| Study Period | 2024 - 2030 |

| Market Size (2025) | USD 74.18 Billion |

| Market Size (2030) | USD 92.53 Billion |

| CAGR (2025 - 2030) | 4.52 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Industrial Valves Market Analysis

The Industrial Valves Market size is estimated at USD 74.18 billion in 2025, and is expected to reach USD 92.53 billion by 2030, at a CAGR of 4.52% during the forecast period (2025-2030).

The industrial valve market is experiencing significant transformation driven by rapid industrialization and technological advancement across core sectors. The chemical industry, a major end-user of industrial valves, has shown remarkable resilience and growth, particularly in Asia-Pacific. According to industry reports, China's chemical production increased by 4.2% in 2022, while the European Chemical Industry Council (CEFIC) projects China's share of global chemical sales to reach approximately 49% by 2030. This growth trajectory has been accompanied by substantial investments in chemical manufacturing facilities, exemplified by BASF's world-class syngas plant construction in Zhanjiang, China, announced in September 2023, representing one of the largest investments in the region.

The power generation sector continues to undergo substantial evolution, particularly in the transition toward cleaner energy sources. According to the International Energy Agency, wind electricity generation achieved a significant milestone in 2022, reaching over 2100 TWh and registering a 14% year-on-year growth. This transformation is further evidenced by major nuclear power developments, including China's approval of three nuclear power plant expansion projects in July 2023, with a combined investment of CNY 120 billion. The Bank of Ayudhya Public Company projects the power generation sector to grow between 2.8% to 3.8% annually, reflecting the robust demand for industrial valves in power infrastructure.

The market is witnessing a notable shift toward smart valve technologies and automation, driven by Industry 4.0 adoption across manufacturing sectors. Major manufacturers are increasingly incorporating digital technologies such as the Industrial Internet of Things (IIoT) and artificial intelligence for predictive maintenance and remote monitoring capabilities. This trend is particularly evident in new industrial facilities, where integrated digital solutions are becoming standard specifications for valve systems, enabling real-time monitoring, improved efficiency, and reduced maintenance costs.

The petrochemical sector is experiencing substantial expansion through strategic investments and new facility constructions. In March 2023, Saudi Aramco announced significant investments in Chinese petrochemical facilities, including a joint venture in Panjin city, Liaoning Province, with an investment of CNY 83.7 billion. This project, along with similar developments across Asia and the Middle East, demonstrates the growing demand for specialized industrial valves in high-pressure and corrosive environments. The industry is also witnessing increased emphasis on sustainable manufacturing practices, with valve manufacturers focusing on developing eco-friendly products and energy-efficient solutions to meet stringent environmental regulations.

Industrial Valves Market Trends

Growing Usage of Valves in the Water and Wastewater Treatment Industry

The water and wastewater treatment industry is experiencing significant growth in water treatment valve usage, driven by increasing water scarcity concerns and stringent environmental regulations worldwide. Water treatment facilities must use specific types of valves in their systems to ensure piping systems operate effectively, safely, and consistently, while preventing unnecessary maintenance. The industry primarily utilizes butterfly valves for regulating or isolating water flow, ball valves for controlling flow and pressure, gate valves as main shutoff mechanisms, check valves to prevent backflow contamination, and globe valves for throttling purposes. These valves play crucial roles in various applications, including water distribution, sewage treatment, and industrial wastewater management.

The increasing industrialization and urbanization have led to massive developments in wastewater treatment infrastructure worldwide. For instance, in 2024, Delhi is working towards constructing Asia's largest wastewater treatment plant, with an impressive sewage water treatment capacity of approximately 564 million liters per day (MLD). The selection of appropriate water treatment valve for water treatment plants is essential since it is a sensitive process, requiring careful consideration of factors such as valve purpose (isolation, throttling, or modulating), process parameters (pressure, temperature, and flow), chemical compatibility (concentration, media, density), and process requirements (allowable leakage rate, frequency of operation, available space, structural considerations, and cleanliness).

