efficiency complements clinical performance. Fluoroscopy systems that bundle AI-enabled dose monitoring meet tightening safety mandates and appeal to mid-tier hospitals. Overall, mature imaging infrastructure sets the stage for high-margin disposable uptake, driving profitable expansion across the interventional radiology market.

By Procedure Type: Therapeutic Growth Outpaces Diagnostic Foundation

Therapeutic procedures are advancing at a 7.32% CAGR, propelled by device breakthroughs like Merit Medical’s Wrapsody cell-impermeable endoprosthesis that achieved strong primary patency for hemodialysis access. Angioplasty and stenting benefit from absorbable scaffolds that support vessel healing while ensuring drug delivery, such as Abbott’s Esprit BTK platform. Ablation technology progression yields predictable lesion boundaries and shrinks collateral injury, broadening oncology and pain-management indications. Consequently, the interventional radiology market size attributed to therapeutic services is projected to reach USD 26.85 billion by 2031 at segment level.

Diagnostic procedures hold a 37.65% share, providing essential imaging roadmaps for interventionists but delivering lower revenue per case. Nevertheless, innovations in cone-beam CT and AI-assisted angiography enhance diagnostic accuracy, indirectly supporting therapeutic expansion. Biopsy and drainage remain vital for oncologic staging and infection control. The enduring diagnostic foundation ensures a steady flow of patients into the therapeutic pipeline, sustaining growth momentum in the broader interventional radiology market.

By Application: Oncology Leadership Challenged By Urology Surge

Oncology remains the largest application, owning 29.10% revenue in 2025 via liver chemoembolization and tumor ablation that demonstrate superior survival outcomes compared with surgery in select patient cohorts. Device innovation—such as precision microcatheters and drug-eluting beads—widens the scope to pancreatic and renal malignancies. Yet Urology & Nephrology is scaling fastest at an 7.85% CAGR, buoyed by guideline-backed prostatic artery embolization that offers durable symptom relief for benign prostatic hyperplasia. FDA approval of ultrasound renal denervation for hypertension further expands the addressable patient base.

Cardiology interventions persist in structural heart and pulmonary embolism management, while gastroenterology cases leverage portal vein recanalization and biliary drainage to defer surgical interventions. Musculoskeletal and pain-management procedures round out emerging niches, underscoring the broadening therapeutic reach of the interventional radiology industry across diverse disease states.

By End-User: Outpatient Facilities Challenge Hospital Dominance

Hospitals control 57.10% of 2025 revenue due to intensive care capabilities and readiness for emergent complications. They remain central for multi-disciplinary tumor boards and combined surgical-interventional cases. However, Office-Based Labs (OBLs) and specialized Imaging Centers are expanding at an 8.12% CAGR, aided by lower overhead, convenient locations, and tailored workflows. The interventional radiology market size for OBLs is on track to exceed USD 9.85 billion by 2031 as reimbursement parity for select procedures levels the economic playing field.

Ambulatory Surgical Centers exploit simplified credentialing to adopt intricate interventions such as outpatient cerebral angiography with safety profiles comparable to inpatient settings. Health systems respond through spoke-and-hub networks that anchor complex cases in flagship hospitals while channeling routine interventions to satellite centers, preserving market reach amid the outpatient shift.

Geography Analysis

North America commanded 42.60% revenue in 2025, supported by established clinical guidelines, high device penetration, and robust R&D commitments including Siemens Healthineers’ USD 150 million facility expansion in the United States. Payment pressures loom as Medicare enacts a 2.83% fee schedule reduction and a projected 4% cut in interventional radiology reimbursements, spurring provider investment in cost-efficient outpatient capacity. Regulatory initiatives such as the FDA’s Transitional Coverage for Emerging Technologies pathway expedite market uptake for breakthrough devices, sustaining innovation flow despite fiscal tightening.

Asia-Pacific registers the fastest growth at a 6.05% CAGR, fueled by large unmet procedural needs, urban hospital build-outs, and joint ventures. Inari Medical’s partnership with 6 Dimensions Capital accelerates commercialization of thrombectomy devices in Greater China, illustrating foreign-domestic collaboration that localizes advanced therapies. Governments prioritize imaging infrastructure and physician training to curb outbound medical tourism, while public-private alliances leverage cloud platforms to scale AI tools across regional networks.

