Market Size of Interventional Oncology Devices Industry

| Study Period | 2019 - 2029 |

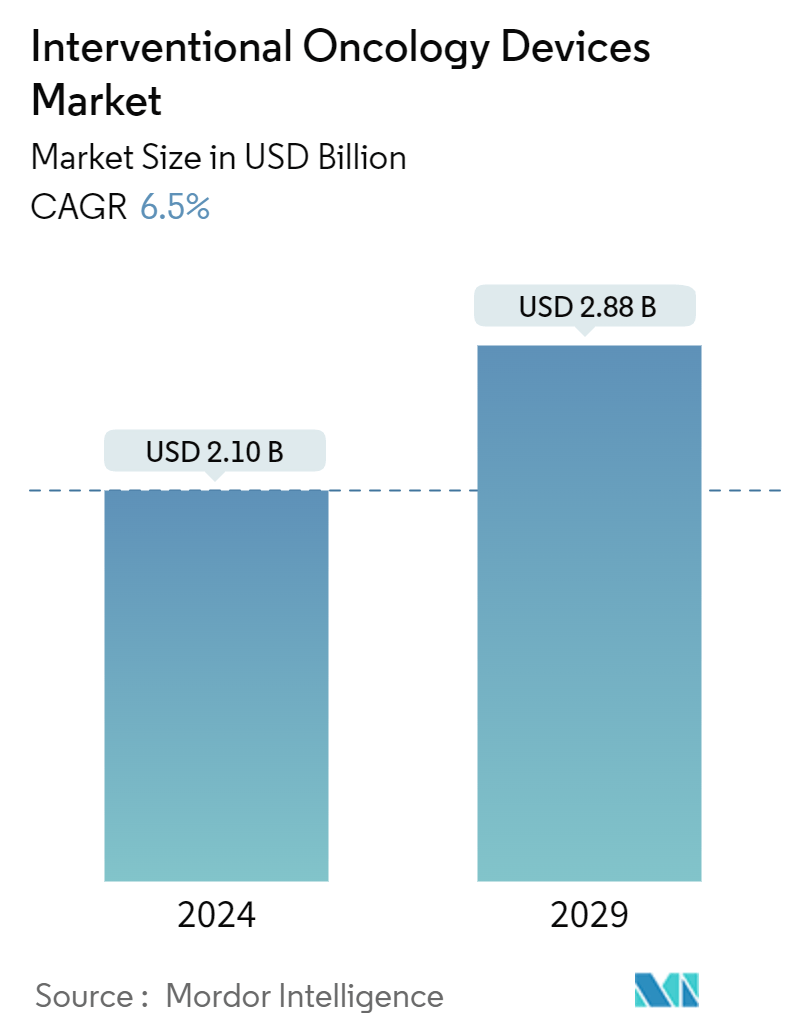

| Market Size (2024) | USD 2.10 Billion |

| Market Size (2029) | USD 2.88 Billion |

| CAGR (2024 - 2029) | 6.50 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Interventional Oncology Market Analysis

The Interventional Oncology Devices Market size is estimated at USD 2.10 billion in 2024, and is expected to reach USD 2.88 billion by 2029, growing at a CAGR of 6.5% during the forecast period (2024-2029).

COVID-19 had a significant impact on the growth of the market. The COVID-19 pandemic affected healthcare systems globally and resulted in the interruption of usual care in many healthcare facilities, exposing vulnerable patients with cancer to significant risks. For instance, according to an article published by the Lancet Oncology in May 2021, a study was conducted in India which showed that the COVID-19 pandemic had a considerable impact on the delivery of oncology services and the long-term effect of cessation of cancer screening, delayed hospital visits on cancer stage migration and outcomes were substantial. Thus, the lack of cancer treatment during the pandemic significantly impacted the market's growth. However, in the post-pandemic period, cancer care has regained traction. Hence, the market studied is expected to have stable growth during the forecast period of the study.

The major factors accounting for the growth of the market include the increase in cancer incidence rate worldwide, high preference for minimally invasive procedures, augmented funding from the government in developed countries, and favorable reimbursement scenario for interventional oncology treatment. According to the American Cancer Society, 1.9 million new cancer cases are expected to occur in the United States in 2022. Furthermore, according to the data updated by WHO in February 2022, the most common cancers around the world are breast, lung, colon and rectum, and prostate cancers. Cancer-causing infections, such as human papillomavirus (HPV) and hepatitis, are also responsible for approximately 30% of cancer cases in low- and lower-middle-income countries. Therefore, an increase in the incidence rate of cancer around the world drives the growth of the interventional oncology devices market during the forecast period.

Additionally, the increasing product developments by key market players are expected to drive the growth of the market. For instance, in November 2021 Fluidx Medical Technology presented the data supporting the potential for oncology drug delivery with the company's next generation, doxorubicin-loaded GPX embolic device.

Thus the above-mentioned factors are expected to drive the growth of the market during the forecast period. However, the dearth of trained interventional oncologists, clinical evidence for localized treatment regions, and stringent regulations for medical devices are expected to restrain the growth of the market.

Interventional Oncology Industry Segmentation

Interventional oncology deals with the treatment of various types of cancer using targeted, minimally invasive procedures performed under image guidance. As minimally invasive procedures are less painful and low-risk than other traditional surgeries, interventional oncology is gaining a lot of importance in treating cancer.

The Interventional Oncology Devices Market is Segmented by Product Type (Ablation Devices (Microwave ablation, Radiofrequency ablation, Cryoablation, and Other Product Types) and Embolization Devices (Microcatheters, Guidewires, and Others), Cancer Type (Lung Cancer, Breast Cancer, Liver Cancer, Kidney Cancer, Prostate Cancer, and Other Cancer Types), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers value (in USD million) for the above segments.

| By Product Type | ||||||

| ||||||

| Embolization Device | ||||||

| Microcatheters | ||||||

| Guidewires | ||||||

| Other Embolization Devices |

| By Cancer Type | |

| Lung cancer | |

| Breast Cancer | |

| Liver Cancer | |

| Kidney Cancer | |

| Prostate Cancer | |

| Other Cancer Types |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Interventional Oncology Devices Market Size Summary

The interventional oncology market is poised for stable growth, driven by an increasing global incidence of cancer and a rising preference for minimally invasive procedures. The market's expansion is supported by augmented government funding in developed regions and a favorable reimbursement landscape for interventional oncology treatments. The COVID-19 pandemic had a significant impact on the market, disrupting cancer care and highlighting the importance of timely treatment. However, the post-pandemic recovery has seen a resurgence in cancer care, contributing to the market's growth trajectory. Key players in the industry are actively developing innovative products, such as Fluidx Medical Technology's doxorubicin-loaded GPX embolic device, which are expected to further propel market expansion. Despite these positive trends, challenges such as a shortage of trained interventional oncologists and stringent medical device regulations may pose constraints to market growth.

The breast cancer segment within the interventional oncology market is anticipated to experience significant growth due to the increasing incidence of the disease and ongoing product launches. The market is characterized by the introduction of innovative solutions, such as IceCube Medical Ltd's ProSense, a liquid-nitrogen-based cryoablation system, which received Breakthrough Device designation from the FDA. North America is expected to maintain a substantial market share, driven by a high cancer incidence rate, advancements in medical imaging technology, and significant investments from key market players. The region's market growth is further supported by the rising prevalence of minimally invasive procedures and the increasing demand for surgical interventions. Major industry players, including Boston Scientific Corporation, Medtronic plc, and Merit Medical Systems Inc., are actively contributing to the competitive landscape, with ongoing product developments and strategic investments aimed at enhancing market presence.

Interventional Oncology Devices Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Perpetual Increase in the Incidence Rate of Cancers Worldwide

-

1.2.2 High Preference for Minimally Invasive Procedures

-

1.2.3 Augmented Funding from the Government in the Developed Countries

-

1.2.4 Favorable Reimbursement Scenario for Interventional Oncology Treatment

-

-

1.3 Market Restraints

-

1.3.1 Financial Burden on the Companies due to Product Recall

-

1.3.2 Dearth of Trained Interventional Oncologists and Clinical Evidence for Localized Treatment Region

-

1.3.3 Stringent Regulations for Medical Devices

-

-

1.4 Porter's Five Force Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value in USD million)

-

2.1 By Product Type

-

2.1.1 Ablation Devices

-

2.1.1.1 Microwave ablation

-

2.1.1.2 Radiofrequency ablation

-

2.1.1.3 Cryoablation

-

2.1.1.4 Other Product Types

-

-

2.1.2 Embolization Device

-

2.1.3 Microcatheters

-

2.1.4 Guidewires

-

2.1.5 Other Embolization Devices

-

-

2.2 By Cancer Type

-

2.2.1 Lung cancer

-

2.2.2 Breast Cancer

-

2.2.3 Liver Cancer

-

2.2.4 Kidney Cancer

-

2.2.5 Prostate Cancer

-

2.2.6 Other Cancer Types

-

-

2.3 Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

2.3.1.3 Mexico

-

-

2.3.2 Europe

-

2.3.2.1 Germany

-

2.3.2.2 United Kingdom

-

2.3.2.3 France

-

2.3.2.4 Italy

-

2.3.2.5 Spain

-

2.3.2.6 Rest of Europe

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 Japan

-

2.3.3.3 India

-

2.3.3.4 Australia

-

2.3.3.5 South Korea

-

2.3.3.6 Rest of Asia-Pacific

-

-

2.3.4 Middle East and Africa

-

2.3.4.1 GCC

-

2.3.4.2 South Africa

-

2.3.4.3 Rest of Middle East and Africa

-

-

2.3.5 South America

-

2.3.5.1 Brazil

-

2.3.5.2 Argentina

-

2.3.5.3 Rest of South America

-

-

-

Interventional Oncology Devices Market Size FAQs

How big is the Interventional Oncology Devices Market?

The Interventional Oncology Devices Market size is expected to reach USD 2.10 billion in 2024 and grow at a CAGR of 6.5% to reach USD 2.88 billion by 2029.

What is the current Interventional Oncology Devices Market size?

In 2024, the Interventional Oncology Devices Market size is expected to reach USD 2.10 billion.