Understand The Key Trends Shaping This Market

Download PDF

Increasing Demand for Valves in the Oil and Gas Industry

The oil and gas industry continues to drive substantial demand for oil and gas valve across upstream, midstream, and downstream operations. In Southeast Asia alone, a total of 54 oil and gas projects across six countries are being implemented for the timeline 2021 to 2025, which collectively would represent approximately 223,000 barrels per day of global crude production and about 8.1 billion cubic feet per day of global gas production by 2025. These developments require extensive valve installations for various critical applications, including flow control, pressure regulation, and safety systems. The industry utilizes a wide range of valve types, including ball valves for on-off services, gate valves for isolation, globe valves for throttling, and check valves for preventing backflow in critical processes.

The expansion of oil and gas infrastructure has led to increased demand for specialized valve technologies that can withstand extreme pressures, temperatures, and corrosive environments. Industrial valves in this sector are crucial components in ensuring safe and efficient operations across the entire value chain, from exploration and production to transportation and processing. The industry requires valves that comply with stringent safety standards and specifications, particularly in applications such as emergency shutdown systems, pressure relief, and flow control in refineries and petrochemical plants. The continuous development of new oil and gas projects, coupled with the modernization of existing facilities, is expected to sustain the strong demand for oil and gas valve in this sector.

Segment Analysis: By Type

Ball Valves Segment in Industrial Valves Market

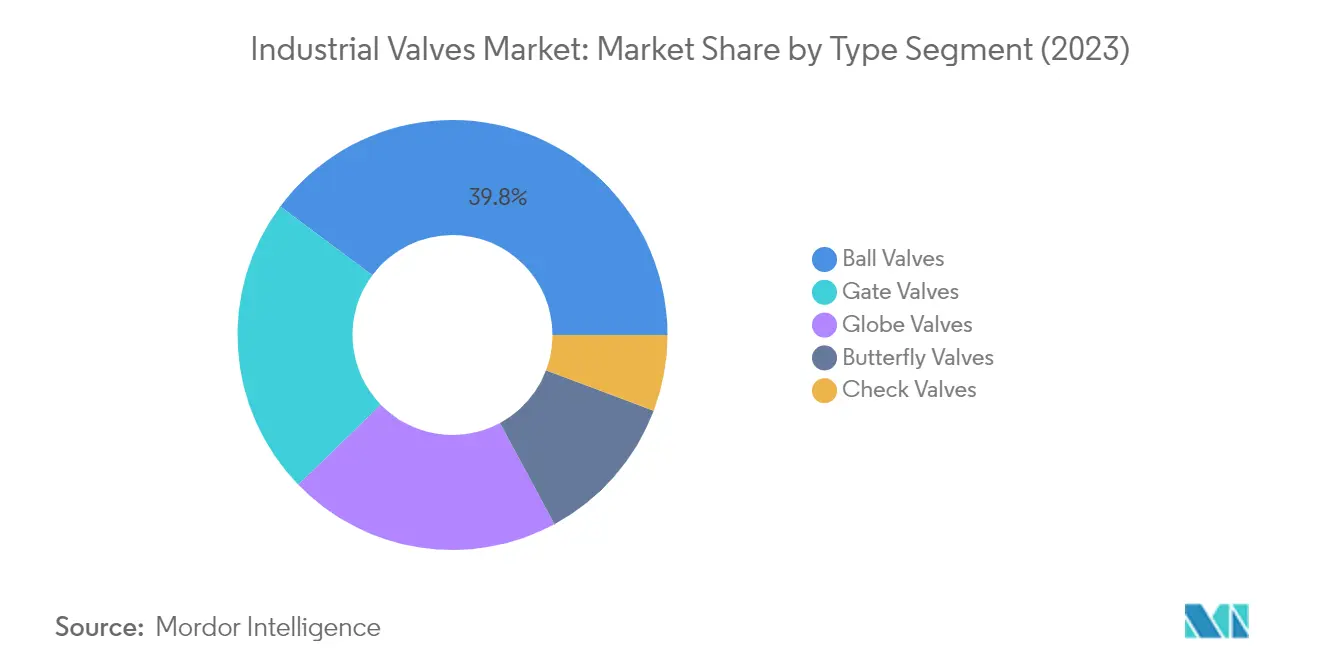

Ball valves continue to dominate the industrial valves market, commanding approximately 40% of the total market share in 2024. These valves are most commonly used for on-off or isolation service applications where straight-line flow and minimum restriction are required. The segment's prominence can be attributed to several key advantages, including straight-through flow characteristics, low turbulence, minimal operating torque requirements, tight closure capabilities, and compact design features. Ball valves find extensive applications across various industries, including oil and gas, chemical processing, petrochemical facilities, refinery operations, pulp and paper manufacturing, power generation plants, and water treatment facilities. The segment's growth is particularly driven by their superior sealing performance, reliability in high-pressure applications, and versatility in handling different types of fluids and gases.

Check Valves Segment in Industrial Valves Market

The check valves segment is experiencing the most rapid growth in the industrial valves market, with an expected growth rate of approximately 7% during 2024-2029. This remarkable growth is primarily driven by the increasing demand for backflow prevention solutions across various industrial applications. Check valves play a crucial role in preventing product contamination, equipment damage, and safety hazards by preventing reverse flow in processing systems. The segment's growth is further bolstered by their extensive use in water treatment systems, pumps and compressors, HVAC systems, and chemical processing facilities. The rising adoption of these valves in critical applications where maintaining unidirectional flow is essential, combined with technological advancements in valve design and materials, continues to drive the segment's expansion.

Remaining Segments in Industrial Valves Market by Type

The industrial valves market encompasses several other significant segments, including butterfly valves, gate valves, and globe valves, each serving distinct industrial applications. Butterfly valves are valued for their lightweight properties and efficient flow control in a compact design, making them ideal for large-flow applications. Gate valves are primarily utilized for the straight-line flow of fluids with minimum restriction, particularly in applications requiring minimal pressure drop. Globe valves excel in applications requiring precise flow regulation and frequent operation, offering superior throttling capabilities. These segments collectively contribute to the market's diversity, serving various industrial needs from basic on-off operations to complex flow control requirements across different pressure and temperature conditions.

Segment Analysis: By Sub-Type

Manual Valves Segment in Industrial Valves Market

Manual valves continue to dominate the industrial valves market, holding approximately 69% of the total market share in 2024. These valves, operated by lever or gear mechanisms, are preferred across various industries due to their reliability, cost-effectiveness, and straightforward operation. The segment's dominance is attributed to their widespread application in traditional industrial processes, lower initial investment costs compared to automated alternatives, and their suitability for applications where frequent valve operations are not required. Manual valves are particularly prevalent in smaller installations, maintenance operations, and industries where automated solutions may not be economically justified. The segment's strong position is further reinforced by their lower maintenance requirements, longer service life, and the ability to operate without external power sources, making them ideal for remote locations and emergency backup systems.

Automated Valves Segment in Industrial Valves Market

The automated valves segment is experiencing rapid growth in the industrial valves market, with an expected growth rate of approximately 6% between 2024 and 2029. This accelerated growth is driven by increasing industrial automation, the need for precise flow control, and a growing emphasis on operational efficiency. The segment encompasses various technologies, including electrical actuators (MOVs), pneumatic valves, and electro-hydraulic valves, each serving specific industrial applications. The adoption of automated valves is particularly strong in industries requiring precise control, remote operation capabilities, and integration with digital control systems. The growth is further fueled by Industry 4.0 initiatives, the rise of smart manufacturing, and an increasing focus on reducing human intervention in hazardous environments. The segment's expansion is also supported by technological advancements in valve automation, improved reliability of automated systems, and the growing need for real-time monitoring and control in industrial processes.

Segment Analysis: By End-User Industry

Oil and Gas Segment in Industrial Valves Market

The oil and gas industry continues to dominate the industrial valves market, commanding approximately 35% of the total market share in 2024. This significant market position is driven by the extensive use of valves across various applications, including onshore oil and gas production processes, offshore production processes, natural gas treatment, oil and gas transportation, and downstream refinery operations. The segment's strength is particularly evident in regions with substantial oil and gas infrastructure development, such as the Middle East, North America, and Asia-Pacific. The demand is further bolstered by ongoing investments in pipeline infrastructure, refinery expansions, and new oil and gas processing facilities across these regions. The segment's robust performance is also attributed to the increasing focus on safety regulations and the need for high-performance valves capable of handling extreme pressures and temperatures in oil and gas operations.

New Energy Segment in Industrial Valves Market

The new energy segment, encompassing hydrogen, wind, solar, geothermal energy, and bioenergy applications, is emerging as the fastest-growing segment in the industrial valves market, with an expected growth rate of approximately 9% from 2024 to 2029. This remarkable growth is primarily driven by the global shift towards renewable energy sources and the increasing investments in clean energy infrastructure. The segment's expansion is particularly notable in regions with aggressive renewable energy targets, such as Europe and Asia-Pacific. The demand for specialized valves in hydrogen infrastructure, solar thermal plants, and geothermal power facilities is increasing significantly. The growth is further accelerated by technological advancements in valve designs specifically tailored for renewable energy applications, along with supportive government policies and initiatives promoting clean energy adoption worldwide.

Remaining Segments in End-User Industry

The industrial valves market encompasses several other significant segments, including water and wastewater management, power generation, and chemical industries. The water and wastewater management segment plays a crucial role in municipal infrastructure and industrial water treatment applications, with an increasing focus on water conservation and treatment efficiency. The power generation segment remains vital for both conventional and nuclear power plants, requiring specialized valves for steam handling and cooling systems. The chemical industry segment continues to demand high-performance valves for handling corrosive materials and maintaining precise flow control in various chemical processing applications. Each of these segments contributes uniquely to the market's dynamics, driven by factors such as urbanization, industrialization, and increasing environmental regulations across different regions.