Europe maintains stable expansion anchored by tight device-safety standards and strong university hospital networks. Philips led European Patent Office filings with 594 medical technology applications in 2024, reinforcing the region’s innovation reputation. Eastern European systems allocate European Union cohesion funds to upgrade angiography labs, boosting procedure capacity. The Middle East & Africa and South America remain nascent but show accelerating adoption as training initiatives like Tanzania’s Road2IR program complete more than 1,500 procedures with high success rates. Multinational OEMs tailor financing packages to penetrate these value-conscious markets, diversifying revenue streams across the global interventional radiology market.

Competitive Landscape

The landscape is moderately consolidated, with imaging conglomerates, catheter specialists, and emerging robotic firms competing on integrated ecosystems. Siemens Healthineers grew Advanced Therapies revenue by 8.0% in 2025 and secured a 10-year modernization partnership with Tower Health, reinforcing its platform approach to imaging, software, and service bundles. Philips invests heavily in AI collaboration, targeting seamless workflows from acquisition to reporting, while emphasizing helium-free MRI to lower lifecycle costs.

Strategic M&A reshapes market boundaries. Stryker’s USD 4.9 billion acquisition of Inari Medical grants immediate entry to high-growth venous thrombectomy and expands its vascular franchise. Boston Scientific broadened its liver-oncology armamentarium by acquiring Intera Oncology devices that deliver hepatic arterial infusion chemotherapy. Robotics innovators pursue niche disruption; Stereotaxis filed for FDA clearance of its EMAGIN catheter, aiming to integrate magnetic navigation with 3D imaging for endovascular procedures.

Patent portfolios remain critical moats. Philips controls 50,500 active patent rights globally, securing freedom to operate across AI, MR gradient coils, and dose-optimization algorithms. At the same time, small device firms leverage faster iteration to target specific indications, often partnering with large OEMs for commercialization scale. Competitive intensity is expected to rise as reimbursement models favor differentiated clinical outcomes that justify premium pricing, compelling all players to accelerate innovation cycles throughout the interventional radiology market.

Interventional Radiology Industry Leaders

Shimadzu Corporation

GE Healthcare

Koninklijke Philips NV

Siemens Healthineers AG

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Stryker completed its USD 4.9 billion acquisition of Inari Medical, entering the peripheral vascular space focused on venous thromboembolism treatment technologies.

- May 2025: Abbott obtained FDA approval for the Tendyne transcatheter mitral valve replacement system, the first device to replace calcified mitral valves without surgery.

- May 2025: Siemens Healthineers invested USD 150 million in new and expanded U.S. facilities to enhance access to imaging and minimally invasive therapies.

- May 2025: Koninklijke Philips NV announced a collaboration with NVIDIA to develop AI models that automate MRI scan planning and image enhancement

- April 2025: RadNet closed its USD 103 million all-stock acquisition of iCAD, expanding AI capability in breast and brain imaging.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the interventional radiology (IR) market as the value generated when physicians perform minimally invasive diagnostic or therapeutic procedures under real-time X-ray, ultrasound, CT, or MRI guidance. Revenues include dedicated imaging suites, catheters, guidewires, balloons, stents, embolization devices, and the workstation software that ties them together. According to Mordor Intelligence, procedure fees, general-purpose diagnostic scanners, and pure service contracts sit outside this financial scope, so they are not counted here.

Scope Exclusions: Stand-alone diagnostic imaging devices, teleradiology services, and non-image-guided catheter therapies are excluded.

Segmentation Overview

- By Product

- Imaging Systems

- Angiography Systems

- Fluoroscopy Systems

- CT Scanners

- MRI Systems

- IR Consumables

- Catheters & Guidewires

- Balloon & Stent Systems

- Embolization & Thrombus Devices

- Accessories & Software

- Imaging Systems

- By Procedure Type

- Diagnostic

- Angiography

- Biopsy & Drainage

- Therapeutic

- Angioplasty & Stenting

- Embolization

- Ablation

- Diagnostic

- By Application

- Cardiology

- Oncology

- Gastroenterology & Hepatology

- Urology & Nephrology

- Other Applications

- By End-user

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Office-Based Labs (OBLs) & Imaging Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with radiologists, cath-lab nurses, biomedical engineers, and payer administrators across North America, Europe, Asia-Pacific, and the Gulf to sense-check adoption curves, ASP movements, and outpatient migration rates. These interviews, combined with a short web survey of ambulatory centers, helped us close data gaps and validate model assumptions.

