Industrial Rubber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

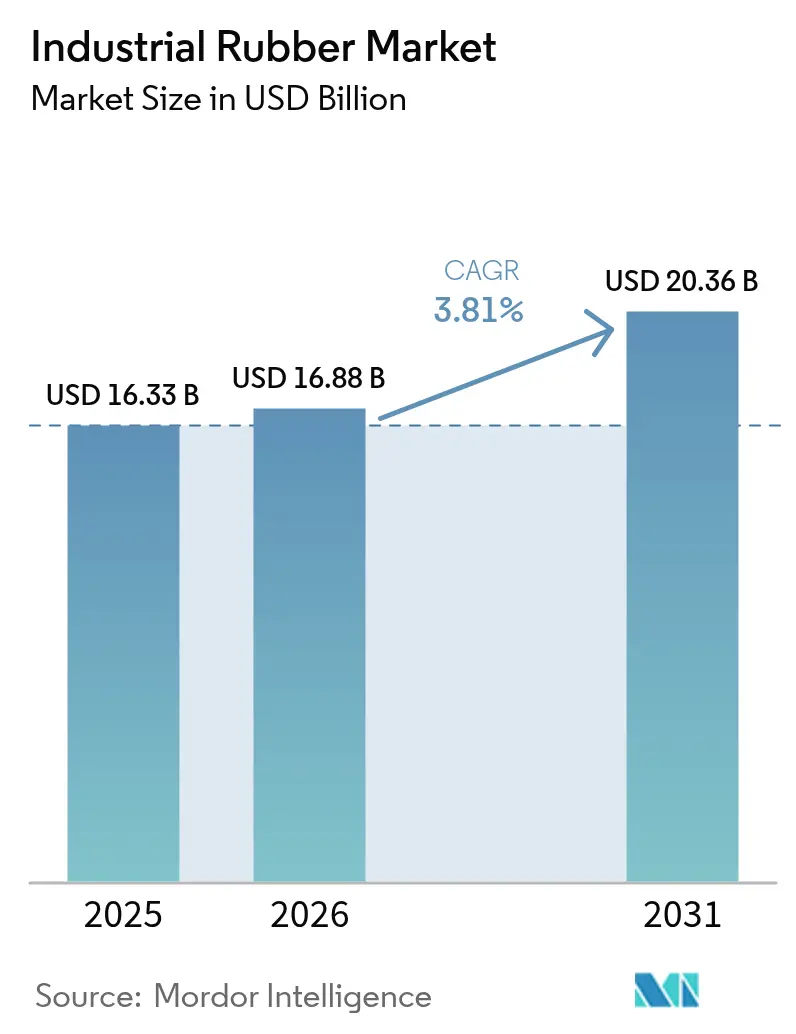

| Market Size (2026) | USD 16.88 Billion |

| Market Size (2031) | USD 20.36 Billion |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Rubber Market Analysis by Mordor Intelligence

The Industrial Rubber Market size is projected to expand from USD 16.33 billion in 2025 and USD 16.88 billion in 2026 to USD 20.36 billion by 2031, registering a CAGR of 3.81% between 2026 to 2031. Electrified vehicles, digitalized compounding lines, and circular-economy mandates are reshaping the industrial rubber market as suppliers replace traditional EPDM with lighter thermoplastic elastomers, embed IoT sensors in mixing mills, and scale reclaimed-rubber devulcanization plants. At the same time, butadiene price swings between USD 800 and USD 1,200 per ton in 2024 forced producers to hedge feedstock risk while accelerating bio-based alternatives. Synthetic grades still dominate, yet reclaimed rubber is advancing at 5.06% annually because EU microplastics rules and China’s Green Manufacturing Action Plan reward closed-loop material flows. Demand is also rising for flame-retardant, high-tensile conveyor belts in new mining corridors across Indonesia, Chile, and South Africa that must meet ISO 340/14890 standards. Asia-Pacific remains the production and consumption hub as Belt and Road corridors add infrastructure megaprojects and India lifts vehicle output toward 5 million units, sustaining tier-1 investment in local sealing, hose, and vibration-control capacity.

Key Report Takeaways

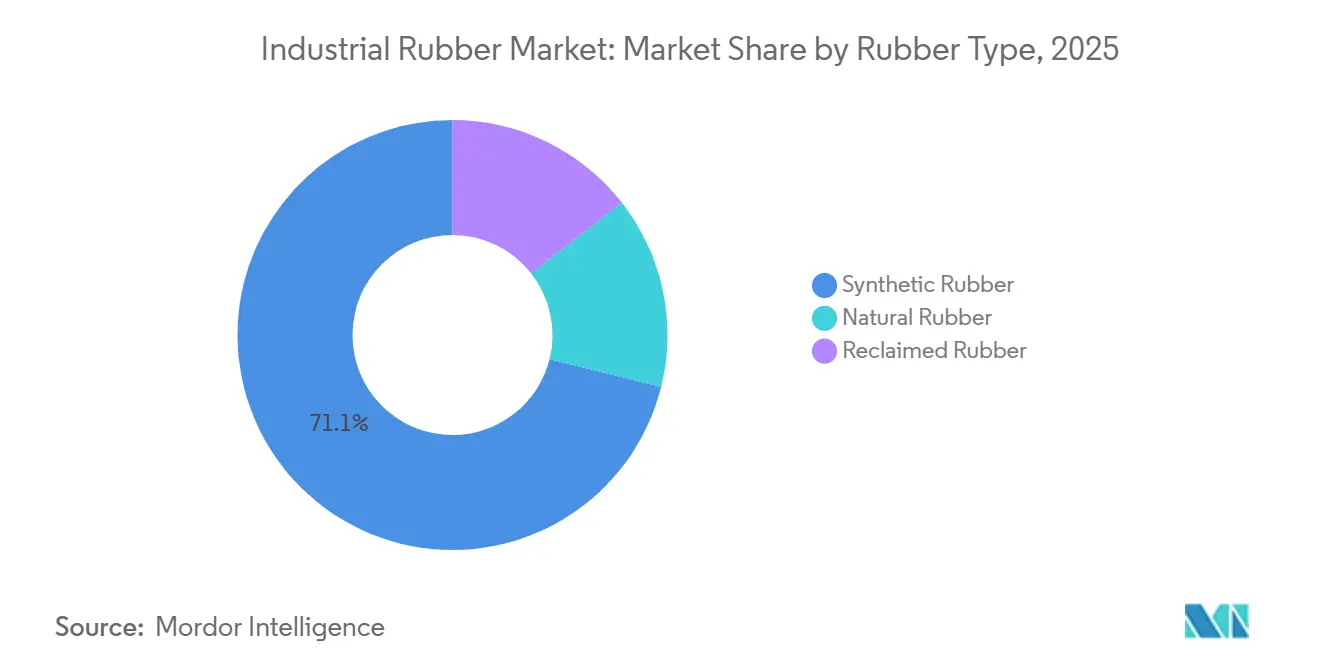

- By rubber type, synthetic rubber led with 71.12% of the industrial rubber market share in 2025, while reclaimed rubber posted the highest projected CAGR at 5.06% to 2031.

- By process, extrusion commanded 45.18% share of the industrial rubber market size in 2025; 3D printing is set to expand the fastest at a 4.20% CAGR.

- By application, conveyor belts accounted for 38.67% of the industrial rubber market size in 2025 and are also advancing at a 4.91% CAGR through 2031.

