| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 2.24 Billion |

| Market Size (2030) | USD 3.06 Billion |

| CAGR (2025 - 2030) | 6.50 % |

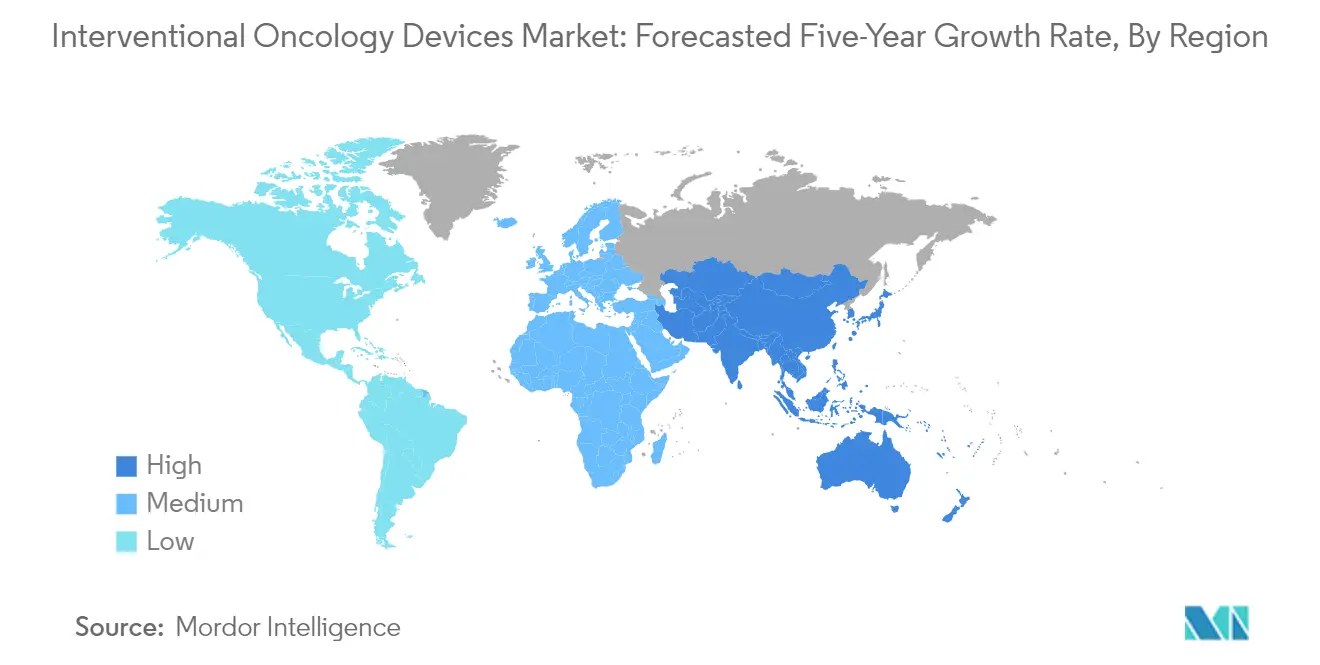

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

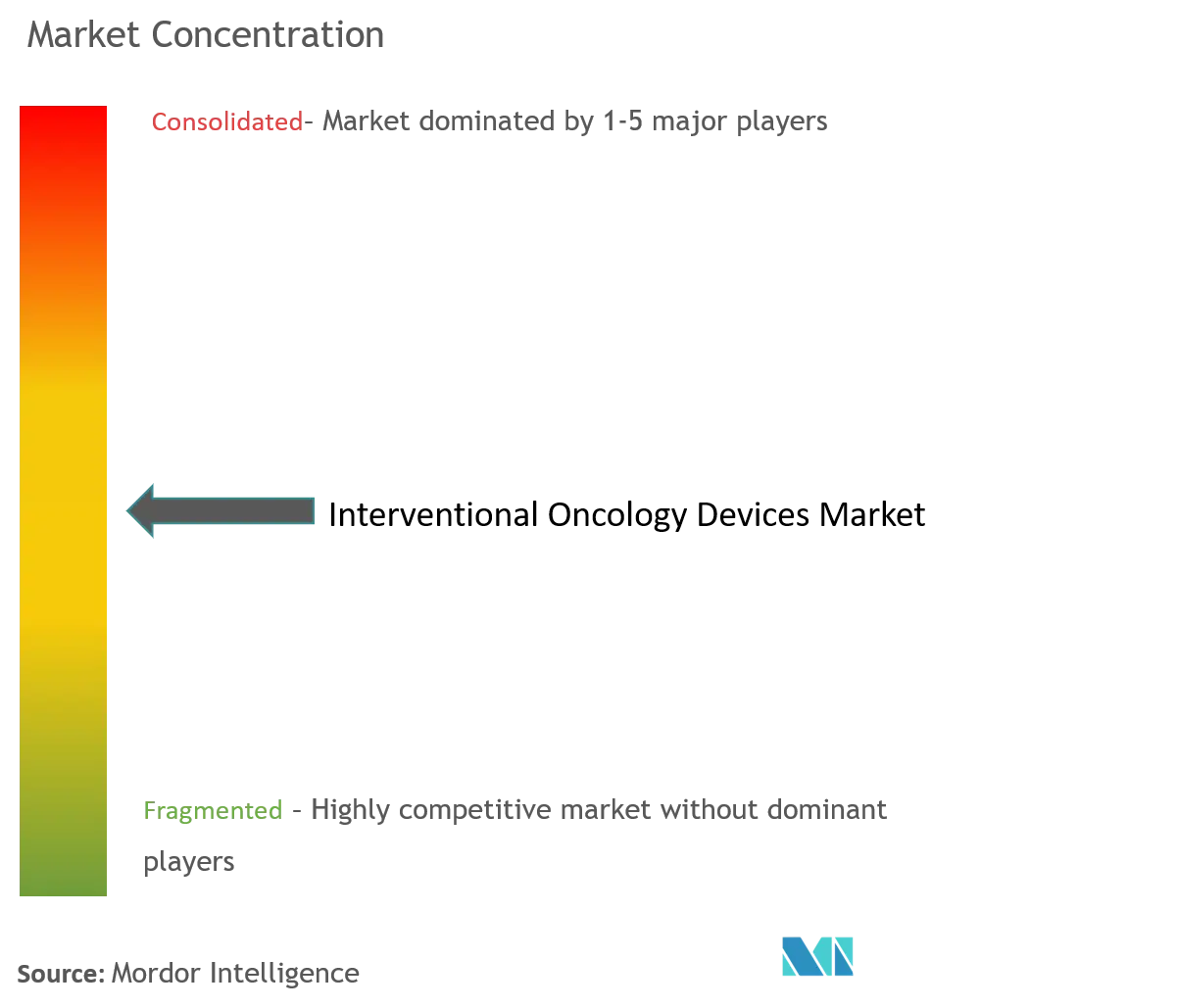

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Interventional Oncology Market Analysis

The Interventional Oncology Devices Market size is estimated at USD 2.24 billion in 2025, and is expected to reach USD 3.06 billion by 2030, at a CAGR of 6.5% during the forecast period (2025-2030).

The interventional oncology devices market is experiencing significant technological advancements, particularly in the integration of artificial intelligence and precision medicine approaches. These developments are revolutionizing patient-specific treatments through personalized screening, diagnosis, staging, risk assessment, and automated neoplastic tissue compartmentalization. According to the World Health Organization's 2022 data, the most prevalent cancers globally remain breast, lung, colon and rectum, and prostate cancers, highlighting the critical need for advanced interventional oncology products across multiple cancer types. The industry is witnessing a notable shift toward multi-parametric characterization and classification systems, enabling more accurate and targeted treatment approaches.

The market landscape is being transformed by breakthrough innovations in ablation technologies and delivery systems. In May 2023, Varian, a Siemens Healthineers company, introduced the Isolis cryoprobe, a single-use disposable device designed for CryoCare systems, representing a significant advancement in procedural efficiency and precision for cryoablation. This innovation trend is further exemplified by the emergence of directional microwave ablation (MWA) technology, which offers unprecedented spatial control of thermal ablation zones, particularly beneficial for challenging tumor cases and expanding clinical applications of thermal ablation as a minimally invasive treatment option in the interventional oncology market.

The industry is witnessing substantial investment in research and development, particularly in combining interventional approaches with emerging therapies. In June 2023, the Philips-coordinated IMAGIO consortium received a EUR 24 million grant from the Innovative Health Initiative for research into minimally invasive cancer treatments, focusing on lung cancer, liver cancer, and soft tissue sarcomas. This collaboration, involving approximately 30 partners and leading European hospitals, demonstrates the industry's commitment to advancing oncology medical devices through multi-stakeholder partnerships.