Industrial Valves Market Geography Segment Analysis

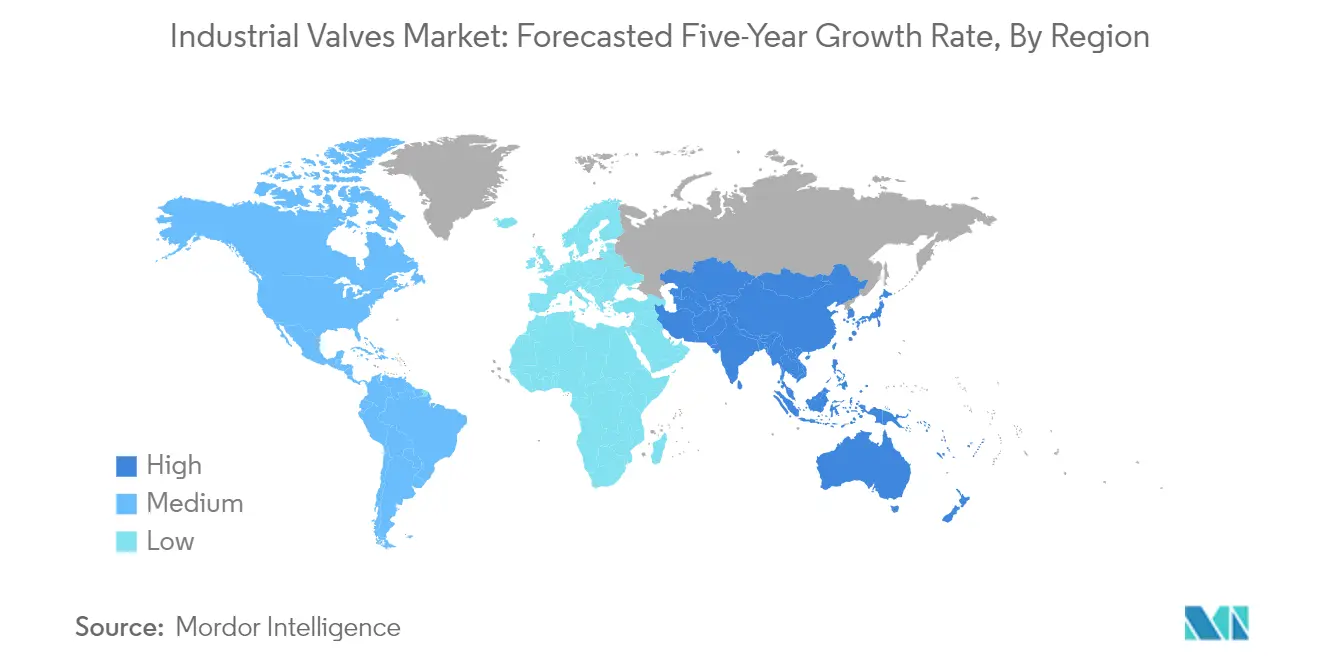

Industrial Valves Market in Asia-Pacific

The Asia-Pacific region represents a dominant force in the global industrial valve market, encompassing major economies like China, India, Japan, and South Korea. The region's market dynamics are shaped by extensive industrial development, rapid urbanization, and significant investments in water treatment infrastructure. Manufacturing capabilities, particularly in China and Japan, combined with growing industrial automation across sectors, have created a robust demand environment. The presence of major industrial valve manufacturers and an increasing focus on technological advancement further strengthen the region's market position.

Industrial Valves Market in China

China stands as the powerhouse of the Asia-Pacific industrial valve market, commanding approximately 59% of the regional market share. The country's dominance is driven by its massive industrial base, extensive oil and gas infrastructure, and growing chemical processing sector. China's market is characterized by strong domestic manufacturing capabilities, with numerous local players competing alongside international industrial valve manufacturers. The country's continued investment in water treatment facilities, power generation infrastructure, and chemical processing plants maintains steady demand for industrial valves across various applications.

Industrial Valves Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 7% during 2024-2029. The country's rapid industrial expansion, particularly in sectors like petrochemicals, water treatment, and power generation, drives this growth. India's government initiatives promoting manufacturing and infrastructure development, coupled with increasing investments in water and wastewater treatment projects, create substantial opportunities for industrial valve manufacturers. The country's focus on modernizing its industrial infrastructure and expanding its manufacturing capabilities continues to boost demand for various types of industrial valves.

Industrial Valves Market in North America and Latin America

The North America and Latin America region represents a mature yet dynamic industrial valve market, encompassing key economies like the United States, Canada, Mexico, Brazil, Argentina, and Chile. The region's market is characterized by advanced industrial infrastructure, stringent regulatory standards, and high technological adoption rates. The presence of major oil and gas installations, chemical processing facilities, and water treatment plants drives consistent demand for industrial valves. The region benefits from ongoing industrial modernization efforts and an increasing focus on energy efficiency across various sectors.

Industrial Valves Market in United States

The United States dominates the North American and Latin American industrial valve market, holding approximately 58% of the regional market share. The country's leadership position is supported by its extensive industrial infrastructure, particularly in the oil and gas sector, chemical processing, and water treatment facilities. The US market is characterized by high technological adoption rates, stringent quality standards, and a strong presence of major industrial valve manufacturers. The country's continued investment in infrastructure modernization and industrial automation maintains robust demand for advanced valve solutions.

Industrial Valves Market in United States - Growth Perspective

The United States also leads the region's growth trajectory, with a projected growth rate of approximately 4% during 2024-2029. This growth is driven by increasing investments in industrial automation, ongoing modernization of water infrastructure, and expansion of chemical processing facilities. The country's focus on energy efficiency and environmental compliance creates demand for advanced control valve technologies. The growing adoption of smart ball valves and an increasing focus on predictive maintenance in industrial applications further supports market expansion in the United States.

Industrial Valves Market in Europe

Europe maintains a significant presence in the global industrial valve market, with Germany, the United Kingdom, Italy, and France serving as key markets. The region's industrial valve sector is characterized by high technological sophistication, a strong focus on innovation, and stringent quality standards. The presence of established manufacturers, coupled with advanced industrial infrastructure across various sectors, drives market development. The region's emphasis on environmental sustainability and energy efficiency influences valve design and applications.

Industrial Valves Market in Germany

Germany leads the European industrial valve market, driven by its robust manufacturing sector, advanced chemical industry, and significant investments in water treatment infrastructure. The country's market is characterized by high-quality standards, technological innovation, and strong export capabilities. German manufacturers are known for their precision engineering and advanced ball valve solutions, particularly in specialized applications for chemical processing and water treatment sectors.

Industrial Valves Market in Germany - Growth Perspective

Germany also demonstrates the strongest growth potential in the European region, supported by continuous industrial modernization and increasing adoption of advanced industrial control valve technologies. The country's focus on Industry 4.0 initiatives and sustainable industrial practices drives demand for smart and energy-efficient valve solutions. Investments in renewable energy infrastructure and water treatment facilities further contribute to market expansion.

Industrial Valves Market in Middle East and Africa

The Middle East and Africa region presents a diverse market landscape for industrial valves, encompassing countries like Saudi Arabia, South Africa, Tanzania, Ethiopia, the Democratic Republic of the Congo, Nigeria, Guinea, and Botswana. The region's market is primarily driven by oil and gas infrastructure, water desalination projects, and growing industrial development. Saudi Arabia emerges as the largest market in the region, benefiting from extensive petrochemical infrastructure and water treatment facilities. Meanwhile, South Africa shows the fastest growth potential, supported by increasing investments in water infrastructure and industrial development projects.

Get Analysis on Important Geographic Markets

Download PDF

Industrial Valves Industry Overview

Top Companies in Industrial Valves Market

The industrial valves market is led by established players like Emerson Electric Co., Flowserve Corporation, SLB, KITZ Corporation, and Crane Company, who collectively maintain a significant market presence. Companies are increasingly focusing on product innovation through enhanced valve designs, smart technologies, and digital integration capabilities to meet evolving industry demands. Operational agility is being achieved through strategic manufacturing facility expansions, strengthening of distribution networks, and development of localized production capabilities. Market leaders are pursuing strategic moves including mergers, acquisitions, and partnerships to expand their product portfolios and geographical reach. Companies are also emphasizing sustainability initiatives, investing in R&D for eco-friendly valve solutions, and developing products that support energy transition goals across various industries.

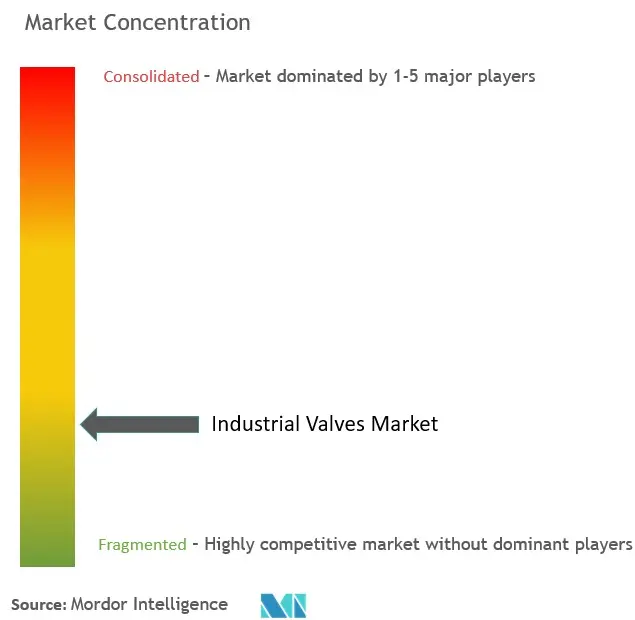

Fragmented Market with Strong Regional Players

The industrial valve market exhibits a highly fragmented structure with a mix of global conglomerates and specialized regional manufacturers. Global players leverage their extensive distribution networks, comprehensive product portfolios, and strong technological capabilities to maintain market leadership, while regional players compete through specialized offerings and a deep understanding of local market requirements. The market is characterized by ongoing consolidation activities, with larger companies actively acquiring smaller specialized manufacturers to enhance their technological capabilities and expand their market presence.

Recent years have witnessed significant merger and acquisition activities aimed at portfolio diversification and geographical expansion. Companies are particularly focused on acquiring businesses that complement their existing product lines or provide access to new technologies and markets. These strategic moves are reshaping the competitive landscape, with companies seeking to strengthen their positions in high-growth regions and emerging market segments while maintaining their core market presence.

Innovation and Adaptability Drive Market Success

Success in the industrial valve market increasingly depends on companies' ability to innovate and adapt to changing industry requirements. Incumbent players are focusing on developing comprehensive solution offerings that combine traditional valve products with digital capabilities, while also expanding their aftermarket services and support networks. Companies are investing in research and development to create more efficient, reliable, and sustainable valve solutions, while also strengthening their manufacturing capabilities to ensure consistent quality and timely delivery.

Market contenders can gain ground by focusing on specialized market segments, developing innovative solutions for specific applications, and building strong relationships with end-users. The relatively low threat of substitution products provides stability, but companies must navigate varying certification requirements and policies across different regions and industries. Success also depends on the ability to manage supply chain complexities, maintain cost competitiveness, and adapt to evolving environmental regulations and industry standards. Additionally, the integration of control valve technologies and process valve solutions is becoming increasingly crucial for meeting specific application needs and enhancing operational efficiency.

Industrial Valves Market Leaders

-

Emerson Electric Co.

-

Flowserve Corporation

-

Crane Co.

-

IMI

-

SLB

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Industrial Valves Market News

- September 2023: Danfoss India opened a new India distribution center in Chennai, India, that is spread over 43,000 square feet and has a 4,000 pallet position facility to support growth plans. This new distribution unit will likely aggregate Danfoss products from Asia, Europe, Latin America, and Denmark.

- February 2023: Flowserve Corporation acquired Velan Inc. in an all-cash transaction valued at USD 245 million, including the purchase of all of the issued and outstanding Velan equity and the assumption. The acquisition added significant value to Flowserve Corporation’s existing valves portfolio.

- November 2022: IMI Saudi Industry, a subsidiary of IMI Critical Engineering, unveiled a new 5,000 m2 facility in Dammam. The facility was expected to supply innovative valve solutions and strengthen national manufacturing capabilities, in line with the Saudi Arabian government's plans to localize key products.

- November 2022: James Walker introduced the Supagraf HT valve stem seal for molten salt media. It could bear ultra-high temperatures combined with chemically aggressive and corrosive media such as molten salts, providing some of the most demanding conditions for valves, process equipment, and products used to seal such applications.

Industrial Valves Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Demand from the Power and Chemical Industry

- 4.1.2 Increase in Demand for Desalination Activity

-

4.2 Restraints

- 4.2.1 Stagnant Industrial Growth in Developed Countries

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

-

5.1 Type

- 5.1.1 Butterfly Valve

- 5.1.2 Ball Valve

- 5.1.3 Globe Valve

- 5.1.4 Gate Valve

- 5.1.5 Plug Valve

- 5.1.6 Other Types

-

5.2 Product

- 5.2.1 Quarter-turn Valve

- 5.2.2 Multi-turn Valve

- 5.2.3 Other Products

-

5.3 Application

- 5.3.1 Power

- 5.3.2 Water and Wastewater Management

- 5.3.3 Chemicals

- 5.3.4 Oil and Gas

- 5.3.5 Other Applications (Includes Food Processing, Mining, and Marine)

-

5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Indonesia

- 5.4.1.6 Vietnam

- 5.4.1.7 Malaysia

- 5.4.1.8 Thailand

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 NORDIC

- 5.4.3.6 Turkey

- 5.4.3.7 Russia

- 5.4.3.8 Spain

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Qatar

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 ALFA LAVAL

- 6.4.2 AVK Holding AS

- 6.4.3 CIRCOR International Inc.

- 6.4.4 Crane Co.

- 6.4.5 Curtiss-Wright Corporation

- 6.4.6 Danfoss AS

- 6.4.7 Zhejiang Dunan Valve Co. Ltd.

- 6.4.8 Emerson Electric Co.

- 6.4.9 Flowserve Corporation

- 6.4.10 Baker Hughes

- 6.4.11 Georg Fischer Ltd.

- 6.4.12 Hitachi Ltd

- 6.4.13 Honeywell International Inc.

- 6.4.14 IMI

- 6.4.15 ITT Inc.

- 6.4.16 KITZ Corporation

- 6.4.17 KLINGER Group

- 6.4.18 Mueller Water Products Inc.

- 6.4.19 NIBCO Inc.

- 6.4.20 Okano Valve Mfg. Co. Ltd.

- 6.4.21 Saint-Gobain

- 6.4.22 SLB

- 6.4.23 TechnipFMC PLC

- 6.4.24 The Weir Group PLC

- 6.4.25 Valvitalia SpA

- 6.4.26 Xylem

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase in Demand for Automatic Valves

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Industrial Valves Industry Segmentation

Industrial valves are mechanical devices that open, close, or partially obstruct passageways to regulate the flow of liquid or gas within a system.

The industrial valve market is segmented by type, product, application, and geography. By type, the market is segmented into butterfly valve, ball valve, globe valve, gate valve, plug valve, and other types (needle valve, etc.). By product, the market is segmented into the quarter-turn valve and multi-turn valve. By application, the market is segmented into power, water and wastewater management, chemicals, oil and gas, and other applications, including food processing, mining, and marine. The report also covers the market size and forecasts for the market in 27 countries across major regions.

For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Type | Butterfly Valve | ||

| Ball Valve | |||

| Globe Valve | |||

| Gate Valve | |||

| Plug Valve | |||

| Other Types | |||

| Product | Quarter-turn Valve | ||

| Multi-turn Valve | |||

| Other Products | |||

| Application | Power | ||

| Water and Wastewater Management | |||

| Chemicals | |||

| Oil and Gas | |||

| Other Applications (Includes Food Processing, Mining, and Marine) | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Indonesia | |||

| Vietnam | |||

| Malaysia | |||

| Thailand | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| NORDIC | |||

| Turkey | |||

| Russia | |||

| Spain | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| United Arab Emirates | |||

| Qatar | |||

| Nigeria | |||

| Egypt | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Industrial Valves Market Research FAQs

How big is the Industrial Valves Market?

The Industrial Valves Market size is expected to reach USD 74.18 billion in 2025 and grow at a CAGR of 4.52% to reach USD 92.53 billion by 2030.

What is the current Industrial Valves Market size?

In 2025, the Industrial Valves Market size is expected to reach USD 74.18 billion.

Who are the key players in Industrial Valves Market?

Emerson Electric Co., Flowserve Corporation, Crane Co., IMI and SLB are the major companies operating in the Industrial Valves Market.

Which is the fastest growing region in Industrial Valves Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Industrial Valves Market?

In 2025, the Asia Pacific accounts for the largest market share in Industrial Valves Market.

What years does this Industrial Valves Market cover, and what was the market size in 2024?

In 2024, the Industrial Valves Market size was estimated at USD 70.83 billion. The report covers the Industrial Valves Market historical market size for years: 2024. The report also forecasts the Industrial Valves Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Industrial Valves Market Research

Mordor Intelligence provides comprehensive market research and consulting expertise in the industrial valve sector. Our detailed analysis covers the global valve industry extensively. We explore the full range of process valve technologies, including ball valve, gate valve, check valve, butterfly valve, and globe valve products. The report offers in-depth insights into industrial control valve systems. It examines both manual valve and automatic valve technologies, along with emerging smart valve solutions for industrial flow control applications.

Our detailed analysis is available as an easy-to-read report PDF for download. It examines crucial applications across oil and gas valve installations, power plant valve systems, and water treatment valve facilities. The report explores various control mechanisms, including pneumatic valve, hydraulic valve, and flow control valve technologies. It also analyzes process control equipment developments. Stakeholders gain valuable insights into pipeline valve trends, pressure control valve innovations, and actuated valve systems. This enables informed decision-making across the industrial fluid control landscape. The comprehensive coverage includes safety valve requirements and emerging opportunities in the evolving control valve market.