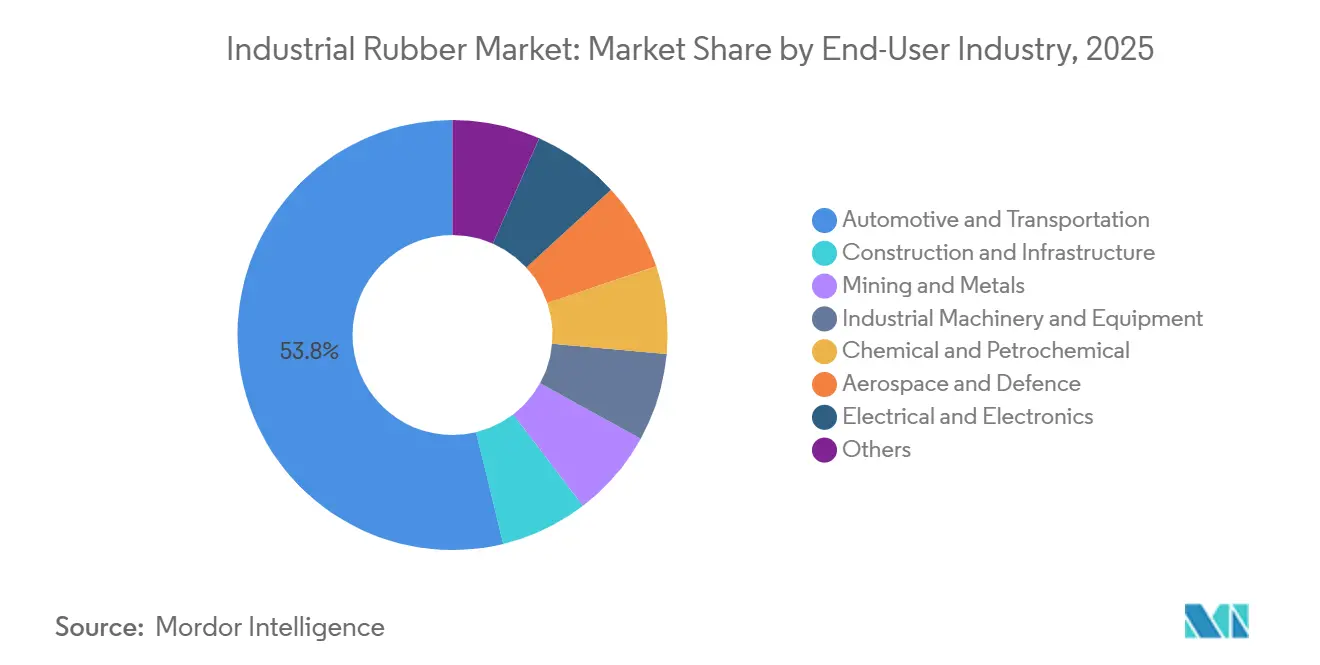

- By end-user industry, automotive and transportation held 53.78% share of the industrial rubber market size in 2025, while aerospace and defense is projected to grow at 4.98% CAGR.

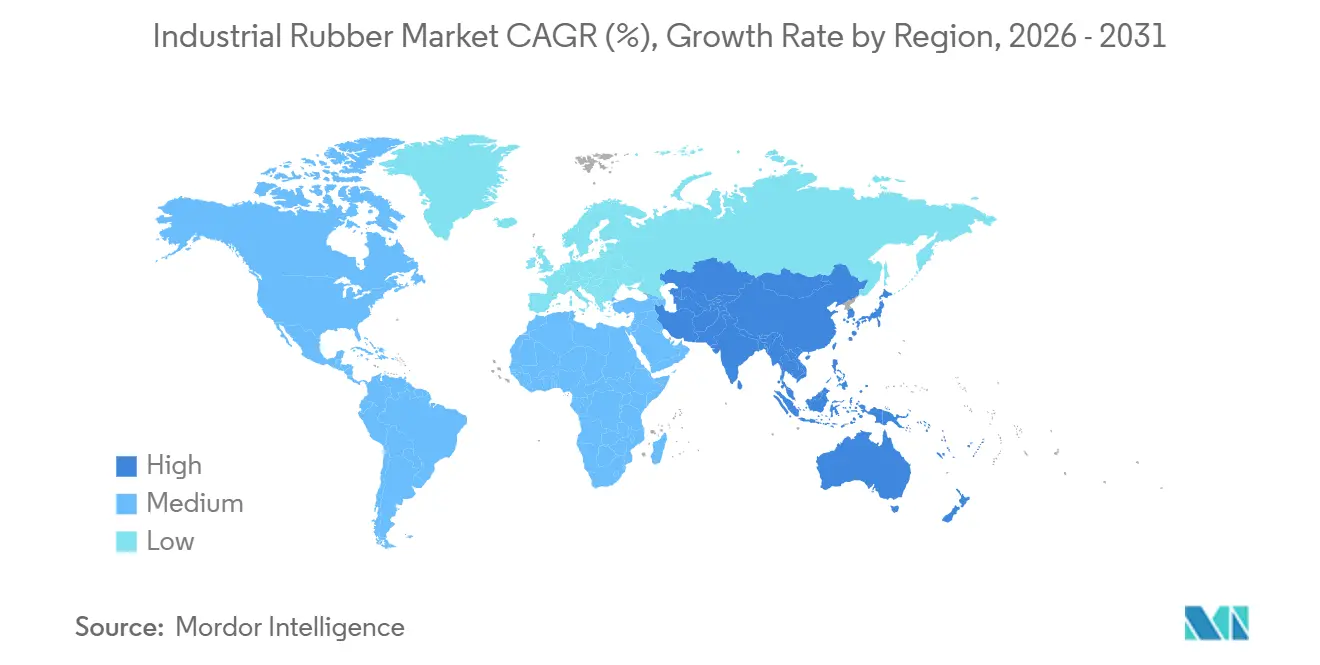

- By geography, Asia-Pacific captured 59.09% of the industrial rubber market share in 2025 and is forecast to rise at a 4.14% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Rubber Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing application as conveyor & transmission belts | +1.10% | APAC core (China, India, Indonesia), spill-over to South America (Chile, Brazil) and MEA (South Africa) | Medium term (2-4 years) |

| Growing demand for high-pressure hoses | +0.80% | Global, with concentration in North America & Middle East oil & gas sectors | Short term (≤ 2 years) |

| EV-led boom in lightweight automotive components | +1.30% | North America, EU, and China automotive manufacturing hubs | Medium term (2-4 years) |

| Infrastructure build-out in emerging economies | +1.00% | APAC (India, Southeast Asia), Middle East (Saudi Arabia, UAE), Africa (Egypt, Nigeria) | Long term (≥ 4 years) |

| Adoption of Industry 4.0 smart rubber-compounding lines | +0.60% | APAC (China, Japan, South Korea), expanding to EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Application as Conveyor & Transmission Belts

Mining, bulk-handling, and e-commerce logistics are switching to steel-cord rubber belts rated above 3,150 N/mm and able to run at ambient temperatures beyond 60°C, spurring specification upgrades in Asia-Pacific and South America. Indonesia’s 1.8 million-ton nickel surge in 2024 accelerated orders for flame-retardant belts compliant with ISO 340 to mitigate underground fire risk. Chile’s 5.3 million-ton copper output retrofit legacy conveyors with low-rolling-resistance belts that cut drive-motor loads 15%. Transmission belts are also evolving, with aramid-fiber reinforcement replacing cotton canvas in high-speed CNC machining centers and automated packaging lines. Embedded RFID tags now allow operators to replace belts based on real-time wear data, lowering the total cost of ownership.

Growing Demand for High-Pressure Hoses

Hydraulic assemblies rated above 350 bar are expanding in offshore oil, subsea construction, and mobile hydraulics as equipment operates at higher loads[1]Parker Hannifin, “787TC High-Pressure Hose,” parker.com. Parker Hannifin’s 787TC hose, launched in 2024, delivers 420 bar working pressure and a 6:1 safety factor under SAE 100R13 and EN 856 4SP. Middle-East crackers commissioned in 2025 specify fluoropolymer-lined hoses for corrosive transfers, a niche growing faster than overall hydraulics. North America’s shale basins, averaging 98 bcf/day in 2025, require hoses able to withstand 10,000 pressure cycles, reinforcing ISO 18752 compliance in new tenders.

EV-Led Boom in Lightweight Automotive Components

Battery-electric vehicle architectures are forcing a redesign of sealing, vibration-isolation, and thermal-management parts, accelerating demand for thermoplastic elastomers and fluoroelastomers that deliver equivalent durability at up to 44% lower mass[2]Cooper Standard, “FlexiCore Lightweight Sealing,” cooperstandard.com. Cooper Standard’s FlexiCore body-sealing system, commercialized in 2024, cut weight by 44% by replacing solid EPDM with foam-core profiles, boosting vehicle range without compromising NVH. Continental’s air-spring modules for electric trucks introduced in 2025 lower lifecycle CO₂ emissions by 50% through material optimization. Rising EV volumes above 20 million units by 2027 are prompting tier-1s to add clean-room molding capacity and seek IATF 16949 certification for battery-pack gaskets that must cycle between -40°C and 125°C while retaining IP67 integrity.

Adoption of Industry 4.0 Smart Rubber-Compounding Lines

IoT sensors and machine-learning algorithms are reducing formulation variance below 1% and cutting scrap by 22% in German InSuKa pilots launched in 2024. The EUR 8.5 million DIPONI consortium running 2025-2029 pairs extrusion digital twins with dynamic die-swell prediction to shave product-development lead times to under 12 months. Japanese plants now use inline rheometers to replace manual Mooney tests, boosting throughput and batch consistency for auto-OEM contracts. China labeled 15 rubber factories “smart manufacturing demonstration facilities” in 2025, backing MES platforms and predictive maintenance rollouts.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental regulations | -0.70% | EU (REACH, microplastics ban), North America (EPA VOC limits), China (Green Manufacturing) | Short term (≤ 2 years) |

| Volatile crude-oil-linked feedstock prices | -0.50% | Global, with acute impact on synthetic rubber producers in APAC and North America | Short term (≤ 2 years) |

| Rapid uptake of reclaimed rubber | -0.40% | EU (circular economy mandates), China (Extended Producer Responsibility), North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Regulations

The EU’s 2023 microplastics restriction phases out rubber granules <5 mm in turf and flooring, adding EUR 50,000-150,000 per product for third-party testing and dossiers to national authorities. REACH Annex XVII limits eight PAHs to 1 mg/kg, forcing tire and belt makers to source low-aromatic process oils and raising raw-material spend by 8-12%. China’s 2024 Green Manufacturing update mandates a 15% VOC reduction per ton of rubber by 2027, driving investment in solvent-recovery systems. The U.S. EPA’s proposed 65 ppb ozone cap under review in 2025 could require USD 2 million-5 million per site for abatement gear in non-attainment areas.

Volatile Crude-Oil-Linked Feedstock Prices

Butadiene tracked crude swings of 40-50% in 2024, reaching USD 1,200 per ton in Northeast Asia and compressing synthetic-rubber margins under fixed OEM supply contracts. Monthly feedstock volatility versus quarterly contract resets is forcing compounders to hedge and multi-source, adding 2-3% to working capital. Natural-rubber prices also fluctuated with erratic monsoons in Thailand and Indonesia, whose plantations supplied 6.2 million tons in 2024. Producers are trialing bio-isoprene despite 20-30% cost premiums to cut reliance on petrochemicals.

Segment Analysis

By Rubber Type: Synthetic Dominance Meets Circular Pressure

Synthetic rubber commanded a 71.12% industrial rubber market share in 2025 as SBR remained the workhorse for abrasion-resistant hoses and seals, while nitrile captured premium fuel-system demand. Reclaimed rubber, however, is expanding 5.06% annually as EU directives push for 25% recycled content by 2030 and China’s EPR scheme incentivizes tire makers to close loops. Tyromer and Genan devulcanize waste tires to recover 70-80% of virgin properties, making reclaimed viable for mats and roofing, but still constrained by ISO 1795 testing gaps that limit use in automotive safety parts.

Feedstock volatility and microplastics scrutiny are prompting compounders to blend synthetic, natural, and reclaimed grades for balanced performance and cost. Fluoro- and silicone-based elastomers, though niche, are outgrowing the broader industrial rubber market at mid-single-digit rates thanks to semiconductor cleanroom, aerospace fuel-system, and medical-device demand where thermal stability is paramount.

Note: Segment shares of all individual segments available upon report purchase

By Process: Extrusion Leads, Additive Manufacturing Disrupts

Extrusion represented 45.18% of the industrial rubber market size in 2025 because of its scalability for profiles, hoses, and weather-strips. Twin-screw lines with inline rheology sensors now cut setup waste by 30% by adapting die geometry in real time. Molding and casting continue to serve high-tolerance engine mounts and vibration isolators, with liquid silicone injection gaining medical and food-contact share under FDA 21 CFR 177.2600 compliance.