Desk Research

We began with public sources such as WHO chronic-disease registries, OECD Health Accounts, the Society of Interventional Radiology annual census, and country-level hospital discharge datasets, which anchor disease prevalence, procedure volumes, and equipment installed base. Device shipment flows were screened through customs dashboards (UN Comtrade, Volza) and company 10-K filings, while Questel patent landscapes helped us map upcoming modality upgrades. Subscription resources from Dow Jones Factiva and D&B Hoovers then provided timely revenue splits for leading vendors.

Because open data in some regions remain thin, our analysts supplemented the above with peer-reviewed journals, government procurement portals, and press releases that detail capital purchases or guideline changes. The sources listed are illustrative only; many more were referenced throughout our desk work.

Market-Sizing & Forecasting

A top-down construct converts national angiography, ablation, and embolization procedure counts into potential demand pools, which are then stress-tested with selective bottom-up roll-ups of supplier shipments and sampled ASP × volume checks. Key variables in the model include oncology and cardiovascular prevalence trends, installed angiography-suite growth, disposable-per-procedure ratios, average length of stay shifts, and currency movements. Results are forecast through 2030 using multivariate regression with exponential smoothing overlays. Coefficient ranges were aligned with expert consensus to capture plausible technology and reimbursement scenarios.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance scans, peer analyst cross-checks, and final sector-lead approval. We refresh the file annually and reopen it mid-cycle if regulatory or recall events change demand signals. A brief audit is run again just before delivery.

Why Mordor's Interventional Radiology Market Baseline Commands Reliability

Published estimates often diverge because firms pick different revenue buckets, growth levers, and refresh cadences. Our disciplined scope selection and annual re-benchmarking reduce that noise for decision-makers.

Key gap drivers include whether disposables beyond the cath-lab are folded in, how aggressively ASP inflation is layered, and if diagnostic-only scanners are lumped with IR systems. Our base year reflects the narrow, procedure-linked universe that hospitals budget for, whereas some publishers widen definitions or extrapolate earlier trends without fresh validation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 28.55 B (2025) | Mordor Intelligence | - |

| USD 32.95 B (2025) | Global Consultancy A | Adds vascular implants and recovery-room disposables, and applies steeper ASP escalation |

| USD 28.83 B (2025) | Industry Analyst B | Counts stand-alone diagnostic imaging revenue as part of IR scope |

These comparisons show that when scope creep or untested inflation multipliers enter the equation, totals swing widely. By anchoring figures to clearly traceable variables and repeating our cross-checks every year, Mordor delivers a balanced, transparent baseline that users can replicate and trust.

Key Questions Answered in the Report

What is the current value of the interventional radiology market?

The market is valued at USD 30.15 billion in 2026 and is forecast to reach USD 39.65 billion by 2031.

Which product segment is growing the fastest?

IR Consumables are expanding at a 7.1% CAGR as therapeutic case volumes rise and single-use devices gain preference.

Why are outpatient facilities gaining market share?

Lower overhead costs, patient convenience, and reimbursement shifts are driving procedures from hospitals to Office-Based Labs and Imaging Centers where growth is 8.12% CAGR.

Which geographic region offers the highest growth potential?

Asia-Pacific leads with a 6.05% CAGR due to infrastructure investments, large patient populations, and strategic joint ventures.

How are AI and robotics influencing the interventional radiology industry?

AI shortens procedure times and improves precision, while robotics enables complex catheter navigation, together enhancing outcomes and differentiating premium systems.

What are the major challenges facing new entrants?

High capital costs for hybrid suites and stringent radiation safety regulations increase barriers, favoring established players with strong compliance capabilities.

Page last updated on: