Market Size of Infrastructure Sector In Asia Pacific Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

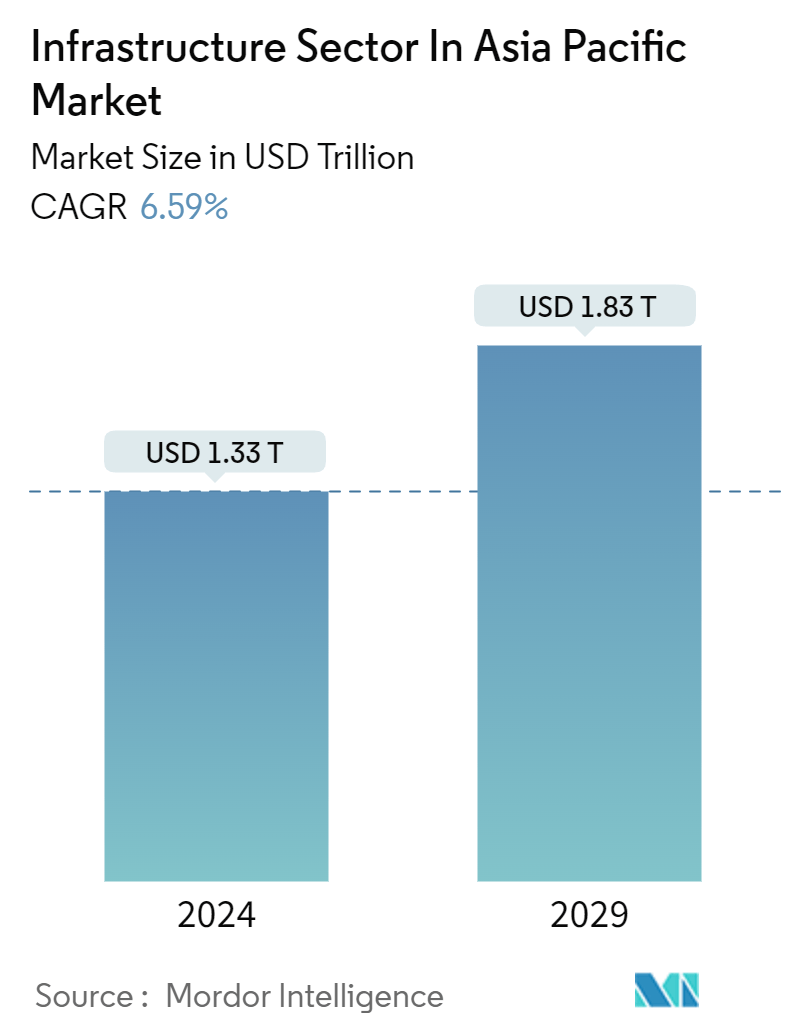

| Market Size (2024) | USD 1.33 Trillion |

| Market Size (2029) | USD 1.83 Trillion |

| CAGR (2024 - 2029) | 6.59 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

APAC Infrastructure Market Analysis

The Infrastructure Sector In Asia Pacific Market size is estimated at USD 1.33 trillion in 2024, and is expected to reach USD 1.83 trillion by 2029, at a CAGR of 6.59% during the forecast period (2024-2029).

Southeast Asia is experiencing a boom in infrastructure, with major projects in Vietnam, Thailand, the Philippines, Malaysia, and Indonesia accepted. Those were supported in many cases by loans and other assistance provided by Japan and China. The distinction between Japan and China's one-year investment in Southeast Asia represents just part of the story. China’s investments in ASEAN infrastructure have risen rapidly in recent years.

The backbone of the Indian economy, the infrastructure sector, is essential to improving the nation's overall development. Other industry sub-segments include telephony, power, roads, ports, etc. India has to enhance its infrastructure to reach its 2025 economic growth target of USD 5 trillion. The National Infrastructure Pipeline (NIP), along with other initiatives like "Make in India" and the production-linked incentives (PLI) program, was launched by the government to promote the expansion of the infrastructure industry. Under the PM Gati Shakti National Master Plan (NMP), 44 Central Ministries and 36 States/UTs have come on board, integrating a total of 1,614 data layers. To uphold data accuracy, key infrastructure ministries have established Standard Operating Procedures (SOPs) within a three-tier system. SOPs have been officially notified for 8 infrastructure ministries and 15 social sector ministries, while development efforts are ongoing for additional ministries and States/UTs.

Japan's Ministry of Land, Infrastructure, and Transportation (MLIT) plays a pivotal role in managing the nation's infrastructure. According to MLIT, proactively detecting and addressing at-risk infrastructure can prevent severe incidents and cut maintenance and renewal costs by an impressive 47%, translating to a potential savings of USD 46 billion by 2048. In light of this, MLIT has been championing Digital Transformation (DX) for infrastructure since 2021, urging municipalities, the entities responsible for managing infrastructure, to adopt and implement advanced inspection technologies. In 2023, over 730,000 bridges, 11,000 tunnels, 10,000 water gates, 470,000 meters of sewage pipes, and 5,000 harbor quays have surpassed the 50-year mark. The challenges posed by this aging infrastructure, coupled with related accidents, have garnered heightened scrutiny from both the government and the public.

Overall, the prospects for regional infrastructure investment are highly promising. While COVID-19 has had a considerable influence on infrastructure development and finance throughout the area, part of that change is beneficial to project lenders and investors. The epidemic has hastened investment in low-carbon, climate-resilient infrastructure, as well as initiatives that improve internet connection and public health. The two areas—ESG and digitalization—will continue to dominate the infrastructure sector for the foreseeable future.

APAC Infrastructure Industry Segmentation

Infrastructure is the backbone of domestic and international commerce and industrial and agricultural production. It is the fundamental organizational and physical framework necessary to operate a firm successfully. The infrastructure sector focuses on major infrastructure such as power, roads and bridges, dams, and urban infrastructure.

A complete background analysis of the market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends is covered in the report.

The APAC infrastructure market is segmented by the infrastructure segment (social infrastructure, transportation infrastructure, extraction infrastructure, manufacturing infrastructure) and by country (China, India, Japan, South Korea, Philippines, and the rest of Asia-Pacific). The report offers market size and forecast values (USD) for all the above segments.

| Social Infrastructure | |

| Schools | |

| Hospitals | |

| Defence | |

| Other social infrastructures |

| Transportation Infrastructure | |

| Railways | |

| Roadways | |

| Airports | |

| Waterways |

| Extraction Infrastructure | |

| Power Generation | |

| Electricity Transmission & Distribution | |

| Water | |

| Gas | |

| Telecoms |

| Manufacturing Infrastructure | |

| Metal and Ore Production | |

| Petroleum Refining | |

| Chemical Manufacturing | |

| Industrial Parks and Clusters | |

| Other manufacturing infrastructures |

| Country | |

| China | |

| India | |

| Philippines | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific |

Infrastructure Sector In Asia Pacific Market Size Summary

The Asia Pacific infrastructure market is poised for significant growth, driven by substantial investments and strategic initiatives across the region. Southeast Asia is witnessing a surge in infrastructure development, with countries like Vietnam, Thailand, the Philippines, Malaysia, and Indonesia leading the charge, often supported by financial assistance from Japan and China. In India, the infrastructure sector is a crucial component of the national economy, with the government implementing programs like the National Infrastructure Pipeline and "Make in India" to boost development. Japan continues to play a dominant role in Southeast Asia, with a focus on large-scale projects, particularly in Vietnam. The region's infrastructure landscape is also evolving in response to the COVID-19 pandemic, which has accelerated investments in low-carbon and climate-resilient projects, as well as those enhancing digital connectivity and public health.

The market is characterized by a fragmented landscape with numerous new entrants vying for projects, supported by private and venture capital investments. Key players include China State Construction Engineering, China Communications Construction Company, Power Construction Corporation of China, Samsung C&T, and Obayashi Corporation. The Philippines is exploring international financing and foreign investment in its infrastructure modernization efforts, while China continues to expand its transportation infrastructure through ambitious plans. Japan is enhancing its transportation networks, including high-speed rail and airport facilities. The market's growth trajectory is further supported by strategic partnerships and investments in renewable energy and green technologies, indicating a robust outlook for the infrastructure sector in the Asia Pacific region.

Infrastructure Sector In Asia Pacific Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Policies and Regulations

-

1.3 Government Regulations and Initiatives

-

1.4 Supply Chain/Value Chain Analysis

-

1.5 Insights into Technological Innovation in the APAC Infrastructure Sector

-

1.6 Impact of Geopolitics and Pandemic on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 Social Infrastructure

-

2.1.1 Schools

-

2.1.2 Hospitals

-

2.1.3 Defence

-

2.1.4 Other social infrastructures

-

-

2.2 Transportation Infrastructure

-

2.2.1 Railways

-

2.2.2 Roadways

-

2.2.3 Airports

-

2.2.4 Waterways

-

-

2.3 Extraction Infrastructure

-

2.3.1 Power Generation

-

2.3.2 Electricity Transmission & Distribution

-

2.3.3 Water

-

2.3.4 Gas

-

2.3.5 Telecoms

-

-

2.4 Manufacturing Infrastructure

-

2.4.1 Metal and Ore Production

-

2.4.2 Petroleum Refining

-

2.4.3 Chemical Manufacturing

-

2.4.4 Industrial Parks and Clusters

-

2.4.5 Other manufacturing infrastructures

-

-

2.5 Country

-

2.5.1 China

-

2.5.2 India

-

2.5.3 Philippines

-

2.5.4 Japan

-

2.5.5 South Korea

-

2.5.6 Rest of Asia Pacific

-

-

Infrastructure Sector In Asia Pacific Market Size FAQs

How big is the Infrastructure Sector In Asia Pacific Market?

The Infrastructure Sector In Asia Pacific Market size is expected to reach USD 1.33 trillion in 2024 and grow at a CAGR of 6.59% to reach USD 1.83 trillion by 2029.

What is the current Infrastructure Sector In Asia Pacific Market size?

In 2024, the Infrastructure Sector In Asia Pacific Market size is expected to reach USD 1.33 trillion.