Inductor Market Size

| Study Period | 2019 - 2029 |

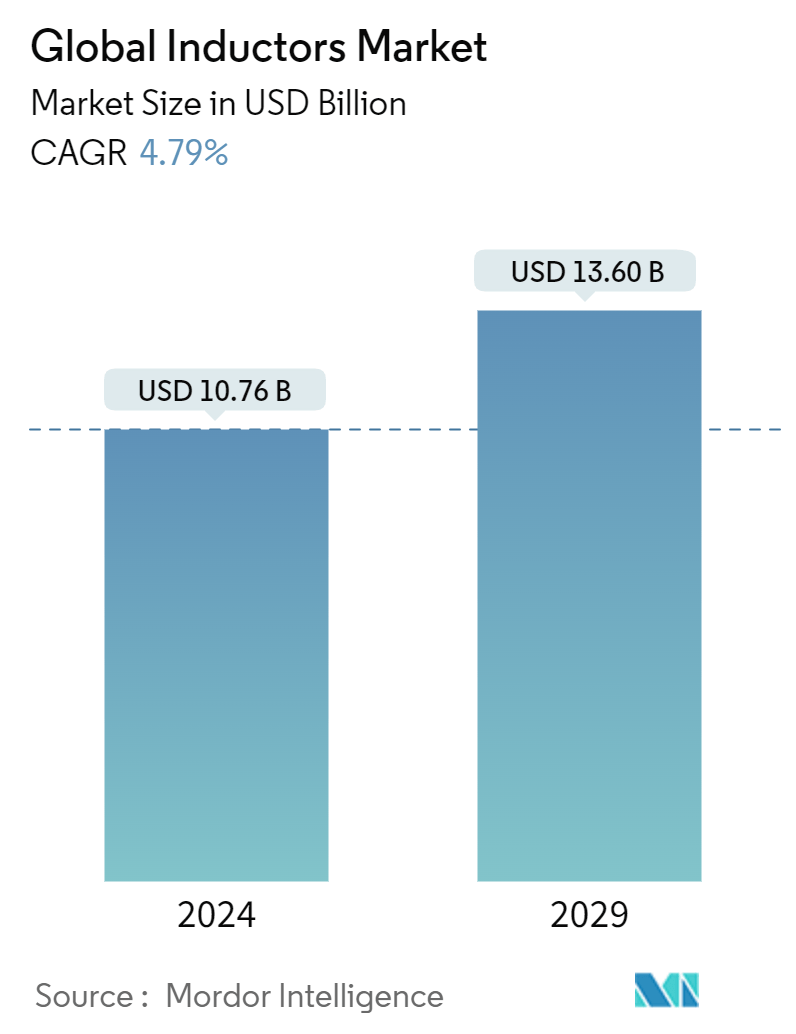

| Market Size (2024) | USD 10.76 Billion |

| Market Size (2029) | USD 13.60 Billion |

| CAGR (2024 - 2029) | 4.79 % |

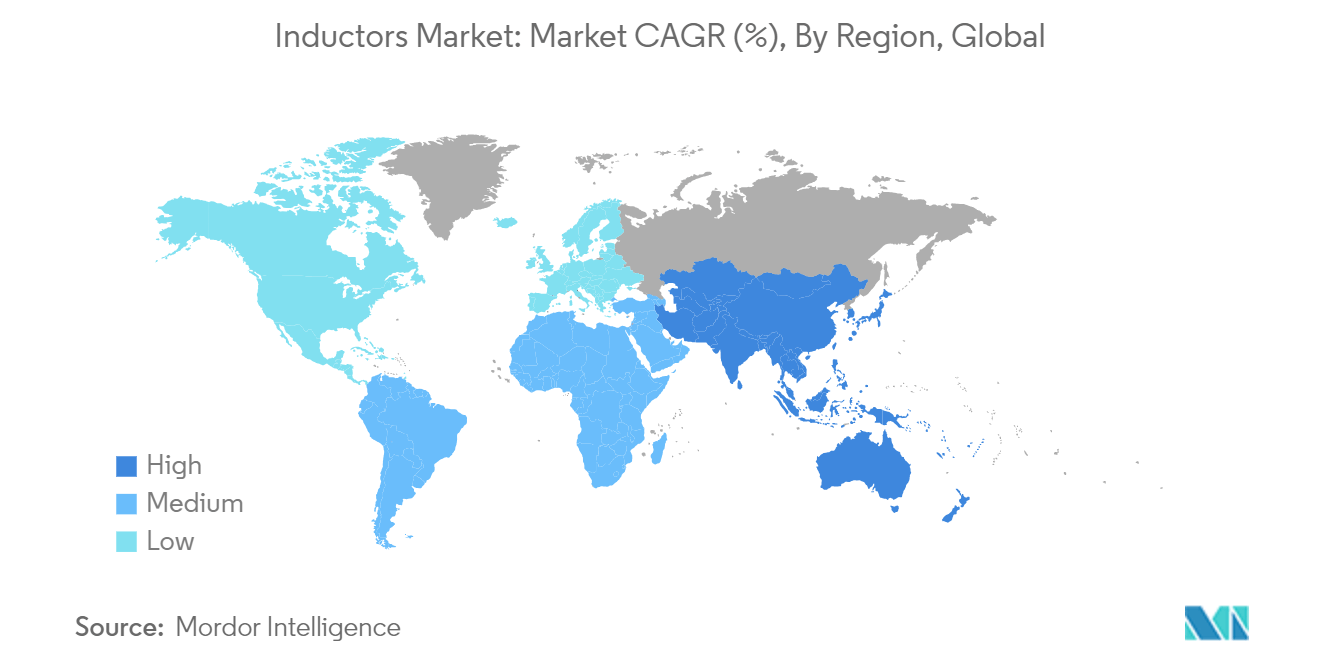

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Inductor Market Analysis

The Global Inductors Market size is estimated at USD 10.76 billion in 2024, and is expected to reach USD 13.60 billion by 2029, growing at a CAGR of 4.79% during the forecast period (2024-2029).

- With the advent of technological advancements, electronics and electronic devices are getting more complex, primarily due to the increasing consumer demand for small or slim devices. Customers have a specific standard for these devices nowadays, for instance, sleek, thin design, with the screen going from edge to edge.

- Smartphones have witnessed the great success of MEMS gyroscopes owing to their low cost, miniature size, and lightweightness. Features like voice-enabled smart devices have increased adoption over the past few years. The adoption of smart devices, such as the Amazon Echo, Google Home, and Sonos, was aggressive by the end of 2023. The younger generation views these devices as the more innovative, faster, and easier way to perform everyday activities. A recent survey conducted by Accenture revealed that more than 50% of internet users use digital voice assistants globally. This is further expected to add to the complexity of electronics, thereby augmenting the demand for inductors.

- Inductors also play an essential role in the healthcare and medical devices industry. Various advancements in the healthcare sector, including improving macro-sized hospital equipment, medical wearables, and point-of-care devices, are expected to increase the demand. The medical industry is continually driving the need for electronics. As technology enhances and smaller, denser, more reliable boards become possible, passive electronic components will play an increasingly important role in healthcare.

- The use of metals, including coppers, iron, and other ferrite substances, for the core and coil of inductors creates the production dependency of inductors on the raw material price. Fluctuations in the supply chain and raw material costs can increase the lead time and impact the profit margin of the market vendors, hindering market growth.

- The increasing inflation and interest rates further decreased consumer spending, which restricted the market’s growth in 2022 and 2023. Due to the war in Russia and Ukraine, European countries experienced inflation, and compared to January 2022, inflation in Germany, Sweden, France, and the United Kingdom increased significantly. In August 2023, the United Kingdom’s inflation rate was 6.7% compared to 5.5% in January 2022. These factors hampered the market’s growth in 2023. According to the Bureau of Labor Statistics, the US manufacturing sector’s output reduced by 0.1% in the third quarter of 2023. This may lead to decreased demand for inductors from the manufacturing sector.

Inductor Market Trends

Frequency Inductor Expected to Witness Significant Growth

- Frequency inductors, called RF (radio frequency) inductors, are specifically designed for applications in high-frequency circuits, such as those used in radio communication, wireless technology, and radar systems. They are necessary because regular inductors, intended for low-frequency applications, may not perform well or even malfunction at higher frequencies due to parasitic capacitance and skin effects. Frequency inductors are optimized to minimize these issues, allowing them to maintain their desired inductance and performance across a wide range of frequencies.

- RF inductors are mainly characterized by low current rating and high electrical resistance. However, the wire resistance increases as the high frequencies are used here. In addition, a few effects come into the picture because of these high-resonant radio frequencies. These include skin effect, proximity effect, and parasitic capacitance.

- RF inductors can be manufactured in different ways. For instance, Murata, one of the prominent vendors of inductors, uses wire wound manufacturing methods, film manufacturing methods, and multi-layer manufacturing methods. Each method has different characteristics.

- There has been a prevailing trend of miniaturization of RF inductors due to their usage in small communication products such as smartphones, wireless modules, Bluetooth modules, etc. Hence, the vendors in the market are focusing on developing small yet powerful RF inductors to contribute to the growth of mobile communication.

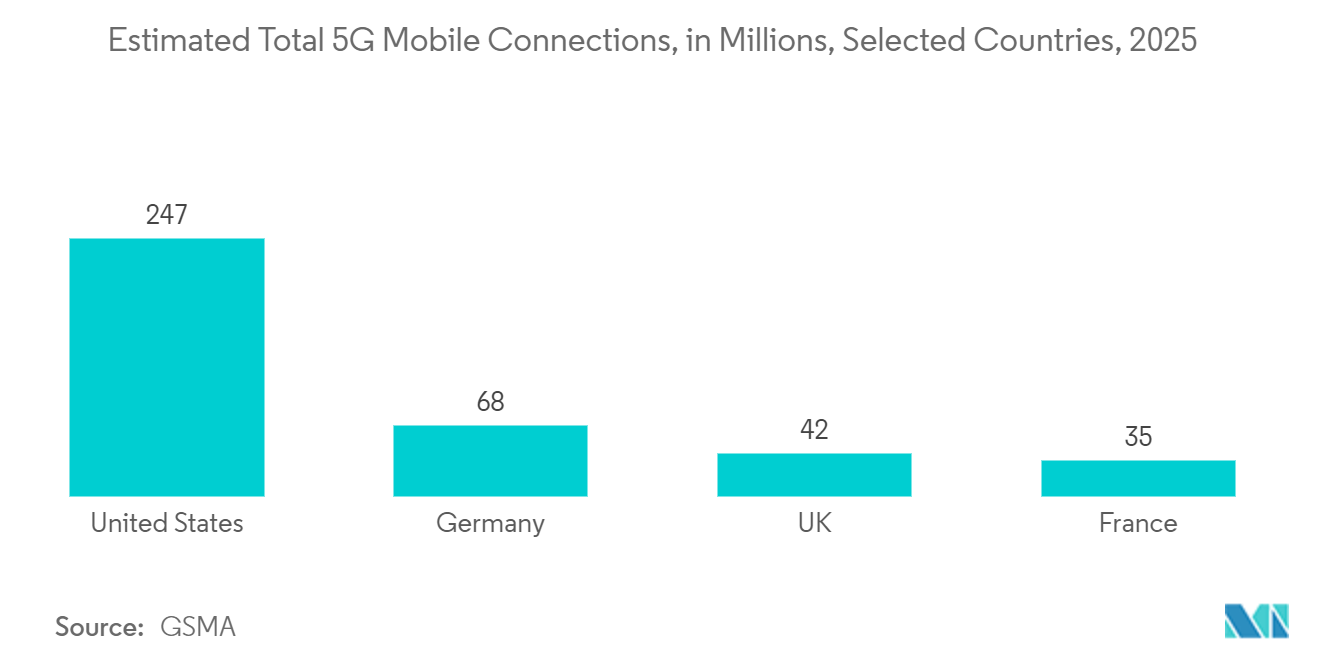

- As consumer electronics is the prominent driver for inductor demand, the growing push to adopt 5G technology is expected to drive the demand for various consumer electronics and communication devices worldwide, impacting market growth. The 5G deployments worldwide are increasing the need for RF inductors for IoTs and conventional smartphones. According to the 5G Americas Organization Report released in May 2023, 5G mobile subscriptions were expected to exceed 1.9 billion in 2023 and reach 5.9 billion by 2027.

- In February 2023, GSMA reported that 5G connections are anticipated to double over the upcoming two years. In addition, GSMA also reported that the growth would come from key markets within APAC and LATAM, like Brazil and India, which have recently launched 5G networks. The expansion of services from Airtel and Jio in 2023 was pivotal to India's ongoing adoption. Moreover, GSMA 5G is expected to account for 145 million in India by the end of 2025.

Asia-Pacific to Register Major Growth

- The Asia-Pacific inductor market is driven by demand from industrial economies and technologically advanced countries, such as China, Korea, Japan, and India. China is one of the largest sources of demand for inductor components, owing to the rapidly growing semiconductor industry and industrial automation.

- The growth of smartphones has been exponential, and the number of smartphone users in the Asian-Pacific countries has increased in the past few years. According to GSMA’s Mobile Economy report, Asia-Pacific is on its way to becoming the world’s largest 5G region by 2025, led by China, Japan, South Korea, and Australia, as well as commercial 5G network launches that are expected to reach 675 million 5G connections, more than half of the global 5G total scheduled by 2025.

- Automotive infotainment systems provide music, videos, other multimedia content, navigation, internet connectivity inside vehicles, and communication with outside systems. Vendors are offering new technology designed to reduce the weight of cable harnesses comprising various telecommunication buses. For instance, in January 2024, TDK Corporation introduced its latest inductor KLZ2012-A series (2.0 mm (L) x 1.25 mm (W) x 1.25 mm (H)) for automotive audio bus (A2B) applications with a wide operation range, high durability, and superior inductance tolerance.

- Ferrite core inductors are expected to witness a rise in adoption owing to the growth in the automotive sector to achieve high efficiency in power conversion models used in automotive. They are also helpful for transformers and inductors in automotive and electronic applications. Industry 4.0 has increased the automation of manufacturing and production processes, thus leading to an increased use of inductors, owing to their presence in many electronic assemblies.

- Overall, along with the rapidly growing automotive sector and increasing demand for inductors, countries such as China, Japan, and South Korea are leading various Smart city initiatives. These innovative initiatives in the region create the potential for using inductors across automotive, transportation, energy, and utilities. Furthermore, communication in the area has also witnessed considerable progress, with companies like Murata deploying specialized inductors for NFC circuits. Such developments are likely to propel the region’s market growth.

Inductor Industry Overview

The inductor market is highly fragmented due to the presence of both global players and small- and medium-sized enterprises. Some of the major players in the market are TDK Corporation, Vishay Intertechnology Inc., Panasonic Corporation, Delta Electronics Inc., and Pulse Electronics (Yageo Corporation). Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- March 2024 - Delta Electronics (Thailand) PCL, a branch of Delta Group, recently opened its latest Delta Plant 8 and R&D Center at Bangpoo Industrial Estate in Thailand. This new facility, spanning 30,400 sq. m, is designed to support Delta's efforts in expanding production and enhancing the development of electric vehicle (EV) power electronics for customers worldwide. Establishing this factory and research center is part of Delta's strategy to meet the increasing demand in the EV market.

- February 2024 - TDK Corporation unveiled its latest MHQ1005075HA line of inductors designed for automotive high-frequency circuits. This new product maintains the same materials and construction techniques as its predecessor. Still, it incorporates TDK's unique design knowledge to enhance the internal structure, focusing on fail-safe design. The series comes in a 1005 size (1.0 × 0.5 × 0.7 mm - L x W x H) and offers inductance ranging from 1.0 nH to 56 nH.

Inductor Market Leaders

-

TDK Corporation

-

Vishay Intertechnology Inc.

-

Panasonic Corporation

-

Delta Electronics Inc.

-

Pulse Electronics (Yageo Corporation)

*Disclaimer: Major Players sorted in no particular order

Inductor Market News

- February 2024 - Abracon, a provider of RF and Antenna solutions, introduced its new "ATL-series" Trans-Inductor Voltage Regulator (TLVR) Inductors with the potential to transform the landscape of power delivery with high performance and reliability. The company's Trans-Inductor Voltage Regulators are designed to meet the escalating need for products that deliver rapid and efficient responses to power fluctuations across diverse applications. These include data centers, electric vehicles, cloud computing, and artificial intelligence (AI) servers. The company is investing in its product portfolio expansion to address the requirements of complex systems and work closely with customers to change the landscape of power supply design.

- January 2024 - TDK Corporation launched its newest addition to the inductor lineup, the KLZ2012-A series. With dimensions of 2.0 mm (L) x 1.25 mm (W) x 1.25 mm (H), these multilayer inductors are specifically designed for automotive audio bus (A2B) applications. Boasting a wide operation range, exceptional durability, and superior inductance tolerance, the KLZ2012-A series is well-suited for high-temperature automotive environments. Notably, these inductors can operate at temperatures up to 150 °C, making them ideal for demanding automotive applications.

Inductor Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Degree of Competition

4.3 Industry Value Chain Analysis

4.4 Impact of Macroeconomic Trends in the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Rise In Innovations in Consumer Electronics Products

5.1.2 Growing Demand for Energy-efficient Electrical and Electronic Systems

5.2 Market Restraints

5.2.1 Rising Cost of Raw Materials, Especially Copper

6. MARKET SEGMENTATION

6.1 By Type

6.1.1 Power

6.1.2 Frequency

6.2 By Core

6.2.1 Air/Ceramic Core

6.2.2 Ferrite Core

6.2.3 Other Cores

6.3 By End-user Vertical

6.3.1 Automotive

6.3.2 Aerospace and Defense

6.3.3 Communications

6.3.4 Consumer Electronics and Computing

6.3.5 Other End-user Verticals

6.4 By Geography***

6.4.1 North America

6.4.2 Europe

6.4.3 Asia

6.4.4 Australia and New Zealand

6.4.5 Latin America

6.4.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 TDK Corporation

7.1.2 Vishay Intertechnology Inc.

7.1.3 Panasonic Corporation

7.1.4 Delta Electronics Inc.

7.1.5 Pulse Electronics (Yageo Corporation)

7.1.6 Sagami Elec Co. Ltd

7.1.7 Taiyo Yuden Co. Ltd

7.1.8 TE Connectivity Ltd

7.1.9 Murata Manufacturing Co. Ltd

7.1.10 Sumida Corporation

7.1.11 Coilcraft Inc.

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Inductor Industry Segmentation

Inductors are passive two-terminal electrical components that store energy in a magnetic field when electric current flows through them. Most power electronic circuits include inductors, which are passive elements that store energy in the form of magnetic energy when electricity is supplied to them. A significant characteristic of an inductor is that it resists changes in the amount of current that passes through it. To equalize the current flowing through it, whenever the current across the inductor varies, it either gains or loses charge.

The inductor market is segmented by type (power and frequency), core (air/ceramic core, ferrite core, and other cores), end-user vertical (automotive, aerospace & defense, communications, consumer electronics & computing, and other end-user verticals), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type | |

| Power | |

| Frequency |

| By Core | |

| Air/Ceramic Core | |

| Ferrite Core | |

| Other Cores |

| By End-user Vertical | |

| Automotive | |

| Aerospace and Defense | |

| Communications | |

| Consumer Electronics and Computing | |

| Other End-user Verticals |

| By Geography*** | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Inductor Market Research FAQs

How big is the Global Inductors Market?

The Global Inductors Market size is expected to reach USD 10.76 billion in 2024 and grow at a CAGR of 4.79% to reach USD 13.60 billion by 2029.

What is the current Global Inductors Market size?

In 2024, the Global Inductors Market size is expected to reach USD 10.76 billion.

Who are the key players in Global Inductors Market?

TDK Corporation, Vishay Intertechnology Inc., Panasonic Corporation, Delta Electronics Inc. and Pulse Electronics (Yageo Corporation) are the major companies operating in the Global Inductors Market.

Which is the fastest growing region in Global Inductors Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Global Inductors Market?

In 2024, the Asia Pacific accounts for the largest market share in Global Inductors Market.

What years does this Global Inductors Market cover, and what was the market size in 2023?

In 2023, the Global Inductors Market size was estimated at USD 10.24 billion. The report covers the Global Inductors Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Global Inductors Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Power Inductor Industry Report

Statistics for the 2024 Power Inductor market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Power Inductor analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Power Inductor Market Report Snapshots