The market is characterized by increasing regional expansion and accessibility initiatives, particularly in emerging markets. For instance, in June 2023, IceCure Medical expanded its presence in India through the introduction of ProSense, a cryoablation system providing ultrasound/CT probe-guided treatment for tumor elimination. This expansion trend is particularly significant given that cancer-causing infections account for approximately 30% of cancer cases in low- and lower-middle-income countries, according to recent WHO data, highlighting the growing need for advanced interventional oncology devices in developing regions.

Interventional Oncology Market Trends

Perpetual Increase in the Incidence Rate of Cancers Worldwide

The growing burden of cancer cases across the globe is one of the crucial health concerns witnessed by many countries, driving significant demand for the interventional oncology devices market. According to the American Cancer Society's 2023 update, about 1.93 million new cancer cases are estimated to be reported in 2023 compared to 1.89 million cases in 2021 in the United States. The rising prevalence of risk factors like obesity is further accelerating cancer incidence rates. For instance, according to the Centers for Disease Control and Prevention's 2023 update, about 684,000 cases of obesity-linked cancers are reported every year, with breast cancer after menopause being the most prevalent.

The increasing burden spans across multiple cancer types, creating sustained demand for interventional procedures. For instance, according to Breastcancer.org data published in January 2022, more than 3.8 million women are living with a history of breast cancer in the United States. Additionally, prostate cancer applications often utilize trans-arterial embolization techniques, and the incidence continues to rise - with 96,400 prostate cancer cases diagnosed in Japan in 2022 compared to 95,400 in 2021. The growing prevalence of various cancer types necessitates advanced oncology medical devices solutions, driving market expansion through increased adoption of ablation, embolization, and other minimally invasive procedures.

Understand The Key Trends Shaping This Market

Download PDF

High Preference for Minimally Invasive Procedures

Minimally invasive surgical (MIS) procedures are increasingly preferred over conventional procedures due to their significant advantages, including less post-operative pain, fewer major operative and postoperative complications, faster recovery times, less scarring, reduced stress on the immune system, and smaller incisions. The emergence of advanced minimally invasive procedures, such as targeted biopsy (TB) and focal therapy (FT), has revolutionized the diagnosis and treatment of localized prostate cancer. According to research published in June 2022, focal therapy is demonstrating oncological efficacy in clinical trial settings as an evolving and promising alternative for definitive treatments.

Recent technological developments have further enhanced the capabilities of minimally invasive interventional procedures. For instance, in April 2023, Ethicon, a Johnson & Johnson MedTech Company, initiated the first North American patient treatment in its IDE clinical trial using the NEUWAVE FLEX Microwave Ablation System guided by the MONARCH Platform. Similarly, in February 2023, the first patient in the USA was treated with the MUSE breast cancer ablation system, a technology developed at the University of Utah equipped to destroy breast tumors without surgery. These advancements continue to drive the adoption of minimally invasive approaches across various cancer treatments, contributing to the growth of the interventional oncology market.

Augmented Funding from the Government in Developed Countries

Government authorities are significantly increasing funding and investments to develop advanced cancer therapies and medical devices. In June 2023, six countries pledged to support a new International Atomic Energy Agency (IAEA) initiative – Rays of Hope – with funding of more than EUR 9 million to address the global gap in cancer care access. This funding will be utilized for purchasing life-saving equipment, enhancing staff skills, and transferring knowledge necessary for preventing cancer deaths. Additionally, in June 2023, the Philips-coordinated IMAGIO consortium received a EUR 24 million Innovative Health Initiative grant to improve clinical outcomes with interventional oncology innovations focused on lung cancer, liver cancer, and soft tissue sarcomas.

The United States government has also demonstrated a strong commitment through substantial funding initiatives. Under the Cancer Moonshot program, USD 1.7 billion was allocated to the Department of Health and Human Services to support dedicated cancer activities across multiple agencies, including the National Cancer Institute, Centers for Disease Control and Prevention, Food and Drug Administration, and Health Resources and Services Administration. The total investment includes USD 7.8 billion for NCI, plus expected critical contributions from USD 2.5 billion for ARPA-H to help deliver on Moonshot goals of reducing cancer death rates by at least 50% over the next 25 years.

Favorable Reimbursement Scenario for Interventional Oncology Treatment

The availability of favorable reimbursement policies for cancer treatment is driving the adoption of interventional oncology devices, as patients can benefit from advanced treatment options without significant financial burden. In many European Union countries, medical device reimbursements are well established. According to the Health Technology Assessment and Reimbursement of Medical Devices report published in 2023, France's Haute Autorité de Santé assesses medical devices for individual use after CE marking approval, with most devices covered by Diagnosis Related Group funding via mandatory health insurance. Innovative or expensive devices must be enlisted on the French LPPR for reimbursement by mandatory health insurance.

Major companies are also actively supporting reimbursement initiatives to increase device accessibility. For instance, Boston Scientific has contracted with the Pinnacle Health Group to assist with coding, coverage, and payment activities related to interventional oncology ablation treatment. The reimbursement support helps providers with coding options and tools, current coverage policy information, reviews of inadequate reimbursement or denials, and patient information requests. Additionally, government schemes like India's Rashtriya Arogya Nidhi and the Health Minister's Cancer Patient Fund provide financial assistance to cancer patients who cannot afford treatment, covering various interventional procedures including radiotherapy, Gamma Knife surgery, and other advanced therapies.

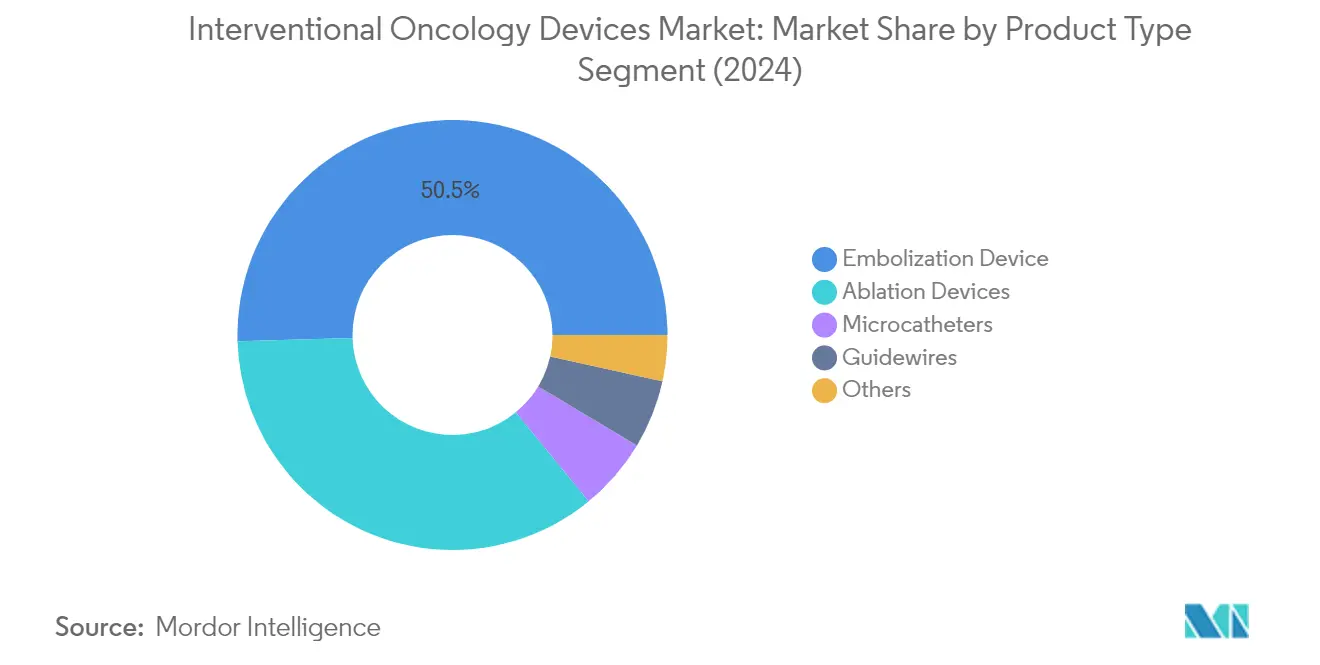

Segment Analysis: By Product Type

Embolization Device Segment in Interventional Oncology Devices Market

The embolization device segment continues to dominate the interventional oncology devices market, commanding approximately 50% of the total market share in 2024. This significant market position is primarily driven by the increased adoption of embolization devices due to their advantages in cancer therapies, particularly in treating liver cancer and other solid tumors. The segment's prominence is further strengthened by the availability of both radioembolic and non-radioembolic agents, offering healthcare providers a comprehensive range of treatment options. The growing preference for minimally invasive procedures and the proven efficacy of embolization techniques in targeting specific tumor sites have contributed to maintaining this segment's leadership position in the market.

Microcatheters Segment in Interventional Oncology Devices Market

The microcatheters segment is emerging as the fastest-growing segment in the interventional oncology devices market, with an expected growth rate of approximately 8% during 2024-2029. This robust growth is attributed to the increasing adoption of microcatheters in super-selective tumor targeting and their crucial role in delivering therapeutic agents precisely to tumor sites. The segment's growth is further propelled by technological advancements in microcatheter design, enabling better navigation through complex vasculature and improved treatment outcomes. The rising demand for targeted drug delivery systems and the expanding applications of microcatheters in various cancer treatments are also contributing to this segment's accelerated growth trajectory.

Remaining Segments in Product Type

The remaining segments in the interventional oncology devices market include ablation devices, guidewires, and other product types, each playing vital roles in cancer treatment procedures. Ablation devices represent a significant portion of the market, offering various technologies such as radiofrequency, microwave, and cryoablation for tumor destruction. Guidewires are essential components in interventional procedures, facilitating precise navigation and device placement. Other product types encompass various supporting devices and accessories that complement the primary interventional oncology procedures. These segments collectively contribute to the comprehensive treatment approach in interventional oncology, providing physicians with a complete toolkit for minimally invasive cancer treatments.

Segment Analysis: By Cancer Type

Liver Cancer Segment in Interventional Oncology Devices Market

The liver cancer segment dominates the interventional oncology devices market, commanding approximately 33% of the total market share in 2024. This significant market position is primarily driven by the increasing adoption of embolization devices due to their advantages in liver cancer therapies. The segment's growth is further supported by the rising success rate of interventional oncology devices in liver cancer treatment, particularly in cases of hepatocellular carcinoma (HCC) and metastatic liver cancer. The availability of various technologies such as microwave ablation devices for interventional oncology, which have several advantages compared to traditional RF ablation for liver tumors, contributes to this segment's dominance. Additionally, the increasing focus on developing specialized devices for liver cancer treatment by major market players and ongoing clinical trials evaluating new therapeutic approaches continue to strengthen this segment's market position.

Lung Cancer Segment in Interventional Oncology Devices Market

The lung cancer segment is emerging as the fastest-growing segment in the interventional oncology devices market, with a projected growth rate of approximately 8% from 2024 to 2029. This remarkable growth is attributed to the increasing adoption of minimally invasive procedures for lung cancer treatment and the development of advanced ablation technologies specifically designed for pulmonary tumors. The segment's growth is further accelerated by technological advancements in navigation bronchoscopy-guided procedures and the introduction of innovative ablation systems designed specifically for lung cancer treatment. The rising success rates of interventional procedures in treating both primary and metastatic lung tumors, coupled with the growing preference for minimally invasive alternatives to traditional surgery, continue to drive this segment's rapid expansion.

Remaining Segments in Cancer Type Segmentation

The remaining segments in the interventional oncology devices market include kidney cancer, breast cancer, prostate cancer, and other cancer types, each contributing significantly to the market's diversity. The kidney cancer segment shows strong potential due to the increasing adoption of ablation techniques for renal tumors. The breast cancer segment benefits from the growing acceptance of minimally invasive procedures and the development of specialized interventional devices for breast tumor treatment. The prostate cancer segment is driven by innovations in focal therapy and the rising demand for minimally invasive treatment options. Other cancer types, including bone, soft tissue, and pancreatic cancers, collectively represent an important market segment as interventional oncology techniques continue to expand their applications across various cancer types.

Interventional Oncology Devices Market Geography Segment Analysis

Interventional Oncology Devices Market in North America

The North American interventional oncology devices market demonstrates robust growth driven by advanced healthcare infrastructure, high adoption of minimally invasive procedures, and a strong presence of key market players. The United States leads the regional market, followed by Canada and Mexico, with these countries showing varying degrees of market maturity and growth potential. The region benefits from favorable reimbursement policies, increased healthcare spending, and continuous technological advancements in interventional oncology procedures.

Interventional Oncology Devices Market in the United States

The United States dominates the North American market, holding approximately 89% of the regional market share in 2024. The country's market leadership is attributed to its well-established healthcare system, presence of major market players, and high prevalence of cancer cases requiring interventional oncology devices. The US market benefits from extensive research and development activities, with numerous clinical trials evaluating new interventional oncology products. The country's robust healthcare infrastructure and increasing adoption of advanced minimally invasive procedures continue to drive market growth.

Interventional Oncology Devices Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of around 8% from 2024 to 2029. The country's market growth is driven by increasing government initiatives in healthcare infrastructure development and rising adoption of interventional oncology devices. Canadian healthcare facilities are increasingly incorporating advanced interventional oncology devices, supported by favorable healthcare policies and growing awareness among healthcare professionals. The country's focus on improving cancer care services and expanding access to minimally invasive procedures contributes to its rapid market growth.

Interventional Oncology Devices Market in Europe

The European interventional oncology devices market showcases significant growth potential, supported by advanced healthcare systems and increasing adoption of minimally invasive procedures across the region. The market landscape varies across different countries, with Germany, the United Kingdom, France, Italy, and Spain representing key markets. The region benefits from strong healthcare infrastructure, favorable reimbursement policies, and active research and development initiatives in interventional oncology.

Interventional Oncology Devices Market in Germany

Germany maintains its position as the largest market in Europe, commanding approximately 23% of the regional market share in 2024. The country's market leadership is supported by its advanced healthcare infrastructure, high healthcare spending, and strong presence of medical device manufacturers. German healthcare facilities demonstrate high adoption rates of interventional oncology procedures, backed by comprehensive insurance coverage and well-established healthcare protocols. The country's focus on technological advancement and quality healthcare delivery continues to drive market growth.

Interventional Oncology Devices Market in France

France emerges as the fastest-growing market in Europe, with a projected growth rate of around 9% from 2024 to 2029. The country's remarkable growth is driven by increasing investments in healthcare infrastructure, rising adoption of minimally invasive procedures, and growing awareness about interventional oncology treatments. French healthcare institutions are actively incorporating advanced interventional oncology devices, supported by favorable government policies and reimbursement scenarios. The country's commitment to advancing cancer care through innovative treatments contributes to its accelerated market growth.

Interventional Oncology Devices Market in Asia-Pacific

The Asia-Pacific interventional oncology devices market demonstrates significant growth potential, driven by improving healthcare infrastructure, increasing healthcare expenditure, and rising awareness about minimally invasive procedures. The region encompasses diverse markets including China, Japan, India, Australia, and South Korea, each with unique healthcare dynamics and growth trajectories. The market benefits from growing investment in healthcare infrastructure and increasing adoption of advanced medical technologies.

Interventional Oncology Devices Market in China

China leads the Asia-Pacific market, demonstrating strong market presence and consistent growth. The country's dominance is attributed to its large patient population, expanding healthcare infrastructure, and increasing government support for advanced medical technologies. Chinese healthcare facilities are rapidly adopting interventional oncology procedures, supported by growing healthcare expenditure and improving access to advanced medical care. The country's focus on healthcare modernization and expanding medical device industry contributes to its market leadership.

Interventional Oncology Devices Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, showing remarkable growth potential. The country's market growth is driven by increasing healthcare awareness, improving healthcare infrastructure, and rising adoption of minimally invasive procedures. Indian healthcare facilities are increasingly incorporating advanced interventional oncology devices, supported by growing private sector investments and government initiatives. The country's large patient population and expanding healthcare sector contribute to its accelerated market growth.

Interventional Oncology Devices Market in Middle East & Africa

The Middle East & Africa interventional oncology devices market shows promising growth potential, characterized by improving healthcare infrastructure and increasing adoption of advanced medical technologies. The region encompasses diverse markets including GCC countries and South Africa, with varying levels of healthcare development and market maturity. Within this region, GCC countries represent the largest market, while South Africa emerges as the fastest-growing market, driven by increasing healthcare investments and growing awareness about minimally invasive procedures.

Interventional Oncology Devices Market in South America

The South American interventional oncology devices market demonstrates steady growth, supported by improving healthcare infrastructure and increasing adoption of minimally invasive procedures. The region includes key markets such as Brazil and Argentina, with varying levels of healthcare development and market penetration. Brazil represents the largest market in the region, while Argentina shows the fastest growth potential, driven by increasing healthcare investments and growing awareness about interventional oncology procedures. The market benefits from expanding healthcare access and growing emphasis on advanced medical technologies.

