Market Size of Industrial AI Software Industry

| Study Period | 2019 - 2029 |

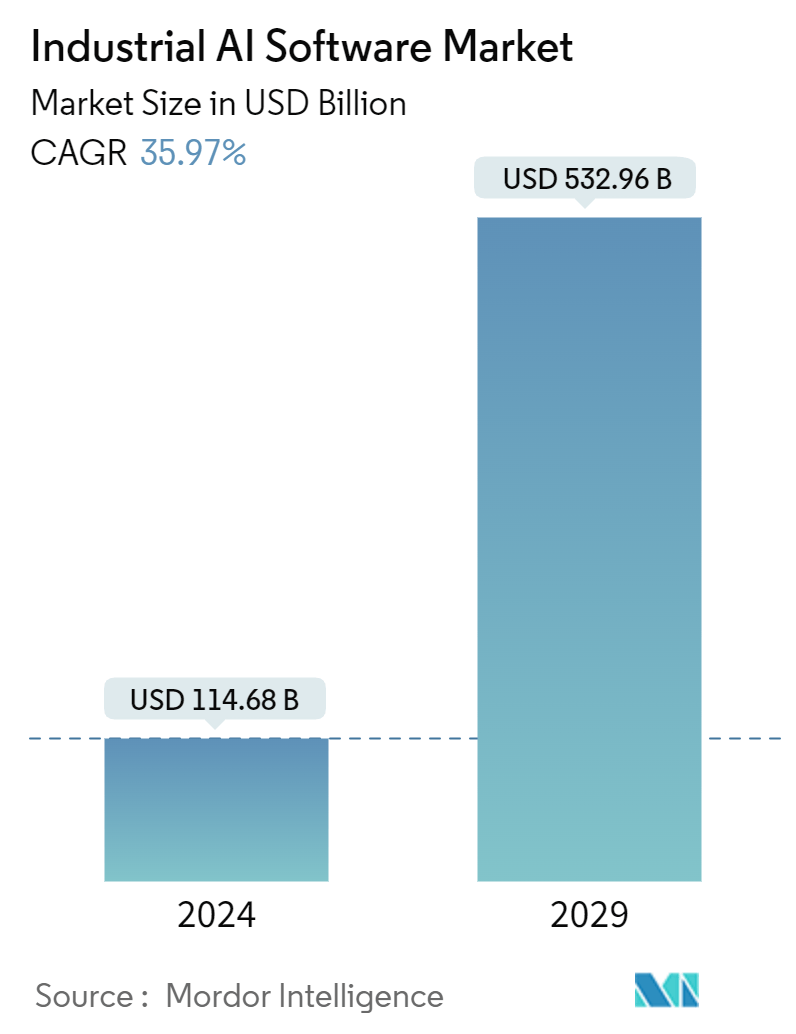

| Market Size (2024) | USD 114.68 Billion |

| Market Size (2029) | USD 532.96 Billion |

| CAGR (2024 - 2029) | 35.97 % |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Industrial AI Software Market Analysis

The Industrial AI Software Market size is estimated at USD 114.68 billion in 2024, and is expected to reach USD 532.96 billion by 2029, growing at a CAGR of 35.97% during the forecast period (2024-2029).

- Increased focus on capturing value from industrial data. This drives the need for multi-dimensional optimization, meaning AI-enabled decision-making and operational agility are becoming more critical to executives. To thrive in today's volatile market, companies must simultaneously optimize their assets and processes across business objectives such as margins, economics, sustainability, etc.

- According to the European Commission, the European AI Strategy seeks to establish the European Union (EU) as a premier AI hub and to guarantee that artificial intelligence (AI) is trustworthy and centered on people. Such a purpose is translated through specific laws and deeds into the European approach to excellence and trust. An essential part of excellence in AI is making the most of available resources and coordinating investments. The Commission intends to invest EUR1 billion annually in AI through the Digital Europe and Horizon Europe programs. Over the digital decade, it will mobilize other investments from the private sector and the Member States to reach an annual investment volume of EUR 20 billion (USD 21.41 billion).

- Although AI is still one of the critical technology areas, organizations require an efficient way to scale their AI practices and use AI in business to accelerate ROI in AI investment. As organizations face more significant pressure to optimize their workflows, more companies will ask BI teams to manage and develop AI/ML models. The two critical factors that will drive this boost of a new BI-based AI developer class: First, enabling BI teams with tools such as automation platforms is more scalable and more sustainable than hiring dedicated data scientists; second, because BI teams are significantly closer to the business use-cases compared to data scientists, the lifecycle from the working model's requirement will be accelerated.

- With the advancement in AI technology, it is becoming more important than ever for the government to innovate its traditional methods to achieve better citizen engagement, interoperability, and accountability. Such trends are driving the demand for AI Governance from enterprises and organizations worldwide. For instance, Google has highlighted five areas where the government, in collaboration with AI practitioners and wider civil society, can play a crucial role in clarifying expectations about AI's application on a context-specific basis. These include explainability standards, safety considerations, approaches to appraising fairness, general liability frameworks, and requirements for human-AI collaboration.

- On the contrary, While most enterprise IT procurement is limited to simply choosing suitable software or hardware and eventually deploying it to serve its purpose, the fundamental trouble with AI is that there's an ongoing requirement for initial training and working with data and calibrating it to deliver the result. There are known problems limiting normalizing data in electronic records. These include natural language processing (NLP), proprietary datasets threatening open innovation, frequent bias in the medical literature due to journal bias and even outright fraud, and the growing complexity of health data such that past data is not specific sufficiently to be useful for current predictions.

Industrial AI Software Industry Segmentation

AI software is a computer program adept of high-complexity tasks, like learning, decision-making, and solving problems. AI software uses machine learning to simulate human intelligence, which can allow the software to complete tasks of increasing nuance and sensitivity. Companies use AI software to help their businesses run more efficiently and find new improvement areas. This can result in the better allocation of human resources, allowing individuals to focus on more strategic and fulfilling tasks.

The industrial AI software market is segmented by type (cloud-based and on-premise), by end-user industries (automotive & transportation, healthcare and life science, aerospace and defense, energy and utilities, retail and consumer packaged goods, and other end-user industries), and by geography (North America, Europe, Asia-Pacific, Latin America and Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Type | |

| Cloud Based | |

| On-Premise |

| By End User Industries | |

| Automotive and Transportation | |

| Retail and Consumer Packaged Goods | |

| Healthcare and Life Science | |

| Aerospace and Defense | |

| Energy and Utilities | |

| Other End-User Industries |

| By Geography*** | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Industrial AI Software Market Size Summary

The industrial AI software market is experiencing significant growth, driven by the increasing need for organizations to harness industrial data for multi-dimensional optimization. This demand is pushing companies to adopt AI-enabled decision-making and operational agility to enhance business outcomes across various objectives such as margins, sustainability, and economic efficiency. The European Union's strategic initiatives to position itself as a leading AI hub further underscore the importance of AI in driving industrial innovation. As organizations strive to scale AI practices efficiently, there is a notable shift towards empowering business intelligence teams with automation tools, which are proving to be more scalable and sustainable than traditional data science approaches. This trend is expected to accelerate the integration of AI into business workflows, enhancing the speed and effectiveness of decision-making processes.

In North America, the industrial AI software market is poised for substantial expansion, with the United States at the forefront due to its readiness for AI adoption and significant investments in research and development. The region's focus on high automation potential and strategic partnerships among key players like Siemens, Nvidia, and Cisco Systems is fostering a competitive landscape. These collaborations aim to enhance product development, manufacturing, and operational efficiencies through advanced AI capabilities. The market's semi-fragmented nature allows for strategic alliances that drive innovation and profitability, as seen in partnerships like those between Intrinsic and Siemens, and Mastek and Netail. Such developments are not only transforming industrial processes but also creating new opportunities for market players to capture a larger share of the growing demand for AI solutions across various sectors.

Industrial AI Software Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Buyers

-

1.2.2 Bargaining Power of Suppliers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitutes

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Industry Value Chain Analysis

-

1.4 Assessment of the Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Type

-

2.1.1 Cloud Based

-

2.1.2 On-Premise

-

-

2.2 By End User Industries

-

2.2.1 Automotive and Transportation

-

2.2.2 Retail and Consumer Packaged Goods

-

2.2.3 Healthcare and Life Science

-

2.2.4 Aerospace and Defense

-

2.2.5 Energy and Utilities

-

2.2.6 Other End-User Industries

-

-

2.3 By Geography***

-

2.3.1 North America

-

2.3.2 Europe

-

2.3.3 Asia

-

2.3.4 Australia and New Zealand

-

2.3.5 Latin America

-

2.3.6 Middle East and Africa

-

-

Industrial AI Software Market Size FAQs

How big is the Industrial AI Software Market?

The Industrial AI Software Market size is expected to reach USD 114.68 billion in 2024 and grow at a CAGR of 35.97% to reach USD 532.96 billion by 2029.

What is the current Industrial AI Software Market size?

In 2024, the Industrial AI Software Market size is expected to reach USD 114.68 billion.