Additive manufacturing is advancing 4.20% as Stratasys TPU 92A gained aerospace certification in 2024, allowing on-demand fabrication of gaskets and seals with 500% elongation. The US Department of Defense standard MIL-STD-3049 accelerates material qualification for field maintenance prints, expanding defense demand. Calendaring, vital for conveyor-belt covers and roofing membranes, is integrating embossing and laminating in a single pass to raise line speed and material utilization.

By Application: Conveyor Belts Drive Volume and Growth

Conveyor belts accounted for 38.67% of application revenue in 2025 and will grow 4.91% annually on mining CAPEX, logistics automation, and infrastructure megaprojects across Asia-Pacific and South America. Steel-cord belts spanning 10 km in Australia and Chile now handle >5,000 t/h under extreme heat and UV, requiring ozone-resistant compounds. Transmission belts evolve from wrapped V-belts to aramid-reinforced synchronous belts that eliminate slip in high-speed machinery.

Pressure hoses benefit from offshore wind installations, global capacity hit 75 GW in 2025, which need seawater-resistant assemblies with integrated pressure sensors for ISO 18752 traceability. Roofing membranes, tubing, and rolls grow more slowly as thermoplastic or metal composites substitute in select applications, although RFID-tagged premium belts now predict splice failure 2-4 weeks ahead, cutting downtime 40%.

By End-User Industry: Automotive Leads, Aerospace Accelerates

Automotive and transportation consumed 53.78% of the industrial rubber market output in 2025, buoyed by 88 million global light-vehicle builds and EV-specific sealing needs. Aerospace and defense, while smaller, posts a 4.98% CAGR as next-gen aircraft and UAV programs require lightweight fire-resistant seals that meet AS9100 standards.

Construction and infrastructure absorb steady demand for bridge bearings and expansion joints as the Asia-Pacific invests USD 1.7 trillion annually. Mining specifies flame-retardant, abrasion-resistant belts and slurry hoses as Indonesia’s nickel and Chile’s copper projects scale. Industrial machinery, chemical processing, and electrical applications drive precision-molded parts in high-temperature, corrosive, and low-smoke environments, while packaging and consumer goods test bio-based elastomers despite 20-30% cost premiums.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific held 59.09% of global industrial rubber market demand in 2025, expanding at a forecast 4.14% CAGR to 2031, supported by USD 1 trillion Belt and Road infrastructure corridors and India’s Production-Linked Incentive for auto manufacturing. ASEAN states attracted USD 890 million in approved rubber projects in 2024 as firms diversify supply chains away from China, while Japanese and Korean processors deploy digital-twin compounding lines for just-in-time auto deliveries.

North America’s share is anchored by 98 bcf/day shale gas production and a USD 1.2 trillion infrastructure program that keeps demand high for bridge bearings, roofing membranes, and high-pressure hydraulic hoses. Mexico’s 3.5 million-vehicle output is localizing rubber components to meet USMCA value rules, drawing investment into extrusion clusters in Guanajuato and Puebla.

Europe’s consumption reflects stringent REACH limits that accelerate reclaimed and bio-based uptake, while Germany’s advanced compounds supply low-VOC parts to machinery OEMs. South America relies on copper, lithium, and iron-ore extraction that needs heavy-duty belts and hoses, whereas the Middle East and Africa grow through Saudi Vision 2030 construction and South Africa’s mining-sector upgrades.

Competitive Landscape

The Industrial Rubber market is moderately fragmented. Tire majors Bridgestone, Continental, and Goodyear integrate raw materials through finished goods, while regional compounders specialize in high-pressure hoses for offshore wind and chemical processing. Regulatory agility is emerging as a moat. Firms with ISO 17025 labs can validate REACH, EPA, and Green Manufacturing compliance faster, deterring new entrants.

Industrial Rubber Industry Leaders

Bridgestone Industrial

ContiTech Deutschland GmbH

Sumitomo Rubber Industries, Ltd.

The Goodyear Tire & Rubber Company

THE YOKOHAMA RUBBER CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: In a move to bolster its off-highway tire capacity in Europe, Yokohama Rubber purchased a former tire facility in Drobeta-Turnu Severin, Romania, for USD 35 million. This acquisition aligns with the company's strategy to expand its footprint in the European market and meet growing demand in the region.

- February 2025: Goodyear unveiled a USD 320 million expansion at its Lawton, Oklahoma plant, aiming to boost production by 10 million annual units, with a focus on premium tires for EVs and autonomous vehicles. This investment underscores Goodyear's commitment to innovation and addressing the evolving needs of the mobility sector.

Global Industrial Rubber Market Report Scope

Industrial rubber is made of polymers and has a major application in end-user industries, including mining, automotive, and others. In the automotive industry, industrial rubber is mainly used as flexible shaft couplings, drive belts, high-pressure hoses, process control rubber sheets, etc. In the mining industry, it is used to make conveyors and transmission belts to carry minerals.

The industrial rubber market is segmented by rubber type, process, application, end-user industry, and geography. By rubber type, the market is segmented into natural rubber, synthetic rubber, and reclaimed rubber. By process, the market is segmented into extrusion, molding and casting, calendaring, and 3-D printing/additive manufacturing. By application, the market is segmented into conveyor belts, transmission belts, pressure hoses, and other applications (roofing, tubes, rolls, and more). By end-user industry, the market is segmented into automotive and transportation, construction and infrastructure, mining and metals, industrial machinery and equipment, chemical and petrochemical, aerospace and defence, electrical and electronics, and other end-user industries (packaging industry, and more). The report also covers the market size and forecasts in 28 countries across major regions. Market sizing and forecasts are made for each segment based on value (USD).

| Natural Rubber |

| Synthetic Rubber |

| Reclaimed Rubber |

| Extrusion |

| Molding and Casting |

| Calendaring |

| 3-D Printing / Additive Manufacturing |

| Conveyor Belts |

| Transmission Belts |

| Pressure Hoses |

| Other Application (Roofing, Tubes, Rolls, etc.) |

| Automotive and Transportation |

| Construction and Infrastructure |

| Mining and Metals |

| Industrial Machinery and Equipment |

| Chemical and Petrochemical |

| Aerospace and Defence |

| Electrical and Electronics |

| Other End-user Industries (Packaging Industry, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Malaysia | |

| Philippines | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Rubber Type | Natural Rubber | |

| Synthetic Rubber | ||

| Reclaimed Rubber | ||

| By Process | Extrusion | |

| Molding and Casting | ||

| Calendaring | ||

| 3-D Printing / Additive Manufacturing | ||

| By Application | Conveyor Belts | |

| Transmission Belts | ||

| Pressure Hoses | ||

| Other Application (Roofing, Tubes, Rolls, etc.) | ||

| By End-User Industry | Automotive and Transportation | |

| Construction and Infrastructure | ||

| Mining and Metals | ||

| Industrial Machinery and Equipment | ||

| Chemical and Petrochemical | ||

| Aerospace and Defence | ||

| Electrical and Electronics | ||

| Other End-user Industries (Packaging Industry, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Malaysia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global demand for industrial rubber be by 2031?

The industrial rubber market size is projected to reach USD 20.36 billion by 2031, advancing at a 3.81% CAGR from 2026.

Which rubber type is expanding fastest?

Reclaimed rubber is growing at a 5.06% CAGR as regulators push recycled-content mandates in Europe and China.

What drives conveyor-belt demand?

Mining CAPEX, logistics automation, and infrastructure megaprojects in Asia-Pacific and South America are raising conveyor-belt installations, driving a 4.91% CAGR through 2031.

Why are high-pressure hydraulic hoses gaining traction?

Offshore oil, subsea construction, and shale gas operations need hoses rated above 350 bar and ISO 18752 compliant to handle higher pressures and cycles.

How are environmental rules affecting producers?

EU microplastics restrictions, China VOC limits, and possible tighter U.S. ozone caps raise testing and abatement costs, collectively reducing the forecast CAGR by 0.8 percentage point.