Market Overview

| Study Period | 2022 - 2030 |

|---|---|

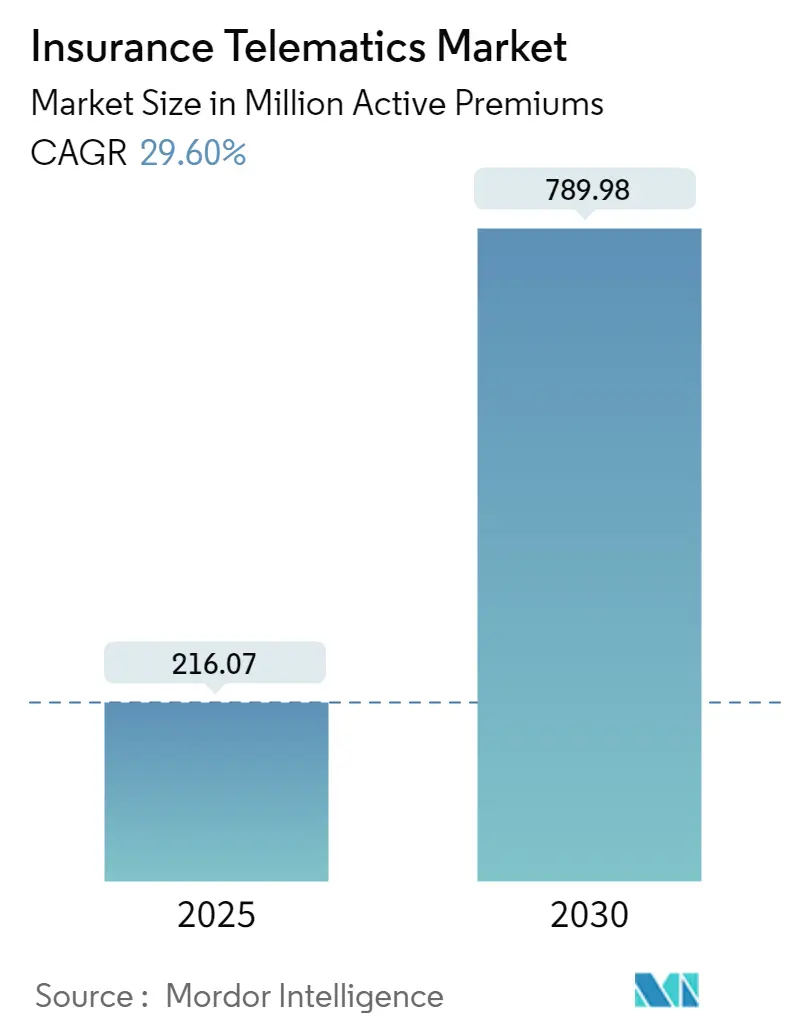

| Market Volume (2025) | 216.07 Million active premiums |

| Market Volume (2030) | 789.98 Million active premiums |

| Growth Rate (2025 - 2030) | 29.60% CAGR |

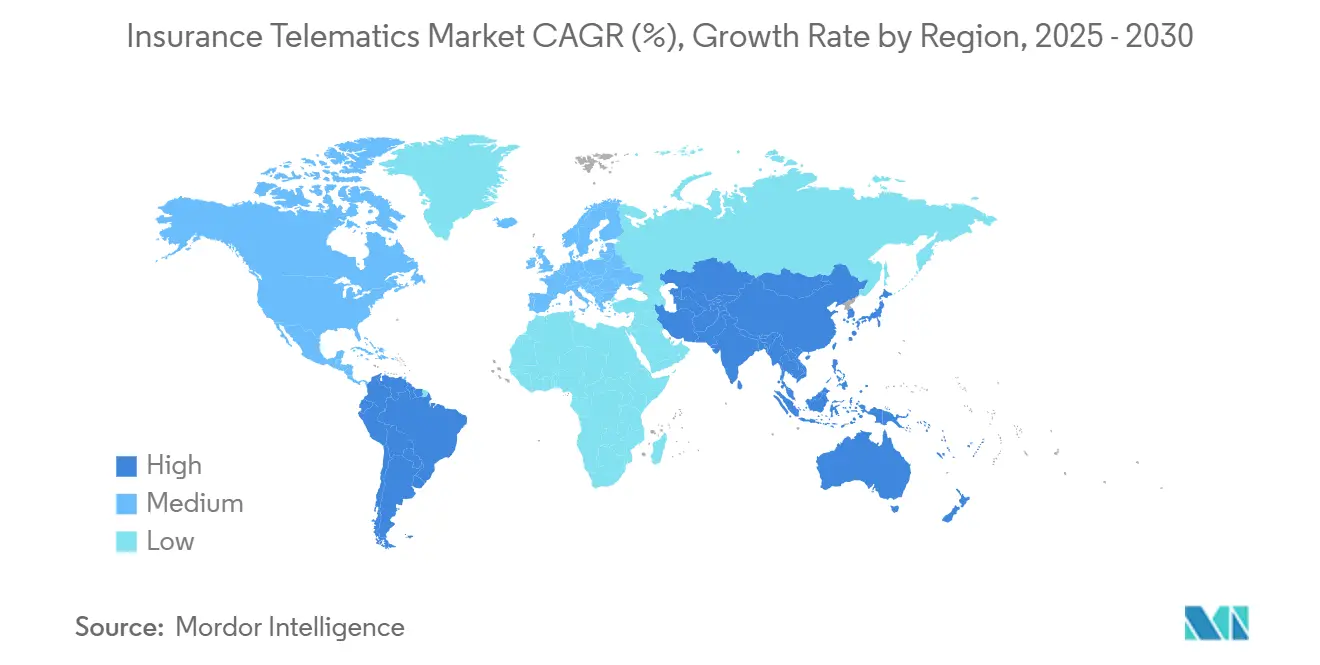

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Insurance Telematics Market Analysis by Mordor Intelligence

The telematics insurance market counts 216.07 million active premiums in 2025 and is projected to reach 789.98 million by 2030, delivering a 29.60% CAGR. The market size expansion reflects insurers’ rapid adoption of data-driven pricing models that rely on real-time driving analytics, automotive connectivity upgrades, and AI-enabled fraud scoring.[1]Cambridge Mobile Telematics, “Direct Assurance Selects Cambridge Mobile Telematics,” cmtelematics.com European carriers maintain an early-mover advantage, while Asia-Pacific shows the steepest adoption curve on the back of regulatory mandates and rising smartphone penetration. Competitive dynamics favour technology-savvy insurers and OEM captive programs that leverage proprietary vehicle data. Headwinds stem from data-privacy compliance costs and cybersecurity risks tied to aftermarket dongles, yet momentum persists as smartphone-centric platforms lower deployment friction and widen addressable customer pools.

Key Report Takeaways

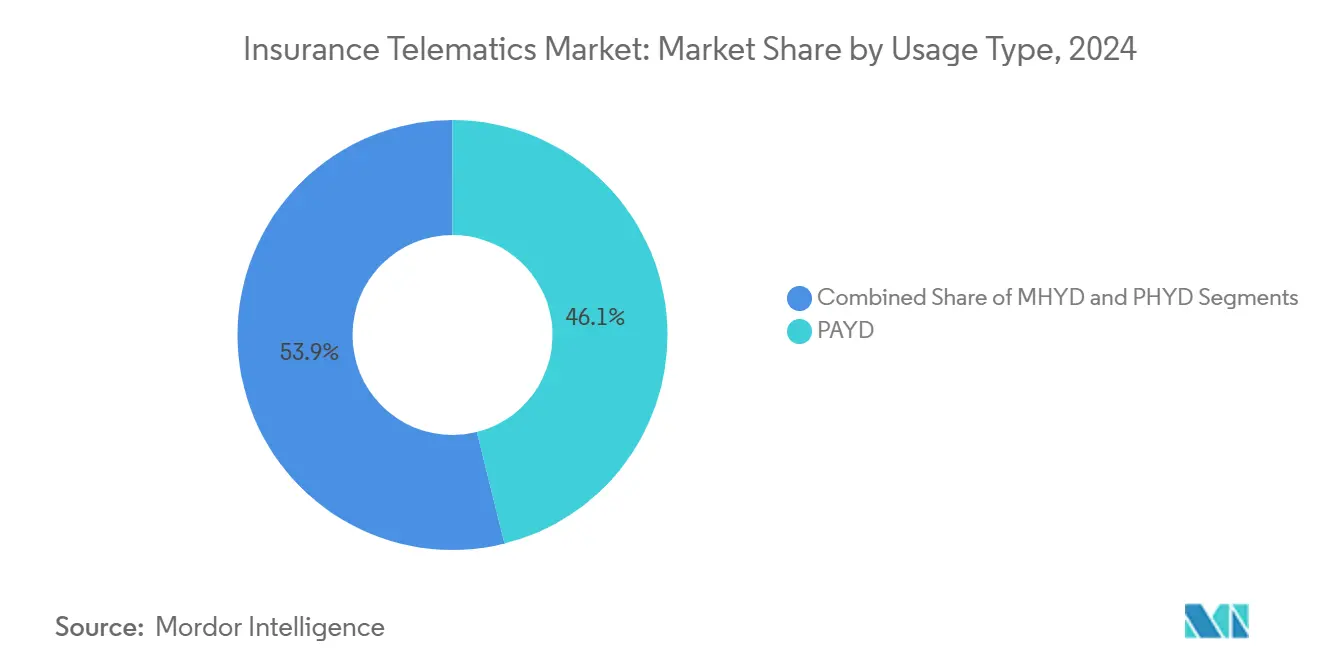

- By usage type, pay-as-you-drive held 46.11% of the telematics insurance market share in 2024, whereas manage-how-you-drive programs are advancing at a 32.60% CAGR through 2030.

- By vehicle type, passenger cars accounted for 74.38% of the telematics insurance market size in 2024, and light commercial vehicles are scaling at a 30.67% CAGR to 2030.

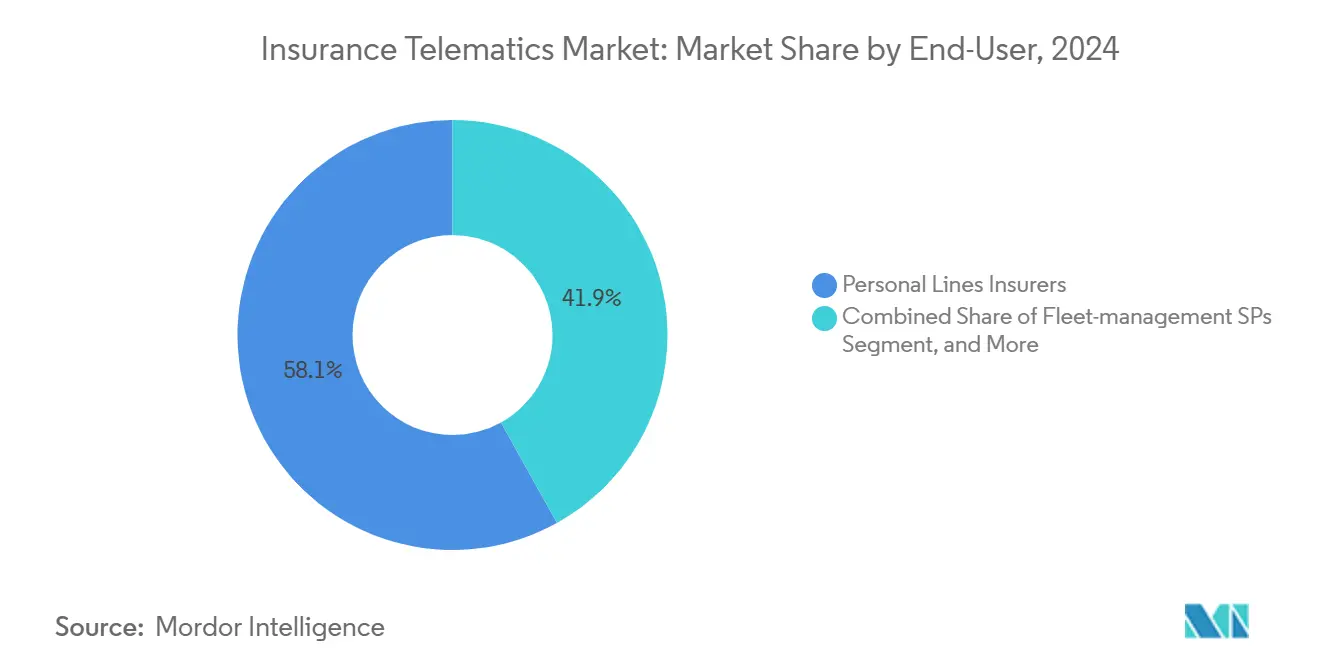

- By end-user, personal lines insurers controlled 58.07% of active policies in 2024, while fleet service providers are poised for a 32.88% CAGR through 2030.

- By distribution, direct-to-consumer captured a 55.33% share in 2024, and OEM-dealer bundles are accelerating at a 31.94% CAGR through 2030.

- By region, Europe led with 32.86% market share in 2024, yet Asia-Pacific is forecast to climb at a 33.61% CAGR between 2025-2030.

Global Insurance Telematics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid insurer shift to Usage-Based Insurance (UBI) | +8.50% | Global, with early adoption in Europe and North America | Short term (≤ 2 years) |

| Automotive connectivity innovations (5G, eSIM) | +6.20% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Stricter road-safety and CO₂ regulations | +4.80% | Europe, North America, expanding to APAC | Long term (≥ 4 years) |

| OEM API monetisation mandates | +3.10% | Europe, North America, selective APAC markets | Medium term (2-4 years) |

| Pay-per-mile subsidies from city congestion schemes | +2.40% | Urban centers in Europe, select North American cities | Short term (≤ 2 years) |

| AI-driven fraud scoring lowering loss ratios | +4.00% | Global, with advanced deployment in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Insurer Shift to Usage-Based Insurance Models

Direct Assurance grew its YouDrive book 27% in 2024 and cut average premiums by EUR 200 (USD 213) per customer, underlining how real-time behavioural data outperforms static demographics for risk pricing. Progressive reported USD 74.4 billion in net written premiums for 2024, up 21%, with telematics programs the chief growth lever.[2]Insurance News Net, “2024 Annual Report Summary,” insurancenewsnet.com Data velocity rather than volume drives competitive gains, as seen in Cambridge Mobile Telematics’ expansion to 1 million Japanese drivers in 2025. As pay-how-you-drive products proliferate, incumbents risk share erosion unless they integrate mobile telematics swiftly.

Automotive Connectivity Innovations Drive Infrastructure Transformation

5G and eSIM technology are converting vehicles into always-on data hubs. BMW’s iX platform, developed with Deutsche Telekom, showcases dual-SIM connectivity that separates telematics from infotainment traffic for resilient data streams.[3]BMW Group, “BMW Integrates 5G and eSIM,” press.bmwgroup.com G+D’s dual-active SIM architecture further secures over-the-air updates and ensures global roaming continuity. Ericsson’s IoT Accelerator lets automakers orchestrate remote SIM provisioning at scale. Embedded connectivity removes aftermarket hardware dependencies, boosts data fidelity, and paves the way for instant crash notification, elevating insurer value propositions from reactive claims settlement to proactive risk prevention.

AI-Driven Fraud Detection Revolutionizes Claims Processing

FRISS analytics reduces claim handling time by 66% and cuts false positives by 75%, saving USD 9.2 million annually for partner carriers. Allstate’s machine-learning patent uses vehicle sensor feeds to anticipate hazards and trigger driver assistance cues. OCTO Telematics has documented a 50% drop in fraudulent claims alongside a 20% faster settlement cycle with AI-supported telematics. These gains strengthen combined ratios and free capital for competitive premium pricing.

OEM API Monetization Creates New Revenue Streams

High Mobility’s data platform works with BMW, Audi, Volkswagen, and Kia to deliver standardized vehicle data directly to insurers, bypassing dongle installation costs. Kia’s 2025 roll-out with LexisNexis across 27 EU countries exemplifies GDPR-compliant, app-based personalization at scale. Allianz argues that the EU Data Act will turbo-charge customer-centric products by mandating non-discriminatory data access for third-party insurers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and consent hurdles (GDPR, CPRA) | -4.20% | Europe, California, expanding globally | Long term (≥ 4 years) |

| Device/data-quality interoperability gaps | -3.80% | Global, particularly affecting aftermarket solutions | Medium term (2-4 years) |

| Rising CAN-bus cyber-attacks on aftermarket dongles | -2.10% | Global, concentrated in markets with high aftermarket adoption | Short term (≤ 2 years) |

| Adverse selection as low-risk drivers exit pools | -1.90% | Developed markets with mature telematics adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy Regulations Create Implementation Complexity

The European Data Protection Board mandates explicit consent, granular purpose limitation, and user revocation rights for in-car data, lengthening onboarding cycles and raising compliance costs. China obliges local data storage plus security assessments before cross-border transfer, fragmenting global platforms and inflating architecture expense. Smaller insurers often lack the resources for continuous privacy audits, nudging market share toward larger carriers that can spread compliance overhead across broader portfolios.

Cybersecurity Vulnerabilities Threaten Market Confidence

Carnegie Mellon research highlights inadequate encryption and open debug ports in many aftermarket dongles, exposing vehicles to location tracking, remote-kill, and hijack risks. Real-world CAN-bus injection attacks enabling headlight-to-OBD thefts underscore the threat to vehicle integrity. Insurance carriers face reputational damage and potential liability if compromised devices facilitate theft or bodily harm. Migration to smartphone or OEM-embedded solutions mitigates exposure, but transition risk lingers.

Segment Analysis

By Usage Type: MHYD Programs Drive Innovation

Manage-how-you-drive products are climbing at a 32.60% CAGR, outpacing the telematics insurance market average as insurers reward safe acceleration, braking, and cornering. India’s 2025 regulation requires carriers to list pay-as-you-drive as a standard motor option, catalysing broader UBI uptake. PAYD retains volume leadership yet faces saturation, while pay-how-you-drive hybrids bridge mileage and behaviour for nuanced risk scores. Cambridge Mobile Telematics’ DriveWell platform demonstrates 20% claim-frequency reduction by gamifying feedback loops, validating MHYD economics.

Adoption barriers center on driver privacy perceptions and sensor calibration, but smartphone telematics’ passive data capture eases these frictions. As regulators promote eco-driving incentives, MHYD aligns closely with urban emissions goals, positioning it as a cornerstone of next-generation mobility insurance.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology Platform: Smartphone Solutions Displace Hardware

OBD-II dongles controlled 39.25% of policies in 2024 but face a decline as smartphone apps grow at a 33.81% CAGR. Smartcar notes dongles incur logistics, tampering, and accuracy costs that erode insurer ROI. Conversely, smartphone sensors plus cloud AI deliver comparable event resolution without hardware overhead. OEM-embedded modules command premium positioning for high-end vehicles, offering secure boot chains and high-rate CAN data, but depend on data-sharing agreements. Black-box devices retain relevance in jurisdictions mandating sealed hardware for legal traceability.

Transition success hinges on battery optimization and motion-co-processing to ensure reliable data while preserving user experience. Zendrive’s mobile SDK shows 98% trip-detection accuracy, proving smartphone viability.