Get Analysis on Important Geographic Markets

Download PDF

Interventional Oncology Industry Overview

Top Companies in Interventional Oncology Devices Market

The interventional oncology companies market is characterized by intense innovation and strategic developments among key players, including Boston Scientific Corporation, Medtronic PLC, Terumo Corporation, Merit Medical Systems, and Becton, Dickinson and Company. Companies are focusing on expanding their product portfolios through continuous research and development in advanced ablation technologies, embolization devices, and minimally invasive surgical tools. Strategic partnerships and collaborations with healthcare providers and research institutions have become increasingly common to enhance market presence and technological capabilities. The industry has witnessed significant investments in developing AI-powered solutions and precision targeting systems for improved treatment outcomes. Geographic expansion, particularly in emerging markets, remains a key focus area, with oncology medical device companies establishing regional manufacturing facilities and distribution networks. Product customization and the development of specialized devices for specific cancer types demonstrate the industry's commitment to meeting diverse clinical needs.

Consolidated Market with Strong Regional Leaders

The interventional oncology devices market exhibits a relatively consolidated structure dominated by large multinational oncology device companies with diverse product portfolios. These established players leverage their extensive research capabilities, global distribution networks, and strong financial positions to maintain market leadership. Regional players maintain a significant presence in specific geographic markets through specialized product offerings and a deep understanding of local healthcare systems. The market has witnessed strategic acquisitions aimed at expanding product portfolios and gaining access to innovative technologies, particularly in emerging therapeutic areas.

The competitive dynamics are shaped by high entry barriers due to stringent regulatory requirements and substantial investment needs in research and development. Companies with established relationships with healthcare providers and strong track records in product safety and efficacy maintain competitive advantages. The market structure encourages collaboration between device manufacturers and healthcare institutions for product development and clinical validation. Local manufacturers, particularly in Asia-Pacific regions, are gradually expanding their presence through cost-effective solutions and region-specific product innovations.

Innovation and Market Access Drive Success

Success in the interventional oncology devices market increasingly depends on developing innovative solutions that improve treatment outcomes while reducing procedural complexity and healthcare costs. Companies must focus on building comprehensive product portfolios that address various cancer types and treatment approaches. Establishing strong relationships with healthcare providers, investing in clinical evidence generation, and maintaining robust quality management systems are crucial for market success. The ability to navigate complex regulatory environments and secure timely approvals for new products remains a critical factor for both established players and new entrants.

Market participants need to address the growing demand for personalized treatment solutions and integration with advanced imaging technologies. Building efficient supply chains and ensuring product availability across diverse geographic markets is becoming increasingly important. Companies must also consider the impact of healthcare reforms and reimbursement policies on product adoption. Success in emerging markets requires understanding local healthcare dynamics and developing market-specific strategies. The ability to provide comprehensive training and support to healthcare providers in utilizing advanced interventional oncology devices remains a key differentiator in the market. The oncology market share by company is influenced by the ability to innovate and adapt to these evolving demands.

Interventional Oncology Market Leaders

-

Boston Scientific Corporation

-

Medtronic plc

-

Terumo Corporation

-

AngioDynamics

-

Merit Medical Systems, Inc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Interventional Oncology Market News

- September 2022- Fluidx Medical completed enrollment in a trial for its GPX embolic device. In the multicenter trial, GPX was used to treat a variety of primary and metastatic tumors, renal adenoma tumors, and a range of other arterial and venous applications. The GPX embolic device is currently under development.

- March 2022- Guerbet launched a line of guidewires and expanded the portfolio with microcatheters resulting in a broad range of interventional imaging and embolization solutions available.

Interventional Oncology Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Perpetual Increase in the Incidence Rate of Cancers Worldwide

- 4.2.2 High Preference for Minimally Invasive Procedures

- 4.2.3 Augmented Funding from the Government in the Developed Countries

- 4.2.4 Favorable Reimbursement Scenario for Interventional Oncology Treatment

-

4.3 Market Restraints

- 4.3.1 Financial Burden on the Companies due to Product Recall

- 4.3.2 Dearth of Trained Interventional Oncologists and Clinical Evidence for Localized Treatment Region

- 4.3.3 Stringent Regulations for Medical Devices

-

4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value in USD million)

-

5.1 By Product Type

- 5.1.1 Ablation Devices

- 5.1.1.1 Microwave ablation

- 5.1.1.2 Radiofrequency ablation

- 5.1.1.3 Cryoablation

- 5.1.1.4 Other Product Types

- 5.1.2 Embolization Device

- 5.1.3 Microcatheters

- 5.1.4 Guidewires

- 5.1.5 Other Embolization Devices

-

5.2 By Cancer Type

- 5.2.1 Lung cancer

- 5.2.2 Breast Cancer

- 5.2.3 Liver Cancer

- 5.2.4 Kidney Cancer

- 5.2.5 Prostate Cancer

- 5.2.6 Other Cancer Types

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Boston Scientific Corporation

- 6.1.2 Medtronic PLC

- 6.1.3 Terumo Corporation

- 6.1.4 Merit Medical Systems Inc.

- 6.1.5 Becton, Dickinson and Company (C.R.Bard Inc.)

- 6.1.6 Profound Medical Corp.

- 6.1.7 AngioDynamics Inc.

- 6.1.8 Cook Medical

- 6.1.9 HealthTronics Inc.

- 6.1.10 IceCure Medical

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers - Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Interventional Oncology Industry Segmentation

Interventional oncology deals with the treatment of various types of cancer using targeted, minimally invasive procedures performed under image guidance. As minimally invasive procedures are less painful and low-risk than other traditional surgeries, interventional oncology is gaining a lot of importance in treating cancer.

The Interventional Oncology Devices Market is Segmented by Product Type (Ablation Devices (Microwave ablation, Radiofrequency ablation, Cryoablation, and Other Product Types) and Embolization Devices (Microcatheters, Guidewires, and Others), Cancer Type (Lung Cancer, Breast Cancer, Liver Cancer, Kidney Cancer, Prostate Cancer, and Other Cancer Types), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers value (in USD million) for the above segments.

| By Product Type | Ablation Devices | Microwave ablation | |

| Radiofrequency ablation | |||

| Cryoablation | |||

| Other Product Types | |||

| Embolization Device | |||

| Microcatheters | |||

| Guidewires | |||

| Other Embolization Devices | |||

| By Cancer Type | Lung cancer | ||

| Breast Cancer | |||

| Liver Cancer | |||

| Kidney Cancer | |||

| Prostate Cancer | |||

| Other Cancer Types | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Interventional Oncology Market Research FAQs

How big is the Interventional Oncology Devices Market?

The Interventional Oncology Devices Market size is expected to reach USD 2.24 billion in 2025 and grow at a CAGR of 6.5% to reach USD 3.06 billion by 2030.

What is the current Interventional Oncology Devices Market size?

In 2025, the Interventional Oncology Devices Market size is expected to reach USD 2.24 billion.

Who are the key players in Interventional Oncology Devices Market?

Boston Scientific Corporation, Medtronic plc, Terumo Corporation, AngioDynamics and Merit Medical Systems, Inc are the major companies operating in the Interventional Oncology Devices Market.

Which is the fastest growing region in Interventional Oncology Devices Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Interventional Oncology Devices Market?

In 2025, the North America accounts for the largest market share in Interventional Oncology Devices Market.

What years does this Interventional Oncology Devices Market cover, and what was the market size in 2024?

In 2024, the Interventional Oncology Devices Market size was estimated at USD 2.09 billion. The report covers the Interventional Oncology Devices Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Interventional Oncology Devices Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Interventional Oncology Devices Market Research

Mordor Intelligence provides a comprehensive analysis of the interventional oncology devices market, utilizing our extensive experience in healthcare industry research. Our latest report examines the full range of oncology medical devices, including chemotherapy devices and interventional consumables. The analysis covers leading interventional oncology companies and their innovative solutions. These range from microwave ablation devices for interventional oncology to advanced tumor treatment equipment.

This detailed report, available as an easy-to-download PDF, offers stakeholders crucial insights into IO devices and emerging technologies. We examine key players, including prominent oncology medical device companies, and their product portfolios. These span interventional oncology products and lung tumor embolization solutions. The report benefits investors, manufacturers, and healthcare providers by offering a detailed analysis of embolization in interventional oncology procedures and market dynamics. Our research supports strategic decision-making for oncology device companies while providing valuable insights into the evolving landscape of interventional oncology medical devices and their applications.