Market Overview

| Study Period | 2017 - 2028 |

|---|---|

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2028 |

| Market Size (2024) | USD 78.77 Million |

| Market Size (2028) | USD 97.15 Million |

| Growth Rate (2024 - 2028) | 5.38% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia Sealants Market Analysis by Mordor Intelligence

The Indonesia Sealants Market size is estimated at 78.77 million USD in 2024, and is expected to reach 97.15 million USD by 2028, growing at a CAGR of 5.38% during the forecast period (2024-2028).

The Indonesian sealants industry is experiencing significant transformation driven by rapid urbanization and infrastructure development initiatives. The government's ambitious infrastructure plans include a massive USD 40 billion investment to extend Jakarta's metro network, demonstrating the scale of construction activities that will require advanced construction sealants solutions. Additionally, the development of Indonesia's new capital city project with an investment of IDR 466 trillion represents a landmark opportunity for the sealants industry, as it will encompass extensive construction of government buildings, residential areas, and supporting infrastructure.

The electronics and electrical equipment manufacturing sector has emerged as a crucial growth driver for the sealants market, with applications ranging from component protection to sensor sealing. The electronic industry is projected to reach USD 22.11 billion by 2025, significantly outpacing neighboring countries in Southeast Asia. This growth is further amplified by the rapid expansion of e-commerce activities and increasing consumer demand for electronic products, creating substantial opportunities for specialized electronic sealants applications in manufacturing and assembly processes.

The healthcare sector represents an expanding market for specialized medical sealants, with applications in medical device assembly and equipment manufacturing. Healthcare spending in Indonesia is projected to reach IDR 1,224 trillion by 2027, indicating substantial growth potential for medical-grade sealants. The industry is witnessing increased demand for high-performance sealing materials that meet stringent medical standards and regulations, particularly in surgical equipment and diagnostic devices.

Sustainable development initiatives are reshaping the sealants market landscape, with increasing emphasis on environmentally friendly products and solutions. The government's commitment to housing development is evident in its plan to renovate 2,200 low-quality houses with a budget of IDR 38.5 billion, creating demand for sustainable sealing materials solutions. This trend is complemented by growing awareness among consumers and industries about the importance of using eco-friendly industrial sealants that comply with environmental regulations while maintaining high-performance standards.

Indonesia Sealants Market Trends and Insights

Government & public investments in residential and non-residential construction projects will boost the industry

- The Indonesian construction industry is expected to expand at a CAGR of roughly 3.43% from 2022 to 2028. Over the last decade, the construction sector in Indonesia has grown with a downward trend, reporting a gain of more than 6.2% in 2019 when compared to 2018. However, the building sector experienced a significant slowdown in 2020 as a result of the COVID-19 epidemic. During the forecast period of 2022 to 2028, the Indonesia building adhesives market is expected to expand at a CAGR of approximately 3.37% in terms of volume and 5.42% in terms of value during the forecast period.

- Currently, the industry is investing in large infrastructure projects in order to increase the development of the country. For instance, Indonesia has been preparing to spend about USD 40 billion to extend Jakarta's metro network, which is poised to boost the country’s construction industry. Furthermore, the government of Indonesia revealed that the new capital city would be built on the island of Borneo with an investment of IDR 466 trillion (GBP 26.6 billion), and construction would take 10 years.

- On the other hand, Mitsubishi Corp., along with Temasek Holding, is planning to build a smart city 25 km southwest of Jakarta. The smart city includes homes, shopping centers, and medical facilities, with the goal of housing 40,000 to 60,000 permanent residents. Moreover, the government has planned to renovate as many as 2,200 low-quality houses in the eastern Indonesian province, which will be renovated and rebuilt with a total budget of IDR 38.5 billion. The development, specifically residential construction, tends to increase the demand for adhesives and sealants in the country.

Understand The Key Trends Shaping This Market

Download PDF

Considerable growth of export values for automotive parts & components will proliferate the industry growth

- The automotive industry in Indonesia remains a promising sector that contributes significantly to the country's economic progress. According to Agus Gumiwang Kartasasmita, Minister of Sector Republic of Indonesia, the automobile industry in Indonesia witnessed tremendous growth in 2021, with a double-digit growth rate of 17.82%. In 2019, the country produced about 12,86,848 units of vehicles which drastically reduced to 6,90,176 units in 2020, accounting for a decline of about 46% owing to the COVID-19 pandemic. Due to this reason, the variation in automotive production between 2019 and 2021 resulted in about -13%, whereas between 2020 and 2021, the variation was about 63%.

- The trade in the automotive sector in Indonesia showed a surplus in all years from 2019 to 2021. Both exports and imports fell in 2020 as a result of the global pandemic, which generated limitations and disruptions in economic activities, so impeding the global supply chain and hurting total production. However, in line with the robust output in 2021, both export and import values increased significantly, with a trade balance of USD 1.93 billion. Although 2021 had the highest level of commercial activity in the prior ten years, the trade balance surplus was the lowest in comparison to 2019 and 2020, which had balance values of USD 2 billion and USD 1.95 billion, respectively.

- Globally, the development of EVs signaled a fundamental shift in the Indonesian transportation sector's policies. Given the country's nickel reserves, Indonesia is well-placed to become a major player in the global EV supply chain. To be a part of the region's EV future, Indonesia needs to invest in technology, talent resources, renewable energy, and infrastructure.

Understand The Key Trends Shaping This Market

Download PDF

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Growing demand from civil aviation will likely boost the need for light aircraft

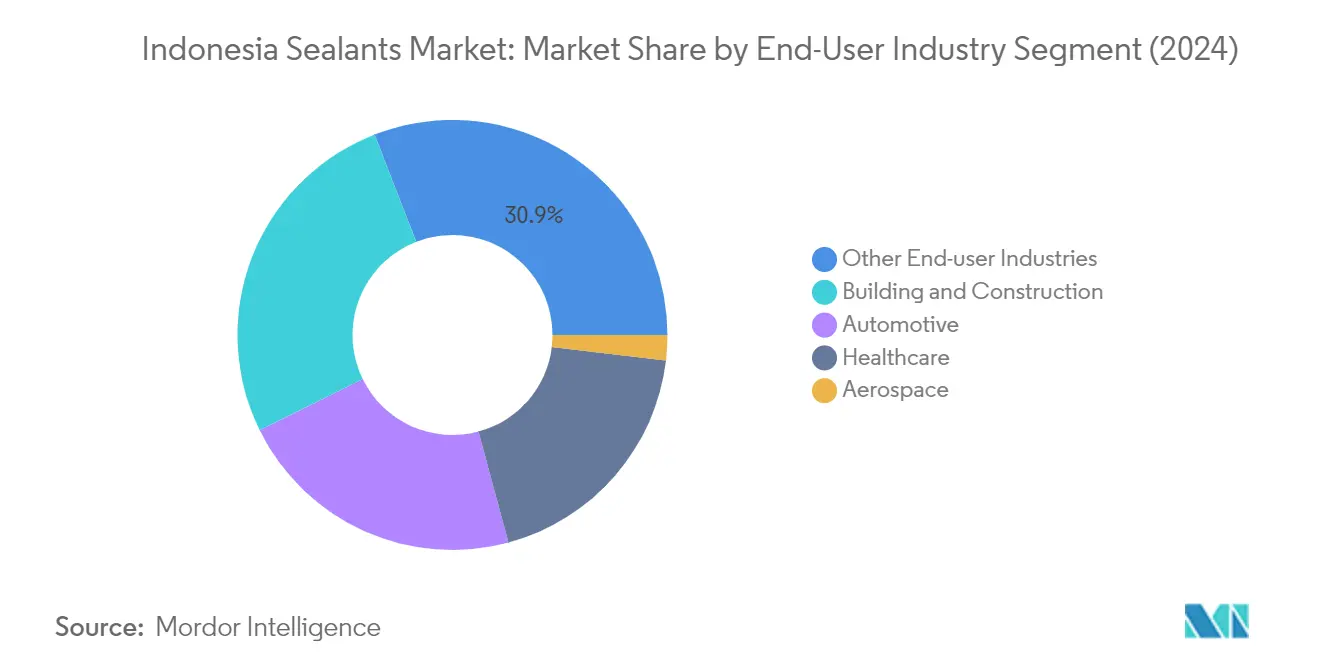

Segment Analysis: End User Industry

Building and Construction Segment in Indonesia Sealants Market

The building and construction segment dominates the Indonesia sealants market, accounting for approximately 26% of the total market value in 2024. This significant market share is driven by the extensive use of construction sealants in various construction applications, including joint sealing, weatherproofing, window sealing, glazing, façade work, and other structural applications. The segment's dominance is further strengthened by Indonesia's robust construction sector, with major infrastructure projects like the development of the new capital city in Borneo and various smart city initiatives driving demand. The versatility of construction sealants, particularly silicone sealants and polyurethane sealants, in providing weatherproofing, waterproofing, and structural bonding solutions has made them indispensable in modern construction practices.

Aerospace Segment in Indonesia Sealants Market

The aerospace segment is emerging as the fastest-growing sector in the Indonesia sealants market, projected to grow at approximately 7% CAGR from 2024 to 2029. This robust growth is primarily driven by Indonesia's ambitious aviation sector expansion plans, with the country positioned to become the fourth-largest air travel market globally by 2030. The increasing demand for specialized aerospace sealants is fueled by their critical applications in aircraft manufacturing, maintenance, repair, and overhaul (MRO) operations. The growth is further supported by the expansion of domestic aircraft production capabilities and the establishment of new aerospace manufacturing facilities in the country. Silicone sealants, in particular, are witnessing high demand due to their superior performance in extreme temperature conditions and excellent adhesion properties required in aerospace applications.

Remaining Segments in End User Industry

The automotive, healthcare, and other end-user industries constitute significant portions of the Indonesia sealants market. The automotive sector utilizes silicone sealants extensively in vehicle assembly, particularly in electric vehicle production, which is gaining momentum due to supportive government policies. The healthcare segment demonstrates steady growth with increasing applications in medical device assembly and surgical equipment manufacturing. Other end-user industries, including electronics, marine, and DIY applications, contribute substantially to the market through diverse applications ranging from electronic component sealing to general industrial maintenance. Each of these segments brings unique requirements and applications, driving innovation in sealant formulations and application technologies.

Segment Analysis: Resin

Silicone Segment in Indonesia Sealants Market

Silicone sealants dominate the Indonesian sealants market, accounting for approximately 47% of the total market value in 2024. These sealants are particularly valued for their versatility and performance characteristics, including their ability to operate across a wide temperature range from 40°F to 100°F. The segment's prominence is driven by its extensive applications in automotive manufacturing, where high-temperature resistance and excellent bonding strength to low surface energy substrates are crucial. In the healthcare sector, silicone sealants are preferred for wound management applications, offering gentle and atraumatic adhesion to the skin while promoting healing. The segment's dominance is further reinforced by its widespread use in construction applications, where its solvent-less nature and low shrinkage characteristics make it ideal for various sealing requirements.

Polyurethane Segment in Indonesia Sealants Market

The polyurethane sealants segment is projected to exhibit the strongest growth in the Indonesian sealants market, with an expected growth rate of approximately 6% during 2024-2029. This growth is primarily driven by its expanding applications in the construction sector, where these sealants are increasingly used for installing skylights and windows, mounting fixtures, sealing gutters, ductwork, and pipe flanges, and forming expansion joints. The segment's growth is further bolstered by the increasing adoption of electric vehicles in Indonesia, with major manufacturers establishing production facilities in the country. Polyurethane sealants are particularly valued in these applications due to their excellent flexibility, durability, and weather resistance properties, making them ideal for both interior and exterior automotive applications.

Remaining Segments in Resin Segmentation

The remaining segments in the Indonesian sealants market include epoxy sealants, acrylic sealants, and other resin-based sealants, each serving specific market niches. Epoxy sealants are valued for their fast curing time and effectiveness in repair applications, particularly in the electronics and automotive sectors. Acrylic sealants have carved out a significant position in construction and DIY applications, offering odorless solutions for household joints and general sealing requirements. Other resin-based sealants, including rubber-based, polyester, and polysulfide variants, contribute significantly to the market by addressing specialized applications across various industries, particularly in high-performance and industrial applications where specific chemical and physical properties are required.

Competitive Landscape

Top Companies in Indonesia Sealants Market

The Indonesian sealants market is characterized by companies focusing heavily on product innovation to maintain their competitive edge, particularly in developing new high-performance sealants for automotive, construction, and industrial applications. Leading manufacturers are emphasizing environmentally friendly solutions, with many companies shifting towards non-toxic and low-VOC content sealant production to align with sustainability trends. Strategic acquisitions of local companies have emerged as a prominent strategy for global players to expand market presence and leverage existing distribution networks. Companies are increasingly specializing in specific business segments to develop expertise and enhance market positioning, while simultaneously investing in research and development to expand their product portfolios. The market also sees significant emphasis on customized solutions and partnerships between global and local players, enabling better service to regional customers while maintaining technological advancement.

Fragmented Market with Strong Local Presence

The Indonesian sealants market exhibits a fragmented structure with a mix of global conglomerates and local specialists competing for market share. Global players like Henkel AG & Co. KGaA, Sika AG, and 3M maintain strong positions through their extensive product portfolios and well-established distribution networks, while local companies such as Dextone Indonesia and IKA Group leverage their market knowledge and customer relationships. The market demonstrates moderate consolidation, with the top five companies collectively holding a significant but not dominant share, indicating healthy competition and opportunities for growth.

The market is characterized by a strong presence of local manufacturers who have maintained their positions through customized solutions and strategic partnerships with global players. These local companies often focus on specific end-user segments or geographical regions, allowing them to build strong customer relationships and respond quickly to market demands. The industry sees regular collaborative ventures between global and local players, combining technological expertise with market knowledge, rather than outright acquisitions, suggesting a preference for partnership-based growth strategies.

Innovation and Distribution Drive Market Success

Success in the Indonesian sealant industry increasingly depends on companies' ability to innovate while maintaining strong distribution networks. Incumbent players must focus on developing environmentally friendly products, expanding their production capabilities, and strengthening their local presence through strategic partnerships. Companies need to invest in research and development to create specialized solutions for specific industries while maintaining cost competitiveness through efficient manufacturing processes. The ability to provide technical support and after-sales service has become crucial for maintaining market position, particularly in high-value applications.

For contenders looking to gain market share, focusing on underserved market segments and developing niche products presents significant opportunities. Companies must build strong relationships with end-users in growing sectors such as construction and automotive, while also investing in local manufacturing capabilities to reduce costs and improve supply chain efficiency. The market shows relatively low substitution risk due to the specific technical requirements of industrial sealants applications, but regulatory compliance, particularly regarding environmental standards, is becoming increasingly important. Success also depends on developing effective distribution channels and maintaining strong relationships with key stakeholders in major end-user industries.

Indonesia Sealants Industry Leaders

-

3M

-

DEXTONE INDONESIA

-

Henkel AG & Co. KGaA

-

Pioneer Adhesives, Inc.

-

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2020: H.B. Fuller Company introduced a new range of Gorilla professional-grade adhesives and sealants for MRO industrial applications.

- April 2019: Dow completed the separation of its Material Science division through a spin-off of Dow Inc.

Indonesia Sealants Market Report Scope

Aerospace, Automotive, Building and Construction, Healthcare are covered as segments by End User Industry. Acrylic, Epoxy, Polyurethane, Silicone are covered as segments by Resin.

End User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Other End-user Industries |

Resin

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

| End User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Other End-user Industries | |

| Resin | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins |

Need A Different Region or Segment?

Customize Now

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF