Market Trends of Industrial Round Wood Industry

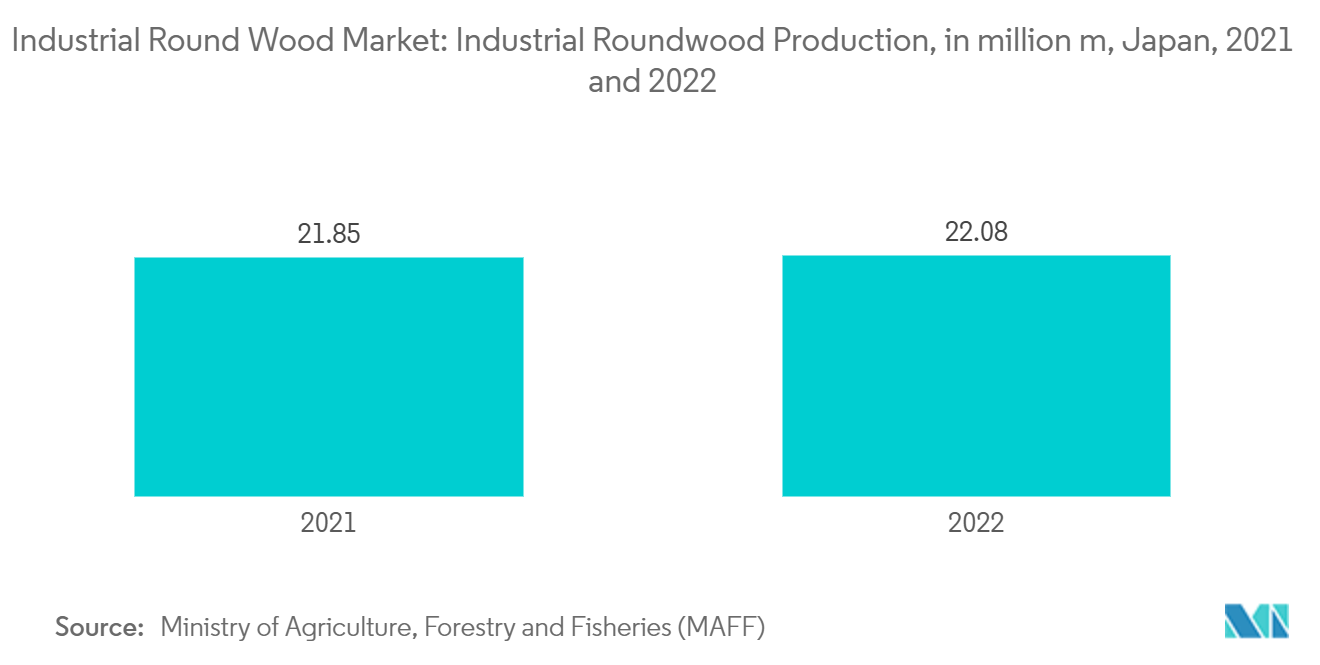

Constant Rise In The Production Of Industrial Roundwood

Consumer awareness of environmental issues and sustainability has significantly increased the demand for certified wood products. Forest certification schemes such as the Forest Stewardship Council (FSC) and the Programme for the Endorsement of Forest Certification (PEFC) have made sustainable sourcing a key driver in the roundwood market. This has enhanced certified production and overall wood product output, including roundwood. For instance, the Ministry of Agriculture, Forestry and Fisheries (MAFF) reported that Japan's roundwood production volume grew from 21.8 million cubic meters in 2021 to 22.0 million cubic meters in 2022.

Advances in forestry management and processing technologies have reduced costs and increased yields, supporting production. In 2022, Henkel Adhesive Technologies invested in 3RT, Melbourne, Australia, to strengthen its timber construction solutions. Henkel and its partners have developed a robotic process to convert forest and plantation residues into high-quality hardwood products. This investment aims to expand Henkel's Engineered Wood business and promote sustainable, future-oriented technologies.

Additionally, roundwood consumption has been growing in many regions during the study period. FAOSTAT data shows that industrial roundwood consumption in North America increased from 516 million cubic meters in 2021 to 519 million cubic meters in 2022. As demand for end products like sawlogs, veneer logs, chips, and wood residues rises, production continues to grow. Therefore, the increasing demand and effective management of roundwood are driving market growth during the forecast period.

Asia-Pacific Dominates the Global Import Market

The Asia-Pacific region, driven by rapid economic growth, industrialization, and urbanization, stands as one of the largest and most dynamic markets for industrial roundwood. The region's diverse demand for wood products—ranging from construction timber and paper products to biomass for energy—has resulted in significant roundwood imports. According to FAOSTAT, in 2022, Asia imported 39,753 thousand cubic meters of coniferous roundwood, surpassing Europe at 38,248 thousand cubic meters, with North America, Africa, and South America trailing at 440, 34, and 34 thousand cubic meters, respectively.

China, Japan, India, South Korea, and several Southeast Asian nations are major players in the Asia-Pacific roundwood market. Urban expansion in China and India is driving a surge in timber demand for housing, roads, and infrastructure, predominantly sourced from imported roundwood, especially softwood for construction framing. Notably, China's urbanization rate rose from 63.4% in 2022 to 64.5% in 2023, according to the World Bank, generating more demand for industrial round wood to accomplish the needs of urbanizing society.

Countries in the Asia-Pacific, especially in Southeast Asia, face limited domestic timber resources, making them heavily reliant on imports for industrial roundwood. This dependency is pronounced in Japan and South Korea, where domestic forests are smaller and yield less. Even timber-rich Malaysia, known for its substantial wood product exports, finds it necessary to import roundwood to satisfy its domestic processing and manufacturing needs. Consequently, the Asia-Pacific's rising local demand, coupled with inconsistent domestic supply, has fuelled its growing import activities.