By Vehicle Type: Commercial Fleets Drive Adoption

Passenger cars contribute 74.38% of active policies, yet commercial light vehicles post the fastest growth thanks to e-commerce delivery optimization and stricter fleet safety standards. Munich Re documents insurers granting up to 15% premium rebates when fleets adopt telematics-enabled driver coaching, improving profitability for both carrier and customer. In heavy vehicles, regulatory tachograph and ADAS mandates embed telematics into compliance routines, cementing baseline adoption.

Fleet managers value telematics beyond insurance, exploiting route analytics and maintenance alerts for total-cost-of-ownership savings. Geotab records 10% fuel efficiency gains when telematics informs coaching and idle-time reduction, bolstering insurer partnerships that hinge on verified operational improvements.

By End-User: Fleet Managers Embrace Technology

Personal lines insurers hold 58.07% of the telematics insurance market size, but fleet-service providers enjoy a 32.88% CAGR as they bundle insurance with driver performance dashboards. Azuga’s solution allows commercial carriers to re-rate premiums mid-term based on real-world safety scores, aligning cost with risk and reducing claim payout volatility. OEM captives are emerging; Tesla and BYD now underwrite in-house, leveraging proprietary battery and ADAS data to quote in real time, challenging traditional intermediated models.

For insurers, fleet accounts offer richer, high-frequency data and better retention given contracted service periods, offsetting the lower margin per vehicle versus personal auto.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: OEM Integration Accelerates

Direct online sales captured 55.33% of policies in 2024, but OEM-dealer bundles are growing fastest at 31.94% CAGR as embedded insurance aligns with vehicle financing cycles. ERGO’s partnership with O2 Telefónica embeds coverage into smartphone contracts, hinting at cross-industry bundling potential. Broker-agent channels retain relevance in complex commercial segments where bespoke coverage still requires advisory.

OEM integration reduces underwriting ambiguity by streaming standardized factory sensor data from day one, compressing the customer acquisition funnel, and supporting dynamic premium models activated at vehicle handover.

Geography Analysis

Europe led with 32.86% market share in 2024 on the strength of GDPR-backed consumer trust and stringent road-safety policies. An EIOPA survey found 17% of carriers already market telematics products, and the forthcoming EU Data Act is expected to raise adoption by formalizing data-sharing rights. Subsidies in congestion-priced cities, notably London and Milan, further magnify pay-per-mile program uptake.

Asia-Pacific is forecast to chart a 33.61% CAGR to 2030 as India mandates AIS-140 location trackers and China standardizes automotive data security. China’s regulator promotes telematics for new-energy vehicle safety analytics, unlocking premium discounts for EV drivers. Japan’s solvency reforms reward capital relief for tech-enabled risk mitigation, incentivizing carriers to allocate budget toward telematics infrastructure.

North America continues to experience steady growth. Progressive’s telematics penetration reached 45% of new auto business in 2024, underpinning its 68% combined ratio outperformance. Data-privacy patchwork and higher litigation risk temper acceleration, but high smartphone adoption sustains momentum.

Middle East, Africa, and South America remain nascent yet promising. Government digitization agendas and rising motorization rates lay groundwork for telematics pilots, with importers keen to embed connectivity to differentiate offerings.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The telematics insurance market shows moderate fragmentation. Cambridge Mobile Telematics, Octo Telematics, Progressive, and Allstate together controlled roughly one-quarter of active premiums in 2024. CMT’s Frost & Sullivan award recognizes its data-science depth and claims-automation toolkit. Octo’s AI suite slashed partner fraud rates by 50%, prompting expansions into Latin America and the Gulf.

Intuit’s 2025 acquisition of Zendrive technology signals fintech convergence, marrying cash-flow analytics with driving behaviour insight for holistic small-business risk profiling.[4]BMW Group, “BMW Integrates 5G and eSIM,” press.bmwgroup.com OEM captives such as Tesla Insurance underprice rivals by up to 30% on certain trims, leveraging granular battery-temperature and ADAS usage data inaccessible to third-party carriers.

Strategic partnerships dominate activity: insurers pair with API aggregators like High Mobility to obtain OEM-grade data without bespoke integrations; reinsurers co-develop dynamic quota-share treaties that flex with real-time loss ratios. Barriers to entry are lowering for data-native startups yet scaling nationwide requires regulatory expertise and capital strength, preserving incumbent relevance.

Insurance Telematics Industry Leaders

-

GEICO (Berkshire Hathaway Inc.)

-

UnipolTech SpA (UNIPOL GRUPPO SpA)

-

Octo Telematics SpA

-

DriveQuant

-

Imertik Global Inc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: Kia partnered with LexisNexis to inject behaviour analytics into its EU mobile app, enabling personalized premiums compliant with GDPR.

- June 2025: Cambridge Mobile Telematics unveiled AI-powered crash reconstruction modules to strengthen claims automation.

- June 2025: Intuit closed the purchase of Zendrive assets, adding driving-risk signals to its financial-services ecosystem.

- January 2025: Direct Assurance picked Cambridge Mobile Telematics to scale YouDrive, France’s largest UBI program.

Global Insurance Telematics Market Report Scope

The market for insurance telematics was analyzed considering the total number of active premiums filed by the various insurance providers operating worldwide.

The insurance telematics market is segmented by usage type (pay-as-you-drive, pay-how-drive, manage-how-you-drive) and geography (North America, Europe, Asia-Pacific, Rest of the World). The market sizes and forecasts are provided in terms of the number of active premiums for all the above segments.

By Usage Type

| Pay-as-you-drive (PAYD) |

| Pay-how-you-drive (PHYD) |

| Manage-how-you-drive (MHYD) |

By Technology Platform

| OBD-II Dongle |

| Embedded OEM Module |

| Smartphone-centric |

| Black-box/Hardwired |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

By End-User

| Personal Lines Insurers |

| Commercial Lines Insurers |

| Automotive OEM Captives |

| Fleet-management Service Providers |

By Distribution Channel

| Direct-to-Consumer |

| Broker/Agent-Mediated |

| OEM/Dealer Bundle |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Usage Type | Pay-as-you-drive (PAYD) | |

| Pay-how-you-drive (PHYD) | ||

| Manage-how-you-drive (MHYD) | ||

| By Technology Platform | OBD-II Dongle | |

| Embedded OEM Module | ||

| Smartphone-centric | ||

| Black-box/Hardwired | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| By End-User | Personal Lines Insurers | |

| Commercial Lines Insurers | ||

| Automotive OEM Captives | ||

| Fleet-management Service Providers | ||

| By Distribution Channel | Direct-to-Consumer | |

| Broker/Agent-Mediated | ||

| OEM/Dealer Bundle | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

Telematics insurance adoption - what drives customer uptake most?

Premium savings tied to real-time driving scores, typically EUR 200 (USD 213) per year in Europe and 10-15% in the U.S., motivate sign-ups that are reinforced by transparent data feedback.

How fast will usage-based policies replace traditional motor coverage?

Active premiums under telematics are growing at a 29.60% CAGR and could exceed 50% of new auto policies worldwide by 2030.

Which region shows the strongest regulatory push?

Asia-Pacific, led by India's AIS-140 tracker mandate and China's automotive data security rules, is forecast to deliver a 33.61% CAGR through 2030.

Do smartphone apps match the data quality of OBD devices?

Studies show 98% trip-capture accuracy for smartphone SDKs and comparable claim triaging, making apps the fastest-growing technology platform segment.

What cybersecurity measures are insurers adopting?

Migration to OEM APIs, encrypted mobile SDKs, and periodic penetration testing are now standard practices to counter CAN-bus injection and dongle tampering threats.

How does AI change claims handling?

AI-driven fraud analytics cut handling time by two-thirds and reduce false positives by 75%, freeing capital that insurers redirect toward competitive pricing.

Page last updated on: