| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 11.28 Billion |

| Market Size (2030) | USD 14.25 Billion |

| CAGR (2025 - 2030) | 4.79 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Inductor Market Analysis

The Global Inductors Market size is estimated at USD 11.28 billion in 2025, and is expected to reach USD 14.25 billion by 2030, at a CAGR of 4.79% during the forecast period (2025-2030).

The global inductor market faces significant macroeconomic headwinds, with rising inflation and interest rates impacting consumer spending patterns and manufacturing output. The United Kingdom experienced an inflation rate of 6.7% in August 2023, reflecting broader economic challenges across European markets. Supply chain disruptions and raw material price volatility, particularly in metals like copper, iron, and ferrite substances, continue to affect production costs and lead times. The US manufacturing sector's output declined by 0.1% in the third quarter of 2023, indicating persistent challenges in the industrial segment that could influence inductor demand.

The industry is witnessing a fundamental shift toward miniaturization and increased complexity in electronic devices, driven by evolving consumer preferences for sleek, compact designs. This trend is particularly evident in the rising adoption of smart home devices and voice-enabled technology, with a recent Accenture survey revealing that over 50% of internet users globally now use digital voice assistants. The integration of multiple circuits operating at different voltage levels and frequencies within single devices has created new technical challenges and opportunities for inductor manufacturers, particularly in developing components that can maintain performance while reducing size.

The acceleration of Industry 4.0 initiatives and industrial automation is reshaping the market landscape, with increasing emphasis on smart manufacturing and connected systems. According to Cisco's projections, the number of network-connected devices is expected to reach nearly 30 billion by 2023, highlighting the growing importance of inductors in supporting IoT infrastructure. The development of smart cities and industrial automation projects across regions has created new application areas for inductors, particularly in power management and signal processing applications.

The market is experiencing significant transformation through emerging applications in healthcare technology and medical devices. The integration of inductors in medical wearables, point-of-care devices, and advanced hospital equipment is creating new opportunities for component manufacturers. According to GSMA forecasts, Latin America alone is expected to reach 1,300 million IoT connections by 2025, indicating the growing potential for inductors in connected healthcare devices and other IoT applications. This evolution in healthcare technology, combined with the need for more reliable and efficient electronic components, is driving innovation in inductor design and manufacturing processes.

Inductor Market Trends

Rise in Innovations in Consumer Electronics Products

The increasing complexity and miniaturization of consumer electronic devices are driving significant innovations in inductor technology. With the advent of technological advancements, electronics and electronic devices are becoming more sophisticated, primarily due to increasing consumer demand for slim and compact devices with enhanced functionality. For instance, smartphones now require multiple inductors within a single device to support various functions, from camera modules and vibrators to displays and power management circuits. This trend is further exemplified by recent industry developments, such as TDK Corporation's introduction of its new PLEA85 series of high-efficiency power inductors in October 2023, specifically developed for battery-powered wearables and other devices to improve operating times.

The emergence of voice-enabled smart devices and the integration of more sophisticated features in consumer electronics have created new opportunities for inductor manufacturers. According to recent industry surveys, more than 50% of internet users globally now use digital voice assistants, demonstrating the growing complexity of electronic devices. This complexity is further augmented by the rapid advancement in mobile communication technology, with 5G mobile subscriptions expected to exceed 1.9 billion in 2023 and reach 5.9 billion by 2027. The industry has responded to these demands through continuous innovation, as evidenced by Taiyo Yuden's September 2023 announcement of mass production of multilayer metal power inductors in the MCOIL LSCN series, specifically designed for power supply circuits in smartphones and wearable devices.

Understand The Key Trends Shaping This Market

Download PDF

Growing Demand for Energy-Efficient Electrical and Electronic Systems

The increasing focus on energy efficiency across various electronic applications is driving the demand for advanced inductors that can optimize power management and reduce energy consumption. Inductors play a crucial role in extending battery life for battery-powered applications by improving the efficiency of power supply circuits through optimal inductance and current-carrying capacity. This is particularly significant as the industry witnesses a surge in portable and battery-operated devices. The market has seen significant advancement in product development, with manufacturers combining the best possible utilization of inductance and current-carrying capacity with low intrinsic losses through innovative material selection and manufacturing technology.

The trend toward energy-efficient electronic devices is further accelerated by rising energy costs and increasing environmental awareness among users. This has led to substantial investments in research and development of energy-efficient inductors, as demonstrated by Samsung Electro-Mechanics' initiation of mass production of thin-film SMD power inductors in July 2023, specifically designed for integration into electric vehicle cameras equipped with self-driving technology. Additionally, the growing adoption of Industry 4.0 and smart manufacturing processes has intensified the need for energy-efficient components, with inductors playing a vital role in power management and energy conservation. According to industry projections, approximately 500 billion devices will be connected to the Internet by 2030, highlighting the critical importance of energy-efficient components in supporting this massive network of connected devices while minimizing power consumption.

Segment Analysis: By Type

Power Segment in Global Inductors Market

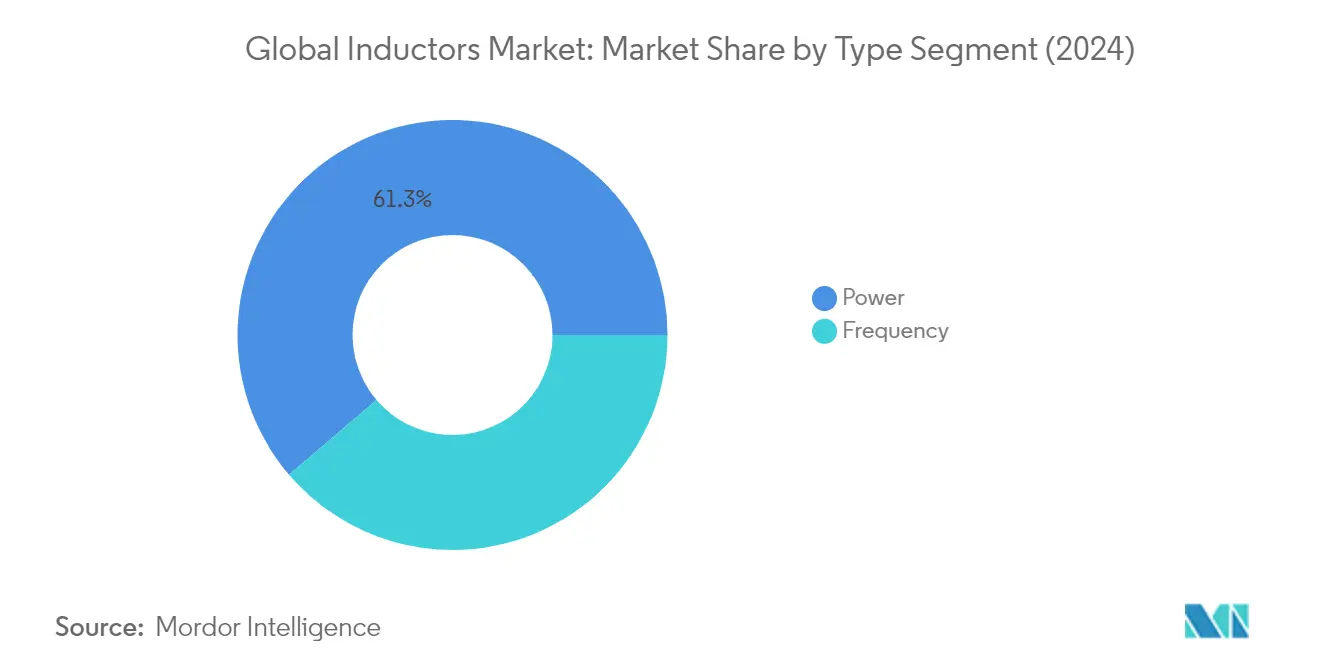

The power inductor market continues to dominate the global inductors market, commanding approximately 61% of the total market share in 2024. Inductors, particularly power inductors, are critical components designed specifically for power supplies and circuits, manufactured using metal composite or ferrite materials. These components play a vital role in voltage conversion and stable power supply to integrated circuits, with applications spanning smartphones, tablets, wearable devices, IoT devices, solid-state drives, and various consumer electronics. The segment's prominence is further reinforced by its extensive use in automotive applications, particularly in LED drivers, radar systems, camera-control systems, and various aerospace and defense applications. The increasing electrification of vehicles, growing adoption of renewable energy systems, and the rising demand for power-efficient electronic devices have significantly contributed to the segment's market leadership.

Frequency Segment in Global Inductors Market

The Frequency segment is emerging as the fastest-growing segment in the global inductors market, projected to grow at approximately 6% CAGR from 2024 to 2029. Also known as RF inductors, these components are specifically engineered for high-frequency applications in radio communication, wireless technology, and radar systems. The segment's growth is primarily driven by the rapid expansion of 5G infrastructure, increasing adoption of IoT devices, and the growing demand for wireless communication technologies. The development of miniaturized RF inductors for compact communication products such as smartphones, wireless modules, and Bluetooth devices has further accelerated segment growth. Additionally, the automotive industry's increasing integration of advanced communication functions, including telematics and V2X (Vehicle-to-Everything) technology, has created substantial opportunities for frequency inductors in modern vehicles.

Segment Analysis: By Core

Air/Ceramic Core Segment in Global Inductors Market

The Air/Ceramic Core segment continues to dominate the global inductors market, commanding approximately 47% market share in 2024. This significant market position is driven by the segment's widespread application in high-frequency circuits, particularly in RF communication systems and power supply filtering circuits. Air core inductors are particularly valued for their saturation-free characteristics and superior performance at high frequencies up to 1 GHz, making them essential components in computer devices, communication equipment, and mobile chargers. The segment's prominence is further reinforced by the growing demand for inductors with improved performance characteristics such as higher efficiency, lower losses, and better frequency response, especially in applications requiring minimal parasitic effects and low losses.

Air/Ceramic Core Segment Growth in Global Inductors Market

The Air/Ceramic Core segment is projected to maintain strong growth momentum with an expected CAGR of approximately 5% during the forecast period 2024-2029. This growth trajectory is primarily driven by the increasing adoption of ceramic core inductors in high-frequency applications requiring low inductance values, shallow core losses, and high Q values. The segment's expansion is further supported by the rising demand for compact inductors that can be integrated into tight spaces while maintaining performance, particularly in emerging applications like 5G wireless communications, IoT devices, and advanced automotive electronics. Manufacturers are continuously innovating to develop smaller, more efficient air and ceramic core inductors that can meet the evolving requirements of modern electronic devices while maintaining thermal stability and performance reliability.

Remaining Segments in Core Segmentation

The Ferrite Core segment represents a crucial component of the ferrite power inductors market, offering high magnetic permeability and low core losses, making them ideal for power supplies, RF circuits, and automotive electronics applications. These cores are particularly valued for their ability to store significant energy in compact spaces and their excellent performance in high-frequency applications. Meanwhile, the Other Cores segment, which includes MPP cores, powdered iron cores, and laminated cores, provides specialized solutions for specific applications requiring unique magnetic properties, such as high saturation flux density and superior temperature stability. Both segments continue to evolve with technological advancements and expanding applications across various industries.

Segment Analysis: By End-User Industry

Consumer Electronics and Computing Segment in Global Inductors Market

The Consumer Electronics and Computing segment dominates the global inductors market, commanding approximately 51% market share in 2024. This significant market position is driven by the widespread integration of inductors in various consumer electronic devices, including smartphones, tablets, laptops, and computing hardware. Multilayer inductors have become increasingly crucial in these applications, particularly in RF front-end modules where they play a vital role in filtering and matching networks for improved communication performance. The segment's growth is further supported by the rising demand for ferrite cores across consumer electronic devices, where they are essential for minimizing electromagnetic interference in cables and connectors, protecting devices like televisions and computers. The continuous innovation in consumer electronics, particularly in areas such as smart devices, wearables, and advanced computing systems, has led manufacturers to develop more compact and efficient inductors that can deliver exceptional inductance values while maintaining minimal form factors.

Automotive Segment in Global Inductors Market

The automotive power inductor market is emerging as the fastest-growing sector in the global inductors market, with a projected growth rate of approximately 6% during 2024-2029. This remarkable growth is primarily driven by the increasing electrification of vehicles and the integration of advanced driver-assistance systems (ADAS). The segment's expansion is further fueled by the growing adoption of electronic control units (ECUs) in modern vehicles, particularly in electric and hybrid vehicles, which require stable power supply over wide temperature ranges. The trend toward vehicle electrification has created significant demand for DC-DC converters with enhanced stability and energy efficiency, particularly in under-hood locations or areas exposed to sunlight. Manufacturers are responding to these demands by developing inductors with low DC resistance to minimize unwanted self-heating and energy losses, while also providing improved saturation characteristics and stability across broad temperature ranges. The increasing focus on safety features and advanced driver assistance systems is creating additional demand for inductors in automotive applications, particularly in radar systems, camera-control systems, and other safety-critical components.

Remaining Segments in End-User Industry

The Communications segment maintains a strong presence in the inductors market, driven by the ongoing deployment of 5G infrastructure and the evolution of wireless communication technologies. The Aerospace and Defense sector demonstrates steady demand for inductors in radar systems, satellite communications, and electronic warfare equipment, benefiting from increased defense modernization initiatives globally. The Other End-user Industries segment, encompassing medical, industrial, and manufacturing sectors, continues to contribute to market growth through applications in medical equipment, industrial automation, and power management systems. These segments collectively represent diverse application areas for inductors, from high-frequency communication devices to precision medical equipment and industrial control systems, showcasing the versatility and essential nature of inductors across multiple industries.

Global Inductors Market Geography Segment Analysis

Inductor Market in North America

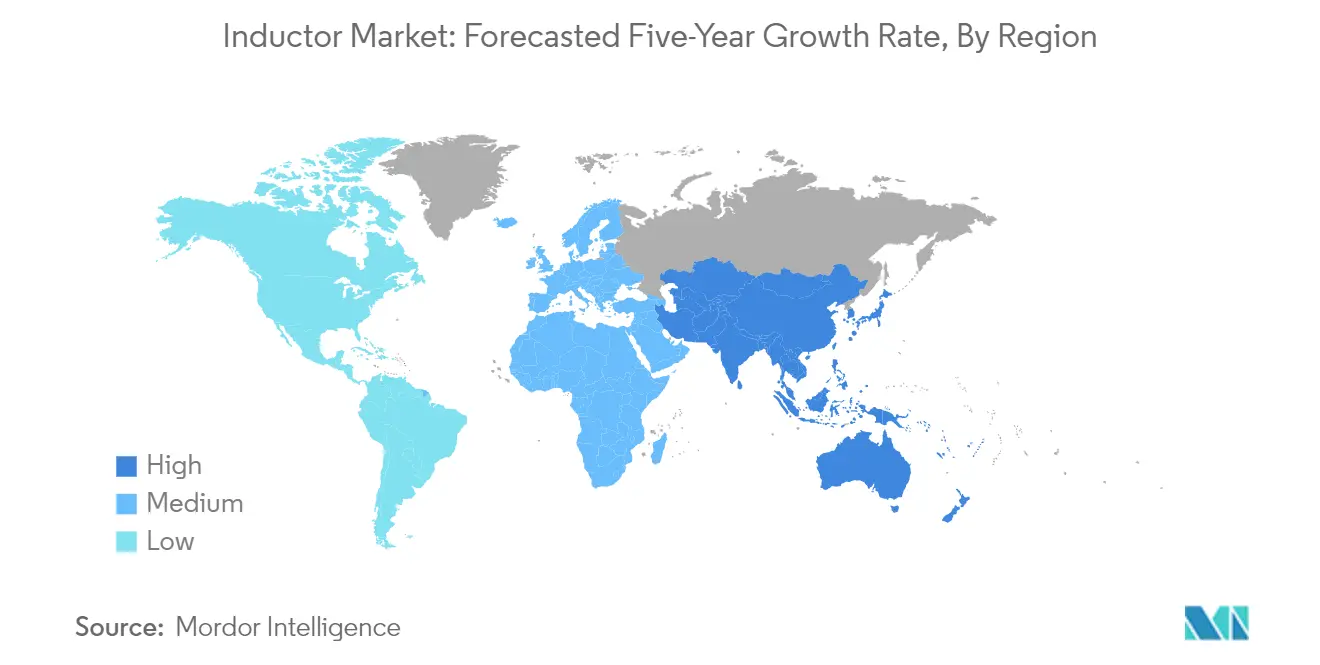

The North American inductor market commands approximately 17% of the global inductor market share in 2024, driven primarily by robust demand from computing, electronics, automotive, and aerospace sectors. The region's market is characterized by extensive R&D activities in the inductor sector, particularly in the United States. The presence of major automotive and aerospace manufacturers has created substantial demand for high-performance inductors. The market shows particular strength in ceramic core inductors, especially in high-frequency applications requiring low inductance values and high Q values. The region's focus on technological advancement, particularly in 5G wireless communications and IoT devices, continues to drive innovation in inductor design and manufacturing. Additionally, the growing emphasis on electric vehicles and renewable energy systems has created new opportunities for power inductor market applications. The presence of stringent quality standards and regulatory requirements has also influenced product development and manufacturing practices in the region.

Inductor Market in Europe

The European inductor market has demonstrated consistent growth, registering approximately 4% growth annually from 2019 to 2024, driven by technological advancements in telecommunication equipment and automotive applications. The region's market is particularly strong in countries like Germany, Norway, and the Netherlands, which are leading the electric vehicle revolution. European manufacturers have maintained a strong focus on developing high-precision components, supported by initiatives like Germany's Industrie 4.0 and similar digital manufacturing programs. The market has seen significant development in power inductors with winding ferrite and multilayer ferrite structures, catering to applications ranging from automotive equipment to mobile devices. The region's emphasis on renewable energy and sustainable technologies has created additional demand for high-performance inductors. The presence of strict environmental regulations and safety standards has influenced product development, pushing manufacturers to innovate in terms of efficiency and sustainability. The market also benefits from strong research and development infrastructure and collaboration between industry and academic institutions.

Inductor Market in Asia-Pacific

The Asia-Pacific inductor market is projected to grow at approximately 6% during the period 2024-2029, establishing itself as the most dynamic region in the global market. The region's dominance is driven by major industrial economies and technologically advanced countries such as China, Korea, Japan, and India. The market benefits from the presence of a robust semiconductor industry and increasing industrial automation initiatives. The region's strong position in consumer electronics manufacturing, particularly smartphones and other mobile devices, continues to drive demand for various types of inductors. The automotive sector in the region has emerged as a significant growth driver, particularly with the rapid evolution of advanced driver-assistance systems and autonomous driving technologies. The market is characterized by continuous innovation in miniaturization and efficiency improvements, supported by significant investments in research and development. The presence of major manufacturing facilities and the ongoing shift towards Industry 4.0 has created additional opportunities for inductor manufacturers.

Inductor Market in Rest of the World

The Rest of the World region, encompassing Latin America, the Middle East, and Africa, represents an emerging market for inductors with significant growth potential. The region's market is characterized by increasing investments in industrial automation and the growing adoption of smart city initiatives. Latin America has shown particular promise with its expanding telecommunications infrastructure and increasing adoption of IoT technologies. The Middle Eastern market is driven by automation in the oil and gas sector, along with significant investments in renewable energy projects. The region's automotive sector, particularly in the UAE and Saudi Arabia, is showing increased interest in electric and hybrid vehicles, creating new opportunities for inductor manufacturers. The market is also benefiting from increasing investments in manufacturing capabilities and the growing adoption of advanced electronics in various industries. The development of smart infrastructure and the increasing focus on energy efficiency are creating additional demand for various types of inductors across the region.

Get Analysis on Important Geographic Markets

Download PDF

Inductor Industry Overview

Top Companies in Global Inductor Market

The global inductor market is characterized by intense innovation and strategic expansion initiatives from leading players like TDK Corporation, Vishay Intertechnology, Panasonic Corporation, and Murata Manufacturing. Companies are heavily investing in research and development to create miniaturized components with enhanced performance capabilities, particularly focusing on automotive and consumer electronics applications. The industry witnesses continuous product launches targeting emerging applications in electric vehicles, 5G infrastructure, and IoT devices. Operational agility is demonstrated through the establishment of new manufacturing facilities across strategic locations, particularly in Asia and North America, to ensure supply chain resilience and proximity to key markets. Market leaders are increasingly adopting automation in their manufacturing processes while simultaneously expanding their distribution networks to improve market penetration and customer service capabilities.

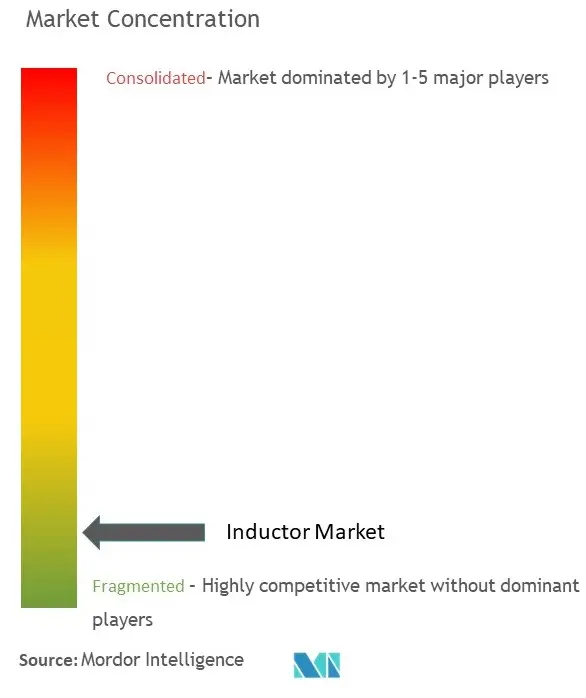

Consolidated Market with Strong Regional Players

The inductor market exhibits a relatively consolidated structure dominated by large multinational corporations with diverse product portfolios and strong manufacturing capabilities. These established players leverage their extensive research capabilities, global distribution networks, and long-standing customer relationships to maintain their market positions. While Japanese and European conglomerates hold significant market share globally, specialized manufacturers focusing exclusively on magnetic components have carved out strong positions in specific application segments and regional markets.

The industry has witnessed strategic consolidation through mergers and acquisitions, primarily driven by the need to acquire technological capabilities and expand geographical presence. Companies are particularly interested in acquiring firms with specialized expertise in emerging applications such as automotive electronics and renewable energy systems. Regional players, especially in Asia, are increasingly forming strategic partnerships with global leaders to enhance their technological capabilities and expand their market reach, while larger corporations are acquiring smaller innovative companies to strengthen their product offerings and maintain a competitive advantage.

Innovation and Customization Drive Market Success

Success in the inductor market increasingly depends on manufacturers' ability to develop customized solutions that address specific application requirements while maintaining cost competitiveness. Incumbent inductor manufacturers are focusing on vertical integration strategies to control costs and quality, while simultaneously investing in advanced manufacturing technologies to improve production efficiency. Companies are also strengthening their design and engineering capabilities to provide application-specific solutions, particularly for emerging sectors like electric vehicles and renewable energy systems.

Market contenders are finding opportunities by focusing on niche applications and developing specialized products for specific industry segments. The ability to provide technical support and collaborate closely with customers during the design phase has become crucial for gaining market share. While substitution risk remains low due to the fundamental nature of inductors in electronic circuits, manufacturers must continually innovate to address challenges such as miniaturization and energy efficiency. Regulatory compliance, particularly in automotive and medical applications, has become a key differentiator, with successful companies maintaining robust quality management systems and obtaining necessary certifications for their target markets.

Inductor Market Leaders

-

TDK Corporation

-

Vishay Intertechnology Inc.

-

Panasonic Corporation

-

Delta Electronics Inc.

-

Pulse Electronics (Yageo Corporation)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Inductor Market News

- February 2024 - Abracon, a provider of RF and Antenna solutions, introduced its new "ATL-series" Trans-Inductor Voltage Regulator (TLVR) Inductors with the potential to transform the landscape of power delivery with high performance and reliability. The company's Trans-Inductor Voltage Regulators are designed to meet the escalating need for products that deliver rapid and efficient responses to power fluctuations across diverse applications. These include data centers, electric vehicles, cloud computing, and artificial intelligence (AI) servers. The company is investing in its product portfolio expansion to address the requirements of complex systems and work closely with customers to change the landscape of power supply design.

- January 2024 - TDK Corporation launched its newest addition to the inductor lineup, the KLZ2012-A series. With dimensions of 2.0 mm (L) x 1.25 mm (W) x 1.25 mm (H), these multilayer inductors are specifically designed for automotive audio bus (A2B) applications. Boasting a wide operation range, exceptional durability, and superior inductance tolerance, the KLZ2012-A series is well-suited for high-temperature automotive environments. Notably, these inductors can operate at temperatures up to 150 °C, making them ideal for demanding automotive applications.

Inductor Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macroeconomic Trends in the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Rise In Innovations in Consumer Electronics Products

- 5.1.2 Growing Demand for Energy-efficient Electrical and Electronic Systems

-

5.2 Market Restraints

- 5.2.1 Rising Cost of Raw Materials, Especially Copper

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 Power

- 6.1.2 Frequency

-

6.2 By Core

- 6.2.1 Air/Ceramic Core

- 6.2.2 Ferrite Core

- 6.2.3 Other Cores

-

6.3 By End-user Vertical

- 6.3.1 Automotive

- 6.3.2 Aerospace and Defense

- 6.3.3 Communications

- 6.3.4 Consumer Electronics and Computing

- 6.3.5 Other End-user Verticals

-

6.4 By Geography***

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 TDK Corporation

- 7.1.2 Vishay Intertechnology Inc.

- 7.1.3 Panasonic Corporation

- 7.1.4 Delta Electronics Inc.

- 7.1.5 Pulse Electronics (Yageo Corporation)

- 7.1.6 Sagami Elec Co. Ltd

- 7.1.7 Taiyo Yuden Co. Ltd

- 7.1.8 TE Connectivity Ltd

- 7.1.9 Murata Manufacturing Co. Ltd

- 7.1.10 Sumida Corporation

- 7.1.11 Coilcraft Inc.

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Inductor Industry Segmentation

Inductors are passive two-terminal electrical components that store energy in a magnetic field when electric current flows through them. Most power electronic circuits include inductors, which are passive elements that store energy in the form of magnetic energy when electricity is supplied to them. A significant characteristic of an inductor is that it resists changes in the amount of current that passes through it. To equalize the current flowing through it, whenever the current across the inductor varies, it either gains or loses charge.

The inductor market is segmented by type (power and frequency), core (air/ceramic core, ferrite core, and other cores), end-user vertical (automotive, aerospace & defense, communications, consumer electronics & computing, and other end-user verticals), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type | Power |

| Frequency | |

| By Core | Air/Ceramic Core |

| Ferrite Core | |

| Other Cores | |

| By End-user Vertical | Automotive |

| Aerospace and Defense | |

| Communications | |

| Consumer Electronics and Computing | |

| Other End-user Verticals | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Inductor Market Research FAQs

How big is the Global Inductors Market?

The Global Inductors Market size is expected to reach USD 11.28 billion in 2025 and grow at a CAGR of 4.79% to reach USD 14.25 billion by 2030.

What is the current Global Inductors Market size?

In 2025, the Global Inductors Market size is expected to reach USD 11.28 billion.

Who are the key players in Global Inductors Market?

TDK Corporation, Vishay Intertechnology Inc., Panasonic Corporation, Delta Electronics Inc. and Pulse Electronics (Yageo Corporation) are the major companies operating in the Global Inductors Market.

Which is the fastest growing region in Global Inductors Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Global Inductors Market?

In 2025, the Asia Pacific accounts for the largest market share in Global Inductors Market.

What years does this Global Inductors Market cover, and what was the market size in 2024?

In 2024, the Global Inductors Market size was estimated at USD 10.74 billion. The report covers the Global Inductors Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Inductors Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Global Inductors Market Research

Mordor Intelligence provides a comprehensive analysis of the inductor market, drawing on decades of expertise in electronic component research. Our latest report explores the full range of inductor manufacturer capabilities. This includes technologies such as ferrite chip inductors, ceramic RF inductors, and power inductor innovations. The analysis also covers emerging trends in automotive grade inductor applications and developments in EV power inductor technology. Additionally, it offers insights into chip wound inductor advancements, detailing manufacturing processes and technological progress.

Stakeholders across the electronics industry will benefit from our detailed examination of ferrite power inductors, RF chip inductor applications, and metal composite power inductor developments. The report, available as a PDF for easy download, includes comprehensive data on companies manufacturing inductors. It also covers integrated power inductor solutions and emerging applications in automotive power inductor systems. Our analysis encompasses molded inductors, air core fixed inductors, and ferromagnetic fixed inductor technologies. This provides valuable insights for industry decision-makers, manufacturers, and investors seeking to understand market dynamics and growth opportunities.